Heavy-Duty Electric Trucks Market Size, Share & Industry Analysis, By Propulsion Type (Battery Electric Trucks (BEV) and Fuel Cell Electric Trucks (FCEV)), By Range (Less than 300 km, 300-500 km, and More than 500 km), By Battery Capacity (150-300 kWh, 300-600 kWh, and Above 600 kWh), By Application (Long-Haul Transportation, Construction & Mining, Municipal & Utility Services, Logistics & Distribution, and Others), By Ownership Model (Fleet-Owned, Leasing / Rental, and Truck-as-a-Service (TaaS)), and Regional Forecast, 2026-2034

Heavy-Duty Electric Trucks Market Size and Future Outlook

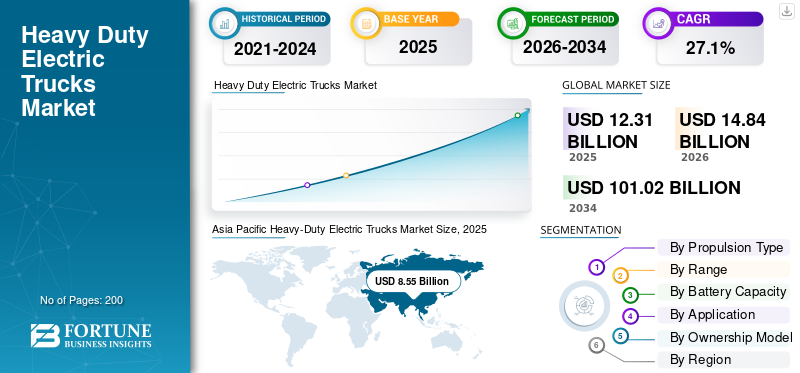

The global heavy-duty electric trucks market size was valued at USD 12.31 billion in 2025. The market is projected to grow from USD 14.84 billion in 2026 to USD 101.02 billion by 2034, exhibiting a CAGR of 27.1% during the forecast period. Asia Pacific dominated the heavy-duty electric trucks market with a market share of 69.45% in 2025.

The global market represents a rapidly evolving segment within the broader commercial vehicles ecosystem, focusing on the electrification of trucks with high gross vehicle weight used for freight transportation. These electric trucks are designed to replace conventional diesel trucks, offering lower CO2 emissions, improved energy efficiency, and reduced environmental impact. The market includes both battery electric vehicle platforms and emerging fuel cell truck technologies, each catering to different operational needs within the trucks industry.

The growth of this market is primarily driven by stringent emission regulations, rising fuel costs, and increasing pressure on fleet operators to reduce their carbon footprint. Governments and regulatory bodies worldwide are promoting electrification through subsidies and mandates targeting heavy duty vehicles, which is accelerating adoption. In addition, improvements in charging infrastructure and the expansion of charging stations are making electric trucks more viable for real-world operations, including long haul trucking.

Another key factor influencing the market expansion is the declining cost of batteries, which directly impacts the total cost of ownership. Fleet operators are increasingly recognizing that electric trucks can offer long-term savings despite higher upfront costs. Moreover, the integration of digital fleet management systems and route optimization tools further enhances operational efficiency.

Looking ahead, trucks are expected to transition steadily toward zero-emission solutions as OEMs invest heavily in new platforms. Key players in the market such as Volvo and Daimler are focusing on partnerships, technology innovation, and large-scale production to strengthen their position and accelerate commercialization.

Download Free sample to learn more about this report.

Heavy-Duty Electric Trucks Market Key Takeaways

- 2025 Market Size: USD 12.31 billion

- 2026 Market Size: USD 14.84 billion

- 2034 Forecast Market Size: USD 101.02 billion

- CAGR: 27.1% from 2026–2034

- Asia Pacific dominated the heavy-duty electric trucks market with a 69.45% share in 2025.

- The FCEV segment is expected to grow at a CAGR of 28.6% over the forecast period.

- The more than 500 km segment is expected to grow at a CAGR of 27.2% over the forecast period.

Asia Pacific

Asia Pacific maintained its dominant position in the market, reaching a valuation of USD 8.55 billion in 2025.

Europe

Europe is expected to become the second-largest regional market, reaching USD 2.16 billion in 2026.

North America

North America is projected to grow at a CAGR of 29.2% during the forecast period and reach USD 1.83 billion by 2026.

U.S.

The U.S. heavy-duty electric trucks market was valued at approximately USD 1.16 billion in 2025, representing around 9.4% of the global market.

Japan

Adoption of heavy-duty electric trucks is expected to increase as fleet operators focus on emission reduction and sustainable transportation.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Stringent Emission Regulations to Accelerate the Adoption of Electric Trucks

Stringent emission regulations aimed at reducing CO2 emissions are significantly driving product adoption, propelling heavy-duty electric trucks market growth. Governments are imposing stricter norms on diesel trucks, encouraging fleet operators to transition toward cleaner alternatives. This shift is expanding the trucks market size, as companies invest in battery electric vehicle and fuel cell truck technologies to comply with environmental mandates.

- For instance, in May 2024, the European Union approved stricter CO2 emission standards for heavy-duty vehicles, mandating significant emission reductions by 2030, accelerating electric truck adoption.

MARKET RESTRAINTS

High Upfront Costs to Limit Large-Scale Adoption

The high initial cost of heavy duty electric trucks compared to diesel trucks remains a key restraint. Despite the lower total cost of ownership over time, the upfront investment required for vehicles and charging infrastructure discourages smaller fleet operators. The limited availability of charging stations further adds to the challenge, slowing adoption across certain regions.

- For instance, in 2024, a report by ICCT (International Council on Clean Transportation) highlighted that electric heavy-duty trucks can cost nearly twice as much as diesel equivalents, limiting adoption among small fleet operators.

MARKET OPPORTUNITIES

Expansion of Charging Infrastructure to Create Growth Opportunities

The rapid development of charging infrastructure and deployment of high-capacity charging stations present significant opportunities for the market. Improved infrastructure supports long-distance operations and enhances feasibility for long haul trucking, increasing adoption across the trucks industry.

- For instance, in 2024, the U.S. government announced funding for nationwide truck charging corridors to support electric heavy-duty vehicles.

MARKET CHALLENGES

Limited Charging Infrastructure in Developing Regions to Restrain Industry Growth

Despite progress, insufficient charging infrastructure in emerging markets remains a major challenge. The lack of widespread charging stations restricts the deployment of heavy duty electric trucks, particularly in remote and long-distance routes, limiting growth potential in the global trucks industry.

- For instance, in 2024, the International Energy Agency (IEA) reported the uneven distribution of truck charging infrastructure globally, with most capacity concentrated in China and Europe.

Segmentation Analysis

By Propulsion Type

Mature Battery Electric Vehicle Technology to Drive BEV Segment Dominance

On the basis of propulsion type, the market is segmented into Battery Electric Trucks (BEV) and Fuel Cell Electric Trucks (FCEV).

The BEV segment dominates the global heavy-duty electric trucks market share due to its maturity, wider availability, and lower operational complexity compared to fuel cell truck solutions. BEVs are well-suited for urban and regional applications, contributing significantly to the trucks market size.

- For instance, in March 2024, Volvo Trucks reported strong demand for its electric truck lineup, with thousands of units delivered globally across logistics and distribution operations.

The FCEV segment is expected to grow at a CAGR of 28.6% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Range

Cost and Performance Balance to Support 300–500 km Segment Dominance

On the basis of range, the market is segmented into less than 300 km, 300-500 km, and more than 500 km.

The 300–500 km range segment dominates the market as it offers an ideal balance between performance and cost. It supports most logistics operations without requiring extremely large batteries, making it suitable for commercial vehicles operating in regional routes.

- For instance, in May 2024, Daimler Truck introduced electric trucks optimized for regional haul applications with ranges around 400 km, targeting logistics operators.

The more than 500 km segment is expected to grow at a CAGR of 27.2% over the forecast period.

By Battery Capacity

Balanced Performance and Cost to Drive 300–600 kWh Segment Leadership

On the basis of battery capacity, the market is segmented into 150-300 kWh, 300-600 kWh, and above 600 kWh.

The 300–600 kWh segment dominates the market due to its ability to support operational needs while maintaining manageable costs. It is widely adopted across multiple vehicle class categories within heavy duty vehicles.

- For instance, in April 2024, Scania launched electric trucks with battery capacities within this range, targeting urban and regional freight applications.

The above 600 kWh segment is expected to grow at a CAGR of 27.9% over the forecast period.

By Application

Rising Freight Movement Demand to Strengthen Logistics & Distribution Segment Leadership

On the basis of application, the market is segmented into long-haul transportation, construction & mining, municipal & utility services, logistics & distribution, and others.

The logistics & distribution segment dominates the market due to the increasing demand for efficient freight movement. Electrification in this segment reduces CO2 emissions while improving efficiency in commercial vehicles operations.

- For instance, in June 2024, Amazon expanded its electric truck fleet in Europe to support sustainable logistics operations.

The long-haul transportation segment is expected to grow at a CAGR of 29.1% over the forecast period.

By Ownership Model

Large Fleet Investments to Drive Fleet-Owned Models Segment Dominance

On the basis of application, the market is segmented into fleet-owned, leasing / rental, and Truck-as-a-Service (TaaS).

The fleet-owned models segment dominates the market as large companies invest directly in electric trucks to optimize the total cost of ownership and gain operational control. This model is common in large logistics operations.

- For instance, in January 2024, Walmart expanded its electric truck fleet to improve sustainability and reduce operational emissions.

The Truck-as-a-Service (TaaS) segment is expected to grow at a CAGR of 27.8% over the forecast period.

Heavy-Duty Electric Trucks Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Heavy-Duty Electric Trucks Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the leading share in 2024, with a value of USD 7.80 billion, and also maintained dominant share in 2025, valuing at USD 8.55 billion. Asia Pacific dominates the market due to strong government support, rapid industrialization, and large-scale adoption in China. The region leads in charging infrastructure deployment and the production of battery electric vehicle technologies. High demand for commercial vehicles and strict emission regulations further drive growth.

- For instance, in 2024 as per the IEA, China accounted for the majority of global electric truck sales, supported by government incentives and infrastructure expansion.

China Heavy-Duty Electric Trucks Market

The China’s market is projected to be one of the largest worldwide, with 2025 revenues touching a value of around USD 7.02 billion, representing roughly 57.0% of global market revenues.

India Heavy-Duty Electric Trucks Market

The India market reached around USD 0.22 billion in 2025, accounting for roughly 1.8% of global revenues.

Europe

The Europe market is estimated to reach USD 2.16 billion in 2026 and secure the position of the second-largest region in the market. The regional market is driven by strict emission regulations and sustainability goals. Countries such as Germany and the U.K. are leading adoption. Investments in infrastructure and policy support are accelerating the transition from diesel trucks to electric alternatives.

Germany Heavy-Duty Electric Trucks Market

The Germany market recorded a value of around USD 0.48 billion in 2025, accounting for roughly 3.9% of global revenues.

U.K. Heavy-Duty Electric Trucks Market

The U.K. market registered a value of around USD 0.31 billion in 2025, accounting for roughly 2.5% of global market revenues.

North America

North America is projected to record a growth rate of 29.2% over the forecast period and reach a valuation of USD 1.83 billion by 2026. North America is witnessing steady growth driven by regulatory support and fleet electrification initiatives. Investments in charging stations and infrastructure are increasing adoption. The U.S. leads the region, supported by strong policy incentives and corporate sustainability goals. The market is still in early stages but shows strong future potential.

U.S. Heavy-Duty Electric Trucks Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market reached a value of around USD 1.16 billion in 2025, representing roughly 9.4% of the global market.

Rest of the World

The rest of the world region is gradually adopting electric trucks, supported by pilot projects and infrastructure development. The market growth is driven by the increasing awareness of sustainability and expansion of the trucks industry into electrified solutions.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Enter Strategic Partnerships to Strengthen Competitive Edge

The competitive landscape of the global market is characterized by rapid innovation, strategic alliances, and aggressive expansion by leading players in the trucks industry. Key manufacturers are focusing on strengthening their portfolios of heavy duty electric trucks by investing in advanced battery electric vehicle platforms and fuel cell truck technologies. Companies are also prioritizing improvements in energy efficiency, vehicle performance, and durability to meet the operational demands of long haul trucking and other heavy-duty applications.

To gain a competitive advantage, players are forming partnerships across the value chain, particularly in charging infrastructure development and hydrogen ecosystems. Collaborations with energy providers and technology firms are enabling faster deployment of charging stations, which is critical for scaling adoption. Additionally, manufacturers are expanding their production capacities and localizing manufacturing to meet region-specific emission regulations and reduce costs.

Another key strategy includes optimizing the total cost of ownership for fleet operators. Companies are offering integrated solutions that combine vehicles, maintenance, financing, and energy services. This approach helps differentiate offerings in a market where upfront costs remain a concern. Digitalization is also playing a vital role, with OEMs integrating telematics and fleet management systems to enhance operational efficiency for commercial vehicles.

Moreover, competitive positioning is influenced by the ability to address multiple vehicle class requirements and varying gross vehicle weight categories. While some players focus on urban and regional applications, others are developing high-capacity solutions targeting heavy-duty segments traditionally dominated by diesel trucks. As trucks market trends shift toward electrification, companies that can balance performance, cost, and infrastructure readiness are expected to lead the market.

LIST OF KEY HEAVY-DUTY ELECTRIC TRUCKS COMPANIES PROFILED

- Volvo Trucks (Sweden)

- Daimler Truck (Germany)

- BYD Company Ltd. (China)

- Tesla Inc. (U.S.)

- Scania AB (Sweden)

- MAN Truck & Bus (Germany)

- PACCAR Inc. (U.S.)

- Hyundai Motor Company (South Korea)

- Isuzu Motors (Japan)

- Hino Motors (Japan)

KEY INDUSTRY DEVELOPMENTS

- October 2025: Hyundai reported that its XCIENT Fuel Cell truck fleet had reached 20 million kilometers in Europe. The milestone supported Hyundai’s case that fuel-cell heavy trucks are now demonstrating real-world durability and commercial readiness in demanding logistics environments.

- June 2025: Daimler Truck, Mitsubishi Fuso, Hino Motors, and Toyota concluded definitive agreements to integrate Mitsubishi Fuso and Hino. The deal aims to combine development, procurement, and production capabilities, potentially creating a stronger Japanese commercial-vehicle group with greater scale for future zero-emission truck technologies.

- May 2025: Volvo formally showed its Volvo FH Aero Electric with e-axle, promising up to 600 km range and charging in about 40 minutes. The truck was positioned as Volvo’s next heavy-duty electric flagship for long-distance transport and a key step toward mainstream zero-emission line-haul operations.

- April 2025: Volvo Trucks delivered more than 5,000 battery-electric trucks across 50 countries. The milestone showed that heavy-duty electric truck adoption is moving beyond pilot stage and into broader commercial deployment across regions and use cases.

- April 2025: Kenworth introduced the next-generation T680E battery-electric truck at ACT Expo 2025. The launch expanded Kenworth’s electric offering for on-highway applications and signaled continued investment by PACCAR brands in the North American heavy-duty EV segment.

- April 2025: Hyundai Motor unveiled the new XCIENT Fuel Cell Class 8 truck at ACT Expo 2025. The company paired the launch with a North America-focused business model and partnerships, reinforcing its ambition to scale hydrogen-based freight transport commercially.

- February 2025: Scania and DHL began testing an electric truck with a fuel-powered range extender for main-carriage transport between Berlin and Hamburg. The project addressed a practical market bottleneck by helping fleets electrify long routes before full charging-network coverage is available.

REPORT COVERAGE

The global heavy-duty electric trucks market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers, and acquisitions. The research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 27.1% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Propulsion Type, Range, Battery Capacity, Application, Ownership Model, and Region |

| By Propulsion Type |

|

| By Range |

|

| By Battery Capacity |

|

| By Application |

|

| By Ownership Model |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 12.31 billion in 2025 and is projected to reach USD 101.02 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 8.55 billion.

The market is expected to exhibit a CAGR of 27.1% during the forecast period of 2026-2034.

The BEV segment leads the market by propulsion type.

Stringent emission regulations is a key factor driving the global market.

Volvo, Daimler, Scania, and MAN Truck & Bus are the top players in the market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us