Human Fibrinogen Concentrates Market Size, Share & Industry Analysis by Application (Congenital Fibrinogen Deficiency, Acquired Fibrinogen Deficiency & Surgical Procedures, and Others), By End-user (Hospitals, Specialty Clinics, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

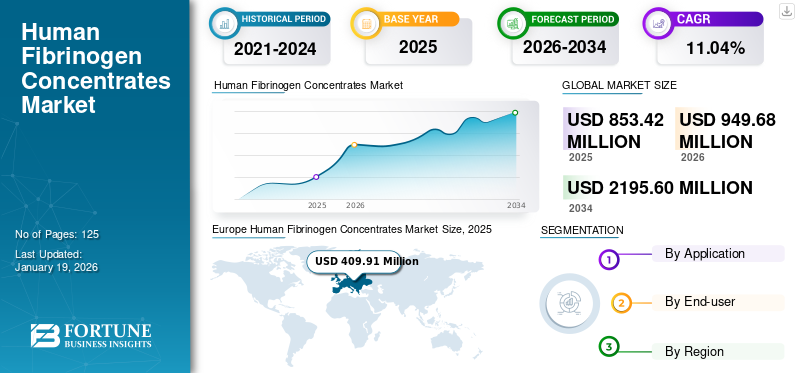

The global human fibrinogen concentrates market size was USD 853.4 million in 2025 and is projected to grow from USD 949.68 million in 2026 to USD 2448.90 million in 2034 at a CAGR of 12.57% during the forecast period. Europe dominated the human fibrinogen concentrates market with a market share of 23.96% in 2025.

Human fibrinogen concentrates are plasma-derived products that rapidly replenish fibrinogen levels in patients experiencing significant bleeding, particularly during surgeries, trauma, or suffering from bleeding disorders such as hyperfibrinogenemia or afibrinogenemia. Deficiency of fibrinogen in the body increases the blood clotting time, thus needing an external measure to support bleeding in deficient patients. Furthermore, the rising prevalence of bleeding disorders, increasing awareness about advanced hemostatic therapies, and technological advancements in plasma fractionation are driving market growth.

- For example, in September 2022, the All India Institute of Medical Sciences (AIIMS) orthopedics division reported that over 250,000 individuals in India underwent total knee replacement surgeries. This high volume of surgical procedures is expected to elevate the demand for related medical products and contribute to the market expansion.

Additionally, the growing adoption of fibrinogen concentrates over traditional blood products due to their safety and efficiency further boosts the product demand. Certain companies present in the market include LFB, Octapharma AG, CSL, and Grifols, S.A. These companies hold critical products in their portfolio, extended research and development capabilities, and are involved in strategic initiatives to amplify their market presence.

- For instance, in February 2024, Grifols, S.A. announced positive results for fibrinogen concentrate (FC) BT524 from Biotest's Phase 3 clinical trial (AdFIrst) for acquired fibrinogen deficiency (AFD).

Download Free sample to learn more about this report.

Human Fibrinogen Concentrates Market Key Takeaways

- 2025 Market Size: USD 853.40 million

- 2026 Market Size: USD 949.68 million

- 2034 Forecast Market Size: USD 2448.90 million

- CAGR: 11.04% from 2026–2034

- Europe dominated the human fibrinogen concentrates market with a 48.03% share in 2025.

- The Acquired Fibrinogen Deficiency & Surgical Procedures segment is projected to account for 92.61% of the market in 2026.

- The Hospitals segment is projected to hold an 83.34% market share in 2026.

North America

North America held 23.96% share in 2025, valued at USD 204.51 million.

Asia Pacific

Asia Pacific held 23.74% share in 2025, valued at USD 202.63 million.

Europe

Europe held 48.03% share in 2025, valued at USD 409.91 million.

U.S.

Market projected to reach USD 225.56 million by 2026.

Japan

Market projected to reach USD 58.31 million by 2026.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Surging Number of Surgical Procedures to Boost Adoption of Fibrinogen Products

The rising prevalence of chronic disorders and trauma cases increases the number of surgical procedures associated with them. Thus, such conditions drive the market demand for advanced hemostatic agents, including fibrinogen concentrate products. The growing number of surgeries across fields such as cardiovascular, neurological, orthopedic, and gynecological disciplines is expected to fuel market growth during the forecast period. Factors contributing to the rise in surgical procedures include an aging population, higher prevalence of various disorders, tobacco use and exposure, physical inactivity, and unhealthy lifestyles.

- For instance, in June 2024, per the data published by the National Institutes of Health, on the “Global Cardiac Surgical Volume and Gaps” report, an average total cardiac surgical volume of 123.2 per 100,000 population per year was performed in high-income countries. This burgeoning volume of surgical procedures further augments the demand for these products.

Moreover, growing demand for reduced operative and postoperative complications in patients with fibrinogen deficiency also bolsters the need for effective products, thus surging the global human fibrinogen concentrates market growth.

MARKET RESTRAINTS

High Cost of Human Fibrinogen Products to Impede Market Growth Prospects

The high cost associated with the fibrinogen products significantly hampers the product adoption in the lower-income regions and restrains the market growth. The high cost is primarily due to complex manufacturing processes, safety requirements, and a stringent regulatory approval process. This limits accessibility and affordability for healthcare providers and patients.

- For instance, per the commercial website, the cost for FIBRINOREL 1g Dried Fibrinogen, 10 ml is around USD 185.4. Such high costs associated with the products may affect their adoption in lower economies.

Furthermore, limited reimbursement policies for the products in emerging areas collectively hamper market expansion.

MARKET OPPORTUNITIES

Strategic Activities between Key Players are Offering Market Growth Opportunities

Strategic activities such as collaborations, mergers, and acquisitions between pharmaceutical companies and biotech firms facilitate the development of advanced fibrinogen products, improving safety and efficacy.

Moreover, the rising number of chronic diseases and surgeries associated with them in developing regions, increased the demand and the focus of key players to develop and launch new products in these regions. Thus, collaborative efforts and joint ventures help penetrate emerging markets and strengthen distribution channels.

- For instance, in June 2024, Plasmagen Biosciences Private Limited collaborated with CSL (CSL Behring) to manufacture and commercialize Haemocomplettan P (Human Fibrinogen Concentrate) in India. Haemocomplettan P is approved for therapy and prophylaxis of hemorrhagic diatheses in congenital afibrinogenaemia and acquired hypofibrinogenaemia. Such collaborations, partnerships to launch their key products in the untapped market, is offering a lucrative opportunity for the market to grow during the forecast period.

MARKET CHALLENGES

Supply Chain Disruption to Impede Market Growth

The manufacturing of human fibrinogen concentrates is tedious work. It involves the need for extensive donor networks, large-scale collection facilities, strict testing, and maintaining cold chain logistics, which can limit the entry of new entrants in the market.

Additionally, the need for highly skilled personnel to manage batch release, documentation, and audits makes quality assurance and regulatory compliance a high barrier, and thus challenges the product production and market growth.

HUMAN FIBRINOGEN CONCENTRATES MARKET TRENDS

Emerging Pipeline Products to Act as a Key Industry Trend in Market

Traditionally, the market has heavily relied on cryoprecipitate as the primary source of fibrinogen, but this approach presents several limitations. Cryoprecipitates are made from pooled plasma and require thawing and preparation before administration, thus delaying urgent treatment during trauma or surgeries.

Thus, such challenges increased the focus of key players to develop and launch advanced products to offer more reliable, standardized, and safe alternatives in clinical applications.

- For instance, in June 2025, Grifols, S.A. announced positive results from their Phase 3 study on BT524, a fibrinogen concentrates. The study assessed the effectiveness and safety of BT524 in managing acquired fibrinogen deficiency (AFD) during major surgeries. The results showed that BT524 successfully met its primary goal by demonstrating non-inferiority to standard treatments such as cryoprecipitate and fresh-frozen plasma (FFP) in controlling bleeding during surgery. BT524 addressed existing challenges by offering a concentrated, standardized fibrinogen dose that can be administered quickly without thawing. This enhances efficiency, predictability, and allows for patient-specific dosing. By improving response times and dosing precision, BT524 can significantly improve clinical outcomes in situations requiring rapid bleeding control.

Such advancements in product development are expected to offer significant global human fibrinogen concentrates market trends.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Application

Increasing Number of Surgeries to Boost Acquired Fibrinogen Deficiency & Surgical Procedures Segment's Growth

Based on application, the market is divided into congenital fibrinogen deficiency, acquired fibrinogen deficiency & surgical procedures, and others.

The acquired fibrinogen deficiency & surgical procedures segment is poised to account for 92.61% of the market share in 2026. The largest share of the segment is due to a rise in the number of cases of acquired fibrinogen deficiency and an increasing number of surgeries, trauma cases, which further drives the demand for fibrinogen concentrates in surgical settings.

- For instance, according to the data published by the Australian Institute of Health and Welfare, in the year 2020-2021, 12,700 coronary artery bypass grafting (CABG) surgical procedures were performed in Australia. Such a large number of surgeries in one region increases the need for adequate hemostatic agents to decrease the blood loss, thus bolstering the segment’s growth in the market.

Congenital fibrinogen deficiency held the market's second-largest share of the segment, and is expected to grow with a moderate CAGR over the forecasted timeframe. The rise in prevalence of fibrinogen deficiency disorders augments the segment's growth. The increase in research and development activities and funding initiatives by key operating players also supports the global market growth.

- For example, as per the data published by Orphanet, the prevalence of afibrinogenemia is estimated to be in the range of 1 to 30 cases in 1 million individuals. This leads to increased demand for fibrinogen concentrates to avoid excessive bleeding in patients and maintain their quality of life.

To know how our report can help streamline your business, Speak to Analyst

By End-user

High Surgical Procedures Case Load in Hospitals to Augment Segment’s Market Dominance

In terms of end-user, the global market can be segmented into specialty clinics, hospitals, and others.

On the basis of end-users, the hospitals segment is projected to dominate the market with a share of 83.34% in 2026. The segment's high share is due to the large volume of surgeries and use of fibrinogen concentrates as agents for bleeding control during various surgical procedures. Additionally, technologically superior infrastructure and expertise afforded by hospitals support a large number of surgical procedures, which contributes to the segmental growth.

- For instance, in September 2023, as per the WHO, the global volume of surgical procedures exceeded 300 million annually. Such a large number of surgeries is expected to boost the growth of the segment in the market.

The specialty clinics segment emerged as the second largest segment, owing to the increased number of specialty clinics in developing countries. Further, the presence of skilled professionals with advanced facilities to propel the segment’s growth in the market.

The others segment accounted for a considerably limited market share. The adoption of these products in the research institutes and healthcare research organizations to develop and launch new products substantially bolstered the market segment growth.

HUMAN FIBRINOGEN CONCENTRATES MARKET REGIONAL OUTLOOK:

In terms of region, the global market can be divided into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Europe

Europe Human Fibrinogen Concentrates Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

Europe contributed 48.03% to the global market in 2025, with a valuation of USD 409.91 million, and is projected to reach USD 452.6 million in 2026. The dominant share of the region is due to the presence of key market players with advanced product offerings, the increasing number of surgeries, and the rising prevalence of inherited blood disorders. The UK market is projected to reach USD 68.09 billion by 2026, while the Germany market is projected to reach USD 109.58 billion by 2026.

- For instance, in November 2019, Octapharma AG approved Fibryga to treat acquired fibrinogen deficiency (AFD) in 15 European countries.

North America

The North America market generated USD 204.51 million in 2025, representing 23.96% of the global market landscape, and is expected to reach USD 233.98 million in 2026. The country's growth is due to an increasing number of patients with blood disorders and a well-established healthcare infrastructure. Additionally, increasing the focus of key players to receive critical regulatory approvals for fibrinogen products will propel the country's market growth. The U.S. market is projected to reach USD 225.56 billion by 2026.

- For instance, in May 2024, according to the data published by the Centers for Disease Control and Prevention, approximately 33,000 males in the U.S. are estimated to have hemophilia. Such a rising number of cases increases the demand for active hemostatic agents and thus propels the market growth.

Asia Pacific

Asia Pacific accounted for USD 202.63 million in 2025, representing 23.74% of the global market share, and is projected to reach USD 224.17 million in 2026. Factors such as an aging population, lifestyle changes, and a rising prevalence of chronic diseases are anticipated to increase patient visits to hospitals across the region. Additionally, active participation from government and private insurance providers offering surgery reimbursement and increasing collaborations to boost the healthcare facilities is expected to accelerate market growth. The Japan market is projected to reach USD 58.31 billion by 2026, the China market is projected to reach USD 105.93 billion by 2026, and the India market is projected to reach USD 23.56 billion by 2026.

- For instance, in December 2024, UK health experts launched the 100-4-100 Project, a global initiative to raise USD 100.0 million to equip 100 hospitals in India and the global South with improved healthcare infrastructure and operational capabilities. This campaign will probably increase the demand for products used in surgical procedures.

Latin America and Middle East & Africa

Latin America contributed approximately USD 21.18 million to the global market in 2025, accounting for 2.48% share, and is expected to reach USD 22.56 million in 2026. In 2025, Middle East & Africa held 1.78% of the global market, reaching a valuation of USD 15.18 million, and is projected to grow to USD 16.38 million in 2026. The increasing number of activities for maintaining bleeding disorders and rising expenditures on healthcare are expected to augment the market growth in these regions during 2026-2034.

- For example, in June 2020, the UAE Hemophilia Group organized a seminar to spread awareness of the challenges affecting bleeding disorder patients. Such programs are expected to propel the market's growth in the region.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Strong Strategic Activities and Robust Product Offering to Maintain Dominance in Market

This market holds a consolidated structure with players such as Octapharma AG, CSL, and LFB accounting for a substantial share in 2024. Octapharma AG held a leading position in the market due to the presence of key products and an expanded focus on regulatory approvals to launch new products to strengthen its positions globally.

Other key players with an important presence in the global market include Grifols S.A., Shanghai RAAS Blood Products Co., Ltd., and the emerging player. The company’s strategic alliances and focus on offering new products are favoring its growth in the market.

LIST OF KEY HUMAN FIBRINOGEN CONCENTRATES COMPANIES PROFILED

- Grifols, S.A. (Spain)

- Shanghai RAAS Blood Products Co., Ltd. (China)

- CSL (Australia)

- LFB (France)

- Reliance Life Sciences (India)

- China Resources Boya Biopharmaceutical Group Co., Ltd. (China)

- Octapharma AG (Switzerland)

KEY INDUSTRY DEVELOPMENTS

- July 2025: Octapharma AG is supporting a USD 29.0 million national clinical trial led by the University of Colorado Anschutz Medical Campus to investigate if early fibrinogen replacement can improve outcomes for trauma patients with severe bleeding.

- October 2024: LFB launched the state-of-the-art manufacturing facility at the Arass site to triple the bioproduction capacities for immunoglobulin, albumin, and fibrinogen.

- December 2022: CSL announced the opening of a new plasma fractionation facility in Australia. This plasma fractionation facility can develop products for the immune system, bleeding disorders, burns, and other critical medical conditions.

- April 2022: Grifols, S.A. acquired Biotest AG, a European healthcare company specializing in innovative hematology and clinical immunology, to boost innovation and expand its product portfolio in plasma products.

- February 2019: LFB unveiled its strategic transformation project to refocus on core business activities, which included the development of a new indication of FibCLOT for patients with fibrinogen deficiency related to severe post-traumatic hemorrhage.

REPORT COVERAGE

The global market analysis focuses on key aspects, such as market drivers, restraints, opportunities, and trends. The research report also includes a detailed global human fibrinogen concentrate market analysis of the human fibrinogen industry technology status and trends, industry entry barriers (financial, technical, talent, and brand), consumer preference analysis, and industry policies and regulations. Moreover, the report covers the impact of the regional situation on human fibrinogen industries, the impact of U.S. Reciprocal Tariffs on the Industry, and others. Furthermore, the report comprises a detailed regional analysis and segmental analysis.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 12.57% from 2026-2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Application

|

|

By End-user

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 853.42 million in 2025 and is projected to reach USD 2,195.60 million by 2034.

In 2025, the market value in Europe stood at USD 409.91 million.

Registering a CAGR of 11.04%, the market will exhibit steady growth over the forecast period.

Based on application, the acquired fibrinogen deficiency & surgical procedures segment is expected to lead this market during the forecast period.

The increasing incidence of bleeding disorders and rising volume of surgical procedures are the major factors driving the market's growth.

Octapharma AG, LFB, and CSL are some of the major players in the global market.

Europe dominated the human fibrinogen concentrates market with a market share of 23.96% in 2025.

The increasing number of collaborations and new product launches is expected to drive the growth and adoption of the products.

- 2021-2034

- 2025

- 2021-2024

- 125

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us