Hypersonic Flight Market Size, Share & Industry Analysis, By End User (Space Agencies, Military & Defense, and Commercial), By Vehicle Type (Military Aircraft/Missiles, Spaceplanes, and Passenger/Commercial Aircraft), By Component (Propulsion Systems, Sensors & Avionics, and Aerostructures & Others), By Propulsion Technology (Scramjet Engines, Combined Cycle Engines, and Rocket Engines & Others), and Regional Forecast, 2026-2034

Hypersonic Flight Market Size and Future Outlook

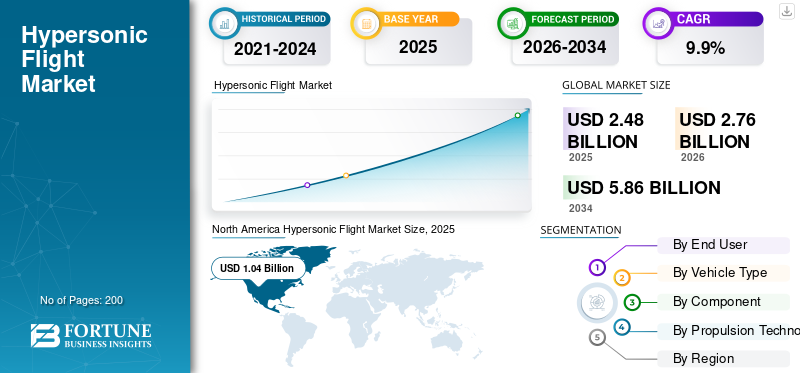

The global hypersonic flight market size was valued at USD 2.48 billion in 2025. The market is projected to grow from USD 2.76 billion in 2026 to USD 5.86 billion by 2034, exhibiting a CAGR of 9.9% during the forecast period. North America dominated the hypersonic flight market with a market share of 41.94% in 2025.

The global hypersonic flight market is experiencing robust growth, driven by escalating defense investments and rapid advancements in propulsion technologies such as scramjet and dual-mode ramjet engines. Governments and private aerospace firms are intensifying research into hypersonic missiles, glide vehicles, and next-generation aircraft capable of exceeding Mach 5. Strategic collaborations between defense agencies such as DARPA and industry leaders are accelerating prototype development and deployment timelines. Growing geopolitical tensions continue to push nations toward hypersonic capabilities as a cornerstone of modern defense doctrine. Simultaneously, commercial prospects in ultra-fast intercontinental travel are emerging, signaling long-term diversification of the market beyond military applications.

Key players in the market include Lockheed Martin, Northrop Grumman, Boeing, Korea Aerospace Industries, and Aerojet Rocketdyne. These companies compete through advanced propulsion system development, cutting-edge thermal protection technologies, precision guidance integration, and mission-specific hypersonic vehicle solutions designed for defense, strategic strike, surveillance, space access, and rapid-response operations. Their efforts are reinforced by strong government contracts, dedicated R&D investments, and strategic partnerships with defense agencies, enabling them to push the boundaries of speed, range, and operational reliability across global hypersonic programs.

Download Free sample to learn more about this report.

HYPERSONIC FLIGHT MARKET TRENDS

Accelerating Innovation in Hypersonic Propulsion and Reusability is a Key Market Trend

The market is witnessing accelerating research into advanced propulsion technologies, such as scramjet engines and dual-mode ramjets, for sustained high-speed cruise and improved fuel efficiency. Partnerships between aerospace companies and organizations such as NASA drive testing of supersonic prototypes toward hypersonic capabilities. Emphasis is growing on reusable vehicles, lightweight, thermally resistant materials, and integration into defense strategies, with North America leading through substantial investments by firms such as Boeing and Lockheed Martin. Commercial interest emerges in rapid intercontinental travel alongside military strikes.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Geopolitical Tensions and Rising Defense Budgets Fuel Market Growth

Rising demand from military applications drives development, as hypersonic systems offer unmatched speed and precision in missile delivery to achieve strategic superiority. Escalating geopolitical tensions spur investments amid a global arms race, with nations prioritizing these capabilities in defense doctrines. Technological progress in propulsion, materials, and avionics, coupled with surging defense budgets, fuels innovation. Strategic alliances between governments, agencies such as DARPA, and industry leaders accelerate prototyping and deployment. This is fueling the hypersonic flight market growth.

MARKET RESTRAINTS

High Costs and Stringent Regulations Slowing Commercialization Limits Market Growth

High development costs for research, production, and testing limit accessibility and slow commercialization, straining manufacturers and investors. Expensive materials and infrastructure needs exacerbate affordability issues. Regulatory approvals require rigorous safety validations under extreme conditions, which delay timelines. These financial and compliance burdens hinder widespread adoption despite technological promise.

MARKET OPPORTUNITIES

Technological Advancements Unlocking Defense, Commercial, and Space Frontiers Generate New Market Growth Opportunities

Hypersonic technologies offer transformative potential for defense, including missile systems, rapid troop deployment, and superior strike capabilities, benefiting contractors such as Lockheed Martin. Commercial aviation sees opportunities to slash intercontinental travel times, while space access improves through enhanced propulsion and manufacturing innovations. Material suppliers and startups gain from advancements in heat-resistant composites. Evolving regulations and maturing tech position both defense and civilian sectors for lucrative expansion through global collaborations.

MARKET CHALLENGES

Technical Complexity and Infrastructure Gaps Impeding Scalability

Technological complexities in propulsion reliability for speeds beyond Mach 5 pose core hurdles, alongside extreme heat management that risks component failure. Aerodynamic stability, fuel efficiency, and structural integrity at hypersonic velocities require ongoing breakthroughs. Integrating into existing airspace lacks tailored regulations for safety, sonic booms, and emissions. Skilled workforce shortages and infrastructure gaps further complicate operational scalability.

Segmentation Analysis

By End User

Deterrence Priorities and Precision-Strike Requirements to Fuel Military & Defense Segment Growth

Based on end user, the market is segmented into space agencies, military & defense, and commercial.

The military & defense segment is anticipated to account for the largest hypersonic flight market share. Military and defense demand is rising as hypersonic is still treated first as a strategic combat capability, not a civil aerospace product. Governments are funding strike reach, survivability, rapid response, and heavily defended target penetration, which keeps procurement, testing, integration, and subsystem investment concentrated within defense programs.

The commercial segment is anticipated to rise with a CAGR of 10.2% over the forecast period.

By Vehicle Type

Operational Strike Utility Led to Dominance of Military Aircraft/Missiles

Based on vehicle type, the market is segmented into military aircraft/missiles, spaceplanes, and passenger/commercial aircraft.

In 2025, the military aircraft/missiles segment dominated the global market. Demand for military aircraft and missiles is rising as armed forces want prompt, survivable strike options that can be launched from land, sea, or air. Most real funding still flows into weaponized delivery systems and operational missile tracks, while passenger hypersonic concepts remain experimental, capital-intensive, and commercially distant.

The spaceplanes segment is projected to grow at a CAGR of 10.9% over the forecast period.

By Component

Propulsion Bottlenecks to Foster Stronger Demand for Propulsion Systems

Based on component, the market is segmented into propulsion systems, sensors & avionics, and aerostructures & others.

The propulsion systems segment is anticipated to witness a dominating market share over the forecast period. Demand for propulsion systems is rising as propulsion still determines speed, range, thermal endurance, and mission reliability. Scramjets, combined-cycle architectures, boosters, cooling systems, fuel management, and test hardware draw outsized funding since propulsion maturity remains one of the biggest barriers between laboratory progress and repeatable operational hypersonic performance.

The aerostructures & others segment is projected to grow at a high CAGR of 9.7% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Propulsion Technology

Near-Term Practicality and Test Needs Supported Rocket Engines & Others Segment Growth

Based on propulsion technology, the market is segmented into scramjet engines, combined cycle engines, and rocket engines & others.

The rocket engines & others segment dominated the market share. Demand for rocket engines and related propulsion hardware is rising as many current systems still need booster stages, launch assistance, or proven high-energy propulsion for demonstrators and near-term weapons. They remain the practical option where air-breathing maturity is incomplete, mission duration is shorter, or space-linked flight profiles are involved.

Combined cycle engines are projected to grow at a CAGR of 10.3% during the study period.

Hypersonic Flight Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and the Rest of the World.

North America

North America Hypersonic Flight Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, at USD 0.94 billion, and maintained the leading share in 2025, at USD 1.04 billion. North America leads demand, with the U.S. still funding and testing common hypersonic missiles while AUKUS-linked cooperation expands allied flight testing. Spending remains strongest in propulsion, integration, testing infrastructure, and mission systems.

U.S. Hypersonic Flight Market

Given North America’s strong contribution and the U.S. dominance in the region, the U.S. market can be estimated at around USD 1.09 billion in 2026, accounting for roughly 9.5% of global sales. U.S. demand remains the highest as the Pentagon continues testing and fielding common hypersonic missiles, while broader defense spending remains unmatched globally. Demand is centered on propulsion, integration, guidance, manufacturing readiness, and flight testing.

Europe

Europe is estimated to reach USD 0.63 billion in 2026 and secure its position as the third-largest region in the market. Europe’s demand is gaining momentum as lessons from the Russia-Ukraine war, rearmament, and new U.K.-European long-range strike cooperation are driving hypersonic work higher. Demand is strongest in demonstrators, propulsion, materials, and missile-defense response layers.

U.K. Hypersonic Flight Market

The U.K. market in 2026 is estimated at around USD 0.11 billion, representing a roughly 11.8% CAGR of global sales. U.K. demand is rising as London is using both national funding and allied cooperation to accelerate hypersonic work.

Germany Hypersonic Flight Market

Germany’s market is projected to reach approximately USD 0.07 billion in 2026. Germany’s demand appears more collaborative than standalone, driven by Europe’s wider rearmament cycle and joint long-range strike work with allies. Near-term demand is expected to be more in industrial participation, systems integration, materials, and defense support.

Asia Pacific

Asia Pacific is projected to grow at 10.1% during the forecast period, the second-highest among all regions, and reach a valuation of USD 0.82 billion by 2026. Asia Pacific demand is rising fast as China, India, and Japan all expand offensive or defensive hypersonic programs. The region is seeing demand across missiles, glide vehicles, scramjets, interceptors, sensors, and testing infrastructure.

China Hypersonic Flight Market

China’s market is projected to be one of the largest in Asia Pacific, with 2026 revenues estimated at around USD 0.48 billion. China remains one of the strongest demand centers, as the PLA already fields operational systems and, according to the U.S. DoD, has the world’s leading hypersonic missile arsenal. That keeps demand elevated across missiles, propulsion, and production.

Japan Hypersonic Flight Market

The Japan market share in 2026 is estimated at around USD 0.10 billion, accounting for roughly 9.6% CAGR during the forecast period. Japan’s demand is accelerating through HVGP development, early deployment of stand-off missiles, and U.S.-Japan Glide Phase Interceptor cooperation. Spending is flowing into missiles, interceptors, radars, networks, and a wider integrated air-and-missile defense architecture.

India Hypersonic Flight Market

The Indian market in 2026 is estimated at around USD 0.14 billion. India’s demand is climbing as DRDO moves from technology demonstration toward missile and scramjet milestones. Recent flight and ground-test progress is pulling demand toward propulsion, thermal management, materials, guidance, and eventual weaponization.

Rest of the World

The rest of the world includes the Middle East & Africa and Latin America. These regions are expected to witness moderate growth in this market space during the forecast period. The Middle East & Africa and Latin America markets are set to reach valuations of USD 0.12 billion and USD 0.05 billion, respectively, in 2026. The rest of the world remains smaller, but demand is building as missile threats intensify. Middle Eastern security pressures support selective interest, while Latin America remains limited by budgets, program scale, and industrial depth.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players are Focusing on Propulsion, Rapid Prototyping, and Integrated Defense Architectures to Boost Market Growth

The strongest market-shaping strategies are coming from companies that are trying to shorten the path from hypersonic R&D to usable military capability. Lockheed Martin is pushing rapid weaponization through ARRW flight-test work, the Mako missile, and new propulsion collaborations with GE, while Northrop Grumman is focusing on scramjet propulsion, solid motors, and air-breathing weapon integration. RTX is advancing both offensive and defensive layers through HACM, HALO, and glide-phase interceptor work, and Aerojet Rocketdyne is helping scale the propulsion backbone with scramjets, ramjets, solid motors, and manufacturing-focused hypersonic production methods. Boeing’s contribution is more enabling than dominant, through Phantom Works hypersonic R&D, strike-platform integration, and missile-defense systems that can help counter advanced threats.

LIST OF KEY HYPERSONIC FLIGHT COMPANIES PROFILED

- Lockheed Martin (U.S.)

- Northrop Grumman (U.S.)

- Boeing (U.S.)

- Raytheon Technologies (U.S.)

- Airbus (France)

- General Dynamics (U.S.)

- Thales Group (France)

- Korea Aerospace Industries (South Korea)

- Aerojet Rocketdyne (U.S.)

- SpaceX (U.S.)

KEY INDUSTRY DEVELOPMENTS

- March 2026: Rocket Lab secured a USD 190 million contract to perform 20 hypersonic test flights for the U.S. Department of Defense's MACH-TB 2.0 program.

- February 2026: The Joint Hypersonics Transition Office (JHTO) awarded six contracts to accelerate technologies exceeding Mach 5. Selected companies included Leidos, GoHypersonic, Special Aerospace Services, Purdue Applied Research Institute, Halo Engines, and Kratos.

- February 2026: The U.K. Ministry of Defence awarded Amentum an "Industry Mission Partner" contract to develop sovereign hypersonic strike capabilities under AUKUS.

- February 2026: Polaris won a BAAINBw contract to develop the AURORA spaceplane, a reusable hypersonic test vehicle.

- October 2025: A S. startup Castelion, secured contracts to integrate its "Blackbeard" hypersonic weapon with U.S. Army HIMARS launchers.

REPORT COVERAGE

The global hypersonic flight market research offers a detailed analysis of emerging trends and rapidly adopted technologies across key regions. The report outlines key drivers of market growth and challenges to expansion, delivering a detailed overview of the industry landscape. The study highlights recent advancements to boost industry insights and support stakeholders in making well-informed decisions.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 9.9% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By End User, By Vehicle Type, By Component, By Propulsion Technology, and Region |

| By End User |

|

| By Vehicle Type |

|

| By Component |

|

| By Propulsion Technology |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 2.48 billion in 2025 and is projected to reach USD 5.86 billion by 2034.

In 2025, the market value in North America stood at USD 1.04 billion.

The market is expected to exhibit a CAGR of 9.9% during the forecast period of 2026-2034.

By end user, the military & defense segment is expected to dominate the market.

Geopolitical tensions and rising defense budgets fuel market growth.

Lockheed Martin, Northrop Grumman, Airbus, General Dynamics, and Thales Group are a few major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us