India Medical Devices Market Size, Share & Industry Analysis, By Type (Orthopedic Devices, Cardiovascular Devices, Diagnostic Imaging, In-vitro Diagnostic (IVD), Minimally Invasive Surgery Devices (MIS), Wound Management, Diabetes Care Devices, Ophthalmic Devices, Dental Devices, Nephrology Devices, General Surgery, and Others), By End-user (Hospitals & ASCs, Clinics, and Others), and Country Forecast, 2026-2034

KEY MARKET INSIGHTS

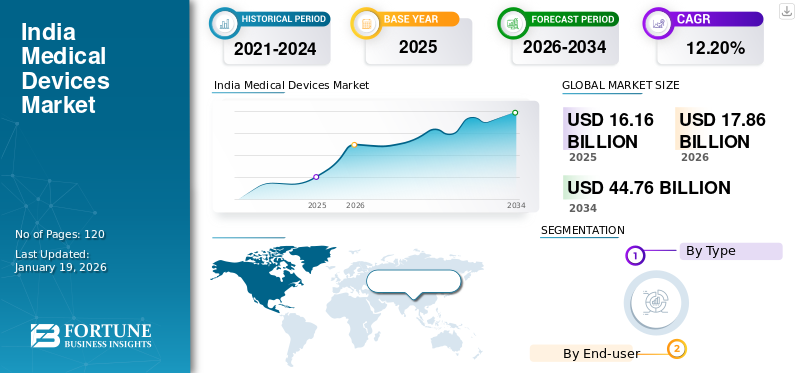

The India medical devices market size was valued at USD 16.16 billion in 2025 and is projected to grow from USD 17.86 billion in 2026 to USD 44.76 billion by 2034, exhibiting a CAGR of 12.20% during the forecast period.

Medical devices include tools and equipment for diagnosis, monitoring, and treatment of medical conditions such as cardiovascular defects, diabetes, trauma & injuries, tumors, and more. Some of these devices include blood pressure monitors, drug delivery devices, diagnostic imaging systems, thermometers, in-vitro diagnostics, fixation devices, dental devices, and others.

The India market is witnessing significant growth due to key factors such as the rising prevalence of chronic diseases and traumatic injuries, which are driving the need for diagnosis and intervention, spurring the adoption of associated medical devices. Moreover, the growing demand for early diagnosis of medical conditions is also expected to propel the use of these devices during the forecast period.

Medtronic, Johnson & Johnson Services, Inc., and GE Healthcare are major players operating in the India market. These players are implementing various growth strategies such as signing collaborations, launching new products, and expanding production capacities to gain a significant share of the India market.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Rising Burden of Chronic Diseases and Aging Population to Fuel Market Growth

In India, there has been a considerable rise in the aging population over the past few years, and it is expected to witness significant growth in the coming years. For instance, according to the data published by the United Nations Population Fund (UNFPA) in September 2023, the population of individuals aged more than 80 years is projected to increase at a rate of around 279.0% between 2022 and 2050 in India.

Such a rise in the aging population prone to chronic medical conditions is increasing the prevalence of chronic diseases such as cardiovascular abnormalities, cancer, and diabetes, which is expected to increase the demand for diagnostic and intervention devices.

- For instance, according to the data from the International Diabetes Federation, India has the second-highest number of diabetic adults (20-79 years) in the world, with 89.8 million cases in 2024, which is expected to rise to 156.7 million by 2050.

Moreover, there is an increasing need for devices such as diagnostic imaging systems, cardiac monitors, insulin pumps, and others, which is attracting international players to expand their footprint in India. This is expected to increase the product availability and drive the India medical devices market growth in the forthcoming years.

Market Restraints

Limited Penetration of Advanced Devices to Hamper Market Growth

Despite rapid technological advancements, India is facing a lower adoption rate of several advanced medical instruments, including surgical robots and high-end imaging systems such as magnetic resonance imaging (MRI) systems, computed tomography (CT) scanners, positron emission tomography (PET) scanners, ultrasound scanners, and point-of-care testing devices.

- For instance, according to the data from the Ministry of Science & Technology, India, in August 2023, India had only a total of 4,800 installed bases of MRIs, which is considerably lower.

This limited adoption rate is mainly due to the high initial costs and ongoing maintenance costs of this advanced equipment, which is deterring healthcare providers, especially in tier-III cities and rural areas, from investing such higher amounts. Moreover, the public healthcare facilities in these areas are facing limited funding, which is further expected to limit the adoption of advanced devices. Moreover, the limited awareness of advanced diagnostic technologies among the rural population, limited reimbursements, and infrastructure in these areas are also restricting the installation of advanced equipment, which is expected to hamper the market growth during the forecast period.

Market Opportunities

Expansion of Healthcare Infrastructure and Medical Tourism to Offer Lucrative Growth Opportunity

In recent years, there has been an increasing healthcare spending favored by government initiatives and the population, which is driving the demand for advanced imaging, diagnostics, consumables, and surgical instruments in India. The government is increasingly investing in developing healthcare infrastructure in the country. Also, the government is focusing on expanding insurance services for low-income families, which is expected to increase the volume of diagnoses and interventions in these areas, thereby demanding advanced equipment.

- For instance, according to the data by the Government of India’s Press Information Bureau in September 2024, the Ayushman Bharat Pradhan Mantri Jan Arogya Yojana (AB PM-JAY) is providing access to high-frequency and low-cost life-saving procedures, such as dialysis, for low-income families to alleviate financial burdens.

Also, the affordability of certain medical procedures, such as dental procedures, cosmetic procedures, and orthopedic procedures, is attracting individuals globally to get their procedures done in India. This rising medical tourism is demanding the development of advanced healthcare facilities, equipped with cutting-edge equipment. Such a scenario is expected to offer lucrative opportunities for prominent players to introduce their devices in the India market, supporting market expansion during the forecast timeframe.

Market Challenges

Shortage of Skilled Professionals to Challenge Market Growth

The introduction of advanced medical devices has surged the demand for highly trained professionals to operate, maintain, and manage these devices. However, India is currently facing a significant shortage of skilled professionals such as surgeons, clinical technicians, and radiologists, particularly in Tier III cities and rural areas, as the healthcare infrastructure is still developing in these areas.

- For instance, according to the data published by the International Journal of Health Technology and Innovation in November 2024, India had only 20,000 radiologists for a 1.4 billion population, which is significantly less compared to Western countries.

This shortage is affecting the system's operation, thereby resulting in delays of certain procedures. This is leading to underutilization of advanced technologies such as AI-powered diagnostics, robotic surgery, and other equipment, which is anticipated to challenge the market expansion during the projection period.

India Medical Devices Market Trends

Increasing Adoption of Wearable and Implantable Devices is a Key Market Trend

Currently, there is a growing awareness of health and fitness due to a higher burden of chronic diseases such as diabetes, cardiovascular diseases, and hypertension in India. This is driving the demand for continuous monitoring of health conditions, ultimately propelling the use of wearable medical devices. As a result, the popularity of continuous glucose monitors (CGM), fitness trackers, smartwatches, and ECG monitors is rising in the country. This continuous monitoring allows for early detection of health conditions, thereby facilitating timely interventions. In response, the key players are increasingly launching such products in India, boosting the product availability.

- For instance, in June 2025, Tracky launched India’s first Bluetooth-enabled Continuous Glucose Monitor (CGM) to transform diabetes care and preventive health management across India.

Moreover, the demand for implantable devices such as pellets, cardiac pacemakers, cochlear implants, neurostimulators, and insulin pumps is increasing due to their ability to provide significant benefits therapeutically. Also, the innovations in minimally invasive procedures are increasing the acceptance of implantable technologies.

Download Free sample to learn more about this report.

Segmentation Analysis

By Type

In-vitro Diagnostics (IVD) Segment Dominated Market Due to Increasing Need for Early Diagnosis

Based on type, the market is segmented into orthopedic devices, cardiovascular devices, diagnostic imaging, in-vitro diagnostic (IVD), minimally invasive surgery devices (MIS), wound management, diabetes care devices, ophthalmic devices, dental devices, nephrology devices, general surgery, and others.

The others segment is anticipated to hold a dominant market share of 31.30% in 2026. The growth is attributed to the increasing adoption of routine monitoring, drug delivery, and home health management devices for chronic diseases such as asthma, hormonal deficiencies, rheumatoid arthritis, and others. As a result, key players are entering the India market to increase their product supply and expand presence in the country.

- For instance, in March 2025, Aerogen Ltd. opened its India headquarters in New Delhi to expand access to its vibrating mesh nebuliser technology and support local respiratory care innovation.

The in-vitro diagnostic (IVD) accounted for the second-largest market share in 2025. This share is attributed to the increasing need for early and accurate diagnosis of chronic and infectious conditions, including cancer, tuberculosis, dengue, and others in India, which is boosting the demand for IVD solutions. Moreover, an increasing number of independent and hospital-based laboratories are also expected to drive the demand for in-vitro diagnostics over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By End-user

Hospitals & ASCs Dominated Due to Established Infrastructure and Higher Utilization of Advanced Technologies

Based on end-user, the market is segmented into hospitals & ASCs, clinics, and others.

The hospitals & ASCs segment held a dominating India medical devices market share in 2025. The segment’s growth is attributed to the ongoing development of hospital infrastructure in India. There has been a surge in the opening of new hospitals, especially in tier-2 and tier-3 cities. These hospitals are increasingly investing in advanced medical technologies, which is expected to drive the demand for cutting-edge medical devices.

- For instance, in May 2023, the Rajasthan state government permitted the inaugural of satellite hospitals in Jaipur's Karbala area (Hawa Mahal) and Chittorgarh.

The clinics segment held the second-largest share of the India market in 2025. The growth is attributed to increasing public awareness about wellness monitoring and early disease detection, which is increasing the number of patient visits to clinics due to better accessibility and availability of specialized care. This is increasing demand for diagnostic, monitoring, and treatment devices in these settings.

COMPETITIVE LANDSCAPE

Key Market Players

Medtronic, Johnson & Johnson Services, Inc., and GE Healthcare to Dominate Market Due to Increasing Investments and Product Commercializations

India's medical devices sector witnessed a fragmented structure, with international leaders including Medtronic, Johnson & Johnson Services, Inc., and GE Healthcare in 2024. These players are focusing on increasing their footprint in the India market through strategic investments and product commercializations. Moreover, they are increasing their focus on expanding the manufacturing capacity of their products in the country to gain a significant portion of the market.

Other major players such as Abbott, Siemens Healthineers AG, and BD are getting involved in strategic partnerships with India’s healthcare providers, launching new products, and enhancing their supply chain for medical devices. These initiatives are expected to help them secure a significant share of the India market in the coming years.

LIST OF KEY INDIA MEDICAL DEVICES COMPANIES PROFILED

- Medtronic (Ireland)

- Johnson & Johnson Services, Inc. (U.S.)

- Boston Scientific Corporation (U.S.)

- GE Healthcare (U.S.)

- Siemens Healthineers AG (Germany)

- Stryker (U.S.)

- Abbott (U.S.)

- BD (U.S.)

- FUJIFILM Corporation (Japan)

KEY INDUSTRY DEVELOPMENTS

- July 2025 – AliveCor, Inc. announced the launch of the Kardia 12L ECG system in India with a unique single-cable design that can detect life-threatening cardiac conditions.

- January 2024 – Medtronic collaborated with Cardiac Design Labs to launch and expand access to CDL’s novel diagnostic technology, Padma Rhythms, an external loop recorder (ELR) patch for heart monitoring.

- May 2024 – OMRON Corporation collaborated with AliveCor, Inc. to launch portable ECG monitoring devices in India.

- July 2024 – Fitterfly Healthtech Pvt. Ltd. partnered with Ascensia Diabetes Care Holdings AG to include Ascensia's premium Bluetooth-enabled Contour Plus Elite glucometer into Fitterfly's diabetes program kits and Fitterfly App.

- November 2024 – Beurer India launched the GL 22 blood glucose monitor to provide innovative and user-friendly health monitoring solutions in India.

REPORT COVERAGE

The market report offers an in-depth analysis of leading companies and the competitive landscape, identifying the key trends, growth drivers, and opportunities shaping the industry. The report delivers key insights such as new product launches, key developments, prevalence of chronic diseases, and technological advancements. The report also covers detailed company profiles and a detailed analysis of market segments.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 12.20% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type · Orthopedic Devices · Cardiovascular Devices · Diagnostic Imaging · In-vitro Diagnostic (IVD) · Minimally Invasive Surgery Devices (MIS) · Wound Management · Diabetes Care Devices · Ophthalmics Devices · Dental Devices · Nephrology Devices · General Surgery · Others |

|

By End-user · Hospitals & ASCs · Clinics · Others |

Frequently Asked Questions

Fortune Business Insights says that the India market value stood at USD 17.86 billion in 2026 and is projected to record a valuation of USD 44.76 billion by 2034.

The market will exhibit a steady CAGR of 12.20% during the forecast period of 2026-2034.

By type, the in-vitro diagnostics segment will lead the market during the forecast period.

The rising burden of medical conditions, increasing aging population, increasing healthcare infrastructure, and rising adoption of wearable medical devices are driving the market growth.

Medtronic, Johnson & Johnson Services, Inc., and GE Healthcare are the major players in the market.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us