Internet of Vehicles Market Size, Share & Industry Analysis, By Solution (On-Vehicle and IoV Management Center), By Networking Technology (Wi-Fi, Bluetooth, and Cellular Network), By Communication Type (Vehicle-to-Vehicle (V2V), Vehicle-to-Infrastructure (V2I), Vehicle-to-Pedestrian (V2P), Vehicle-to-Cloud (V2C), and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

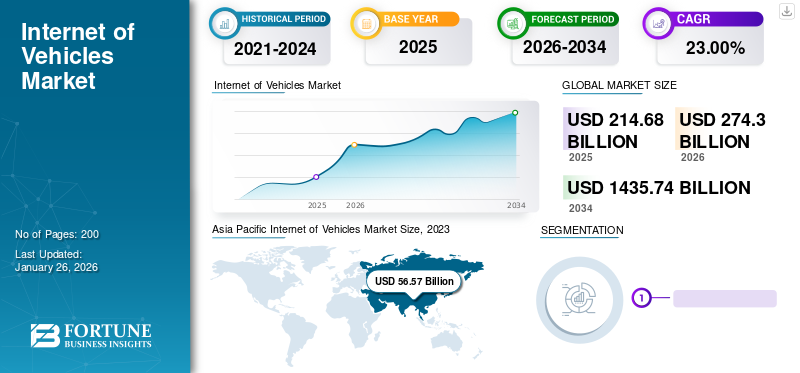

The global Internet of Vehicles market size was valued at USD 214.68 billion in 2025. The market is projected to grow from USD 274.30 billion in 2026 to USD 1,435.74 billion by 2034, exhibiting a CAGR of 23% during the forecast period. Asia Pacific dominated the global market with a share of 39.67% in 2025.

Internet of Vehicles (IoV) combines three networks, a vehicular mobile internet, an intra-vehicle network, and an inter-vehicle network. Based on integrating these networks into one, IoV is defined as a wide-ranging distributed system for information exchange and wireless communication between vehicles to everything, also called V2X (where X includes Internet, roads, people, and vehicles, among others). It uses standard data interaction and communication protocols. It is an integrated system that provides intelligent vehicle control, dynamic information service, and traffic flow management.

Download Free sample to learn more about this report.

Global Internet of Vehicles Market Overview

Market Size:

- 2025 Value: USD 214.68 billion

- 2026 Value: USD 274.30 billion

- 2034 Forecast Value: USD 1,435.74 billion, with a CAGR of 23.0% from 2026–2034

Market Share:

- Asia Pacific: Dominated the market in 2025 with 39.67% share, driven by strong automotive production and infrastructure in China and India.

- Europe: Rapid adoption of connected technologies supports market growth.

- North America: High penetration of vehicle telematics and intelligent transport systems propels expansion.

Industry Trends:

- Surge in cloud-based vehicle architectures and OTA (over-the-air) updates.

- Integration of vehicle-to-everything (V2X) communication including V2V, V2I, and V2C.

- Deployment of real-time vehicle telematics for diagnostics, maintenance, and driver behavior monitoring.

- Development of smart mobility platforms to support autonomous and connected transportation.

Driving Factors:

- Rising demand for connected and autonomous vehicles with real-time data exchange.

- Government support and investment in intelligent transportation infrastructure.

- Increased use of fleet telematics and logistics optimization tools.

- Enhanced focus on road safety, energy efficiency, and predictive maintenance.

- Growing urbanization and congestion driving adoption of smart traffic solutions.

Closed facilities during the COVID-19 pandemic led to significant developments in IoT and cloud-based solutions for vehicles. Since manufacturing facilities were closed, automakers focused on integrating software solutions into their products during the lockdown period, such as the use of Over-the-Air (OTA) software updates in vehicles to improve customers’ driving experience.

The rising demand for safer and more effective road transportation solutions is a major factor contributing to the development of the IoV network across the world. Additionally, connected vehicle technologies are acting as the first step toward building a robust network of vehicles. However, this digital transition in the automotive sector has also introduced new threats of user data leaks and hacking their personal information stored in the vehicle. Nevertheless, significant players in the IoT and automotive industry are focused on creating a robust network structure to negate such risks to accelerate the adoption of IoV technologies.

Download Free sample to learn more about this report.

Internet of Vehicles Market Trends

Rising Adoption of Cloud-based Architecture and Connected Car Technology to Accelerate Market Growth

With the advancement of 5G network, manufacturers aim to shift to a cloud-based electrical/electronic (E/E) vehicle architecture. Processor-intensive tasks, such as road condition observation and image processing can be shifted to cloud. It enhances processing capabilities and improves operational efficiency - some of the benefits that are necessary to fulfill future mobility requirements.

The automotive industry witnessed an intense inclination toward the integration of internet of things (IoT). Trends, such as connected vehicle technology and autonomous driving solutions are noticing rapid technological advancements. Thus, the automotive sector is likely to follow the trend of connected devices and IoT to facilitate seamless communication and transfer of vehicle data between various end users, such as Vehicle-to-Vehicle (V2V), Vehicle-to-Infrastructure (V2I), Vehicle-to-Cloud (V2C), and others.

Internet of Vehicles Market Growth Factors

Need for Effective Traffic and Transportation Solutions to Fuel Market Progress

The major factors leading to the rapid development of Internet of Vehicles technology are demand for robust vehicle safety functions and better road infrastructure. Implementing Internet of Vehicles technology is expected to lower road fatalities and enhance the driving experience. Technologies, such as V2V and V2I, allow vehicles to transfer and gather information related to traffic congestions, route solutions, parking, battery management, and charging stations. These features reduce the hassle and enhance the driving experience.

The increasing development of connectivity among vehicles is opening up new market opportunities for suggestive data solutions. These include finding lower congestion routes, fuel optimization driving options, and various other factors that are contributing toward the overall internet of vehicles architecture. Moreover, safety features, such as ADAS, predictive maintenance, and automotive e-call provide vehicle data, such as the location of the crash, vehicle name, user name, and license plates to the nearest emergency centers. Thus, the need for better safety systems and road infrastructure is expected to drive the Internet of Vehicles market growth.

High Demand for Vehicle Telematics to Drive Market Growth

Vehicle telematics is an onboard communication system integrated with the latest vehicle models, which allows the vehicle to share data related to component health, dysfunctionality, predictive maintenance, and others. Integrating telematics devices with the vehicle allows users as well as OEMs to access various analytics and vehicle insights to improve driving experience and streamline the vehicle maintenance operations. Moreover, telematics also allows the vehicle to receive data from different sources and display it to the user on its Head Unit Display.

Some of the major application areas of vehicle telematics include vehicle tracking and fleet operation tracking. This form of telematics acts as a communicator between the network infrastructure and the vehicle. Furthermore, increasing focus from various fleet operators to introduce telematics into their existing fleet is further expected to fuel market growth. Thus, growing technological advancement in vehicle telematics is expected to aid the development of the Internet of Vehicles network.

RESTRAINING FACTORS

Security Concerns Related to Data Privacy to Restrain Market Growth

Internet of Vehicles creates a network of connected devices and integrates different services, technologies, and communication protocols, which can create information security issues. It makes the system vulnerable to malicious interference such as Distributed Denial-of-Service (DDoS) attacks. Increasing vehicle data hacking incidents may hamper the market expansion as consumers hesitate to opt for it due to lower security protocols in place.

The system can be targeted at multiple levels, such as the vehicle or communication network transferring the data. Vehicle parts, such as steering wheel, brakes, GPS, accelerator, and alarms, can be accessed remotely in Internet of Vehicles technology, and a successful breach can lead to fatalities. Thus, concerns about data leaks and network hacks might restrain the product’s adoption.

Internet of Vehicles Market Segmentation Analysis

By Solution Analysis

Higher Integration of Advanced Vehicle Technologies to Fuel Adoption of On-Vehicle Solutions

By solution, the market is segmented into on-vehicle and IoV management center.

The on-vehicle segment held a leading market share 61.21% in 2025 and is expected to dominate the Internet of Vehicles market share during the forecast period. This is owing to increased integration of telematics and connected vehicle technology in upcoming vehicles including connected cars, electrification technology, and autonomous driving technology. For instance, in March 2022, Navistar announced its fully connected solutions by standardizing factory-installed telematics devices on its class 6 and 8 vehicles. The company aims to accelerate the use of connected technology in the commercial vehicles segment by introducing the latest technological trends.

The IoV management center segment is expected to show a rapid growth rate during the forecast period due to the growing demand for serving solutions, data exchange, and storage points for future vehicles. The management center includes infrastructure that communicates, stores, and analyzes data shared with vehicles. As connected vehicle technology grows, the segment will likely grow as well to accommodate various road and vehicle solutions.

By Networking Technology Analysis

Wi-Fi Technology to Gain Significant Traction for its Extremely Low Transfer Failure Rate

Based on networking technology, the market is segmented into Wi-Fi, Bluetooth, and cellular network.

The Wi-Fi segment held the largest share of the market in 2025. Wi-Fi offers successful data exchange for low as well as high frequency of communications with a failure rate of less than 1%. Additionally, in-vehicle Wi-Fi enables on-the-go connectivity via mobile hotspots, allowing users to connect with intelligent devices. These factors are boosting the growth of this segment.

The cellular network segment is anticipated to show exponential growth during the forecast period. This is attributed to the increasing development of 5G-based Internet of Vehicle solutions, which offer reliability, extremely high bandwidth & data transfer rate, and ultra-low latency as compared to the existing communication networks. The increasing development of technologies which depend on cellular data transfer is further expected to boost market growth during the forecast period.

By Communication Type Analysis

To know how our report can help streamline your business, Speak to Analyst

Growing Demand for Safety Solutions in Vehicles to Fuel Use of V2V Communication System

Based on communication type, the market is segmented into Vehicle-to-Vehicle (V2V), Vehicle-to-Infrastructure (V2I), Vehicle-to-Pedestrian (V2P), Vehicle-to-Cloud (V2C), and others.

The V2V segment dominated the market with a share of 41.59% in 2026. V2V provides low delay time and reliable exchange of information, such as situational awareness messages and map data. Furthermore, it is a complementary technology expected to support and enhance the operation of autonomous vehicles. Hence, these factors will fuel the dominance of this segment during the forecast period.

The V2I segment is expected to grow faster during the forecast period. The increasing implementation of this communication system in traffic management, which can be used on high-traffic highways to optimize vehicle flow and maximize fuel economy, is driving the growth of this segment.

REGIONAL INSIGHTS

Asia Pacific Internet of Vehicles Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific to Dominate Global Market Due to High Production Rate of Vehicles

Asia Pacific

In 2025, Asia Pacific generated USD 85.16 billion, contributing 39.67% to global market revenue, and is projected to grow to USD 109.69 billion in 2026. Asia Pacific held a significant market share and outsized the market share of other regions owing to the higher rate of production of connected vehicles and growing infrastructure within the region. Asia Pacific is also expected to record the highest growth rate of 25.8% owing to the adoption of futuristic mobility technologies in larger automotive markets, such as China, India, and other Asian countries. Additionally, most of the prominent automakers within the market belong to Asia Pacific.The Japan market is projected to reach USD 26.53 billion by 2026, the China market is projected to reach USD 40.42 billion by 2026, and the India market is projected to reach USD 9.39 billion by 2026.

Europe

Europe maintained a strong presence in the global market, reaching USD 66.51 billion in 2025, accounting for 30.98% share, and is expected to reach USD 84.15 billion in 2026. Europe accounted for a significant market share owing to the greater adoption rate of connected vehicle technology due to the establishment of supporting infrastructure and higher consumer preference toward advanced in-vehicle and innovative mobile technology within the region. Due to the presence of major automotive vehicle companies in the region, the market is expected to grow at a steady rate.The UK market is projected to reach USD 7.2 billion by 2026, while the Germany market is projected to reach USD 38.48 billion by 2026.

North America

The North America region captured 21.22% of the global market in 2025, generating USD 45.55 billion in revenue, and is projected to reach USD 57.88 billion in 2026. The North America Internet of Vehicles market accounted for a trivial market share, and it is expected to grow significantly due to a more substantial adoption rate of newer automotive technologies and well-established infrastructure in the region. The rest of the world is likely to follow the growth trends of the major regions and grow substantially as key European regions aim to expand their manufacturing operations in the African continent.The U.S. market is projected to reach USD 24.78 billion by 2026.

List of Key Companies in Internet of Vehicles Market

Major Players to Introduce Technological Advancements to Offer Additional Value for Products

Volkswagen (VW) is one of the leading players in the market’s competitive landscape attributed to the popularity of its Internet of Vehicles services such as Car-Net and Volkswagen Connect. It is also an active member of the 5G Automotive Association, which accelerates the development of cellular V2X (C-V2X) technology and improves system standardization, among other functions. Additionally, major players are rushing toward integrating 5G technology in their upcoming models to provide a fast and highly efficient data exchange between vehicles.

Players, such as AT&T, Verizon Technologies, Microsoft, and Oracle, are leading in cloud-based solutions and looking forward to working with leading automakers in the industry, such as General Motors, Robert Bosch, BMW, and Audi, to provide innovative IoT solutions in the automotive sector. The rising development of electrification technology and supporting infrastructure, such as charging stations and Vehicle-to-Grid technology, are some of the major technological trends, which the key market players are focusing on.

Request for Customization to gain extensive market insights.

LIST OF KEY COMPANIES PROFILED:

- NXP Semiconductors (Netherlands)

- Intel Corporation (U.S.)

- IBM Corporation (U.S.)

- Google LLC (U.S.)

- Cisco System, Inc. (U.S.)

- Volkswagen (Germany)

- Ford Motor Company (U.S.)

- Veniam (U.S.)

- Audi (Germany)

- BMW (Germany)

- Robert Bosch (Germany)

- Qualcomm (U.S.)

- Ford (U.S.)

- Tata Communications (India)

- CarIQ (U.S.)

- AT&T (U.S.)

- Verizon Technologies Inc. (U.S.)

- General Motors (U.S.)

- Microsoft (U.S.)

- Samsung Electronics (South Korea)

KEY INDUSTRY DEVELOPMENTS:

- December 2023 – Virtual Internet, one of the leading player in the software 5G technology announced its broadband technology Virtual 5G, has begun distribution for android auto. Through this integration the users will be able to carry out various function from inside the cabin at much higher speeds.

- April 2023 – Keysight announced the expansion of its business unit ‘Novus’ by adding Novus Mini to its industrial and automotive IoT solutions portfolio. The service will provide a compact test platform for service engineers deploying automotive and industrial IoT solutions.

- March 2023 – Aeris, an IoT solutions company, acquired the IoT accelerator and connected vehicle cloud divisions from Ericsson. The company aims to form a partnership and provide innovative solutions to one of the largest markets in the automotive industry, the Asia Pacific region.

- February 2023 – Qualcomm launched the next generation of the snapdragon automotive platform featuring the company’s fastest modem, the new Auto 5G modem. It possesses 50% more processing power and a network capacity of up to 200Mhz, which can also support low latency connectivity and satellite communications.

- February 2023 – Chinese city Wuxi, situated in the eastern Jiangsu province, introduced new laws for Internet of Vehicles (IoV) to adopt the technology for public transport, traffic monitoring & management systems, logistics, and delivery. The city aims to promote a full range of car connectivity and networking technologies to accelerate the adoption of intelligent transport and to develop smart cities.

REPORT COVERAGE

The market research report covers a detailed analysis of the market and focuses on key aspects such as leading companies, product types, and prominent applications of the product. Besides, the report offers insights into the latest market trends and highlights key industry developments. In addition to the aforementioned factors, the report delivers in-depth analysis of several factors that have contributed to the market’s growth in recent years.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2024 |

|

Estimated Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 23% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Solution

|

|

By Networking Technology

|

|

|

By Communication Type

|

|

|

By Geography

|

Frequently Asked Questions

Fortune Business Insights estimates that the global market size was USD 214.68 billion in 2025 and is projected to reach USD 1,435.74 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 85.16 billion.

Registering a CAGR of 23%, the market will exhibit promising growth during the forecast period of 2026-2034.

The Vehicle-to-Vehicle (V2V) segment is expected to be the leading segment in this market during the forecast period.

Asia Pacific held a leading share of the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us