Aircraft Landing Gear Market Size, Share & Industry Analysis, By Type (Nose Landing Gear and Main Landing Gear), By Platform (Fixed-Wing and Rotary-Wing), By Arrangement (Tail Wheel, Tandem, and Tri-Cycle), By Component (Retraction System, Brakes & Wheels, Steering, and Others), By End User (OEM and Aftermarket), and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

KEY MARKET INSIGHTS

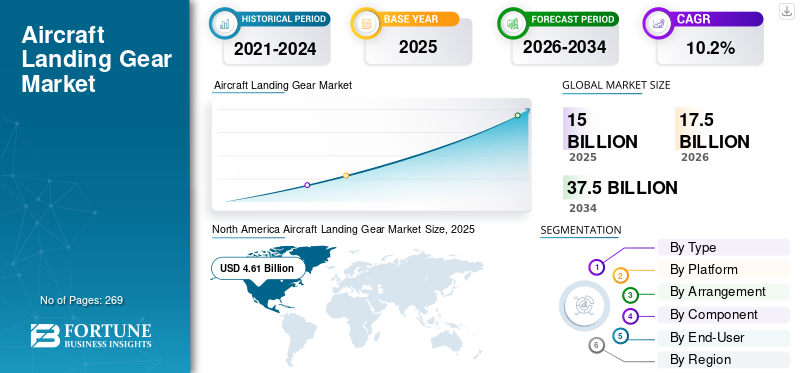

The global aircraft landing gear market size was valued at USD 14.98 billion in 2025. The market is projected to grow from USD 17.52 billion in 2026 to USD 38.21 billion by 2034, exhibiting a CAGR of 10.2% during the forecast period. North America dominated the global aircraft landing gear market with a market share of 30.77% in 2025.

Aircraft landing gear, also called undercarriage, comprises struts, wheels, brakes, steering systems, retraction units, and actuators that hold up the plane on the ground, ease taxiing, handle takeoffs and landings, and soak up landing shocks. This market handles production, sales, and upkeep for gear suited to commercial airliners, military planes, and general aviation craft. End users are split between OEMs fitting new builds and aftermarket services for fixes and overhauls.

Safran, Collins Aerospace, Liebherr, Héroux-Devtek, Honeywell, Triumph Group, GKN Aerospace, Eaton, Magellan Aerospace, and Sumitomo Precision are a few key players in the market. These firms pursue strategic partnerships to expand capabilities, invest in R&D for lightweight composites and electric actuation systems, and develop advanced braking and steering technologies to gain a competitive edge in the market.

Download Free sample to learn more about this report.

AIRCRAFT LANDING GEAR MARKET Key Takeaways

- 2025 Market Size: USD 14.98 billion

- 2026 Market Size: USD 17.52 billion

- 2034 Forecast Market Size: USD 38.21 billion

- CAGR: 10.2% from 2026–2034

- North America dominated the global aircraft landing gear market with a market share of 30.77% in 2025.

- The main landing gear segment is expected to account for 57.14% of the market in 2026.

- The fixed-wing segment is projected to lead the global market with a share of 61.99% in 2026.

North America

The market reached USD 5.9 billion in 2025 and is projected to grow to USD 6.9 billion in 2026, supported by major aircraft OEMs, strong commercial aircraft production, defense spending, and a robust aftermarket ecosystem.

Asia Pacific

Valued at USD 3.0 billion in 2025, the region is expected to remain the fastest-growing market, driven by expanding commercial aviation fleets, increasing passenger traffic, and rising aircraft procurement across emerging economies.

Europe

The region continues to witness steady demand for aircraft landing gear systems, supported by established aerospace manufacturing capabilities, fleet modernization programs, and ongoing maintenance activities.

U.S.

The market is estimated at approximately USD 4.84 billion in 2026, driven by the world's largest commercial and military aircraft fleet, creating sustained demand for landing gear replacement, maintenance, and overhaul services.

Japan

The market is estimated at around USD 0.63 billion in 2026, supported by commercial fleet renewal, participation in global aircraft programs, and continued demand from military transport and patrol aircraft.

Read More

AIRCRAFT LANDING GEAR MARKET TRENDS

Adoption of Lighter and Robust Landing Gear to Favor Market

Landing gear is a heavily loaded structure in an aircraft. Its weight varies from 3% to 6% of the total aircraft weight. The companies involved in the production business are manufacturing robust and lighter landing gear without compromising its functions, operations, performance, safety, and maintenance requirements. This is made possible by using materials of higher strength, fracture toughness, and fatigue properties. These materials mainly include ultra-high-strength alloy steels, corrosion-resistant steel, titanium alloys, high-strength aluminum alloys, and composites. Increasing focus of aircraft manufacturers on adopting various high tensile strength materials to better brace and cope with the ground impact while landing is also expected to influence the aircraft landing gear market growth in the coming years.

- For instance, in June 2023, TISICS advanced commercial aviation with LightLand, a ceramic fiber-reinforced metal composite landing gear developed with Safran Landing Systems, targeting 30-70% weight cuts for net-zero emissions by 2050.

Russia-Ukraine War Impact

Landing gear systems are heavily dependent on high-strength titanium alloys and specialty steels for main struts, axles, and load-bearing components. Russia was a significant upstream supplier of aerospace-grade titanium, either directly or indirectly, before 2022.

- Sanctions and self-sanctioning by Western OEMs disrupted established procurement routes.

- OEMs and tier-1 suppliers (Safran Landing Systems, Collins, Liebherr) were forced to requalify alternative suppliers in Japan, the U.S., and Europe.

- This requalification increased cost, lead times, and certification effort, particularly for forged components with long approval cycles.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Commercial Aircraft Production and Fleet Replacement to Propel Market Growth

Air traffic and air travel are surging globally, which is driving an increase in the production of commercial aircraft. Major OEMs have steadily increased output rates across narrowbody and widebody programs to fulfil surging airline orders and clear extensive backlogs.

- For instance, in 2025, Airbus increased commercial programs targeting 75 A320 Family aircraft monthly by 2027, led by the A321neo, capturing two-thirds of 7,000+ backlog orders. Moreover, Boeing announced its plans to increase monthly production of its 737 aircraft to 47 units.

In addition, global aircraft fleet replacement and expansion accelerate globally, propelled by robust air travel demand, necessitating the substitution of aging fleets with efficient, sustainable alternatives.

- For instance, in January 2026, Alaska Airlines placed its largest-ever order for 105 Boeing 737-10s and five 787 widebodies, with options for 35 more 737-10s through 2035. It serves as fleet replacement by upgrading narrowbody operations to efficient 737 MAX variants during widespread industry retirements of older aircraft.

MARKET RESTRAINTS

Safety Concerns Related to Landing Gear Systems to Hamper Market Growth

In the aviation industry, the safety of passengers is the utmost priority for the airline operators. Landing gear systems comprise several system components and parts. A slight mistake by the crew or engineering team in the functioning of this gear can lead to major aircraft disasters. In recent times, there have been a few airplane accidents, mostly at the time of aircraft landing, which have reiterated the risks surrounding this type of gear system. Landing gear failures such as collapse, retraction malfunction, or brake system issues can lead to severe operational disruptions, aircraft damage, and regulatory scrutiny.

MARKET OPPORTUNITIES

Rising MRO Demand from Increased Flight Hours to Present Market Growth Opportunities

Rising Maintenance, Repair, and Overhaul (MRO) demand arrives from surging global flight hours, accelerating wear on landing gear components such as brakes, wheels, and retraction systems. High landing frequency accelerates wear of brakes, wheels, and selected structural components, increasing replacement and overhaul demand. Suppliers that offer integrated MRO services, exchange programs, and predictive maintenance solutions can capture recurring revenue beyond initial OEM delivery. As airline cost pressure increases, operators are also more willing to enter long-term service agreements, improving revenue visibility for landing gear OEMs and Tier-1 suppliers. Airlines face mandatory overhauls and replacements, creating steady aftermarket revenue streams beyond initial OEM installations. Moreover, there is a shift toward consolidation and capability expansion in the aftermarket. For example, GA Telesis completed the acquisition of AAR’s landing gear, wheels, and brakes overhaul business.

MARKET CHALLENGES

Supply Chain Disruptions Present a Major Market Challenge

Supply chain disruptions present a major market challenge for aircraft landing gear. Global events such as geopolitical tensions, including the Russia-Ukraine conflict, and tariffs disrupt supplies of critical raw materials such as titanium, essential for struts and actuators, causing shortages and production delays. Logistics bottlenecks and uneven material availability extend lead times, inflate costs, and hinder manufacturers' ability to meet rising demand from commercial and military fleets. OEMs and MRO providers face added pressure from regional sourcing shifts and the need for alternative suppliers, slowing innovation in lightweight composites and electric systems.

Segmentation Analysis

By Type

Increased Passenger Traffic and Aircraft Deliveries to Boost Main Landing Gear Segmental Growth

Based on the type, the market is bifurcated into nose landing gear and main landing gear.

The main landing gear segment is expected to account for 57.14% of the market in 2026. A major factor in the segmental growth is the increased passenger aircraft and aircraft deliveries in the Middle East and Asian countries. Growing orders for modern aircraft across the world are pushing the demand for advanced landing gear systems.

- For instance, in January 2026. Alaska Airlines finalized its largest-ever aircraft order, acquiring 110 Boeing jets comprising 105 737-10 narrowbodies and five 787 Dreamliners.

The nose landing gear segment is anticipated to rise with a CAGR of 9.8% over the forecast period.

By Platform

Fixed-wing Segment Led Market Due to Rise in Low-Cost Carriers

Based on the platform, the market is bifurcated into fixed-wing and rotary-wing.

In 2026, the fixed-wing segment is projected to lead the global market with a share of 61.99%, driven by the growth of low-cost carriers (LCCs), which require a large number of dependable, efficient aircraft for high-frequency routes.

The rotary-wing segment is expected to grow at a high CAGR of 10.8% over the forecast period.

By Arrangement

Tri-Cycle Segment to Take the Lead Due to Its High Stability

Based on the arrangement, the market is segmented into tail wheel, tandem, and tri-cycle.

The tri-cycle segment holds a market share of 67.10% in 2026. The tricycle landing gear segment benefits greatly from high stability since it offers better directional control and safety on the ground, allowing the related driving arrangements to operate more effectively and dependably.

The tandem segment is projected to grow at a high CAGR of 11.9% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Component

High Replacement Rate to Boost Brakes & Wheels Segment Growth

Based on the component, the market is segmented into retraction systems, brakes & wheels, steering, and others.

The brakes & wheels segment is anticipated to witness a dominating market share over the forecast period. The prominence of brakes and wheels is due to their high replacement rate compared to other landing gear parts, especially in commercial aircraft that are heavily used. Frequent brake wear during landing, rejected take-offs, and taxiing creates strong demand in the aftermarket, which supports the segment’s revenue leadership.

The retraction system segment is projected to grow at a CAGR of 55.71% in 2026.

By End User

Execution of Aircraft Backlog and High Production Boosted OEM Segment Expansion

Based on the end user, the market is bifurcated into OEM and aftermarket.

The OEM segment dominated the market share. The segmental dominance directly comes from the execution of the aircraft backlog and the normalization of production rates across key programs.

In addition, the aftermarket segment is projected to grow at a high CAGR of 10.8% during the study period.

Aircraft Landing Gear Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Aircraft Landing Gear Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America accounted for USD 5.9 billion in 2025, representing 39.10% of the global market share, and is projected to reach USD 6.9 billion in 2026. The region dominance is driven by the presence of major aircraft OEMs, high commercial aircraft production rates, and a large in-service fleet requiring regular landing gear overhauls. Strong defense aviation spending and sustained aftermarket demand further support regional market leadership.

U.S Aircraft Landing Gear Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 4.84 million in 2026, accounting for roughly 9.1% CAGR. Growth in the U.S. market is driven by the world’s largest installed commercial and military aircraft fleet, resulting in high replacement and overhaul demand.

Europe

The Europe market was valued at USD 3.3 billion in 2025, capturing 22.30% of global revenue, and is estimated to reach USD 4 billion in 2026. Increasing focus on fleet modernization, sustainable aircraft programs, and collaborative defense aviation initiatives across European nations continues to drive both OEM and aftermarket demand.

U.K Aircraft Landing Gear Market

The U.K. market in 2026 is estimated at around USD 0.55 billion, representing roughly 10.9% CAGR during the study period. The growth of the country is growing significantly due to strong integration activity within global commercial aircraft programs. Moreover, UK-based landing gear suppliers remain deeply embedded in Airbus and defense aviation supply chains, which helps in overall growth.

Germany Aircraft Landing Gear Market

Germany’s market is projected to reach approximately USD 0.83 billion in 2026. Growth is mainly aftermarket-driven, supported by Germany’s strong airline base and MRO ecosystem.

Asia Pacific

In 2025, Asia Pacific held 18.80% of the global market, reaching a valuation of USD 3 billion, and is projected to grow to USD 3 billion in 2026, and secure the position of the third-largest region in the market and fastest growing during the study period. Growth is primarily driven by the rapid expansion of commercial aviation fleets, rising air passenger traffic, and increasing aircraft procurement by emerging economies such as China and India.

Japan Aircraft Landing Gear Market

The Japanese market in 2026 is estimated at around USD 0.63 billion, accounting for roughly 13.8% of the compound annual growth rate (CAGR) during the forecast period. This growth is fueled by Japan’s steady renewal of its commercial fleet, participation in global widebody and narrowbody programs, and ongoing operation of military transport and patrol aircraft that depend on strong multi-wheel main landing gear assemblies.

China Aircraft Landing Gear Market

China’s market is projected to be one of the largest in Asia Pacific, with 2026 revenues estimated at around USD 1.52 billion. China’s strong position comes from its large and growing commercial aircraft fleet, consistent deliveries of narrowbody and widebody aircraft, and expanding military aviation programs.

India Aircraft Landing Gear Market

The Indian market in 2026 is estimated at around USD 0.59 billion. This growth is driven by fleet upgrades, increased aircraft use at crowded airports, and the adoption of better nose gear steering and monitoring systems to improve taxi efficiency and ground handling performance.

Latin America

The Latin America region captured 5.20% of the global market in 2025, generating USD 0.78 billion in revenue, and is projected to reach USD 0.85 billion in 2026. The growth is driven by aging fleets, high utilization of narrowbody aircraft on short- and medium-haul routes, and required landing gear overhaul cycles. The expansion of regional MRO capabilities and an increased focus on life-extension programs continue to boost aftermarket demand.

Middle East & Africa

Middle East & Africa contributed approximately USD 0.29 billion to the global market in 2025, accounting for 14.50% share, and is expected to reach USD 0.29 billion in 2026. The growth is backed by rapid expansion in the aviation sector, new airline launches, and the development of airport infrastructure, along with an increase in both commercial and military aircraft.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Partnerships Between Key Players to Fuel Market Expansion

The aircraft landing gear market stays consolidated, led by major players such as Safran Landing Systems, Collins Aerospace, Héroux-Devtek, Liebherr-Aerospace, and Sumitomo Precision Products, holding significant shares via OEM contracts. Strategic partnerships drive expansion as Safran teams with Airbus on A350 gear upgrades, Collins Aerospace partners with Boeing for 787 systems, and Héroux-Devtek supplies military platforms alongside Lockheed Martin. These collaborations strengthen supply chains amid rising narrow-body demand and defense fleet modernizations.

LIST OF KEY AIRCRAFT LANDING GEAR COMPANIES PROFILED

- AAR Corporation (U.S.)

- Alaris Aerospace (Canada)

- CIRCOR International Inc. (U.S.)

- Collins Aerospace (U.S.)

- GKN Aerospace (U.K.)

- Hawker Pacific Aerospace (Australia)

- Heroux-Devtek Inc. (Canada)

- Liebherr Group AG (Switzerland)

- Magellan Aerospace Corporation (Canada)

- Safran SA (France)

- Triumph Group Inc. (U.S.)

- Honeywell Aerospace (U.S.)

KEY INDUSTRY DEVELOPMENTS

- June 2025: Safran Landing Systems and REVIMA expanded their long-term partnership to include maintenance and repair capabilities for new-generation landing gear on A320neo, A330neo, and A350-900 main landing gear. This aligns the aftermarket network with fleets that are moving into their higher-maintenance years.

- April 2025: Liebherr-Aerospace, OEM for Airbus A350 nose landing gear, partnered with REVIMA to expand MRO services via REVIMA's Asia Pacific facility.

- April 2025: Kratos unveiled a rendering of its XQ-58 Valkyrie drone variant featuring integrated tricycle landing gear for conventional takeoff and landing (CTOL/HTOL). This enhances operational flexibility, boosts sortie generation rates, and simplifies logistics by avoiding expendable rocket motors.

- October 2023: Safran Landing Systems signed a five-year contract with Wizz Air to perform maintenance and repair on landing gear for 57 A320-family aircraft at Safran’s Gloucester facility in the U.K. This indicates growing demand for narrowbody gear servicing as usage increases.

- April 2023: Liebherr-Aerospace and REVIMA signed a memorandum of understanding at MRO Americas 2023 to provide maintenance and repair for Airbus A350 nose landing gear in the Asia Pacific region. This expands Liebherr’s landing gear service network and brings it closer to operators.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 10.2% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type, Platform, Arrangement, Component, End User, and Region |

|

By Type |

· Nose Landing Gear · Main Landing Gear |

|

By Platform |

· Fixed-Wing · Rotary-Wing |

|

By Arrangement |

· Tail Wheel · Tandem · Tri-Cycle |

|

By Component |

· Retraction System · Brakes & Wheels · Steering · Others |

|

By End User |

· OEM · Aftermarket |

|

By Region |

· North America (By Type, Platform, Arrangement, Component, End User, and Country) o U.S. (Type) o Canada ( Type) · Europe (By Type, Platform, Arrangement, Component, End User, and Country/Sub-region) o U.K. (Type) o Germany (Type) o France (Type) o Italy (Type) o Russia (Type) o Rest of Europe (Type) · Asia Pacific (By Type, Platform, Arrangement, Component, End User, and Country/Sub-region) o China (Type) o India (Type) o Japan (Type) o Australia (Type) o Rest of Asia Pacific (Type) · Latin America (By Type, Platform, Arrangement, Component, End User, and Country/Sub-region) o Brazil (Type) o Mexico (Type) o Rest of Latin America (Type) · Middle East & Africa (By Type, Platform, Arrangement, Component, End User, and Country/Sub-region) o UAE (Type) o Saudi Arabia (Type) o South Africa (Type) o Rest of Middle East & Africa (Type) |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 14.98 billion in 2025 and is projected to reach USD 38.21 billion by 2034.

In 2025, the market value in North America stood at USD 4.61 billion.

The market is expected to exhibit a CAGR of 10.2% during the forecast period of 2026-2034.

By type, the main landing gear segment is expected to dominate the market.

Rising commercial aircraft production and fleet replacement propel market growth.

Safran Landing Systems, Collins Aerospace, Héroux-Devtek, and Liebherr-Aerospace are a few key players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 269

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us