Medical Implants Market Size, Share & Industry Analysis, By Product Type (Orthopedic Implants {Joint Reconstruction Implants, Spine Implants, & Others}, Cardiovascular Implants {Cardiac Rhythm Management Devices, Structural Heart Implants}, Dental Implants, Cosmetic & Reconstructive Implants {Breast Implants, Facial Implants}, Neurological Implants {Deep Brain Stimulators, Spinal Cord Stimulators}, & Others), By Material (Metallic Implants, Polymer Implants, Ceramic Implants, Biomaterial-Based Implants), By End-user (Hospitals & ASCs, Specialty Clinics), & Regional Forecast, 2026-2034

Medical Implants Market Size and Future Outlook

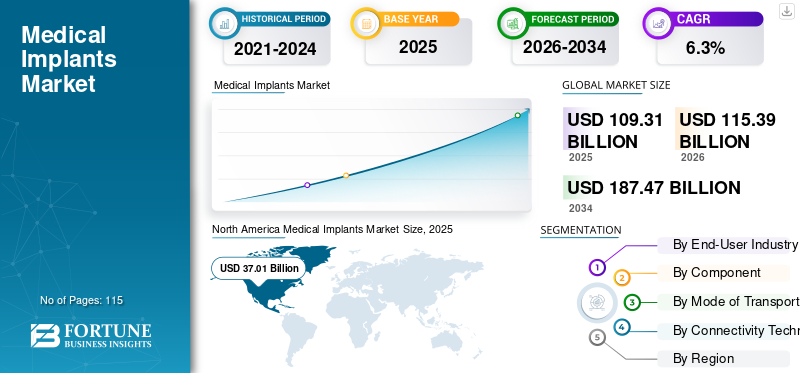

The global medical implants market size was valued at USD 109.31 billion in 2025. The market is projected to grow from USD 115.39 billion in 2026 to USD 187.47 billion by 2034, exhibiting a CAGR of 6.3% during the forecast period. North America dominated the medical implants market with a market share of 33.86% in 2025.

Medical implants are devices placed inside the body to replace, support, or improve the function of damaged body parts. The product portfolio includes a wide range of devices such as orthopedic implants, cardiac implants, dental implants, and neurostimulators, amongst others. The market growth is primarily attributed to the increasing prevalence of chronic conditions, growing life expectancy, and technological advancements. In addition, an aging population and a rise in the number of product launches are also projected to have a positive impact on the market growth. Also, continuous product innovation and strategic acquisitions by major companies further support market expansion.

- For instance, in January 2025, Zimmer Biomet announced plans to acquire Paragon 28 to strengthen its orthopedic implant portfolio and expand its presence in foot and ankle solutions.

Furthermore, many key industry players, such as Johnson & Johnson MedTech, Medtronic plc.

Stryker Corporation, Zimmer Biomet Holdings, Inc., and Abbott Laboratories, operating in the market, are focusing on developing various innovative technologies to offer better products with improved accuracy and efficiency.

Download Free sample to learn more about this report.

MEDICAL IMPLANTS MARKET TRENDS

Growing Emphasis on Minimally Invasive Surgical Procedures Curate New Market Trend

The market is witnessing considerable demand for minimally invasive surgeries across the globe. These surgical procedures are appropriate for implant placements. Moreover, patients and surgeons also prefer procedures that involve smaller incisions, less pain, and faster recovery. This preference is influencing implant design, surgical tools, and hospital workflows. Further, manufacturers are aligning product development with these clinical needs. The trend is especially visible in orthopedic and cardiac implant procedures, where faster patient mobility and shorter hospital stays are key goals.

- For instance, in May 2023, Medtronic received FDA approval for its Micra systems. The newly launched next-generation technology enables leadless pacing functionalities.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Increased Life Expectancy and Growing Prevalence of Chronic Conditions to Accelerate Market Growth

The global aging population is one of the major drivers impacting the global medical implants market growth. Older adults are more likely to develop joint degeneration, heart rhythm disorders, and other conditions that require implant-based treatment. Moreover, at the same time, lifestyle diseases such as obesity and diabetes are increasing among younger populations. As a result, the number of implant procedures continues to rise across orthopedic, cardiac, and dental segments. Hospitals are also focusing more on long-term treatment outcomes and mobility restoration.

- For instance, according to data published by the Centers for Disease Control and Prevention, an estimated 40% of the U.S. population was obese during 2022-2023.

MARKET RESTRAINTS

High Cost of Implant Procedures to Deter Market Growth

Medical implant procedures can be expensive because they involve advanced devices, skilled surgeons, and hospital infrastructure. In addition, in many regions, insurance coverage is limited or varies widely, which makes patients delay elective procedures such as joint replacements. Moreover, hospitals in price-sensitive markets also face budget constraints when stocking premium implant systems. Even when clinical need exists, affordability concerns can slow adoption. These cost pressures are especially visible in developing countries, where out-of-pocket spending remains high.

MARKET OPPORTUNITIES

Expansion of Outpatient and ASC-Based Implant Surgeries to Offer Lucrative Market Growth Opportunities

More implant procedures are gradually shifting from large hospitals to ambulatory surgery centers (ASCs) and specialized outpatient facilities. These centers focus on efficiency, faster discharge, and lower procedural costs. This shift creates opportunities for implant manufacturers to design products and service models tailored for high-throughput outpatient settings. Moreover, market players are also developing ASC-focused solution bundles to support this transition. As healthcare systems try to reduce hospital burden and improve cost efficiency, outpatient implant procedures are expected to grow steadily, creating a strong long-term opportunity for the medical implants market.

MARKET CHALLENGES

Strict Regulatory and Approval Requirements Pose a Critical Challenge to Market Growth

Medical implants must meet very strict safety and quality standards before reaching the market. Regulatory approvals can take time and require extensive clinical and manufacturing documentation. Any delay in approvals or compliance issues can slow product launches and market entry. In addition, post-market surveillance requirements are becoming more demanding, increasing the burden on manufacturers. Smaller companies may find it difficult to navigate complex regulatory pathways. These factors can slow innovation cycles and create barriers for new entrants, making regulatory pressure an ongoing challenge in the medical implants market.

Segmentation Analysis

By Product Type

Higher Number of Joint Replacement Procedures in the Orthopedic Implants Segment Growth

Based on the product type, the market is divided into orthopedic implants, cardiovascular implants, dental implants, cosmetic & reconstructive implants, neurological implants, and others.

The orthopedic implants segment is anticipated to account for the largest medical implants market share. The segment growth is attributed to the substantial volume of joint replacement procedures, the rise in prevalence of orthopedic conditions, and the aging population. In addition, technological developments and new product launches by market players are also expected to augment segment growth during the forecast period.

- For instance, in February 2026, Arthrex announced the launch of its TightRope SB all-suture implant for anterior cruciate ligament reconstruction. Moreover, the new device is also incorporated with soft button technology.

The dental implant segment is anticipated to rise with a CAGR of 7.4% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Material

Significant Support and Long-term Durability of Metallic Implants to Accelerate Segment Growth

Based on material, the market is segmented into metallic implants, polymer implants, ceramic implants, biomaterial-based implants, and others.

In 2025, the metallic implants segment dominated the global market. Metallic implants dominate because they provide strong mechanical support and long-term durability inside the body. Moreover, materials such as titanium and stainless steel are widely trusted by surgeons for orthopedic, dental, and cardiac applications. In addition, hospitals prefer metallic implants for load-bearing procedures including hip and knee replacements. These materials also have a long clinical history, which increases physician confidence.

The biomaterial-based implants segment is anticipated to rise with a CAGR of 7.8% over the forecast period.

By End-User

Availability of Superior Surgical Infrastructure in Hospitals & ASCs to Boost Segment Growth

Based on end-user, the market is segmented into hospitals & ASCs, specialty clinics, and others.

In 2025, hospitals & ASCs held the highest market share. Hospitals and ambulatory surgery centers (ASCs) account for the largest share because most implant procedures require surgical infrastructure, trained specialists, and post-operative care. Hospitals handle complex cases and emergency trauma, while ASCs are increasingly performing elective implant procedures such as joint replacements. Furthermore, the segment is set to hold 79.0% share in 2026.

In addition, the specialty clinics segment is projected to grow at a CAGR of 6.7% during the study period.

Medical Implants Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Medical Implants Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valued at USD 35.19 billion, and also maintained the leading share in 2025, with USD 37.01 billion. The market in North America is expected to increase due to higher surgical volume, technological advancements, and an aging population.

U.S Medical Implants Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 33.95 billion in 2026, accounting for roughly 29.4% of global sales.

Europe

Europe is projected to record a growth rate of 5.7% in the coming years and reach a valuation of USD 33.44 billion by 2026. The region is estimated to witness considerable market growth due to rising investments for new product development and the growing prevalence of orthopedic conditions.

U.K Medical Implants Market

The U.K. market in 2026 is estimated at around USD 5.62 billion, representing roughly 4.9% of global revenues.

Germany Medical Implants Market

Germany’s market is projected to reach approximately USD 7.72 billion in 2026, equivalent to around 6.7% of global sales.

Asia Pacific

Asia Pacific is estimated to reach USD 29.73 billion in 2026 and secure the position of the third-largest region in the market.

Japan Medical Implants Market

The Japanese market in 2026 is estimated at around USD 5.33 billion, accounting for roughly 4.6% of global revenues.

China Medical Implants Market

China’s market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 10.05 billion, representing roughly 8.7% of global sales.

India Medical Implants Market

The Indian market in 2026 is estimated at around USD 6.78 billion, accounting for roughly 5.9% of global revenues.

Latin America and the Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The Latin America market is set to reach a valuation of USD 7.31 billion in 2026. In the Middle East & Africa, the GCC is set to reach a value of USD 2.22 billion in 2026.

South Africa Medical Implants Market

The South African market is projected to reach around USD 0.92 billion in 2026, representing roughly 0.80% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Rising Number of Collaborations Coupled with New Product Launches by Key Players to Boost Market Progress

The global medical implants market holds a semi-consolidated market structure, constituting prominent players such as Johnson & Johnson MedTech, Medtronic plc., Stryker Corporation, Zimmer Biomet Holdings, Inc., and Abbott Laboratories. The significant global share of these companies is due to numerous strategic activities, including distribution collaborations and new product launches.

- For instance, in August 2024, Zimmer Biomet highlighted the use of its Persona IQ smart knee implant, which includes an embedded sensor to remotely monitor patient recovery data such as motion and walking patterns.

Other notable players in the global market are Boston Scientific Corporation, Edwards Lifesciences Corporation, Institut Straumann AG, and Dentsply Sirona Inc. These companies are expected to prioritize collaborations to increase their global market share during the forecast period.

LIST OF KEY MEDICAL IMPLANTS COMPANIES PROFILED

- Johnson & Johnson MedTech (U.S.)

- Medtronic plc (Ireland)

- Stryker Corporation (U.S.)

- Zimmer Biomet Holdings, Inc. (U.S.)

- Abbott Laboratories (U.S.)

- Boston Scientific Corporation (U.S.)

- Edwards Lifesciences Corporation (U.S.)

- Institut Straumann AG (Switzerland)

- Dentsply Sirona Inc. (U.S.)

- Cochlear Limited (Australia)

KEY INDUSTRY DEVELOPMENTS

- June 2025: Johnson & Johnson MedTech announced the launch of its KINCISE 2 surgical automated system for knee replacement surgery.

- April 2025: Medtronic plc received FDA approval for its SelectSecure Model 3830 pacing lead for the treatment of ventricular tachyarrhythmias and ventricular fibrillation.

- October 2024: VISIE Inc. successfully conducted a demonstration of its continuous anatomic auto-tracking for knee surgery.

- April 2024: Medtronic plc received FDA approval for its Inceptiv spinal cord stimulator.

- December 2021: Integer Holdings Corporation acquired Oscor, Inc. in order to strengthen the manufacturing of cardiovascular devices, neurostimulation, and peripheral vascular devices.

REPORT COVERAGE

The global medical implants market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, as well as key industry developments and investments by key regions. The global market research report also provides a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.3% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product Type, Material, End-User, and Region |

| By Product Type |

|

| By Material |

|

| By End-User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 109.31 billion in 2025 and is projected to reach USD 187.47 billion by 2034.

In 2025, the market value for North America stood at USD 37.01 billion.

The market is expected to exhibit a CAGR of 6.3% during the forecast period.

By product type, the orthopedic implants segment is expected to lead the market.

Rising emphasis on minimally invasive surgical procedures and increasing prevalence of orthopedic conditions are driving market expansion.

Johnson & Johnson MedTech, Medtronic plc., Stryker Corporation, Zimmer Biomet Holdings, Inc., and Abbott Laboratories are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 115

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us