Military Transmit and Receive Module Market Size, Share & Industry Analysis, By Component (Transmitter Modules, Receiver Modules, Transceiver Modules (T/R Combined), Power Amplifier Modules, Phase Shifters, and Others), By Technology (Gallium Arsenide (GaAs), Gallium Nitride (GaN), Silicon-based, Analog Technology, and Digital Technology), By Frequency (Single Band and Multi Band), By Power Output, By Module Architecture, By Size (Small, Medium, and Extra Large), By Deployment Mode, By Application, By Platform, By End User, and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

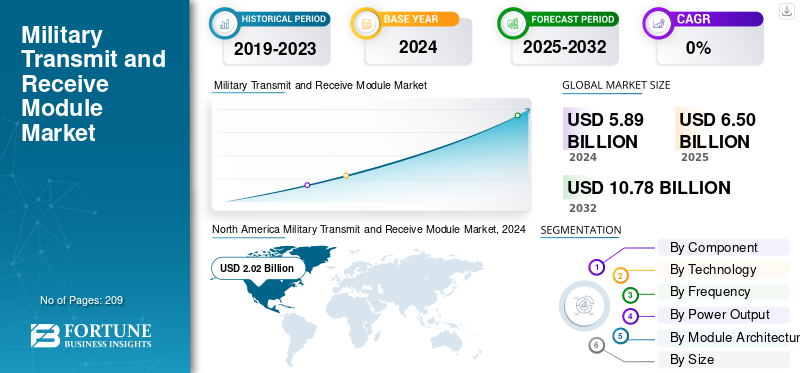

The global military transmit and receive module market size was valued at USD 6.5 billion in 2025. The market is projected to grow from USD 6.85 billion in 2026 to USD 12.16 billion by 2034, exhibiting a CAGR of 7.40% during the forecast period. North America dominated the military transmit and receive module market with a market share of 34.10% in 2025.

The military transmit and receive (T/R) module combines the transmitter unit responsible for sending radio waves and the receiver unit that detects incoming or reflected signals, usually in conjunction with power amplification and signal conditioning elements. It is a critical component of active electronically scanned array (AESA) radars, allowing for instant beam steering without mechanical motion, thus improving radar responsiveness and precision.

Military transmit and receive modules are the central part of cutting-edge defense electronics, providing superiority in detection, secure communication, and electronic warfare. Technological advancements, particularly in GaN semiconductors, have transformed these modules into more powerful, compact, and efficient radars. The complexity and size of today's military systems, coupled with the rising need for multi-domain interoperability and fast adaptability, fuel strong market expansion.

The transition from Gallium Arsenide (GaAs) to Gallium Nitride (GaN) technology in T/R modules significantly enhanced power density, efficiency, and thermal handling, enabling modules to provide more transmit power in a reduced size and longer life. This results in better radar range, resolution, and multi-functionality essential for contemporary military requirements.

Top military transmit and receive module companies such as Northrop Grumman, Lockheed Martin Corporation, L3Harris Technologies, Inc., Thales Group, and Raytheon use innovation, strategic investment, and scalable manufacturing to extend their leadership in this dynamic and strategically critical market sector. Their products shape future secure communication & radar capability and enable armed forces with a decisive tactical advantage in rapidly changing threat environments.

Download Free sample to learn more about this report.

Military Transmit and Receive Module Market Key Takeaways

- 2025 Market Size: USD 6.5 billion

- 2026 Market Size: USD 6.85 billion

- 2034 Forecast Market Size: USD 12.16 billion

- CAGR: 7.40% from 2026-2034

- North America dominated the military transmit and receive module market with a 34.10% share in 2025.

- Transceiver Modules (T/R Combined) accounted for a 43.57% share in 2026.

- Gallium Arsenide (GaAs) technology held a 37.22% share in 2026.

North America

North America generated USD 2.22 billion in 2025 and is projected to reach USD 2.33 billion in 2026.

Europe

Europe accounted for USD 1.27 billion in 2025 and is projected to reach USD 1.35 billion in 2026.

Asia Pacific

Asia Pacific recorded USD 1.77 billion in 2025 and is expected to grow to USD 1.89 billion in 2026.

U.S.

The market is projected to reach USD 2.19 billion by 2026.

Japan

The market is projected to reach USD 0.19 billion by 2026.

Read More

Market Dynamics

Market Drivers

Growing Use of Gallium Nitride Technology Revolution and Semiconductor Advancement Significantly Drives Market Growth

The shift in paradigm from conventional Gallium Arsenide (GaAs) to Gallium Nitride (GaN) semiconductor technology is a transformative force driving the military transmit and receive module market growth. GaN technology provides higher power density (5-10 times more than GaAs), better thermal management, and higher efficiency, allowing radar systems to realize extended detection range, improved resolution, and compact form factors essential for contemporary military use. Large defense companies are quickly embracing GaN-based solutions, such as Raytheon's new APG-82(V)X radar system, incorporating GaN technology for improved fire control and electronic warfare.

- For instance, in June 2025, New fabrication processes developed by MIT researchers integrate high-performance GaN transistors into standard silicon CMOS chips for the first time, introducing faster, energy-efficient electronics. This technology is big by addressing critical Size, Weight, and Power (SWaP) constraints in unmanned platforms, space-based systems, and portable military equipment while also allowing multi-function capabilities previously impossible using legacy semiconductor materials.

Market Restraints

Manufacturing Complexity and High Development Costs Can Hinder Market Growth

The military T/R module market is impacted heavily by rising production expenses and integration difficulties with complex technology, with automotive GaN-based systems requiring premium pricing to more mature technologies such as intricate fabrication needs and tough military-grade requirements. Next-generation T/R module development mitigates heavy R&D expenditures over USD 500 million annually from top players, while fulfilment of military standards for automotive reliability, electromagnetic compatibility, and environmental hardness introduces layers of expense and complexity.

The shift from hardware-centric to software-configured radar architectures imposes further integration headaches, prompting defense contractors to redesign established supply chains and manufacturing processes tuned to vertical integration models. Electronic component shortages continue through 2025, with semiconductor lead times continuing to be unpredictable despite gains over the crisis highs of 2022. High fabrication costs related to advanced materials, specialized fabrication facilities, and tight quality control requirements constrain market penetration, benefiting primarily larger defense contractors and more mature market entrants.

Market Opportunities

Growing Development of Software-Defined Radar and Adoption of Artificial Intelligence Integration Catalyze Market Growth

Software-defined radar architectures combined with artificial intelligence offer unprecedented opportunities for T/R module innovation. This innovative combination will now enable adaptive frequency management, autonomous threat recognition, and instantaneous electronic warfare countermeasures. The AI-powered airborne radar of China demonstrated 99% tracking accuracy against sophisticated electronic jamming in 2025. Cognitive radar dynamically alters frequencies, beam directions, and waveforms to sidestep interference.

Northrop Grumman's development in June 2025 of ML algorithms for the EA-18G Growler electronic attack suite, which is expected to be released in 2025, is an example of this trend toward cognitive electronic warfare systems. Model-based design techniques support complete digital twins during T/R module development, shortening development time and expensive iterations while improving system reliability.

Market Challenges

Regulatory Compliance and Cybersecurity Integration Can Hamper Market Growth

Military transmit and receive module producers work within increasingly complicated regulatory environments that blend standard ITAR/EAR export controls with new cybersecurity needs and environmental standards. Cumbersome military requirements for electromagnetic compatibility, environmental hardness, and operational security require exhaustive testing and certification procedures that add significantly to development time and cost. The incorporation of AI and machine learning features creates new cybersecurity threats in the form of adversarial attacks on algorithms that may invalidate decision-making or produce false threat analyses.

Defense institutions should weigh operational benefits of AI integration against strong cyber-resilience capabilities, with T/R modules that embed sophisticated encryption, secure booting procedures, and tamper-resistant hardware.

Military Transmit and Receive Module Market Trends

Miniaturization and Multi-Function Integration in Military Equipment for Different Applications Boost Market Growth

The technology environment promotes exuberant miniaturization and multifunctional integration, with T/R modules achieving unparalleled power density through innovative packaging technologies such as Low-Temperature Co-fired Ceramic (LTCC), Multi-Chip Modules (MCM), and System-in-Package (SiP) architectures. Hensoldt's Space T/R modules feature standardized modular configurations tested for space use, proven to contain radiation-hardened components qualified against multipaction and RF corona discharge. Meanwhile, CAES provides ultra-high-density, miniaturized radar modules for hypersonic use, boasting shock-resistant performance exceeding 100,000g.

Technological progress focuses on broadband frequency coverage and multi-spectrum capabilities, where future-generation T/R modules cover multiple frequency bands simultaneously to enable various mission applications on a single platform. L3Harris' 4W T/R Power Module offers 6-18 GHz wideband coverage for phased array and electronic warfare, whereas Qorvo's QPF0219 combines 2-18 GHz frequency coverage and 10W saturated output power with GaN-on-SiC technology.

Download Free sample to learn more about this report.

Segmentation

By Component

Increase Preference for Integrated Multi-function Capabilities Boosted Transceiver Modules (T/R Combined) Segment Growth

The market is classified by component into transmitter modules, receiver modules, transceiver modules (T/R combined), power amplifier modules, phase shifters, and others.

Transceiver Modules (T/R Combined) represent the fastest-growing segment and the dominant portion of the market, will accounting for approximately 43.57% of the market share in 2026. In general, the commanding position of this segment reflects the industry's strategic shift toward integrated multi-function capabilities, which enable simultaneous transmit-receive operations within compact form factors that are increasingly adopted in modern military platforms, driven by strict SWaP requirements. Additionally, the integrated transceiver architectures eliminate redundant RF pathways, thereby reducing component count and lowering manufacturing costs. This simplification leads to increased system reliability through simplified integration with digital beamforming processors and adaptive waveform generators.

- June 2025: Sivers Semiconductors won a contract from aiRadar Inc. to develop an advanced 28GHz Ka-band antenna module based on a TRX BF02 beamforming transceiver chip, supporting high-performance radar deployments with 16TX+16RX channel capability, demonstrating accelerated commercial-to-defense technology transfer.

Power amplifier modules are the second-fastest growing segment, with a projected CAGR of 7.9% over the forecast period. Growth reflects accelerating demand for high-power GaN-based solutions essential for next-generation AESA radar systems. Rapid segment expansion is due to the technological superiority created by GaN-on-SiC power amplifiers, which provide up to 3-5 times higher power density than legacy LDMOS technologies, allowing for compact amplifier designs capable of supporting high-performance transmit outputs (500W-2kW per module array) critical for long-range surveillance and multi-target tracking missions.

To know how our report can help streamline your business, Speak to Analyst

By Technology

Most Superior Performance Characteristics and Military Advantages of Gallium Nitride (GaN) Technology Catalyze Segmental Growth

The market is classified by technology into Gallium Arsenide (GaAs), Gallium Nitride (GaN), silicon-based, analog technology, and digital technology.

Gallium Nitride (GaN) technology is the fastest-growing segment in the market, showing an exceptional compound annual growth rate of 8.8% over the forecast period of 2026-2034. The significant growth in the segment reflects the paradigm shift from the legacy Gallium Arsenide technology toward high-power density semiconductor solutions driven by AESA Radar modernization programs, space-based surveillance system expansion, and emerging hypersonic missile defense requirements that drive unprecedented power efficiency and thermal performance. The GaN technology enjoys 5-10 times superior power density in comparison to traditional GaAs devices while operating at identical frequency bands, hence compacting T/R module designs to support Size, Weight, and Power optimization for unmanned platforms, space payloads, and next-generation fighter aircraft with distributed aperture arrays.

- August 2025: Agnit Semiconductors, India's first vertically integrated GaN ecosystem player, achieved a major milestone with the signing of the Ministry of Defence iDEX, the 300th iDEX contract milestone, for the design and development of advanced GaN semiconductors critical for next-generation wireless transmitters in defense radars and electronic warfare jammers, with volume production expected within 12 months.

Gallium Arsenide (GaAs) technology maintains a dominant installed base, will accounting for approximately 37.22% of the military transmit and receive module market share in 2026. The dominance is driven by telecommunications, defense, and automotive radar sectors needing exceptional noise performance, radiation tolerance, and temperature stability over extreme operating environments. Gallium Arsenide HEMT technology also gives superior noise figure performance of 0.5-1.5 dB LNA configurations, fundamentally superior to GaN alternatives for precision receiver applications requiring exceptional signal sensitivity and low-noise amplification characteristics that accelerate the market growth.

By Frequency

Multi Band Segment to Lead Market Due to Frequency Agility and Electronic Warfare Resilience

The market is classified by frequency into single band and multi band.

The multi-band transceiver module will witness the fastest growth, with a CAGR of 8.4%. This growth is driven by paradigm shifts toward software-defined, frequency-agile radar architectures that enable adaptive operation across contested electromagnetic environments. Multi-band technology features integrated TR modules spanning L/S/C-band (1-8 GHz continuous coverage) with modular architectures that allow for rapid frequency switching, waveform reconfiguration, and simultaneous multi-mission operation without platform-level hardware modification.

- July 2025: Analog Devices presented the Apollo MxFE AD9088-8T8R multi-band phased array radar transceiver at the International Microwave Symposium, allowing agile multiband operation through a wideband RF front-end that covers up to 55 GHz to support next-generation modular AESA architectures with unprecedented frequency flexibility.

Single-band transmit and receive module systems will hold the 57.59% market share in 2026. Single-band architecture concentrates performance capabilities on optimized performance within specific frequency allocations: L-Band (1-2 GHz), S-Band (2-4 GHz), X-Band (8-12 GHz), and Ku-Band (12-18 GHz), with specialized design allowing superior performance metrics: lower noise figure (in LNA implementations), higher power output density, and optimized impedance matching across narrower frequency spans compared to wideband alternatives.

By Power Output

Growing Solid-State Power Amplifier Technology Transition to Boost Very High Power (>1000W) Segment Expansion

The market is classified by power output into medium power (10W-100W), high power (100W-1000W), and very high power (>1000W).

The very high power (>1000W) is the fastest-growing segment, with a CAGR of 9.0% from 2026 to 2034, driven by strategic ballistic missile defense systems, long-range air surveillance radar modernization, and emerging hypersonic threat detection requirements. Industrial maturation through the achievement of Manufacturing Readiness Level 10 by means of GaN-on-SiC technology enables domestic production scaling in support of DoD manufacturing readiness objectives; Allied procurement standardization of this segment drives market growth.

- In October 2025, Lockheed Martin successfully promoted the AN/TPY-4 radar featuring 1,152 GaN T/R modules at DSEI 2025, providing a 1,000+ km detection range in Focused Stare Mode, securing the contract award by Sweden in June 2025, the third NATO nation selection. With Sweden receiving the first unit by late 2027, this establishes momentum toward the consolidation of the NATO standard ground-based surveillance architecture.

The high power (100W-1000W) segment maintains the dominant market position, will commanding approximately 44.07% of the global market share in 2026. High-power module dominance encompasses naval AESA radar standardization, fighter aircraft AESA systems, and ground-based air defense systems such as the U.S. Navy SPY-6 family deploying 37-57 Radar Modular Assemblies per destroyer array with 200W average power per RMA; F-22, F-35, Gripen, Typhoon requiring 100-200W module densities per platform for simultaneous multi-target engagement; Patriot, THAAD, S-400, BUK variants employing 150-400W module configurations. Segmental growth is driven by operational maturity, achieved through decades of deploying GaAs-based T/R modules, establishing supply chain ecosystems, and developing manufacturing expertise, as well as field reliability characterization, which enables competitive pricing, rapid procurement, and inventory availability to support military sustainment cycles.

By Module Architecture

Modular/Multi-Channel Segment to Lead Due to Scalability, Platform Standardization, Field Replaceability and Operational Advantages

The market is classified by module architecture into unitary/single channel, modular/multi-channel, solid-state, and multi-mission.

The modular/multi-channel transmit and receive module architecture represents the fastest-growing and dominant market segment, commanding a market share of approximately 36.89% worth USD 2.17 billion in 2024 and growing at a CAGR of 8.8% through 2032, driven by the scalability, field replaceability, and fast configurability needs of next-generation phased array radars. Multi-channel architecture will include integrated Quad Transmit Receive Modules (QTRM) using 4-8 T/R channels with associated DC power distribution, digital control electronics, and factory calibration within line-replaceable units that enable flexibility across diverse operational requirements.

- For instance, in July 2025, AXISCADES, the parent company of Mistral Solutions, got several defense orders valued at over Rs 680 crores, including the S-Band Octal DTRM/DRM contract for Rs 150 crore production value, 500 units over 2-4 years and development of Surveillance Radar DTM/DRM, for Rs 200 crore production quantity: 400 units, showcasing India's fast-tracking indigenous multi-channel T/R module manufacturing.

The second fastest-growing segment represents the solid-state transmit and receive module architecture, which is projected to see a CAGR of 8.1% through 2032, expanding from USD 1.64 billion in 2024 to USD 3.16 billion by 2032, driven by the fundamental technology transition from legacy magnetron and traveling-wave tube (TWT) vacuum technologies toward semiconductor-based power amplification, offering improved reliability, superior operational lifespan, and graceful degradation characteristics.

By Size

Medium (100-300mm) Segment Dominates Due to Platform Standardization and Operational Scalability

The market is classified by size into small (<100mm), medium (100-300mm), and extra large (>500mm).

Medium-size, within 100-300mm dimensions, transmit and receive modules represent both the fastest growth and dominant market segment, accounting for about 49.32% market share worth USD 2.90 billion in 2024, while developing at a CAGR of 8.3% through 2032 to reach USD 5.64 billion by 2032, driven by universal adoption across next-generation AESA radar platforms and modular architecture standardization. The dominance of medium-size T/R modules reflects an optimized balance between power density that enables high-performance radar operations, thermal management that enables sustained operation without complex cooling infrastructure, and physical dimensions that allow dense element packing, thus supporting thousands of modules per platform array.

- For instance, in November 2025, Sivers Semiconductors secures a contract from aiRadar Inc. for the development of an advanced 28GHz Ka-band antenna module based on the TRX BF02 beamforming transceiver chip to support high-performance radar deployment with 16TX+16RX channel capability in ultra-compact form factor (150x80x25mm), demonstrating acceleration in technology transfer from commercial to defense for medium-sized module development.

The Extra Large (>500mm) sub-segment is estimated to be the second fastest-growing segment, projected at a CAGR of 7.4% through 2032, growing from USD 0.6 billion in 2024 to USD 1.8-2.4 billion by 2033, considering modernization programs for long-range air surveillance radars, ballistic missile defense system expansion, and emerging space-based surveillance constellations. The dominance of extra-large modules would include strategic early warning radar, such as Lockheed Martin AN/TPY-4 with a large-format array of 1,152 GaN radiators, deployments of 3DELRR by the U.S. Air Force, and NATO integrated air defense command centers that need 1,000+ km detection ranges against emerging ballistic and hypersonic threats.

By Deployment Mode

Platform Transportability and Rapid Deployment Capability to Fuel Mobile/Transportable Segment Growth

The market is classified by deployment mode into fixed/stationary, mobile/transportable, and man-portable.

Mobile/transportable transmit and receive module systems represent the fastest-growing deployment segment with a projected CAGR of 8.3% through 2032, expanding from USD 2.34 billion in 2024 to USD 4.57 billion by 2032, driven by military doctrine evolution emphasizing rapid deployment, expeditionary operations, and distributed defense architectures reducing infrastructure dependencies. Mobile/transportable deployment dominance reflects strategic requirement for rapidly-deployable air defense systems capable of 8-15 minute operational setup timelines supporting forward operating bases, contested forward locations, and dynamic threat environments requiring system mobility across diverse terrains.

- For instance, in March 2025, the Ministry of Defence India signed a USD 2.74 million contract with BEL for 18 Ashwini LLTR systems featuring solid-state T/R modules with 15-minute operational deployment capability, 4-person operating teams, helicopter underslung transport, and C-130 air transportability supporting expeditionary operations across India's diverse geographic terrain.

The fixed and stationary installation of transmit and receive modules remains the dominant market position, holding about 48.90% of the global market share, valued at around USD 2.87 billion in 2024, with a stable CAGR at 6.8% through 2032. This is indicative of the entrenched deployment across strategic defense installations, air traffic control facilities, and ballistic missile defense command centers where permanent infrastructure investments have to be made, with operational service life extending beyond several decades.

By Application

Increasing Electromagnetic Contested Environment to Bolster Electronic Warfare Segment Growth

The market is classified by application into Radar (AESA/MF‑R), Electronic Warfare, Military Communications & Datalinks, High‑Power Microwave, and Intelligence, Surveillance & Reconnaissance (ISR).

Electronic Warfare will be the fastest-growing transmit and receive segment, with a projected CAGR of 9.9% through 2025-2032, growing from USD 1.00 billion in 2024 to USD 2.19 billion by 2032, driven by the increasing electromagnetic contested environment, proliferation of advanced jamming systems, and integration of AI-enabled cognitive electronic warfare capabilities. The EW segment acceleration reflects a fundamental doctrine evolution toward multi-domain warfare that places emphasis on electronic attack, electronic protection, and electronic warfare coordination integrated within unified command architectures, which require wideband high-power T/R modules to enable multiple-frequency-band jamming simultaneously.

- For instance, in October 2025, Northrop Grumman demonstrated the Integrated Vertical Electronic Warfare Suite (IVEWS) for F-16 fighters. The ultra-wideband T/R module architecture enables simultaneous multi-band radar operation and electronic warfare coordination on a pulse-to-pulse basis, detecting and countering rapidly frequency-hopping adversary threats while maintaining full radar functionality.

The Radar (AESA/MF‑R) segment accounts for around 53.50% of the global military transmit and receive module market share, which will amount to around USD 3.14 billion in 2024, while growing stably at a CAGR of 6.6% through 2032, reflecting growing demands for integrated surveillance-tracking-engagement systems within single-platform apertures. T/R modules are around 40-50% of the AESA system total cost, making these components fundamental value drivers and critical performance limiters for advanced radar systems.

By Platform

Space-based Segment to Propel Segment Growth Due to Satellite Constellation Deployment

The market is classified by platform into ground-based systems, naval/maritime, airborne, missile/munition systems, and space-based.

Space-based transmit and receive module systems represent the fastest-growing segment in this platform, with a projected CAGR of 10.8% through 2032, from USD 0.23 billion in 2024 to USD 0.54 billion by 2032, driven by accelerating satellite constellation deployment, emerging space situational awareness requirements, and a strategic imperative for persistent global surveillance capabilities. This growth of space-based T/R modules reflects the evolution of fundamental military doctrine toward space-enabled operations that create unprecedented demand for compact, radiation-hardened T/R modules supporting SAR, communication terminals, and space surveillance functions.

- For instance, in June 2024, ESA placed contracts with Airbus Defence and Space, OHB, and Thales Alenia Space to develop zero-debris LEO satellite platforms that comply with the Zero Debris standard, which is enabled by advanced radiation-hardened T/R modules for sustainable space operations and emerging space sustainability regulations.

The airborne transmit and receive module systems dominate about 30.94% of the global military T/R module market, valued at about USD 1.82 billion in 2024, while sustaining a 7.9% CAGR through 2032, reflecting entrenched deployment across fighter aircraft, bomber platforms, surveillance aircraft, and unmanned aerial vehicles. It is regarded as a segment showcasing solid market fundamentals driven by continuous fighter jets modernization and next-generation platform development programs. Fighter aircraft AESA radar dominance includes operational platforms such as F-22 Raptor (1,500+ T/R modules per aircraft), F-35 Lightning II APG-81 with comparable density, Gripen E/F, Eurofighter Typhoon E-SCAN, Rafale F3/F4 with 2,000+ modules representing established procurement platforms generating sustained T/R module demand through production runs spanning 2025-2050.

By End User

Unprecedented Defense Spending Emphasis Boosted Defense Departments/Military Segment Growth

The market is classified by end user into defense departments/military, defense equipment OEMs, private military contractors, and government agencies.

The Defense Departments/Military T/R module market share is dominated by Defense Departments and Military end-users with 67.49% valued at USD 3.97 billion in 2024, accelerating at an unprecedented CAGR of 7.8% through 2032, driven by unprecedented defense spending emphasis, modernization programs, and direct government procurement expanding from USD 2,443 billion global military expenditure in 2023 toward USD 2,750+ billion by 2030. The growth trajectory of the military as an end-user reflects a fundamental transformation of the procurement pattern toward direct government-to-manufacturer contracting, bypassing the traditional prime contractor intermediary setup and establishing military services as the primary stakeholder in T/R module technology decisions and acquisition timelines.

- For instance, in November 2024, Hyderabad-based Unistring Tech Solutions (UTS) won a USD 4.32 million contract from an Indian public sector unit for the advanced AESA radar system to detect/track 100 simultaneous drone targets, marking the latest trend in emerging indigenous military procurement patterns, which empower specialist defense technology startups and mid-cap integrators.

Defense Equipment Original Equipment Manufacturers (OEMs) are predicted to be the second fastest-growing sub-segment with a CAGR of 7.7%. OEM growth trajectory reflects competitive strategy emphasizing supply chain control, proprietary design differentiation, and margin capture across the full value chain from component development through system-level integration. Prime contractors such as Raytheon, Northrop Grumman, Lockheed Martin, Leonardo, Thales, BAE Systems, and regional competitors command contracts that create institutional leverage, enabling vertical integration investments amortized across large production volumes.

Military Transmit and Receive Module Market Regional Outlook

By region, the market is divided into North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America.

North America

North America Military Transmit and Receive Module Market, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

In 2025, North America generated USD 2.22 Billion, contributing 34.14% to global market revenue, and is projected to grow to USD 2.33 Billion in 2026. The region's leading position is due to its high expenditure on defense, with the U.S. having the highest military expenditure globally, at around USD 886 billion annually. Other factors include the superior technological upgradation of EW capabilities on F/A-18 aircraft by world-class defense contractors such as Raytheon, Northrop Grumman, and Lockheed Martin, which drives regional growth. The U.S. market is projected to reach USD 2.19 billion by 2026.

The SPY-6 radar modernization program is the cornerstone of U.S. Navy regional growth, deploying four variants across more than 31 Navy ships over the next decade, and driving billions of dollars in procurement opportunities for T/R modules across multiple variants. Continuous investment in research and development by leading defense contractors, with an estimated annual spend of over USD 500 million, drives innovation in GaN technology, AI integration, and multi-mission radars. In June 2025, Raytheon was awarded a USD 536 million contract by the U.S. Navy for integration and production support of SPY-6, while an additional contract worth USD 646 million covered additional hardware production to further modular radar deployment across the naval fleet.

Asia Pacific

Asia Pacific recorded a market size of USD 1.77 Billion in 2025, capturing 27.18% of the global market share, and is projected to reach USD 1.89 Billion in 2026, driven by rapid military modernization across China, India, Japan, and South Korea, with combined defense expenditures surpassing USD 510 billion annually. India's Atmanirbhar Bharat and Make in India initiatives are driving indigenous radar development, with the DRDO's Ashwini AESA radar program being a highly representative example. This initiative reduces dependencies on foreign vendors while creating substantial indigenous T/R module manufacturing capacity through BEL, Mistral Solutions, and Cyient. Military technology advancements in China emphasize stealth-penetrating radars (YLC-2E/YLC-8E), the production of quantum radar starting in October 2025, and the integration of GaN-based AESA systems for the J-20 fighter jets, positioning China as a technological leader in advanced T/R modules. The Japan market is projected to reach USD 0.19 billion by 2026, while the China market is projected to reach USD 0.8 billion by 2026, and the India market is projected to reach USD 0.31 billion by 2026.

Europe

The Europe market accounted for USD 1.27 Billion in 2025, representing 19.58% of the global industry, and is expected to reach USD 1.35 Billion in 2026, driven by NATO's modern defense programs, geopolitical tensions stemming from the Russia-Ukraine conflict, and collaborative defense initiatives focused on interoperability and technological sovereignty. The European Defence Readiness Roadmap 2030 (announced October 2025) commits significant investment to close capability gaps; the focus will be on European Air Shield, Eastern Flank Watch, and the European Drone Defence Initiative, all of which require state-of-the-art radar and T/R module technologies. Leonardo's ECRS Mk2 radar development for the Eurofighter Typhoon represents its flagship technological achievement, featuring wideband GaN-based T/R modules with multi-function electronic warfare capabilities and synthetic aperture radar imaging. The critical design review was achieved in June 2024, and initial operating capability is expected by 2030. The UK market is projected to reach USD 0.25 billion by 2026, while the Germany market is projected to reach USD 0.31 billion by 2026.

Middle East & Africa

The Middle East & Africa market generated USD 0.93 Billion in 2025, representing 14.24% of the global market landscape, and is expected to reach USD 0.96 Billion in 2026, driven by regional geopolitical tensions, increased defense budgets averaging 3.9% of GDP allocation, and emerging procurement initiatives in rich GCC countries. Saudi Arabia remains the largest spender in this region, with more than an annual USD 85+ billion defense budget, ranking fifth in the world, especially in technologically advanced air defense radar systems for ballistic and cruise missile defenses; thus, the recent procurement of the radar system for Hanwha M-SAM II clearly highlighted the preference for high-performance AESA technologies.

Latin America

Moderate but accelerating growth is seen in the Latin America accounted for USD .32 Billion in 2025, representing 4.86% of the global market share, and is projected to reach USD .32 Billion in 2026, since defense spending is generally concentrated in Brazil, Colombia, Mexico, and Peru, which are pursuing air force modernization and border security upgrades. Brazil has a multi-year procurement program for 36+ Gripen fighters, featuring technologically advanced radar and electronic warfare suites, which drives substantial demand for T/R modules through both Saab-Embraer technology transfer arrangements and indigenous capability development at Embraer facilities. At the same time, Colombia is enhancing its air defense capabilities through work with Saab Giraffe radar systems and negotiations for Gripen fighters, amidst regional narcotics trafficking threats and geopolitical tensions.

COMPETITIVE LANDSCAPE

Key Market Players

The global military transmit and receive module market is considered moderately concentrated, with a competitive structure marked by bifurcation between established defense prime contractors at the high-value, complex system integration level and specialized semiconductor and RF component manufacturers focused on niche segments with technological innovations.

Market concentration reflects high technological barriers to entry, stringent military qualification requirements, and substantial R&D investment thresholds of over USD 500 million annually across leading players. The competitive intensity also varies significantly depending on the segment: Defense and aerospace applications generally feature long-term contracts, established customer relations, and high-performance switching costs, whereas commercial applications have lower entry barriers and much more dynamic competitive dynamics.

Merger and acquisition activity remains moderate, with larger players making strategic moves to expand product portfolios, capture key GaN manufacturing capabilities, and solidify market positions. The prime contractors in defense maintain vertical integration strategies, controlling critical supply chain elements from semiconductor fabrication through system-level integration to build formidable competitive moats against any emergent challengers.

The geographic concentration of centers is primarily in North America and Europe, due to advanced technological capabilities and substantial defense budgets. In contrast, Asia Pacific has recently become a fast-growing region, driven by the military modernization programs of China, India, Japan, and South Korea, and indigenous manufacturing initiatives.

List of Key Military Transmit and Receive Module Companies Profiled

- Aselsan A.Ş. (Turkey)

- BAE Systems plc (U.K.)

- Cobham Advanced Electronic Solutions (U.S.)

- Cyient Limited (India)

- Elbit Systems Ltd. (Israel)

- Hanwha Systems (South Korea)

- Hensoldt AG (Germany)

- Israel Aerospace Industries (IAI) (Israel)

- Kyocera Corporation (Japan)

- L3Harris Technologies, Inc. (U.S.)

- Leonardo S.p.A. (Italy)

- Lockheed Martin Corporation (U.S.)

- Mistral Solutions Pvt. Ltd. (India)

- Mitsubishi Electric Corporation (Japan)

- National Chung-Shan Institute of Science and Technology (Taiwan)

- Northrop Grumman Corporation (U.S.)

- Raytheon (RTX Corporation) (U.S.)

- Saab AB (Sweden)

- Thales Group (France)

KEY DEVELOPMENTS

- October 2025: The U.S. Army has awarded Saab a contract worth USD 46 million for the supply of Giraffe 1X short-range 3D radars supporting security cooperation partners. Compact X-band AESA radar features 360°/1-second refresh capability, detecting small drones up to 4 km and air targets 75+ km. Deliveries start in 2026.

- October 2025: Saab secured a contract from the NATO Support and Procurement Agency (NSPA) to extend the lifespan of the Arthur radar systems used by the Spanish Army. The estimated value of the contract is around USD 51.2 million.

- October 2025: The German government chose Raytheon to supply the SPY-6(V)1 radar, built by Raytheon, for installation on eight F127 frigates under a foreign military sales contract with the U.S. Navy. This contract will also provide extensive support and services to tailor the radar to fit the ship's design, marking Germany as the first foreign buyer of the SPY-6.

- September 2025: Northrop Grumman entered into memoranda of understanding with three companies based in Taiwan to provide the AN/TPS/78 Advanced Capabilities Radar. The agreements include Ramatek Company, Champion Auto, and Vivian and Vincent International Trading Company Ltd., which will collaborate with Northrop Grumman to facilitate the deployment of the radar system in Taiwan.

- August 2025: Northrop Grumman successfully conducted its initial trial of the Deep Space Advanced Radar Capability (DARC), demonstrating the multi-antenna radar's capability to monitor multiple satellites. The test featured seven of the anticipated 27 parabolic dish antennas that comprise the DARC system and validated that the idea of coordinating multiple antennas to function as a single, larger antenna is indeed effective.

REPORT COVERAGE

The global military transmit and receive module market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the global market trends and market dynamics expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.4% from 2026-2034 |

| Unit | USD Billion |

|

Segmentation |

By Component

By Technology

By Frequency

By Power Output

By Module Architecture

By Size

By Deployment Mode

By Application

(ISR) By Platform

By End User

|

|

Region

|

North America (By Component, By Technology, By Frequency, By Power Output, By Module Architecture, By Size, By Deployment Mode, By Application, By Platform, By End User, By Country)

Europe (By Component, By Technology, By Frequency, By Power Output, By Module Architecture, By Size, By Deployment Mode, By Application, By Platform, By End User, By Country)

Asia Pacific (By Component, By Technology, By Frequency, By Power Output, By Module Architecture, By Size, By Deployment Mode, By Application, By Platform, By End User, By Country)

Middle East & Africa (By Component, By Technology, By Frequency, By Power Output, By Module Architecture, By Size, By Deployment Mode, By Application, By Platform, By End User, By Country)

Latin America (By Component, By Technology, By Frequency, By Power Output, By Module Architecture, By Size, By Deployment Mode, By Application, By Platform, By End User, By Country)

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 6.5 billion in 2025 and is projected to reach USD 12.16 billion by 2034.

In 2025, the market value in North America stood at USD 2.22 billion.

The market is expected to exhibit a CAGR of 7.4% during the forecast period of 2026-2034.

The Transceiver Modules (T/R Combined) segment is expected to hold the highest CAGR over the forecast period.

The growing use of gallium nitride technology revolution and semiconductor advancement significantly drives the market growth.

Aselsan A.Ş. (Turkey), BAE Systems plc (U.K.), Cobham Advanced Electronic Solutions (U.S.), Cyient Limited (India), Elbit Systems Ltd. (Israel), Hanwha Systems (South Korea), Hensoldt AG (Germany), and Israel Aerospace Industries (IAI) (Israel) are some of the top players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 209

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us