Naval Vessels Electronic Countermeasures (ECM) Market Size, Share & Industry Analysis, By Platform Type (High-End Surface Combatants, Mid-Tier Combatants, Capital/Large-Deck Vessels, and Other), By Component (Sensors and Receive Chain, Effectors, Countermeasure Hardware, Mission Electronics, Software and Support, and Others), By Capability (Radar Jamming, Deception Jamming, Decoy Countermeasures, and Integrated Soft-Kill Suite), By Fit Type (Line-fit and Retrofit), By End User (Navy and Coast Guard/Maritime Security), and Regional Forecast, 2026-2034

Naval Vessels Electronic Countermeasures (ECM) Market Size and Future Outlook

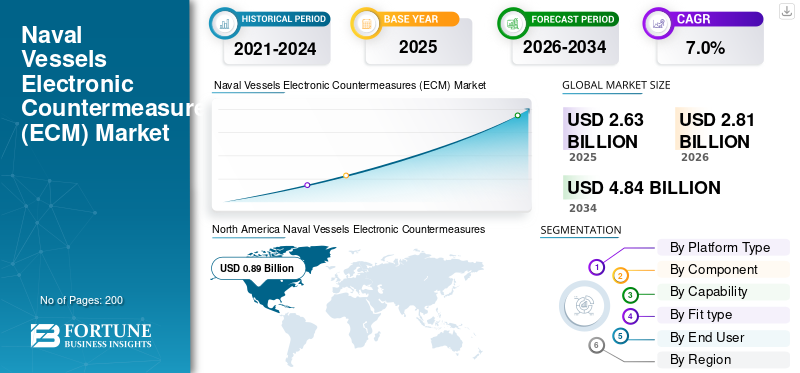

The Naval Vessels Electronic Countermeasures (ECM) market size was valued at USD 2.63 billion in 2025. The market is projected to grow from USD 2.81 billion in 2026 to USD 4.84 billion by 2034, exhibiting a CAGR of 7.0% during the forecast period. North America dominated the naval vessels electronic countermeasures (ecm) market with a market share of 33.84% in 2025.

The global naval vessels electronic countermeasures (ECM) market covers shipborne electronic warfare systems used to detect, jam, deceive, and divert hostile sensors and weapon-guidance systems targeting naval vessels. The market is being supported by rising defense budgets, a stronger focus on fleet survivability, and growing demand for electronic attack, electronic support, and signals intelligence capabilities. The growth is especially visible across North America, Asia Pacific, and the Middle East, where naval modernization programs are actively driving market growth in the broader electronic warfare market.

Key players in the market are Lockheed Martin, Northrop Grumman, BAE Systems, L3Harris Technologies, and Elbit Systems. These companies are driving the growth of the market through system integration, upgrade programs, and an advanced defense supply chain. Their developments in modular electronic warfare systems, software-led upgrades, and ship protection solutions are resulting in expanded capability and competitive market share due to stronger technology positioning over the forecast period.

Download Free sample to learn more about this report.

Naval Vessels Electronic Countermeasures (ECM) Market Trends

Integration of Layered Soft-Kill Electronic Warfare Architecture is Emerging as a Major Market Trend

A major trend in the market is the shift from stand-alone jammers or decoy launchers to integrated soft-kill architectures that connect detection, command-and-control, jamming, and decoy response in one structure. Navies are increasingly looking for systems that can react faster to modern anti-ship missile threats, coordinate multiple countermeasure layers, and be integrated into both current and future surface fleets. This trend is important as it changes ECM from a hardware-heavy defensive add-on into a more networked and software-led combat function, making fleet survivability more adaptive and operationally coherent.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Naval Modernization Programs and Electronic Survivability Requirements are Driving Market Growth

The naval vessels electronic countermeasures (ECM) market growth is rising due to the fast modernization of naval fleets, mainly in the Asia Pacific, North America, and the Middle East. As anti-ship missile threats and radar-guided systems become more advanced, navies are ordering electronic warfare systems that combine electronic attack, electronic support, and signals intelligence for real-time threat response. Increasing defense budgets are supporting procurement of next-generation ECM suites, and integration of these systems into both new build and retrofit programs is significantly driving market growth across the broader electronic warfare market.

In December 2023, the U.S. Navy awarded Northrop Grumman a contract to deliver the Surface Electronic Warfare Improvement Program (SEWIP) Block 3 systems, designed to improve shipboard electronic attack capability against advanced threats, highlighting the role of ECM in naval modernization programs.

MARKET RESTRAINTS

High Integration Complexity and Lifecycle Costs Restrain Market Development

A major restraint in the global market is the complexity of integrating electronic warfare systems with existing naval platforms, particularly in retrofit programs. Moreover, modern ECM requires close-fitting coupling with combat management systems, sensors, and onboard electronics, resulting in an increase in both technical risk and cost. Additionally, lifecycle expenses, which consist of software upgrades, testing, and maintenance, put pressure on defense budgets, particularly in smaller markets, further restraining the market growth.

MARKET OPPORTUNITIES

Expansion of Retrofit and Upgrade Programs Creates Significant Growth Opportunities

A major opportunity in the market lies in the large installed base of aging fleets requiring modernization. Many navies, mainly other than North America, are not replacing platforms at the same pace but are upgrading existing ships with advanced electronic warfare systems. This creates demand for retrofit programs of modular ECM solutions, including capabilities such as electronic attack, electronic support, and signals intelligence. As defense budgets focus on investing in survivability upgrades instead of full platform replacement, the retrofit-driven mandate is driving market growth.

MARKET CHALLENGES

Rapid Evolution of Electronic and Missile Threats Represent Major Market Challenges

The development of electronic and missile threats represents major problems in the current market. Anti-ship systems that use modern technology have become effective in dealing with old-fashioned electronic jamming and decoy techniques. Therefore, electronic warfare systems continue evolving, and original equipment manufacturers (OEMs), including Lockheed Martin, Northrop Grumman, BAE Systems, L3Harris Technologies, and Elbit Systems, need to constantly develop their capabilities in electronic attacks, support, and intelligence. Additionally, it is also important for navies to have up-to-date versions of software and other updates, putting more financial pressure and challenging the market growth.

Impact of Ongoing Conflicts

Ongoing Conflicts are Accelerating Demand for Layered Naval Survivability and ECM Upgrades across Global Fleets

Ongoing conflicts are having a direct impact on the global market by reinforcing how exposed modern warships and commercial shipping routes are to anti-ship missiles, drones, and other electronically guided threats. The conflict environment in and around the Red Sea, combined with broader state-on-state and proxy competition, has pushed navies to place greater emphasis on electronic warfare systems that can detect, disrupt, deceive, and defeat incoming threats in real time. This is increasing the importance of electronic attack, decoy deployment, and integrated soft-kill architectures, while also strengthening the case for faster retrofit cycles and higher survivability spending on major surface combatants.

In March 2024, the U.S. Central Command reported that Houthi forces fired an anti-ship ballistic missile into the southern Red Sea and that U.S. forces also conducted self-defense strikes against two anti-ship cruise missiles assessed as an imminent threat to merchant vessels and U.S. Navy ships.

Segmentation Analysis

By Platform Type

High-End Surface Combatants Segment Dominates the Market Due to the Focus on Advanced Shipborne Electronic Warfare Requirements

Based on platform type, the market is categorized into high-end surface combatants, mid-tier combatants, capital/large-deck vessels, and other.

The high-end surface combatants dominated the market in 2025, because destroyers, advanced frigates, and other top-tier surface warships carry the heaviest burden for radar jamming, deception, decoy coordination, and integrated soft-kill response. These platforms operate in the most threat-dense environments and therefore require more sophisticated electronic warfare systems than lower-tier vessels. They also need higher-value upgrades and deeper system integration, keeping them at the center of ECM spending even as mid-tier combatants expand their role over time.

The mid-tier combatants segment is expected to grow at a CAGR of 8.1% over the forecast period.

By Component

Countermeasure Hardware Dominates the Market Due to the Deployment of Soft-Kill Effects Against Threats

On the basis of component, the market is classified into sensors and receive chain, effectors, countermeasure hardware, mission electronics, software and support, and others.

Countermeasure hardware dominated the global market in 2025, because naval survivability depends heavily on the physical deployment layer, mainly decoy launchers, expendable countermeasure systems, trainable launchers, and associated onboard defensive hardware. While software, mission electronics, and response logic are becoming more important, the hardware layer remains the most noticeable and consistently procured part of many naval ECM programs because it directly supports the ship to deploy soft-kill effects against incoming threats. This keeps countermeasure hardware at the center of investment across both newbuild and retrofit programs.

The software and support segment are expected to show the fastest growth, registering a CAGR of 8.9% over the forecast period.

By Capability

Radar Jamming Dominates the Market Due to its Core Active-Response Function in the Electronic Warfare Industry

The market is further divided by capability into radar jamming, deception jamming, decoy countermeasures, and integrated soft-kill suite.

Radar jamming dominated the global naval vessels electronic countermeasures (ECM) market share in 2025, as it is the main direct and operationally important capability for degrading hostile radar tracking, missile seeker performance, and fire-control effectiveness against naval vessels. Additionally, it is still the backbone of many shipborne electronic warfare systems, especially on major combatants that need to respond quickly in dense electromagnetic environments. Deception, decoys, and integrated soft-kill coordination are gaining relevance; radar jamming continues to hold the largest share because it is the core active-response function in the broader electronic warfare market and remains important to naval survivability programs.

The deception jamming is the fastest-growing segment and is expected to grow at a CAGR of 7.8% across the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Fit Type

Retrofit Segment Led the Market Due to the Installation of Modern Electronic Warfare Systems

Based on fit type, the market is bifurcated into line-fit and retrofit.

The retrofit segment led the global market in 2025. A large share of the world’s naval fleet is aged and needs updates instead of complete replacement. Adding modern electronic warfare systems, such as electronic attack, electronic support, and decoy capabilities, to existing platforms is cost-effective and faster than new build programs. Therefore, navies focus on upgrading older ships with better ECM suites to counter changing threats. This makes retrofit an important factor in boosting growth in the overall electronic warfare market.

The line-fit is the fastest-growing segment in the market and is expected to grow at a CAGR of 8.0% during the forecast period.

By End User

Navy Segment Led the Market Due to the Installation of Advanced Ship-Borne Electronic Warfare Systems

Based on end user, the market is segmented into navy and coast guard/maritime security.

The navy segment held the largest naval vessels electronic countermeasures (ECM) market share in 2025, as advanced ship-borne electronic warfare systems are mainly installed on naval combatants in high-threat maritime areas. Destroyers, frigates, corvettes, aircraft carriers, and other warships need an integration of electronic attack, electronic support, decoy control, and enhanced survivability compared to coast guard or maritime security fleets. Therefore, most ECM spending is focused on navies; in these areas, mission intensity, platform complexity, and fleet modernization needs are the greatest.

The coast guard/maritime security segment is expected to show the fastest market growth, registering a CAGR of 8.8% over the forecast period.

Naval Vessels Electronic Countermeasures (ECM) Market Regional Outlook

By region, the market is categorized into North America, Europe, Asia Pacific, and the rest of the world.

North America

North America Naval Vessels Electronic Countermeasures (ECM) Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America holds the largest market share, and is anticipated to grow at a CAGR of 5.3% during the forecast period. The dominance is because the region combines the world’s most mature shipborne electronic warfare systems base with sustained modernization spending on high-end combatants. The U.S. Navy remains the biggest contributor, supported by large-scale upgrades in electronic attack, threat warning, and anti-ship missile defense, while Canada adds a smaller but still relevant modernization layer through frigate and electronic warfare support programs. As a result, the region holds the largest market position due to strong fleet scale, deep integration capability, and consistent investment in survivability-focused naval systems.

U.S. Naval Vessels Electronic Countermeasures (ECM) Market

Based on the strong contribution of North America and the dominance of U.S. within the region, the U.S. market stood at around USD 0.83 billion in 2025, growing at a CAGR of 5.1% during the forecast period.

Europe

Europe held around 28.21% share of the global market in 2025. Europe is a technology-focused and integration-driven market in the ECM sector. Strong industrial capabilities and collaborative defense programs support this market. The U.K, France, Germany, and Italy are modernizing their fleets with improved electronic warfare systems. They particularly focus on interoperability, NATO cooperation, and layered soft-kill ability. The region has established companies such as BAE Systems and reliable subsystem suppliers. These players make consistent investments in electronic attack, electronic support, and signals intelligence.

France Naval Vessels Electronic Countermeasures (ECM) Market

The French market reached approximately USD 0.13 billion in 2025, equivalent to around 17.43% of Europe revenues.

U.K. Naval Vessels Electronic Countermeasures (ECM) Market

U.K. market stood at around USD 0.14 billion in 2025, representing roughly 18.46% of Europe revenues.

Asia Pacific

Asia Pacific holds a significant share of the market, and is anticipated to grow at the highest CAGR of 8.7% over the forecast period. The region’s market growth is driven by fleet expansion and rising maritime tensions in this region. China, India, Japan, and South Korea are increasing defense budgets, leading to both newbuild programs and retrofit demand for advanced ECM. The region is also shifting toward local development while partnering with global firms such as Lockheed Martin, Northrop Grumman, L3Harris Technologies, and Elbit Systems. This mix of scale, modernization efforts, and capability growth makes Asia Pacific an important player in the global market due to ongoing procurement activities.

China Naval Vessels Electronic Countermeasures (ECM) Market

The Chinese market revenues stood at around USD 0.21 billion in 2025, representing roughly 29.77% of the global sales.

Japan Naval Vessels Electronic Countermeasures (ECM) Market

The Japanese market in 2025 stood at around USD 0.13 Billion, accounting for roughly 17.46% of Asia Pacific revenues.

Rest of the World

The rest of the world includes Middle East & Africa and Latin America region. The rest of the world holds a comparatively smaller market share but is expected to grow at a CAGR of 6.8% during the forecast period. In the Middle East & Africa, demand comes from high-value platforms that prioritize survivability and quick-response electronic warfare systems. Latin America is focused on upgrading mid-tier fleets and on cost-effective ECM integration.

Latin America Naval Vessels Electronic Countermeasures (ECM) Market

The market in Latin America reached around USD 0.08 billion in 2025, accounting for roughly 30.52% of rest of the world revenues.

Middle East & Africa Naval Vessels Electronic Countermeasures (ECM) Market

The Middle East & Africa market stood at around USD 0.19 billion in 2025, representing roughly 69.48% of the rest of the world.

COMPETITIVE LANDSCAPE

Key Industry Players

Technology Depth, Naval Integration Capability, and Upgrade Execution are Defining Competition Among the Key Players

The competitive landscape in the market features the main global defense companies and specialized electronic warfare providers. They compete based on system maturity, naval integration ability, upgrade options, and their footprint in the existing fleet. Northrop Grumman has a strong position with the U.S. Navy’s SEWIP Block 3. This system enhances the fleet with non-kinetic electronic attacks. BAE Systems remains the main player due to its broader naval defense integration and additional survivability options. L3Harris Technologies is significant through its maritime electronic support measures and overall naval mission-system integration. Elbit Systems is increasing its role with naval electronic warfare, signals intelligence, and decoy countermeasure solutions focused on modern anti-ship missile defense.

The main differentiator in leading players is not just hardware supply, but companies’ ability to deliver a more complete survivability architecture across newbuild and retrofit programs. The market is moving toward integrated soft-kill frameworks that connect detection, electronic attack, decoy deployment, and command-and-control, which favors companies that can support long upgrade cycles and complex fleet integration.

List of Key Naval Vessels Electronic Countermeasures (ECM) Companies Profiled

- Northrop Grumman Corporation (U.S.)

- Lockheed Martin Corporation (U.S.)

- BAE Systems plc. (U.K.)

- L3Harris Technologies, Inc. (U.S.)

- Elbit Systems Ltd. (Israel)

- Thales Group (France)

- Saab AB (Sweden)

- Leonardo S.p.A. (Italy)

- Indra Sistemas, S.A. (Spain)

- HENSOLDT AG (Germany)

KEY INDUSTRY DEVELOPMENTS

- March 2025: Rafael and Elbit Systems announced that they received a contract to supply a maritime EW self-protection solution for new frigates of NATO European countries, including a Naval Decoy Control & Launching System (DCLS) and related integrated self-protection capability.

- November 2024: Naval Group signed a Memorandum of Understanding with Thales and KNDS to develop the multi-purpose and modular launching system (MPLS), designed to respond to asymmetric threats through the deployment of multiple effectors, including soft-kill and countermeasure applications relevant to naval EW.

- October 2024: The U.K. Ministry of Defense placed a contract valued at USD 3.64 million for test and practice cartridges and related safety assessment work to support trials of the EWCM 1a Ancilia launcher.

- October 2024: Lockheed Martin announced its first international SEWIP sale to Japan, under a USD 113.00 million U.S. Navy contract for full-rate production of SEWIP Block 2 AN/SLQ-32(V)6 and AN/SLQ-32C(V)6 systems for the U.S. Navy and the Government of Japan through the Foreign Military Sales program.

- March 2024: The U.K government awarded a contract worth USD 170.10 million to equip Royal Navy warships with Ancilia trainable decoy launchers to counter missile and drone threats.

- September 2022: Naval Group launched HS Kimon, the first FDI frigate for the Hellenic Navy, and stated that the vessel benefits from Thales’ latest innovations in radar, sonar, and electronic warfare.

- December 2020: The U.K Ministry of Defence launched the first phase of its Maritime Electronic Warfare Program (MEWP) worth USD 676.27 million. The program covers next-generation maritime EW capability for the Royal Navy and supports future deployment across major surface combatants.

REPORT COVERAGE

The global naval vessels electronic countermeasures (ECM) market analysis provides an in-depth study of market size, company profiling & forecast by all the market segments included in the report. It includes details on the market dynamics and trends that are expected to drive the market during the forecast period. It offers information on the technological advances, new product launches, key industry experts' developments, and details on strategic partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market share and profiles of key market players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.0% from 2026 to 2034 |

| Unit | Value (USD Billion) |

|

Segmentation

|

By Platform Type

|

|

By Component

|

|

|

By Capability

|

|

|

By Fit type

|

|

|

By End User

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 2.63 billion in 2025 and is projected to reach USD 4.84 billion by 2034.

In 2025, the North America market value stood at USD 0.89 billion.

The market is expected to exhibit a CAGR of 7.0% during the forecast period.

The high-end surface combatants segment led the market by platform type.

Rising naval modernization programs and electronic survivability requirements are driving market growth.

Key players in the market include Northrop Grumman, Lockheed Martin, BAE Systems, L3Harris Technologies, Elbit Systems, and Thales.

North America dominated the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us