North America Synthetic Bone Void Fillers Market Size, Share & Industry Analysis, By Material (Calcium Phosphate, Calcium Sulfate, Bioactive Glass, Synthetic Polymer, Composites, and Others), By Form (Gel, Granules, Paste, Putty, and Others), By Application (Spinal Fusion, Joint Reconstruction, Foot & Ankle, and Others), By End-user (Hospitals & ASCs, Clinics, and Others), and Country Forecast, 2026-2034

North America Synthetic Bone Void Fillers Market Size and Future Outlook

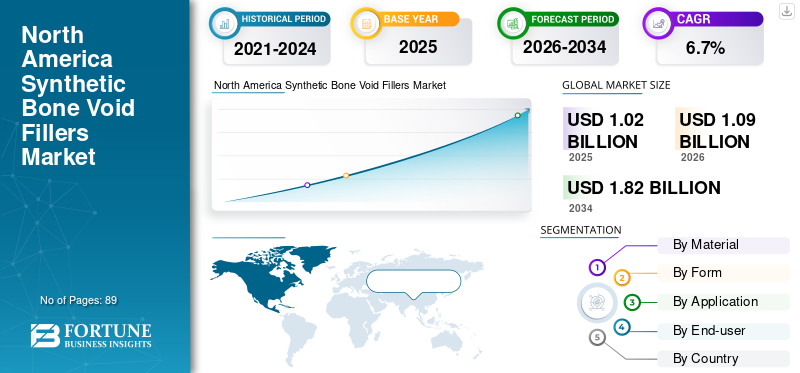

The North America synthetic bone void fillers market size was valued at USD 1.02 billion in 2025. The market is projected to grow from USD 1.09 billion in 2026 to USD 1.82 billion by 2034, exhibiting a CAGR of 6.7% during the forecast period.

Synthetic bone void fillers are resorbable biomaterials used in orthopedic and trauma surgeries to fill non-structural bone defects or gaps, providing a scaffold for new bone growth. These synthetic materials, such as calcium phosphates, calcium sulfate, bioactive glass, and others, mimic natural bone mineral composition to promote osteoconduction, guiding bone cells to regenerate within the void. The market growth is attributed to rising product launches and regulatory approvals of synthetic bone void fillers, driven by growing clinical needs for bone defect treatment.

Furthermore, the prominent market companies include Stryker, Depuy Synthes, Zimmer Biomet, and BONESUPPORT AB, which are focusing on new launches and strategic initiatives to expand their market share.

Download Free sample to learn more about this report.

NORTH AMERICA SYNTHETIC BONE VOID FILLERS MARKET TRENDS

Development of Antibiotic-Impregnated Synthetic Bone Void Fillers Targeting Infection Control to Emerge as a Key Market Trend

Currently, there has been an increasing shift toward antibiotic-loaded and infection-focused formulations, due to increasing cases of bone infections and surgical site infections, driven by orthopedic surgeries. These fillers offer dual clinical benefits by providing structural support for the bone defect while enabling targeted, high-concentration antibiotic delivery directly to the infection site.

As a result, there is an increasing clinical research initiatives and regulatory submissions for such products by key players. For instance, in April 2025, BONESUPPORT AB filed an FDA submission for CERAMENT V, a vancomycin-eluting bone graft substitute to treat bone infections including those from MRSA/MRSE, leveraging extensive clinical data from CERAMENT G and its prior Breakthrough Device status.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Prevalence of Bone Conditions and Growing Surgical Procedures are Driving Demand in North America

Over the past few years, there has been a significant rise in the prevalence of bone disorders such as osteoporosis, which is further leading to osteoporotic fractures, driving the demand for surgical interventions, which often involve bone void fillers.

- For instance, according to the International Journal of Basic & Clinical Pharmacology, published in June 2025, an estimated 10.0 million individuals in the U.S. had osteoporosis, with an additional 44.0 million presenting with low bone mass.

Moreover, the rising volume of orthopedic procedures, trauma, and reconstructive procedures due to an aging population is also expected to drive the North America synthetic bone void fillers market growth.

MARKET RESTRAINTS

Competition from Alternative Bone Grafting Options Restrains Market Growth in North America

Despite significant demand for synthetic bone void fillers, alternative bone grafting options, such as autografts and allografts, have been widely used in orthopedic procedures due to their proven clinical efficacy and surgeon familiarity. Autografts offer superior osteoinductive and osteogenic properties in challenging fractures while avoiding the risks of foreign-body reactions inherent to synthetic materials.

As a result, the increasing preference for non-synthetics is anticipated to limit the market penetration of synthetic bone void fillers, hindering market growth in the forthcoming years.

MARKET OPPORTUNITIES

Growing Research and Innovations to Create Significant Growth Opportunities

Recently, there has been increasing clinical research and innovation focused on advanced synthetic biomaterials, as the growing number of bone defect cases and associated conditions has intensified the need for effective and predictable bone void management solutions.

The research efforts are primarily focused on developing synthetic formulations that are expected to accelerate bone regeneration, reduce infection risk, and enable use in challenging anatomical sites. Such a scenario is expected to create lucrative opportunities for market expansion.

- For instance, in September 2024, Biocomposites launched two Phase II clinical trials, BLADE-VG2 and BLADE-OPU2, evaluating STIMULAN VG, a pre-mixed calcium matrix antibiotic carrier containing vancomycin and gentamicin for treating diabetic foot osteomyelitis and stage IV pressure ulcers in the U.S.

MARKET CHALLENGES

Challenges from Clinical Concerns to Hinder Synthetic Bone Void Filler Use in North America

Despite increasing clinical acceptance, the synthetic bone void fillers continue to face significant challenges due to under-penetration in certain orthopedic and trauma procedures and the presence of specific clinical and procedural limitations. In some applications, concerns about infection risk, inflammatory responses, and inconsistent bone-regeneration outcomes associated with certain synthetic formulations have led to cautious adoption by surgeons.

- For instance, according to the data published by the Journal of Orthopedic Experience & Innovation in April 2025, Synthetic bone void fillers such as CERAMENT deliver clinical advantages but come with elevated costs and potential local reactions, especially in calcium sulfate formulations.

Segmentation Analysis

By Material

Significant Properties Such as Osteoconductivity and Higher Availability to Drive Calcium Phosphate Segment’s Growth

By material, the market is segmented into calcium phosphate, calcium sulfate, bioactive glass, synthetic polymer, composites, and others.

To know how our report can help streamline your business, Speak to Analyst

The calcium phosphate segment held the largest market share in 2025. The segment’s growth is attributed to the osteoconductive properties of calcium phosphate and their availability in multiple delivery formats, such as injectable and moldable, which is expected to drive their usage across trauma & extremities, spine, and reconstruction.

Additionally, the calcium sulfate segment is projected to grow at a 6.4% CAGR over the forecast period.

By Form

Superior Handling and Ease of Delivery Increased Adoption of Paste

By form, the market is segmented into gel, granules, paste, putty, and others.

The paste segment accounted for the largest market share in 2025. The segment's growth is attributed to superior handling and ease of delivery. These formulations provide ready-to-use or minimally prepared injectability for accurate filling of irregular bone voids, making them especially beneficial for minimally invasive surgeries. Moreover, the segment is projected to hold a 40.8% share in 2026.

On the other hand, the granules segment is projected to grow at a CAGR of 6.2% during the forecast period.

By Application

Growing Number of Spinal Fusion Procedures Boosted Segment Expansion

By application, the market is segmented into spinal fusion, joint reconstruction, foot & ankle, and others.

The spinal fusion segment accounted for the largest market share in 2025 and is anticipated to expand at the fastest CAGR over the forecast period. The segment’s growth is driven by the high and rising burden of degenerative spine disorders and aging individuals in the U.S. and Canada, resulting in an increasing number of spinal fusion procedures in the region. Moreover, the segment is projected to hold a 43.0% share in 2026.

- For instance, according to the data from the Swanson School of Engineering at the University of Pittsburgh in January 2024, interbody spinal fusion accounts for an estimated 342,000 cases annually in the U.S.

On the other hand, the joint reconstruction segment is anticipated to expand at a CAGR of 6.0% during the forecast period.

By End-user

High Volume of Complex Orthopedic Surgeries in Hospitals and Increasing Number of ASCs Fueled Hospital & ASCs Segment’s Growth

By end-user, the market is divided into hospitals & ASCs, clinics, and others.

The hospitals & ASCs segment held the largest market share in 2025. The segment growth is attributed to the use of larger volumes of synthetic bone void fillers in complex orthopedic procedures, such as spinal fusion, trauma fixation, joint reconstruction, and revisions. Additionally, an increasing number of ASCs and the shift of spine, foot & ankle, and trauma cases to these settings are expected to favor the use of injectable, ready-to-use fillers for greater efficiency. Moreover, the segment is projected to hold a 77.4% share in 2026.

- For instance, according to MedPAC data, between 2022 and 2023, Medicare-certified Ambulatory Surgery Centers (ASCs) increased by 2.5% to a total of 6,308 ASCs, compared with 2.2% growth between 2018 and 2022.

On the other hand, the clinics segment is projected to grow at a CAGR of 6.9% during the forecast period.

North America Synthetic Bone Void Fillers Market Country Outlook

By country, the market has been studied across the U.S. and Canada.

U.S. Synthetic Bone Void Fillers Market

The U.S. accounted for the largest share of revenues in 2024, valued at USD 0.85 billion, and was further valued at USD 0.91 billion in 2025. The growth is attributed to the high volume of orthopedic procedures, particularly spinal fusion, joint reconstruction, and sports injury-related surgeries, which consume larger volumes of synthetic bone void fillers per case. Moreover, the U.S. leads in the adoption of synthetic graft substitutes due to surgeons' preference for avoiding autograft complications, which is expected to support market growth further.

- For instance, in January 2026, MidAmerica Orthopaedics mentioned that more than 300,000 lumbar spinal fusions are performed annually in the U.S.

Canada Bone Void Fillers Market

Canada is projected to grow at a CAGR of 6.9% during the forecast period, reaching USD 0.12 billion by 2026. The country's growth is attributed to increasing investments by several provincial health systems in elective orthopedic capacity to address surgical backlogs, supporting the adoption of synthetic bone void fillers in the upcoming years.

COMPETITIVE LANDSCAPE

Key Industry Players

Increasing Focus on Portfolio Expansions and Increasing Investments to Increase Market Share of Key Players

Stryker, Depuy Synthes (Johnson & Johnson Services, Inc.), Zimmer Biomet, and BONESUPPORT AB accounted for the largest North America synthetic bone void fillers market share in 2025. These companies are focusing on investments in trauma-focused biomaterials and integration with internal fixation systems to strengthen their competitive position.

Furthermore, other prominent players such as Biocomposites, Medtronic, NovaBone, and Arthrex Inc. are expanding their portfolios through new launches and strengthening their foothold in the market through strategic agreements, which is expected to help enhance market share.

- For instance, in November 2024, NovaBone secured FDA 510(k) clearance (K242299) for its bioactive synthetic bone graft, NovaBone Putty, for use in interbody fusion procedures within the intervertebral disc space alongside cleared fusion devices.

LIST OF KEY NORTH AMERICA SYNTHETIC BONE VOID FILLERS COMPANIES PROFILED

- Stryker (U.S.)

- Zimmer Biomet (U.S.)

- Medtronic (Ireland)

- DePuy Synthes (Johnson & Johnson Services, Inc.) (U.S.)

- Anthrex, Inc. (U.S.)

- BONESUPPORT AB (Sweden)

- Biocomposites (U.K.)

- NovaBone (U.S.)

- Bonalive Ltd (Finland)

- Bone Solutions, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- October 2025: Johnson & Johnson Services, Inc. announced plans to separate its orthopedics business to prioritize portfolio investments and commercialization in trauma or spine ecosystems where synthetic graft substitutes are routinely bundled.

- July 2025: SurGenTec received additional FDA 510(k) clearance for OsteoFlo HydroFiber, its synthetic bone graft, now approved as a bone void filler for tumors, cysts, trauma, and osteomyelitis.

- May 2025: Bone Solutions, Inc. received FDA clearance expanding Mg OSTEOCRETE and Mg OSTEOINJECT (magnesium phosphate bone substitutes) for pediatric use in patients aged 7 years or older, enabling minimally invasive Sclerograft treatment for unicameral bone cysts in extremity and pelvic voids.

- April 2025: Stryker completed the sale of its U.S. spinal implants business to Viscogliosi Brothers, LLC. This divestiture sharpened Stryker's North American focus on synthetic bone void fillers.

- March 2025: Biocomposites partnered with Novo Holdings & TA Associates to strengthen its ability to scale commercial reach, support R&D or clinical evidence, and expand penetration of synthetic graft or void-filling platforms in North America.

- March 2022: Biocomposites entered into a multi-year agreement with Zimmer Biomet to exclusively distribute genex Bone Graft Substitute with its delivery options and new mixing system in the U.S. orthopaedic market.

- January 2022: BONESUPPORT AB announced a distribution agreement with OrthoPediatrics Corp. to distribute its CERAMENT bone void filler (BVF) to pediatric hospitals within the U.S.

REPORT COVERAGE

The North America synthetic bone void fillers market report provides a comprehensive analysis of all market segments. It also covers market dynamics and key insights, including the prevalence of key conditions, new product launches, key industry developments, and technological advancements. It also outlines the competitive landscape and detailed company profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Billion) |

|

Growth Rate |

CAGR of 6.7% from 2026-2034 |

|

Segmentation |

By Material, Form, Application, End-user, and Country |

|

By Material |

|

|

By Form |

|

|

By Application |

|

|

By End-user |

|

|

By Country |

|

Frequently Asked Questions

Fortune Business Insights says that the market stood at USD 1.02 billion in 2025 and is projected to reach USD 1.82 billion by 2034.

The market will exhibit steady growth at a CAGR of 6.7% during the forecast period (2026-2034).

Based on material, the calcium phosphate segment led the market in 2025.

The rising prevalence of bone defects and the increasing number of orthopedic procedures are among the factors driving market growth.

Stryker, Depuy Synthes (Johnson & Johnson Services, Inc.), Zimmer Biomet, and BONESUPPORT AB are major players in the market.

- 2021-2034

- 2025

- 2021-2024

- 89

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us