Personal Care Active Ingredients Market Size, Share & Industry Analysis, By Type (Photoprotection Actives, Renewal & Antioxidant Actives, Biofunctional Repair Actives, and Others), By Application (Skincare, Haircare, Sun Care, Oral Care, and Others), and Regional Forecast, 2026-2034

Personal Care Active Ingredients Market Size and Future Outlook

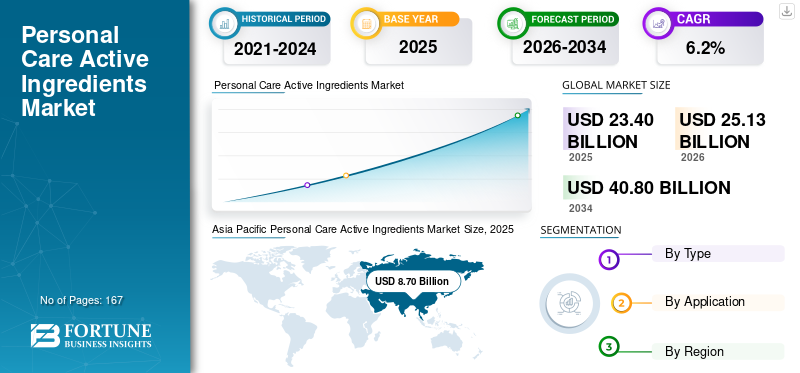

The global personal care active ingredients market size was valued at USD 23.40 billion in 2025. The market is projected to grow from USD 25.13 billion in 2026 to USD 40.80 billion by 2034, exhibiting a CAGR of 6.2% during the forecast period. Asia Pacific dominated the personal care active ingredients market with a market share of 37.17% in 2025.

Personal care active ingredients encompass specialty bioactive, synthetic, natural, and biotechnology-derived constituents used in cosmetic and personal care formulations to deliver specific functional benefits, such as anti-aging, hydration, skin brightening, sun protection, acne control, barrier repair, scalp care, and oral care. These materials are integrated into skincare, haircare, sun care, oral care, and body care products, as well as active-led color cosmetic formulations. They comprise peptides, vitamins, botanical extracts, ceramides, enzymes, antioxidants, exfoliating acids, UV filters, anti-acne agents, microbiome-supporting ingredients, and other functional bioactives.

A key driver of demand is the continued expansion of the global beauty and personal care industry, particularly in skincare, dermocosmetics, sun care, and premium haircare. This supports strong downstream demand for active ingredients used in face creams, serums, sunscreens, scalp treatments, and functional body care products.

The market is dominated by several major players, including BASF SE, Croda International Plc, Givaudan, Symrise AG, dsm-firmenich, Evonik Industries, Clariant, Lubrizol, Ashland, and Seppic. They are active in cosmetic bioactives, botanical extracts, peptides, ceramides, UV filters, functional polymers, and sustainable personal care ingredients. These companies compete through broad portfolios, application laboratories, sustainability credentials, ingredient efficacy data, formulation support, and global distribution reach.

Download Free sample to learn more about this report.

PERSONAL CARE ACTIVE INGREDIENTS MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 23.40 billion

- 2026 Market Size: USD 25.13 billion

- 2034 Forecast Market Size: USD 40.80 billion

- CAGR: 6.20% from 2026–2034

- Asia Pacific dominated the market with a 37.17% share in 2025.

- The Photoprotection Actives segment held the largest market share in 2025.

- The Skincare segment held the largest market share in 2025.

Asia Pacific

Reached USD 8.70 billion in 2025, driven by strong personal care manufacturing, K-beauty, J-beauty, and rising skincare demand.

Europe

The market is projected to reach USD 6.61 billion by 2026, supported by a strong cosmetics industry and demand for sustainable, science-backed ingredients.

North America

Growth is driven by premium skincare, clean beauty, anti-aging products, and dermatologist-backed brands.

U.S.

The market is projected to reach USD 4.95 billion by 2026, accounting for 19.7% of global sales.

Japan

The market is projected to reach USD 1.64 billion by 2026, accounting for 6.5% of global revenue.

Read More

PERSONAL CARE ACTIVE INGREDIENTS MARKET TRENDS

Shift from Single-Claim Beauty Ingredients to Science-Backed Multifunctional Actives is a Key Market Trend

A major trend in the market is the shift from basic cosmetic actives to multifunctional materials that combine multiple claims in a single formulation. Brands are increasingly using ingredients that support hydration, barrier repair, brightening, microbiome balance, anti-aging, and environmental protection together. This is particularly visible in skincare and dermocosmetic formulations, where consumers expect visible efficacy, clinical substantiation, and compatibility with sensitive skin.

The rise of longevity beauty, skin-barrier care, microbiome care, and biotech-derived ingredients reinforces this trend. At in-cosmetics Global 2025, several suppliers highlighted longevity, clean beauty, personalized beauty, and AI-supported formulation as major innovation themes. Personal Care Insights reported that natural ingredients, holistic well-being, and AI-shaped beauty were among the standout themes at the event.

Suppliers are also launching ingredients that combine sustainability and efficacy. For instance, in April 2025, dsm-firmenich introduced SYN-COLL CB, a patented natural-origin tripeptide designed to support collagen and address skin-aging applications. In April 2025, Clariant launched its Clariant Beauty positioning with new solutions across skin care, hair care, and sun protection.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Premiumization, Dermocosmetics, and Skincare-First Beauty are Accelerating Active Ingredient Adoption

The personal care active ingredients market growth is strongly driven by the premiumization of beauty and the increasing consumer demand for claim-led products. Skincare has become a central category in global beauty, with serums, face creams, sunscreens, ampoules, masks, and dermatology-inspired products using higher concentrations of actives than traditional cosmetic formulations. The rising popularity of ingredients such as niacinamide, vitamin C derivatives, peptides, ceramides, retinoid alternatives, exfoliating acids, and barrier-support materials is increasing the active-ingredient intensity of finished products.

The European market provides a strong demand signal. Cosmetics Europe reported that Europe’s cosmetics and personal care retail sales were around USD 122 billion in 2024, with skincare the largest category at USD 35.4 billion. This category composition is important as skincare products typically use a higher value share of actives than rinse-off products such as shampoos or basic cleansers.

In the U.S., the Personal Care Products Council describes the cosmetics and personal care industry as dynamic, innovation-driven, and supportive of jobs, economic activity, and scientific advancement. This supports the role of personal care brands and ingredient suppliers in developing new active-led formulations for mass, premium, and dermocosmetic channels.

MARKET RESTRAINTS

High Development Costs Due to Regulatory Scrutiny and Claim Substantiation Hinder Market Growth

A key restraint for the market is the high regulatory and technical burden associated with personal care active ingredients. UV filters, anti-acne ingredients, skin-lightening ingredients, preservatives with active functions, and certain exfoliating or bioactive materials are subject to strict regional rules. In the EU, UV filters are listed in Annex VI of the Cosmetics Regulation and are subject to concentration limits, restrictions, and labeling requirements.

In the U.S., sunscreen active ingredients are regulated under OTC sunscreen rules, with specific permitted active ingredients and concentration limits outlined in 21 CFR Part 352. This creates regional complexity for formulators that sell across multiple markets, as the same sun care formulation may need to be adjusted by geography.

Claim substantiation is another restraint. Ingredients positioned for anti-aging, brightening, acne care, barrier repair, microbiome support, or hair growth support often require efficacy testing, stability testing, toxicology documentation, and finished-product compatibility evaluation. These requirements extend launch timelines and raise formulation costs, particularly for smaller personal care brands and local manufacturers.

MARKET OPPORTUNITIES

Biotechnology, Natural-Origin Actives, and Sustainable Sourcing Create Premium Growth Spaces

A strong opportunity exists in biotechnology-derived and natural-origin personal care active ingredients. Fermentation-based ceramides, peptides, vegan collagen alternatives, plant stem-cell extracts, microbiome-supporting actives, and upcycled botanical ingredients are gaining attention as brands try to balance efficacy, sustainability, and clean-label positioning. These materials often command premium pricing and are used in high-margin skincare, scalp care, sun care, and dermocosmetic products.

Supplier activity supports this opportunity. Evonik highlights ceramide technologies for skin and hair care, positioning ceramides as materials that support moisture retention and barrier function. The company also showcased biotechnology-driven personal care innovations, including biosurfactants, biopolymers, ceramides, and vegan collagen, at in-cosmetics Global 2025.

Croda’s 2024 results also indicate the strategic importance of beauty actives. The company described its Beauty Actives business as a leader in peptides, biotech-derived ingredients, botanicals, and ceramides, while noting that Consumer Care sales grew in 2024, led by Asia.

MARKET CHALLENGES

Raw Material Volatility, Formulation Complexity, and Price Sensitivity Pressure Margins are Key Market Challenges

The market faces challenges due to volatility in raw materials, particularly botanical extracts, specialty oils, UV filters, vitamins, fermentation-derived materials, and high-purity specialty chemicals. Many actives depend on agricultural feedstocks, controlled fermentation, specialty synthesis, or highly specific purification processes. This can create margin pressure when costs rise faster than beauty brands are willing to absorb.

The complexity of formulation also constrains adoption. Personal care active ingredients must maintain stability across a range of pH levels, temperatures, packaging formats, emulsion systems, and preservative systems. For instance, vitamin C derivatives, retinoid alternatives, enzymes, peptides, and botanical extracts may necessitate meticulous formulation to prevent degradation, discoloration, odor issues, or loss of efficacy.

Price sensitivity is especially important in mass-market products. While premium and dermocosmetic brands can support higher active loading and stronger claims, mass personal care products often require lower-cost actives or lower inclusion rates. This creates a two-speed market: premium active systems grow faster in value. At the same time, high-volume applications such as body care and hair care maintain higher volume but lower average prices.

Segmentation Analysis

By Type

Photoprotection Actives Segment Led Market Due to High Usage in Sun Care and SPF-Enabled Products

Based on type, the market is segmented into photoprotection actives, renewal & antioxidant actives, biofunctional repair actives, and others.

The photoprotection actives segment accounted for the largest personal care active ingredients market share in 2025, driven by rising awareness of photoaging, skin cancer prevention, pollution protection, and daily SPF use. The segment is expected to grow steadily, with stronger growth in Asia Pacific, Latin America, and the Middle East driven by climate conditions, urban beauty routines, and rising adoption of sun protection. Furthermore, this segment is projected to grow at a CAGR of 6.7% over the study period.

The renewal & antioxidant actives segment is expected to grow significantly over the forecast period. This segment is of significant commercial importance, as it directly underpins high-demand claims such as anti-aging, skin glow, tone correction, acne care, and pore refinement. It is extensively utilized in serums, creams, toners, peeling products, acne treatments, face masks, and body care products. Growth is facilitated by consumer familiarity with “hero ingredients” such as vitamin C, niacinamide, AHA/BHA acids, and antioxidants. Moreover, this segment is anticipated to grow at a CAGR of 5.6% over the study period.

By Application

To know how our report can help streamline your business, Speak to Analyst

Skincare Segment to Grow with the Fastest CAGR Due to Growing Usage of Active Ingredients

In terms of application, the market is categorized into skincare, haircare, sun care, oral care, and others.

The skincare segment is projected to grow at the highest CAGR of 6.7% over the study period. Skincare products use a wide range of active ingredients, including peptides, vitamins, antioxidants, ceramides, brightening agents, botanical extracts, exfoliating acids, and microbiome-supporting ingredients. Serums, creams, lotions, masks, toners, and spot treatments typically make strong efficacy claims, which increase the perceived value of the active ingredients in each product.

The hair care segment includes shampoos, conditioners, scalp treatments, hair masks, leave-in products, anti-dandruff products, hair fall products, and repair serums. Active ingredient demand is growing as the category moves from basic cleansing toward scalp health, hair fiber repair, hair density support, anti-frizz, bond repair, and microbiome-related positioning. The segment is anticipated to expand faster than conventional haircare ingredients, as consumers increasingly view scalp care as an integral part of skincare. This phenomenon, known as the “skinification of haircare,” underpins demand for biofunctional, botanical, and barrier-supporting active ingredients. Furthermore, this segment is projected to grow at a 5.6% CAGR over the study period.

The sun care segment is expected to grow significantly over the forecast period. Growth is primarily driven by the widespread adoption of daily sunscreen use, increased awareness of photoaging, growing consumer preferences for lightweight formulations, and rising demand for multifunctional SPF products that offer UV protection alongside hydration, brightening, anti-pollution, and skin-barrier benefits. The Asia Pacific region is expected to remain a major hub for innovation in this segment, driven by robust daily sun-protection habits in Japan, South Korea, China, and Southeast Asia. Furthermore, this segment is projected to grow at 6.1% CAGR over the study period.

Personal Care Active Ingredients Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Personal Care Active Ingredients Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2024, the Asia Pacific region held the largest market share at USD 8.06 billion and maintained its leadership in 2025, at USD 8.70 billion. The region’s growth is supported by large-scale personal care manufacturing, rising middle-class consumption, strong skincare routines, K-beauty and J-beauty innovation, expanding Indian beauty demand, and increasing adoption of sun care and active-led haircare products.

China Personal Care Active Ingredients Market

In 2026, the Chinese market is projected to attain a valuation of USD 3.70 billion. China remains the largest regional market due to its scale in skincare, sun care, haircare, and domestic beauty brands.

To know how our report can help streamline your business, Speak to Analyst

Japan Personal Care Active Ingredients Market

The Japanese market in 2026 is estimated at around USD 1.64 billion, accounting for roughly 6.5% of global revenues.

India Personal Care Active Ingredients Market

The India market in 2026 is estimated at around USD 1.16 billion, accounting for roughly 4.6% of global revenues.

Europe

Europe is expected to experience substantial market growth in the coming years. Over the forecast period, the region is projected to grow at an annual rate of 57.8%, reaching a market valuation of USD 6.61 billion in 2026. Europe is a major market for personal care active ingredients, supported by a strong cosmetics manufacturing sector, regulatory discipline, export-oriented beauty brands, and high demand for sustainable, science-backed ingredients. Cosmetics Europe reported that European cosmetics and personal care retail sales were around USD 122 billion in 2024, with skincare, toiletries, and haircare as the leading categories.

U.K. Personal Care Active Ingredients Market

The U.K. market in 2026 is estimated at around USD 1.44 billion, accounting for roughly 5.7% of global revenues.

Germany Personal Care Active Ingredients Market

Germany’s market in 2026 is estimated at around USD 1.50 billion, accounting for roughly 6.0% of global revenues.

North America

North America represents a mature but high-value market, supported by premium skincare, dermocosmetics, clean beauty, dermatologist-backed brands, and strong demand for anti-aging and sun care products. The U.S. dominates regional consumption due to the presence of large beauty brands, contract manufacturers, indie brands, and active-led skincare innovation. North America is expected to grow steadily, with value growth driven by peptides, ceramides, retinoid alternatives, microbiome-supporting actives, premium sunscreen formulations, and clinical-positioned skincare.

U.S. Personal Care Active Ingredients Market

Given the U.S. dominance in the region, the U.S. market is estimated at around USD 4.95 billion in 2026, accounting for roughly 19.7% of global sales.

Latin America and Middle East & Africa

Latin America is expected to record moderate-to-high growth, led by Brazil and Mexico. Brazil is the region’s largest beauty and personal care market and has strong demand for haircare, body care, sun care, and botanical ingredients. Mexico benefits from proximity to North American supply chains, rising skincare adoption, and growing local manufacturing. The Middle East & Africa market is smaller than other regions. Still, it is expanding due to rising personal care penetration, premium beauty demand in the GCC, a young demographic, and climate-driven demand for sun care, hydration, body care, and hair care. GCC countries are the most value-intensive markets in the region, driven by premium beauty consumption and high per-capita spending. The Latin America market is projected to reach USD 1.91 billion in 2026.

GCC Personal Care Active Ingredients Market

The GCC market in 2026 is estimated at USD 0.87 billion, accounting for approximately 3.5% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Efficacy Data, Sustainability, and Application Support are Core Differentiators

The market is moderately fragmented, with large specialty chemical companies competing alongside biotechnology specialists, botanical extract producers, peptide suppliers, UV-filter manufacturers, and regional ingredient distributors. Large players benefit from global production networks, regulatory expertise, application laboratories, technical documentation, and relationships with multinational personal care brands.

Competitive advantage is increasingly based on substantiated claims, sustainable sourcing, natural-origin content, biotechnology capabilities, formulation support, and regional technical service. Ingredient suppliers are not only selling materials but also supporting brands with finished-formulation concepts, clinical data packages, sensory evaluations, stability guidance, and regulatory documentation.

Companies such as Croda, Givaudan, Symrise, BASF, Evonik, dsm-firmenich, Clariant, and Lubrizol are strengthening their active ingredient portfolios through product launches, sustainability programs, biotech platforms, and distribution partnerships. Croda’s public reporting describes Beauty Actives as a business with leadership in peptides, biotech-derived ingredients, botanicals, and ceramides. At the same time, Givaudan reported double-digit growth in Fragrance Ingredients and Active Beauty in 2024.

LIST OF KEY PERSONAL CARE ACTIVE INGREDIENT COMPANIES PROFILED

- BASF SE (Germany)

- Croda International Plc (U.K.)

- Givaudan (Switzerland)

- Symrise AG (Germany)

- dsm-firmenich (Netherlands)

- Evonik Industries AG (Germany)

- Clariant AG (Switzerland)

- Lubrizol Corporation (U.S.)

- Ashland Inc. (U.S.)

- Seppic (France)

KEY INDUSTRY DEVELOPMENTS

- March 2026: Symrise established a new Care & Wellness Division within its Scent & Care segment, bringing together cosmetic ingredients, health actives, and biotics to support science-backed beauty, wellbeing, and longevity-focused solutions.

- April 2025: BASF expanded its portfolio of natural-based personal care ingredients with new products presented under its Longevity Ecosystem at in-cosmetics Global, including Verdessence Maize, Lamesoft OP Plus, and Dehyton PK45 GA/RA.

- April 2025: Clariant launched Clariant Beauty, a new personal care positioning combining Clariant and Lucas Meyer Cosmetics expertise. The launch included solutions for skin care, hair care, and sun protection, including GlowCytocin, Melicica, Aristoflex SUN, and Nipaguard SCE Vita.

- March 2025: Lubrizol announced the launch of new naturally derived skin, sun, and hair care ingredients at in-cosmetics Global, strengthening its sustainable beauty solutions portfolio.

- January 2025: Univar Solutions and dsm-firmenich announced an expanded distribution partnership for beauty and personal care actives, including synthetic peptides, organically grown plant extracts, and other natural ingredients.

REPORT COVERAGE

The global personal care active ingredients market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on market dynamics and trends expected to drive the market during the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The market research report also includes a detailed competitive landscape, with market share and profiles of key market players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.2% from 2026 to 2034 |

| Unit | Value (USD Billion) Volume (Kiloton) |

| Segmentation | By Type, Application, and Region |

| By Type |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 23.40 billion in 2025 and is projected to reach USD 40.80 billion by 2034.

Recording a CAGR of 6.2%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

The skincare application segment is expected to grow at the highest CAGR during the forecast period.

Asia Pacific held the highest market share in 2025.

Premiumization, dermocosmetics, and skincare-first beauty are accelerating the adoption of active ingredients.

- 2021-2034

- 2025

- 2021-2024

- 167

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us