Personal Care Chemicals Market Size, Share & Industry Analysis, By Type (Surfactants, Emollients, Conditioning Polymers, Actives, and Others), By Application (Skin Care, Hair Care, Oral Care, Color Cosmetics, and Others), and Regional Forecast, 2026-2034

Personal Care Chemicals Market Size and Future Outlook

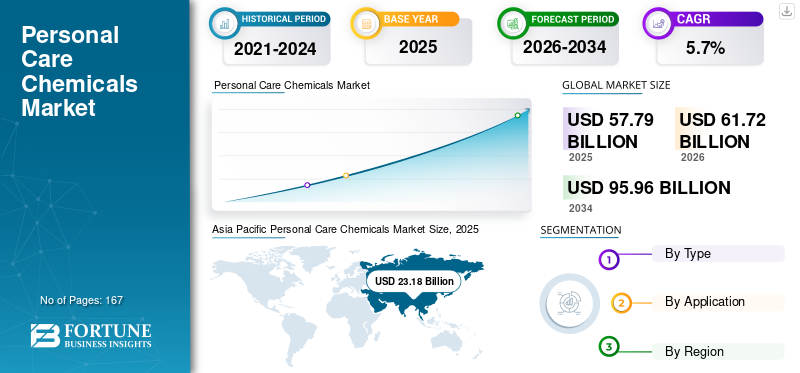

The global personal care chemicals market size was valued at USD 57.79 billion in 2025. The market is projected to grow from USD 61.72 billion in 2026 to USD 95.96 billion by 2034, growing at a CAGR of 5.7% during the forecast period. Asia Pacific dominated the personal care chemicals market with a market share of 40.11% in 2025.

Personal care chemicals are specialized ingredients used in formulating products for skin care, hair care, sun care, color cosmetics, deodorants, toiletries, and select hygiene-oriented applications. These substances encompass surfactants, emollients, emulsifiers, conditioning agents, preservatives, rheology modifiers, UV filters, and bio-based or biotech active ingredient systems designed to enhance texture, efficacy, stability, mildness, and sensory performance. The category is increasingly influenced by consumer preferences for multifunctional, safer, high-performance, and environmentally friendly formulations that promote moisturization, scalp care, microbiome balance, anti-pollution protection, and UV protection.

Furthermore, the market includes several major suppliers, including BASF SE, Croda International plc, Evonik, Clariant, Symrise, Lubrizol, and Ashland. Their competitive advantage is founded on extensive formulation portfolios, biotechnology-driven innovation, sustainable sourcing, application laboratories, and close collaboration with multinational beauty brands and regional formulators.

Personal Care Chemicals Market Takeaways

- 2025 Market Size: USD 57.79 billion

- 2026 Market Size: USD 61.72 billion

- 2034 Forecast Market Size: USD 95.96 billion

- CAGR: 5.7% from 2026–2034

- Asia Pacific dominated the personal care chemicals market with a market share of 40.11% in 2025.

- Actives segment maintained its market dominance in 2025.

- Skin care segment maintained its leading personal care chemicals market share in 2025.

Asia Pacific

In 2024, the Asia Pacific region accounted for the largest share, valued at USD 21.68 billion, and continued to lead in 2025, valued at USD 23.18 billion.

Europe

Europe is expected to experience significant personal care chemicals market growth over the coming years and is expected to attain a market valuation of USD 10.79 billion by 2026.

North America

North America continues to be a well-established yet highly appealing market, distinguished by robust demand for dermocosmetics, anti-aging solutions, scalp health products, premium hair care, and performance-oriented sun care.

U.S.

The U.S. market is estimated to be valued at around USD 13.17 billion in 2026, accounting for roughly 21.3% of global sales.

Japan

The Japan market is estimated to be around USD 2.99 billion in 2026, accounting for roughly 4.9% of the global revenues.

Read More

Download Free sample to learn more about this report.

PERSONAL CARE CHEMICALS MARKET TRENDS

Sustainable Performance Is Reshaping Formulation Priorities across Beauty and Hygiene

One of the most visible market trends is the shift from single-function commodity ingredients toward high-performance systems that combine efficacy, sensorial appeal, sustainability, and easier formulation processing. Ingredient suppliers are increasingly developing bio-based emollients, mild surfactants, multifunctional preservation systems, and biotech actives that enable brands to make stronger claims around naturality, reduced climate footprint, and performance. Evonik, for example, explicitly framed its 2025 in-cosmetics positioning around high-performance, eco-friendly personal care solutions, while Clariant tied its 2025 launches to hair care, skin care, and sun protection needs under a sustainability-led “Clariant Beauty” platform.

Simultaneously, the market is advancing toward claim-driven innovation in areas such as longevity, scalp wellness, barrier repair, stress defense, and sun care. L’Oréal recognizes that beauty routines are becoming more sophisticated and that consumer demand continues to grow across various regions and generations. Meanwhile, Croda highlights the significance of peptides, ceramides, hair proteins, mineral sunscreens, emulsifiers, and emollients in sophisticated formulations. Consequently, the market is increasingly influenced not solely by foundational formulation chemistry but also by evidence-supported active ingredients, premium sensorial systems, and distinctive product differentiation.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Premium Skin, Hair, and Suncremium Skin, Hair, and Sun s, bare Formulations are Raising Ingredient Intensity per Product

The primary catalyst for market growth is the steady increase in formulation complexity in daily-use personal care products. As consumer routines become increasingly specialized, brands are adopting larger, more varied ingredient formulations that incorporate surfactants, emollients, rheology modifiers, preservatives, delivery systems, and multiple active ingredients to enhance performance. This trend is particularly evident in hair care formulations, anti-frizz and bond-repair systems, microbiome-friendly cleansers, hybrid makeup and skincare products, and suncare formulations that demand heightened sensory performance without compromising protective qualities. L’Oréal’s 2025 beauty market analysis underscores the ongoing advancement in both skin and hair routines, while Croda’s consumer care review illustrates the growing reliance on effect and formulation ingredients working synergistically.

An additional layer of support emerges from consumer migration toward efficacy-backed claims such as barrier support, brightening, collagen support, anti-stress, and anti-aging solutions. Croda’s beauty actives positioning explicitly references peptides as effective ingredients for preventing skin aging, while multiple recent launches from suppliers such as Lubrizol, Ashland, and Symrise are centered on oxidative-stress defense, collagen support, and longevity-linked claims. Consequently, the category benefits not only from unit growth but also from increased active loading and more sophisticated, high-value formulation systems.

MARKET RESTRAINTS

Regulatory Complexity and Claim Substantiation are Slowing Reformulation Cycles

A significant constraint in the market is the escalating compliance obligations related to ingredient safety, environmental profiles, traceability, and marketing claims. Personal care formulations must adhere to stringent standards for toxicology, preservation efficacy, allergen disclosure, labeling, and regional restrictions, which can hinder raw material substitution and increase reformulation costs. This issue is particularly pronounced with respect to preservatives, UV filters, silicones, ethoxylates, fragrances, and certain claim-sensitive functional materials used in premium beauty products. The 2024 activity report of Cosmetics Europe further illustrates how regulatory developments and sustainability policies continue to influence the industry's operational landscape.

This burden is intensified by the fact that brands increasingly seek ingredients that are simultaneously of natural origin, globally compliant, sensorially elegant, highly stable, and high-performing. In practice, very few materials can satisfy all of these criteria without concessions. Suppliers must therefore allocate additional resources to formulation guidance, testing support, and claim documentation prior to widespread adoption of new chemistries by customers. This process lengthens commercialization cycles and may temporarily favor established chemistries over innovative alternatives, even as consumer preferences shift toward cleaner or more sustainable solutions.

Furthermore, variations in regional regulatory frameworks mean that “global” beauty product launches often require formulation modifications. A UV filter, preservative approach, or active-delivery system deemed acceptable in one market may require reformulation in another. For a global supplier of personal care chemicals, this can constrain economies of scale and extend the timeline from innovation to revenue, particularly in rapidly growing sectors such as sun care and active skin treatments.

MARKET OPPORTUNITIES

Biotechnology, Natural Performance, and Claim-Driven Actives are Expanding Value Creation

One of the most promising opportunities resides in biotechnology-enabled ingredients that enhance efficacy while simultaneously supporting sustainability initiatives. Recent product launches from BASF, Croda, Symrise, Lubrizol, Ashland, and Evonik indicate a market trend toward biotech neuroactives, plant-based preservation platforms, collagen-supportive actives, microbiota-linked skin defense, and environmentally friendly emollients. These innovations are closely aligned with consumer demand for premium skincare, scalp wellness, stress resilience, and long-term healthy aging.

Sun care and environmental protection represent another significant area of opportunity. BASF’s introduction of Uvinul® TS Hydro in 2025 illustrates how suppliers are focusing on lighter textures and improved UV-phase equilibrium in contemporary sun care products. Simultaneously, Clariant’s 2025 product portfolio launch explicitly addresses trends in skin care, hair care, and sun protection. As exposure to climate elements, pigmentation issues, and daily sunscreen application increase, suppliers equipped with robust UV protection systems and compatible sensorial modifiers are positioned to capitalize on disproportionate growth.

There is also considerable headroom in emerging markets, where beauty routines are increasingly adopting premium and digital influences. L’Oréal highlights the expansion of the middle class and an additional potential consumer base worth hundreds of billions by 2030. Concurrently, BASF indicates that it is broadening its presence within emerging markets. This development provides opportunities for ingredient suppliers to expand localized concepts across scalp care, textured hair, dermocosmetics, hybrid sun care, and affordable premium cleansing products.

MARKET CHALLENGES

Cost Pressure, Natural Trade-Offs, and Fast-Moving Consumer Expectations are Tightening Execution

The market also faces structural challenges related to raw material volatility, rapid time-to-market, and formulation compromises. Specialty emollients, plant-derived actives, fermentation-based materials, proteins, and advanced preservation systems often incur higher costs and have more intricate supply chains than traditional chemistries. Simultaneously, brands seek expedited launch cycles and more robust claims, thereby pressuring suppliers to shorten development timelines while maintaining stability and compliance.

A second challenge is that numerous “clean,” natural, or biodegradable pathways still necessitate compromises in formulation. Mild surfactants may influence foam or viscosity; plant-derived preservation systems might require re-optimization; natural polymers can exhibit different behaviors compared to synthetic rheology systems; and ultra-light sensorial profiles in sun care continue to pose technical challenges. Consequently, the market continues to favor suppliers that provide not only ingredients but also pre-validated formulation packages and application support.

Finally, social media-driven beauty cycles are accelerating product turnover. BASF’s SEPAWA 2025 communication explicitly linked product concepts to the trend dynamics of Gen Z and Generation Alpha, demonstrating how rapidly textures, claims, and aesthetics are evolving. For suppliers, this necessitates continuous portfolio updates to maintain relevance within a market where growing demand is coupled with expedited innovation obsolescence.

Segmentation Analysis

By Type

Continued Differentiation through Quantifiable Claims Contributed to Actives Segmental Growth

Based on type, the market is segmented into surfactants, emollients, conditioning polymers, actives, and others.

The actives segment maintained its market dominance in 2025, as brands continue to differentiate through quantifiable claims such as anti-aging, brightening, hydration, microbiome support, stress defense, anti-pollution protection, and skin regeneration support. Croda International plc introduced Zenakine, a biotech-based neuroactive aimed at addressing stress-related skin concerns; Lubrizol launched Lectroglaze for antioxidant defense associated with the skin microbiota; Symrise introduced Mindera as a plant-based platform for product protection and Cellexora MD as a plant-derived exosome ingredient; and Ashland emphasized Collapeptyl, a biofunctional that supports collagen. These product launches demonstrate that the active ingredient segment is expanding at a compound annual growth rate exceeding the broader market average and is expected to grow at a 6.2% over the study period.

The emollients segment held a substantial market share in 2025 and is projected to grow at a CAGR of 5.6% during the forecast period, attributable to its widespread application in moisturizers, creams, lotions, sun care products, cosmetics, and high-end hair systems. Emollients are integral to the sensory experience of the skin, including ease of application, barrier reinforcement, and a refined after-feel, thereby rendering them indispensable in both mass-market and luxury formulations. This segment particularly advantages from the consumer shift toward lightweight textures, long-lasting makeup comfort, microbiome-compatible skin care, and sensory-rich hybrid products.

The conditioning polymers segment is experiencing robust growth, driven by premiumization across hair repair, scalp care, curl management, frizz control, and protective styling. As hair care routines become more focused on treatment, formulators are progressively dependent on cationic polymers, proteins, silicones, and specialized conditioning systems to enhance detangling, softness, shine, heat protection, and deposition efficiency.

By Application

To know how our report can help streamline your business, Speak to Analyst

Strong Demand for Products that Address Moisturization and Anti-Aging Led to Dominance of Skincare Segment

In terms of application, the market is categorized into skin care, hair care, oral care, color cosmetics, and others.

The skin care segment maintained its leading personal care chemicals market share in 2025, driven by premiumization, sophisticated routines, and strong demand for products that address moisturization, demand for anti-aging, barrier repair, brightening, and stress defense. L’Oréal recognizes skincare as the largest category in the global beauty market, accounting for 39% of the market, highlighting significant demand for ingredients such as emollients, humectants, active compounds, rheology modifiers, emulsifiers, and preservation systems. Additionally, the segment benefits from increased consumer preference for clinically supported claims and biotech-enhanced ingredients. Moreover, it is projected to grow at a 6.2% compound annual growth rate over the study period.

The hair care segment is anticipated to experience some of the most rapid CAGR of 5.5% during the forecast period, driven by advancements in scalp health, damage repair, curl care, color protection, and salon-inspired treatment protocols. L’Oréal allocates 21% of the global beauty market to hair care, thereby reaffirming its strategic importance. Concurrently, both Croda and Clariant recognize hair care as a primary focus for innovation.

The color cosmetics segment is experiencing consistent growth in the market, driven by the premiumization of makeup products and the rising popularity of hybrid formulations that combine aesthetic appeal with therapeutic benefits. Contemporary color cosmetics are progressively integrating personal care ingredients such as emollients, film formers, pigment dispersants, preservatives, UV filters, and specialty polymers to enhance texture, spreadability, adhesion, durability, and skin feel. This trend is particularly evident in foundations, BB/CC creams, lip products, primers, and complexion enhancers, where consumer preferences are shifting toward lightweight, multifunctional products that offer additional skin benefits.

Personal Care Chemicals Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Personal Care Chemicals Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2024, the Asia Pacific region accounted for the largest share, valued at USD 21.68 billion, and continued to lead in 2025, valued at USD 23.18 billion. The region benefits from its extensive consumer base, increasing middle-class expenditure, robust beauty innovation cycles, and well-established manufacturing ecosystems in China, Japan, South Korea, India, and Southeast Asia. L’Oréal’s regional analysis indicates that North Asia accounts for 27% of the global beauty market, while SAPMENA-SSA accounts for 12%, underscoring the significant scale and momentum of demand across Asia.

China Personal Care Chemicals Market

By 2026, the Chinese market is projected to reach USD 7.54 billion. China remains the region's largest demand center, supported by premium skin care, functional sun care, scalp care, and digital-first product launches. Growth is reinforced by local innovation, rapid product refresh cycles, and strong uptake of efficacy-led beauty concepts.

To know how our report can help streamline your business, Speak to Analyst

Japan Personal Care Chemicals Market

The Japan market is estimated to be around USD 2.99 billion in 2026, accounting for roughly 4.9% of the global revenues.

India Personal Care Chemicals Market

The Indian market is estimated at around USD 1.68 billion in 2026, accounting for roughly 2.7% of global revenues.

Europe

Europe is expected to experience significant personal care chemicals market growth over the coming years. Throughout the forecast period, the region is expected to expand at an annual rate of 5.2%, attaining a market valuation of USD 10.79 billion by 2026. It is projected that Europe will experience stable growth during this period, driven by high-end skincare, dermocosmetics, trends in sustainable formulations, and rigorous regulatory frameworks.

U.K. Personal Care Chemicals Market

The U.K. market is estimated to be valued at around USD 2.31 billion in 2026, accounting for roughly 3.7% of global revenues.

Germany Personal Care Chemicals Market

Germany’s market is estimated to be valued at around USD 2.55 billion in 2026, accounting for roughly 4.1% of global revenues.

North America

North America continues to be a well-established yet highly appealing market, distinguished by robust demand for dermocosmetics, anti-aging solutions, scalp health products, premium hair care, and performance-oriented sun care. The PCPC indicates that the U.S. cosmetics and personal care products industry achieved total sales of USD 210.6 billion in 2022, emphasizing the substantial downstream consumption base that sustains ingredient demand.

U.S. Personal Care Chemicals Market

Given North America’s significant contribution and the U.S. dominance in the region, the U.S. market is estimated to be valued at around USD 13.17 billion in 2026, accounting for roughly 21.3% of global sales.

Latin America and Middle East & Africa

Latin America and the Middle East & Africa are relatively smaller in absolute size yet continue to present significant growth prospects. According to L’Oréal’s regional distribution, Latin America accounts for 9% of the global beauty market. Additionally, expansion into emerging markets, advancements in affordability tiers, and increasing grooming routines are facilitating the gradual penetration of ingredients. The Latin American market is anticipated to attain a valuation of USD 7.08 billion by the year 2026.

Moreover, the Gulf Cooperation Council (GCC) region exhibits emerging trends of premiumization across skincare, fragrances, and salon-related hair categories, which are underpinned by elevated consumer expenditure and climate-driven demand for hydration and protective products.

GCC Personal Care Chemicals Market

The GCC market in 2026 is estimated at USD 1.83 billion, accounting for approximately 3.0% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Enhanced Performance, Sustainability, and Application Support Will Assist in Gaining Competitive Edge

The market is moderately fragmented, with prominent multinational specialty-chemical corporations competing alongside biotechnology innovators and formulation specialists. Competitive advantage is contingent upon the capacity to integrate extensive product portfolios with robust technical support, comprehensive regulatory documentation, and innovation that responds to current trends. Suppliers capable of aiding customers in reducing development timelines while simultaneously achieving performance and sustainability objectives are optimally positioned to increase their market share.

Major incumbents such as BASF SE and Croda International plc capitalize on their scale, global manufacturing capabilities, and extensive product portfolios encompassing surfactants, emollients, active ingredients, preservation systems, and suncare technologies. Firms including Evonik, Clariant, Symrise, Lubrizol, and Ashland further enhance the competitive landscape through specialized platforms in biosolutions, plant-based protection, collagen-support actives, and advanced formulations for hair and skin. Recent industry launches indicate that the forthcoming phase of competition will focus on biotechnology, environmentally sustainable chemistries, and high-value claims, rather than merely on commodity volume.

LIST OF KEY PERSONAL CARE CHEMICALS COMPANIES PROFILED IN REPORT

- BASF SE (Germany)

- Croda International plc (U.K.)

- Evonik Industries AG (Germany)

- Clariant AG (Switzerland)

- Symrise AG (Germany)

- Lubrizol Corporation (U.S.)

- Ashland Inc. (U.S.)

- Solvay SA (Belgium)

- Dow (U.S.)

- Givaudan Active Beauty (Switzerland)

KEY INDUSTRY DEVELOPMENTS

- March 2026: Symrise introduced Cellexora™ MD, a plant-derived exosome-based cosmetic ingredient sourced from upcycled Italian apple side streams, aimed at long-term skin regeneration and vitality.

- September 2025: Croda launched Zenakine™, a biotech-based neuroactive ingredient designed to counteract stress effects on the skin.

April 2025: BASF launched natural-based innovations for personal care at in-cosmetics Global 2025, reinforcing its push into sustainable surfactants, emollients, polymers, active systems, and UV filters - April 2025: Clariant introduced “Clariant Beauty,” launching new solutions across skin care, hair care, and sun protection categories under a sustainability and performance-led platform

REPORT COVERAGE

The global personal care chemicals market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on market dynamics and trends expected to drive the market during the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market shares and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.7% from 2026-2034 |

| Unit | Value (USD Billion) and Volume (Kiloton) |

| Segmentation | By Type, Application, and Region |

| By Type |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 57.79 billion in 2025 and is projected to reach USD 95.96 billion by 2034.

Recording a CAGR of 5.7%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

The skin care application segment led in 2025.

Asia Pacific held the highest market share in 2025.

Premium skin, hair, and suncare formulations are raising ingredient intensity per product and accelerating the adoption of personal care chemicals.

- 2021-2034

- 2025

- 2021-2024

- 167

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us