Polyester Film Market Size, Share & Industry Analysis, By Type (Biaxially Oriented Polyester (BOPET) Film, Metallized Polyester Film, and Others), By Application (Packaging, Electrical & Electronics, Industrial, Imaging & Photographic, and Others), and Regional Forecast, 2025-2032

KEY MARKET INSIGHTS

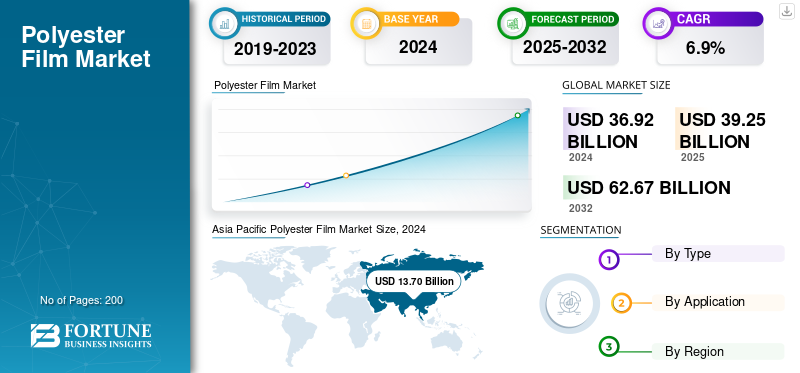

The global polyester film market size was valued at USD 36.92 billion in 2024. The market is projected to grow from USD 39.25 billion in 2025 to USD 62.67 billion by 2032, exhibiting a CAGR of 6.9% during the forecast period. The Asia Pacific dominated global market with a share of 37.11% in 2024.

Polyester film is a thin, flexible plastic film made from polyethylene terephthalate (PET), a thermoplastic polymer belonging to the polyester family. It is produced through extrusion and biaxial orientation, where molten PET resin is stretched in machine and transverse directions to enhance its strength, clarity, and dimensional stability. It is widely recognized for its high tensile strength, moisture resistance, low gas permeability, and excellent dielectric characteristics, making it suitable for packaging and tec

hnical applications. In packaging, they are used for food, beverage, and pharmaceutical products due to their ability to preserve freshness and protect against environmental factors. In industrial and electronic applications, ester films are used as insulation materials, substrates for printing and lamination, and components in flexible circuits and solar panels.

The polyester film market is driven by the rising demand for durable and lightweight packaging materials, particularly in the food, beverage, and pharmaceutical sectors. The expansion of the electronics and electrical industry boosts the use of films for insulation and flexible circuits. The increasing emphasis on sustainable and recyclable materials supports the innovation of bio-based and recyclable PET films. Additionally, technological advancements in coating and metallizing processes enhance film performance, expanding applications in solar, automotive, and industrial sectors.

Furthermore, the market encompasses several major players, including TEKRA, LLC., Ester Industries Limited, Jindal Films Limited, Kolon Industries, and Mitsubishi Polyester Film GmbH. A broad portfolio, innovative product launches, and strong geographic presence expansion have supported the dominance of these companies in the global market.

Download Free sample to learn more about this report.

Polyester Film Market KEY TAKEAWAYS

- 2024 Market Size: USD 36.92 billion

- 2025 Market Size: USD 39.25 billion

- 2032 Forecast Market Size: USD 62.67 billion

- CAGR: 6.9% from 2025–2032

- Asia Pacific dominated the market with a 37.11% share in 2024.

- Biaxially Oriented Polyester (BOPET) film segment held the largest market share.

- Packaging segment is projected to hold a 38.9% share in 2025.

Asia Pacific

USD 13.70 billion in 2024. Strong growth driven by flexible packaging demand, electronics manufacturing, and photovoltaic applications supported by rapid urbanization and e-commerce expansion.

Europe

USD 7.11 billion in 2025. Driven by strict sustainability regulations and strong demand from packaging, electronics, and renewable energy sectors.

North America

USD 10.82 billion in 2025. Growth supported by high-performance packaging demand and expansion in EV, solar, and electronics industries.

U.S.

USD 9.09 billion in 2025. Demand driven by food & beverage packaging, electrical insulation films, and sustainable packaging initiatives.

China

USD 4.25 billion in 2025. Driven by electronics, PV production, packaging growth, and strong PET supply chain integration.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Expanding Demand for Flexible and Sustainable Packaging Solutions to Propel the Market Growth

Biaxially oriented polyethylene terephthalate (BOPET) offers superior tensile strength, clarity, and barrier properties, making it ideal for packaging food, beverages, pharmaceuticals, and personal care products. The growing consumer preference for lightweight, durable, and re-sealable packaging has led to widespread adoption of this sustainable alternative to rigid plastics. Major FMCG and food brands are incorporating PET-based flexible packaging to reduce plastic waste and carbon footprint. These factors contributed to a positive rise in polyester film market growth.

- For instance, Nestlé and PepsiCo have transitioned to recyclable PET laminates in their snack and beverage packaging. The material’s low oxygen and moisture permeability also helps extend shelf life, reducing food spoilage and waste, an important consideration for manufacturers facing sustainability mandates.

MARKET RESTRAINTS

Hike in Crude Oil Prices and Disruption of Supply Chain Led to Market Hindrance

Petroleum-based feedstock’s fluctuations in global crude oil prices directly affect polyester resin production costs. During oil price spikes or supply chain disruptions, manufacturers experience squeezed profit margins and pricing uncertainty.

- For instance, the Russia-Ukraine conflict in 2022 caused significant instability in oil and petrochemical markets, raising the cost of PTA and MEG and increasing production expenses for polyester films. This volatility complicates long-term contract pricing, with packaging and electronics manufacturers demanding stable cost structures.

MARKET OPPORTUNITIES

Rising Demand from the Solar and Renewable Energy Sector to Create Lucrative Growth Opportunities

PET films are critical in solar photovoltaic (PV) modules, where they are used as backsheet and encapsulation layers due to their strong insulation, UV stability, and weather resistance. These films help protect solar cells from mechanical and environmental stress, thereby extending module lifespan and efficiency.

- Companies such as DuPont Teijin Films and SKC Inc. have developed advanced polyester films tailored for PV applications, including high-reflectivity and hydrolysis-resistant variants. In building-integrated photovoltaics (BIPV) and energy-efficient construction, these films are utilized in low-emissivity (Low-E) and solar control window coatings, thereby reducing heat transmission and enhancing energy performance.

Governments worldwide promote renewable energy through subsidies and carbon neutrality goals, increasing demand for these materials. For instance, India’s National Solar Mission and Europe’s Green Deal have significantly increased solar module installations, directly benefiting film consumption.

MARKET CHALLENGES

Environmental Concerns and Plastic Waste Regulations to Hamper Market Growth

Governments and regulatory bodies in Europe and North America have introduced stringent waste management and extended producer responsibility (EPR) norms that penalize non-recyclable packaging formats.

- For example, the European Union’s Directive on Single-Use Plastics and Packaging Waste targets the reduction of multilayer film waste, pressuring manufacturers to develop mono-material or recyclable alternatives. Similarly, India’s Plastic Waste Management Rules (2022) mandate recyclability and traceability in flexible packaging. These measures increase the compliance costs of film producers and may limit the use of conventional PET films in specific packaging applications.

POLYESTER FILM MARKET TRENDS

Technological Advancements and Product Innovation Led to Significant Market Trends

Innovations in film orientation, coating, and metallization technologies have enabled manufacturers to tailor film properties for specific end-use requirements. Advanced coating processes enhance barrier performance, printability, and surface energy, thereby facilitating applications in electronics, packaging, and industrial laminates. Metallized PET films, for example, offer enhanced light and gas barrier properties for capacitor and packaging applications.

- Manufacturers such as Toray Industries and Polyplex Corporation are investing in high-speed, energy-efficient film lines and surface-modification technologies to meet evolving performance demands.

Download Free sample to learn more about this report.

Segmentation Analysis

By Type

Increasing Demand From Various Sectors Led the Biaxially Oriented Polyester (BOPET) Film Segment’s Growth

The market is segmented by type into biaxially oriented polyester (BOPET) film, metallized polyester film, and others.

The Biaxially Oriented Polyester (BOPET) film segment held the largest polyester film market share in 2024 and is expected to experience substantial growth. This growth is driven by its widespread adoption across packaging, electrical insulation, and industrial applications, owing to its superior mechanical strength, dimensional stability, and optical clarity. The global shift toward lightweight, durable, and recyclable packaging materials has substantially increased the use of BOPET films in flexible food and beverage packaging.

The growth of the metallized polyester film segment is driven by its enhanced barrier and decorative properties, which make it essential in packaging, insulation, and capacitor applications. These films combine the mechanical durability of PET with the reflective and barrier properties of metals such as aluminum, providing superior protection against light, moisture, and oxygen.

By Application

Owing to the Increasing Demand from food, Beverage, and Pharmaceutical applications, the packaging segment led the market.

Based on application, the market is segmented into packaging, electrical & electronics, industrial, imaging & photographic, and others.

To know how our report can help streamline your business, Speak to Analyst

The packaging segment dominates the market, driven by the global demand for flexible, lightweight, and durable packaging materials. Polyester (BOPET) films offer excellent barrier properties against oxygen, moisture, and aroma, making them ideal for food, beverage, and pharmaceutical applications that require extended shelf life and product protection. Furthermore, the segment is set to hold a 38.9% share in 2025.

The electrical & electronics segment is witnessing favorable growth throughout the forecast period. This expansion is attributed to its widespread use for insulation, dielectric, and protective applications due to its superior thermal stability, electrical strength, and dimensional consistency. BOPET films serve as key materials in capacitors, cable wraps, flexible printed circuits, and motor insulation, supporting modern electronics' ongoing miniaturization and efficiency demands. In addition, electrical & electronics applications are projected to grow at a CAGR of 7.1% during the study period.

The growth of the industrial segment in the market is driven by the increasing demand from diverse applications, including solar backsheets, release liners, graphic films, and insulation tapes. Its ability to withstand harsh environments, exposure to UV radiation, solvents, and temperature extremes, drives use across the construction, automotive, and renewable energy sectors.

The imaging and photographic segment is driven by the use of films as stable, transparent substrates in printing, x-ray, and graphic media. Polyester films replaced traditional cellulose acetate bases because of their superior dimensional stability, clarity, and chemical resistance. In medical imaging, PET films are used in X-ray and diagnostic films, where precision, flatness, and moisture resistance are critical.

Polyester Film Market Regional Outlook

By region, the market is categorized into North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

Asia Pacific

Asia Pacific Polyester Film Market Size, 2024 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific held the dominant share in 2023, valued at USD 12.84 billion, and maintained its leading position in 2024, with a value of USD 13.70 billion. The factors that foster the region's dominance include rising consumer spending, urbanization, and e-commerce penetration, which are fueling the growth of flexible packaging. Asia’s electronics and photovoltaic manufacturing leadership also underpins strong demand for high-performance PET films. With increasing regulatory emphasis on sustainability, countries such as Japan and South Korea are investing in the development of recycled and bio-based PET films. In 2025, the Chinese market is estimated to reach USD 4.25 billion.

- China is the fastest-growing market, driven by its massive production capacities, cost advantages, and integration of upstream PET resin supply. The country’s rapid industrialization and strong electronics manufacturing ecosystem, particularly in display panels, photovoltaic modules, and lithium-ion batteries, drive the demand for advanced polyester films. Moreover, China’s growing domestic packaging industry, supported by rising e-commerce penetration and demand for consumer goods, significantly increases the use of BOPET and metallized films. The government’s push for a circular economy and green manufacturing, including PET recycling initiatives, also promotes sustainable film development.

To know how our report can help streamline your business, Speak to Analyst

Europe

Europe is expected to experience growth in the polyester film market in the coming years. During the forecast period, the European region is projected to record a growth rate of 6.5%, the second-highest among all regions, and reach a valuation of USD 7.11 billion by 2025. The market's growth is driven by strong regulations such as the European Packaging Waste Directive and circular economy initiatives. Germany, the UK, France, and Italy lead in demand, particularly from the packaging, electronics, and renewable energy industries. The European market prioritizes recyclable mono-material packaging and films with a lower environmental impact, driving investment in chemical recycling and the utilization of post-consumer PET. Backed by these factors, countries including the U.K. are expected to record the valuation of USD 0.83 billion, Germany to record USD 1.49 billion, and France to record USD 0.82 billion in 2025.

North America

After Europe, the market in North America is estimated to reach USD 10.82 billion in 2025 and secure the position of the third-largest region in the market. A strong emphasis on sustainability and high-performance materials drives the market's growth. The U.S. leads the region, with major consumption in food packaging, flexible laminates, and electrical insulation films. Growth is further supported by the expansion of EV manufacturing, solar power installations, and advanced electronics, which rely on PET films for capacitors, flexible circuits, and solar back sheets. In 2025, the U.S. market is estimated to reach USD 9.09 billion.

- In the U.S., the market is driven by the growing demand for high-performance packaging materials and technological advancements in flexible packaging and electrical insulation applications. The country’s robust food, beverage, and pharmaceutical industries rely heavily on BOPET films due to their superior tensile strength, thermal stability, and barrier properties. The trend toward sustainable and recyclable packaging films, supported by initiatives such as the U.S. Plastics Pact, further encourages manufacturers to innovate in recyclable and biobased films. Moreover, investments in electrical and electronic infrastructure, such as energy-efficient transformers and EV components, drive film use in insulation, capacitors, and flexible circuits.

Latin America

Over the forecast period, the Latin America and Middle East & Africa regions are expected to witness moderate growth in this market. The Latin America market in 2025 is set to record USD 3.93 billion in valuation. The market's growth is driven by the expansion of consumer goods and packaging sectors in countries such as Brazil and Mexico. Rising urbanization and retail modernization have increased demand for flexible packaging, particularly in food and beverage applications.

Middle East & Africa

In the Middle East and Africa, the GCC is expected to reach a value of USD 1.21 billion in 2025. The market’s growth is attributed to rising demand for packaging and electrical insulation applications. The GCC countries, especially Saudi Arabia and the UAE, are investing in packaging manufacturing and industrial diversification, boosting demand for PET films in flexible laminates and labeling.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Market Participants Witness Significant Growth Opportunities with Innovative Packaging Solutions

The global market is highly fragmented and competitive. In terms of market share, a few major market players dominate the market industry by offering innovative packaging solutions. These major players in the market are constantly focusing on innovation and expanding their customer base across the regions.

Major players in the market include TEKRA, LLC., Ester Industries Limited, Jindal Films Limited, Kolon Industries, Mitsubishi Polyester Film GmbH, and others. Numerous other players operating in the industry are focused on delivering advanced packaging solutions.

LIST OF KEY POLYESTER FILM COMPANIES PROFILED

- TEKRA, LLC. (U.S.)

- Ester Industries Limited (India)

- Jindal Films Limited (India)

- Kolon Industries (South Korea)

- Mitsubishi Polyester Film GmbH (Germany)

- Polyplex Corporation Limited (India)

- Sumilon Polyester Ltd. (India)

- Terphane LLC (U.S.)

- Toray Industries (Japan)

- Toyobo Co. Ltd. (Japan)

KEY INDUSTRY DEVELOPMENTS

- March 2024: Mitsubishi Chemical Corporation introduced new biodegradable polyester films that would meet the rising demand among customers for sustainable packaging alternatives. This environmentally benign solution would serve relevant industries that are switching to polymer sustainability.

- October 2021: Mitsubishi Chemical Corporation committed an investment of USD 127 million to expand the polyester film capacity of its German subsidiary Mitsubishi Polyester Film GmbH in Wiesbaden, adding an annual capacity of 27,000 tons. This expansion is to be completed by the end of 2024.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2019-2032 |

|

Base Year |

2024 |

|

Estimated Year |

2025 |

|

Forecast Period |

2025-2032 |

|

Historical Period |

2019-2023 |

|

Growth Rate |

CAGR of 6.9% from 2025-2032 |

|

Unit |

Value (USD Billion), Volume (Kiloton) |

|

Segmentation |

By Type, Application, and Region |

|

By Type |

|

|

By Application |

|

|

By Region |

o Rest of Middle East & Africa (By Application) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 36.92 billion in 2024 and is projected to reach USD 62.67 billion by 2032.

In 2024, the market value stood at USD 51.36 billion.

The market is expected to exhibit a CAGR of 6.9% during the forecast period of 2025-2032.

The biaxially oriented polyester (BOPET) film segment led the market by Type.

The key factors driving the market’s increasing use in flexible packaging, electrical insulation, and industrial applications are its excellent tensile strength, barrier properties, and dimensional stability.

TEKRA, LLC., Ester Industries Limited, Jindal Films Limited, Kolon Industries, and Mitsubishi Polyester Film GmbH are among the prominent players in the market.

Asia Pacific dominated the market in 2024.

The increasing demand for sustainable and recyclable film solutions, as well as the growing use in electronics and solar applications, are some of the factors expected to favor product adoption.

- 2019-2032

- 2024

- 2019-2023

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us