Polymer Nanocomposites Market Size, Share & Industry Analysis, By Nanofiller Type (Nanoclays, Carbon Nanotubes, Nano-CaCO₃, and Others), By Application (Packaging, Automotive, Electronics, Construction, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

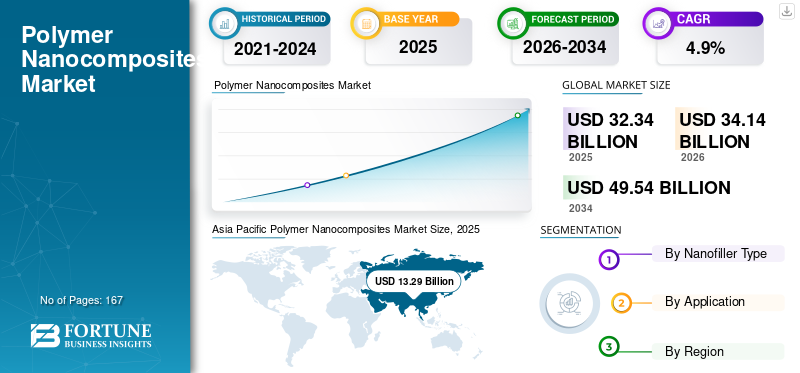

The global polymer nanocomposites market size was valued at USD 32.34 billion in 2025. The market is projected to grow from USD 34.14 billion in 2026 to USD 49.54 billion by 2034, exhibiting a CAGR of 4.9% during the forecast period. Asia Pacific dominated the global polymer nanocomposites market with a market share of 41.09% in 2025.

Polymer nanocomposites are engineered materials that incorporate nanoscale fillers into polymer matrices to achieve stronger, lighter, and more functional performance than conventional polymers. Their ability to enhance mechanical strength, barrier behaviour, thermal stability, and conductivity at low loading levels makes them valuable across packaging, automotive, electronics, construction, and industrial markets where legacy polymer systems no longer meet rising performance expectations.

The growth of the polymer nanocomposites market is shaped by a mix of established materials producers and nanotechnology specialists. Key participants include nanoComposix, Polymer Composites Inc., Makevale Group, Arkema, Evonik Industries AG, Nanocyl SA, Resonac Corporation, Mitsui Chemicals, Nanoshell LLC, and RTP Company. Their focus on nanofiller innovation, dispersion technologies, and application-specific formulations underpins their competitive positioning, while close engagement with converters and OEMs supports ongoing adoption across high-growth end-use sectors.

Download Free sample to learn more about this report.

Polymer Nanocomposites Market Key Takeaways

- 2025 Market Size: USD 32.34 billion

- 2026 Market Size: USD 34.14 billion

- 2034 Forecast Market Size: USD 49.54 billion

- CAGR: 4.9% from 2026–2034

- Asia Pacific dominated the global polymer nanocomposites market with a 41.09% share in 2025.

- Carbon nanotubes segment accounted for the dominant market share in 2025.

- Electronics segment held the largest market share globally in 2025.

North America

North America benefited from advanced R&D capabilities and rising EV and electronics demand.

Asia Pacific

Asia Pacific held the leading market position with USD 13.29 billion in 2025.

Europe

Europe witnessed strong growth driven by sustainability initiatives and circular economy regulations.

U.S.

Robust research ecosystem and EV growth accelerate adoption of advanced nanocomposite materials.

Japan

Advanced materials innovation supports adoption in high-performance electronics and automotive applications.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Rising Performance Requirements Are Accelerating the Shift toward Nano-Enhanced Polymers

Industries are increasingly demanding lighter, stronger, and more durable materials capable of meeting elevated mechanical, thermal, and barrier expectations without requiring fundamental changes to existing processing infrastructure. They address this need by delivering substantial performance gains at low filler loadings, enabling converters to meet stringent lightweighting, sustainability, and reliability objectives across various applications, including packaging, automotive, electronics, and construction.

It now functions as a practical “performance upgrade pathway” for processors seeking better material output while retaining their current equipment, cycle times, and formulation frameworks. This alignment between rising performance pressure and the ability to integrate nanocomposites with minimal disruption is strengthening adoption momentum across both high-value and mid-volume segments.

- According to Composites Science and Technology (2022), nanoclay- and CNT-reinforced polymers can deliver reinforcement levels comparable to microfillers at 10–20% lower loading, which directly contributes to weight reduction and improved processing efficiency.

MARKET RESTRAINTS

High Nanofiller Costs Are Limiting Adoption in Price-Sensitive Segments

Nanofillers such as CNTs, nanoclays, and metal oxides continue to carry higher production and surface-treatment costs, creating sustained pricing pressure for compounders and converters operating in margin-sensitive markets. Beyond raw material pricing, processors often face added expense related to dispersion optimization, screw configuration adjustments, drying requirements, and extended formulation trials. These cumulative cost layers reduce the economic attractiveness of nanocomposites in high-volume applications where incremental performance gains may not immediately justify the price premium, ultimately slowing broader substitution of conventional fillers in cost-driven end-use segments.

- According to Cabot’s CNT product literature (2024), carbon nanotubes remain significantly more expensive than standard fillers, such as carbon black or talc, which restricts their commercial use largely to applications where the performance uplift provides clear economic justification.

MARKET OPPORTUNITIES

Improvements in Dispersion and Surface Modification to Boost Product Adoption

Advances in nanofiller surface treatments, compatibilizers, and the incorporation of masterbatches are steadily reducing long-standing dispersion challenges. As dispersion becomes more reliable, converters can achieve consistent mechanical, barrier, and thermal improvements across different polymer systems. This growing level of process predictability is widening the scope for nanocomposites, allowing them to move from niche technical applications into larger-volume product categories.

- According to the peer-reviewed journal Polymers (MDPI), progress in nanoclay surface modification has “significantly improved dispersion quality,” enabling more uniform performance gains across commercial polymer matrices.

POLYMER NANOCOMPOSITES MARKET TRENDS

Sustainability Priorities Are Steering R&D toward Bio-Based Nanocomposites

Companies are increasingly allocating resources toward the development of polymer nanocomposites based on bio-derived matrices or environmentally compatible nanofillers, as sustainability expectations rise across major end-use sectors. This shift is driven by customer demand for lower-carbon materials, stricter regulatory direction, and the need to future-proof product portfolios. Bio-based nanocomposites are gaining traction as a way to retain the performance benefits of nano-enhancement while reducing dependence on conventional fossil-derived polymers.

This trend is influencing investment decisions, with material producers expanding work on renewable resins, natural nanofillers, and recyclable composite systems. These developments reflect a broader push to align next-generation polymer solutions with corporate ESG goals and circular-economy requirements.

MARKET CHALLENGES

Lack of Standardized Testing and Safety Frameworks Is Slowing Market Growth

Despite technical progress, the absence of harmonized standards for nanoparticle handling, migration, and performance evaluation continues to slow qualification cycles, thereby slowing polymer nanocomposites market growth. In the absence of unified regulatory frameworks, processors and end-users often rely on internal testing protocols, leading to inconsistent benchmarks across regions and applications. This uncertainty is particularly restrictive in sectors such as food packaging, medical products, and high-reliability components, where regulatory clarity and long-term safety validation are essential. Until standardized methods become widely accepted, scale-up and cross-industry adoption will remain slower than the technology’s performance potential.

- According to the OECD Working Party on Manufactured Nanomaterials (2023), globally unified testing and safety standards for nanomaterials are still lacking, which forces companies to depend on internal evaluation methods when assessing nano-enabled products.

Download Free sample to learn more about this report.

Segmentation Analysis

By Nanofiller Type

Carbon Nanotubes Segment Dominated due to their Exceptional Electrical Conductivity

Based on nanofiller type, the market is classified into nanoclays, carbon nanotubes, nano-CaCO₃, and others.

To know how our report can help streamline your business, Speak to Analyst

The carbon nanotubes segment accounted for the dominant share of the polymer nanocomposites market in 2025. CNTs lead the nanofiller category due to their exceptional electrical conductivity, mechanical reinforcement, and thermal stability allow them to deliver high performance at very low loading levels. These characteristics make CNT-based nanocomposites suitable for conductive components, EMI shielding, EV battery structures, lightweight automotive parts, and advanced electronics. Their ability to combine strength, functionality, and durability within polymer systems reinforces their position as the preferred nanofiller in high-value, technology-intensive applications.

- The National Institute of Standards and Technology (NIST) notes that carbon nanotubes exhibit extremely high electrical conductivity and tensile strength at low concentrations, which makes them valuable additives for improving the performance of polymer materials.

By Application

Electronics Segment Led the Market due to its Properties

In terms of application, the market is categorized into packaging, automotive, electronics, construction, and others.

The electronics segment accounted for the largest polymer nanocomposites market share in 2025 and is expected to dominate during the forecast period. Electronics manufacturers are increasingly adopting nano-enhanced polymers as they deliver the conductivity, thermal stability, mechanical strength, and miniaturization capabilities required in modern devices. Carbon nanotubes, graphene derivatives, and oxide nanofillers enable heat dissipation, EMI shielding, electrostatic control, and improved structural performance within lightweight polymer systems. As electronic products continue to shrink while integrating more functionality, it remains the preferred material solution for reliability and performance.

- A 2024 study published in Heliyon reports that CNT-enhanced polymer nanocomposites deliver significant improvements in mechanical strength while simultaneously enhancing electrical and thermal functionality, underscoring their suitability for high-performance electronic components that require both structural integrity and functional properties.

The automotive segment is expected to grow at a CAGR of 4.8% over the forecast period.

Polymer Nanocomposites Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Polymer Nanocomposites Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant share in 2025, valued at USD 13.29 billion. The region leads the polymer nanocomposites market due to its extensive plastics processing base and a strong presence in the packaging, automotive, electronics, and construction industries. China anchors demand with scale in manufacturing and diversified end-use sectors, while Japan and South Korea support high-performance adoption through advanced materials capabilities. India continues to expand usage as converters integrate nano-enabled materials into packaging and automotive product lines.

To know how our report can help streamline your business, Speak to Analyst

Europe

Europe’s regulatory pressures, circular economy programs, and sustainability-led material substitution are accelerating the shift toward nano-enhanced polymers. Germany, France, and Italy serve as core hubs, where automotive, engineering plastics, and advanced packaging sectors increasingly rely on nanocomposites to meet lightweighting and performance targets. The region benefits from a strong institutional focus on long-term material efficiency, supporting steady integration across high-value applications.

North America

North America benefits from a mature ecosystem for high-performance polymers supported by automotive, aerospace, electronics, and consumer packaging industries. Strong R&D capabilities, robust industry-university collaboration, and established experience with composite materials enable faster integration of nanocomposites across applications that require mechanical, thermal, or barrier enhancements. Functional nanocomposites are gaining traction as EVs and electronics drive demand for conductive and thermally stable polymer systems.

Latin America

Latin America exhibits steady demand, driven by flexible and rigid packaging, automotive assembly, and select industrial applications. Brazil and Mexico remain the primary markets, as local processors increasingly explore nano-enhanced materials to enhance packaging durability, improve barrier properties, and meet rising sustainability expectations. Regional growth remains closely tied to industrial modernization and the expansion of consumer-goods sectors.

Middle East & Africa

The Middle East & Africa region is at an early stage, but shows growing potential. Downstream plastic manufacturing in the Gulf is expanding under diversification programs, creating opportunities for nano-enabled materials in packaging, pipes, and industrial components. Construction growth and renewable energy investments in the UAE, Saudi Arabia, Egypt, and South Africa support the gradual inclusion of nano-enhanced polymers into local value chains. Over time, continued material upgrades across key industries are expected to drive broader adoption of the product across these regions.

COMPETITIVE LANDSCAPE

Key Industry Players

Material innovation and Application-focused engineering are shaping competition in the Polymer Nanocomposites Market

The polymer nanocomposites market is shaped by companies that combine nanofiller expertise with strong polymer capabilities and reliable processing support. Competition centers on delivering consistent performance at low loading levels, ensuring stable dispersion, and meeting functional requirements across various applications, including electronics, automotive, packaging, and industrial sectors. Players who can align nanofiller chemistry, polymer design, and application engineering hold a stronger competitive position as end-users push for lightweighting, miniaturization, and functional enhancement.

Key companies in the market include Arkema, Evonik, Mitsui Chemicals, Resonac Corporation, Nanocyl SA, RTP Company, Makevale Group, Polymer Composites Inc., Nanoshell LLC, and nanoComposix. Large polymer and specialty chemical firms bring high-performance resin systems and advanced additives, while nanomaterial specialists provide CNTs, nanoclays, and oxide-based fillers. Compounders and formulators convert these materials into application-ready masterbatches and compounds for converters and OEMs.

Moreover, companies are enhancing their competitiveness through improved nanofiller dispersion, advanced surface modification technologies, and higher-performance polymer matrices. Strategic priorities include recyclable and circular-grade polymers, conductive and thermally stable formulations for electronics, and automotive materials that support lightweighting and durability. Firms that integrate materials expertise with technical service and close customer collaboration are best positioned as polymer nanocomposites continue to expand into high-demand, performance-driven applications.

LIST OF KEY POLYMER NANOCOMPOSITES COMPANIES PROFILED

- Polymer Composites Inc. (U.S.)

- Makevale Group (U.K.)

- Arkema (France)

- Evonik (Germany)

- Nanocyl SA. (Belgium)

- Resonac Corporation (Japan)

- Mitsui Chemicals, Inc. (Japan)

- Nanoshell LLC (U.S.)

- RTP Company (U.S.)

- nanoComposix (U.S.)

KEY INDUSTRY DEVELOPMENTS

- October 2025: Evonik partnered with Schneider Electric to automate a thermoplastic processing and recycling plant at its Essen site. The collaboration aims to improve process efficiency, optimize the use of recycling additives, and strengthen Evonik’s broader circular plastics

- October 2025: Evonik announced that it will present its latest polymer chemistry innovations at K-Fair 2025 in Düsseldorf. The showcase features new mass-balanced, high-performance polymers, including PA12 and PEEK, reinforcing the company’s commitment to circular and sustainable polymer systems.

- September 2025: Mitsui Chemicals signed a Memorandum of Understanding with Idemitsu Kosan and Sumitomo Chemical to integrate Sumitomo’s PP and LLDPE businesses into their existing polyolefin group. The move is designed to strengthen supply competitiveness, enhance portfolio efficiency, and support long-term growth in high-performance polyolefins.

- June 2023: Arkema acquired a controlling stake in PI Advanced Materials, a global leader in polyimide films used in electronics and EVs. This acquisition expands Arkema’s advanced polymer portfolio with ultra-high-performance polyimides for applications such as batteries, displays, semiconductors, and flexible electronics.

- November 2021: Mitsui Chemicals and Microwave Chemical launched a joint initiative to commercialize microwave-based chemical recycling technology capable of converting difficult-to-recycle plastics directly back into monomers. The approach aims to lower emissions and increase the recyclability of composite and polymer waste streams.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.9% from 2026-2034 |

|

Unit |

Value (USD Billion) Volume (Kiloton) |

|

Segmentation |

By Nanofiller Type, Application, and Region |

|

By Nanofiller Type |

· Nanoclays · Carbon Nanotubes · Nano-CaCO₃ · Others |

|

By Application |

· Packaging · Automotive · Electronics · Construction · Others |

|

By Geography |

· North America (By Nanofiller Type, Application, and Country) o U.S. (By Application) o Canada (By Application) · Europe (By Nanofiller Type, Application, and Country/Sub-region) o Germany (By Application) o U.K. (By Application) o France (By Application) o Italy (By Application) o Rest of Europe (By Application) · Asia Pacific (By Nanofiller Type, Application, and Country/Sub-region) o China (By Application) o Japan (By Application) o India (By Application) o South Korea (By Application) o Rest of Asia Pacific (By Application) · Latin America (By Nanofiller Type, Application, and Country/Sub-region) o Brazil (By Application) o Mexico (By Application) o Rest of Latin America(By Application) · Middle East & Africa (By Nanofiller Type, Application, and Country/Sub-region) o Saudi Arabia (By Application) o South Africa (By Application) o Rest of the Middle East & Africa (By Application) |

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 32.34 billion in 2025 and is projected to reach USD 49.54 billion by 2034.

Recording a CAGR of 4.9%, the market is slated to exhibit steady growth during the forecast period (2026-2034).

The electronics segment led in 2025.

Asia Pacific held the highest market share in 2025.

nanoComposix, Polymer Composites Inc., Makevale Group, Arkema, and Evonik Industries AG are some of the top players in the market.

Improvements in dispersion and surface modification are expected to boost product adoption.

Rising performance requirements are accelerating the shift toward nano-enhanced polymers.

- 2021-2034

- 2025

- 2021-2024

- 167

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us