Robotic Wing Assembly Systems Market Size, Share & Industry Analysis, By Aircraft Type (Commercial Aircraft, Military Aircraft, and Others), By Automation Level (Fully Automated Systems, Semi-Automated Systems, and Others), By Application (Wing Skin Drilling & Fastening, Wing Panel & Spar Assembly, Composite Wing Assembly, and Others), and Regional Forecast, 2026-2034

Robotic Wing Assembly Systems Market Size and Future Outlook

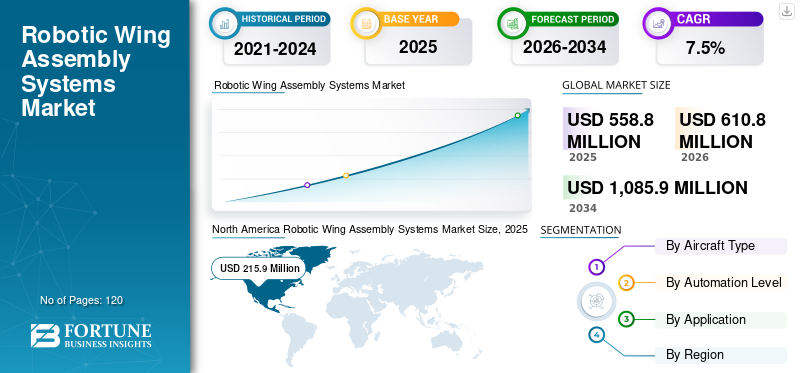

The global robotic wing assembly systems market size was valued at USD 558.8 million in 2025. The market is projected to grow from USD 610.8 million in 2026 to USD 1,085.9 million by 2034, exhibiting a CAGR of 7.5% during the forecast period. North America dominated the robotic wing assembly systems market with a market share of 38.64% in 2025.

Robotic wing assembly systems refer to advanced automated manufacturing solutions used in aircraft production for drilling, fastening, panel alignment, composite integration, and structural assembly of aircraft wings. These systems enhance precision, reduce labor dependency, and improve production throughput in the manufacturing of commercial and military aircraft.

The market is witnessing steady expansion driven by rising aircraft production rates, increasing demand for lightweight composite wings, and the aerospace industry's shift toward Industry 4.0-enabled manufacturing environments. Aircraft OEMs are investing heavily in fully automated robotic drilling and fastening systems to enhance structural high precision and reduce assembly cycle times.

Major players such as Airbus SE, The Boeing Company, KUKA AG, FANUC Corporation, ABB Ltd., Electroimpact Inc., Broetje-Automation GmbH, MTorres, Kawasaki Heavy Industries, and Fives Group are actively advancing robotic wing assembly capabilities.

- For instance, in July 2023, Airbus inaugurated a new automated wing assembly line in the U.K., integrating advanced robotics and digital manufacturing systems to support the ramp-up of A320 family production.

Download Free sample to learn more about this report.

ROBOTIC WING ASSEMBLY SYSTEMS MARKET TRENDS

Integration of Fully Automated and Digital Twin Technologies Transforming Wing Manufacturing

A key trend shaping the market is the adoption of fully automated robotic drilling and fastening systems integrated with digital twin technologies. Aerospace manufacturers are increasingly deploying advanced robotics capable of high-precision hole drilling, automated fastening, and real-time quality monitoring.

In addition, composite wing manufacturing requires complex automated handling systems, driving demand for robotic integration with AI-enabled inspection and predictive maintenance capabilities.

- For instance, in 2024, Boeing expanded the use of robotic drilling systems at its 777X production facilities, enhancing automation in wing structural assembly processes.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Commercial Aircraft Production and Precision Manufacturing Driving Market Growth

Increasing global air travel demand has accelerated commercial aircraft production, creating strong rise in the robotic wing assembly systems market growth. Aircraft wings require high structural accuracy, and robotic systems provide repeatable precision while reducing manufacturing defects.

Furthermore, aerospace OEMs are investing in production scalability to meet order backlogs, further driving demand for fully automated wing assembly solutions.

- For instance, in 2024, Airbus increased its A320 family production targets, supporting further investments in automated wing-manufacturing infrastructure.

MARKET RESTRAINTS

High Capital Investment and Integration Complexity Restricting Adoption

Robotic wing assembly systems require substantial capital expenditure and complex integration with existing production lines. Smaller aerospace manufacturers may face financial constraints when adopting fully automated systems.

Additionally, workforce retraining and technical expertise requirements may slow the transition from semi-automated to fully automated systems.

- For instance, in 2024, aerospace manufacturers highlighted cost challenges associated with next-generation automation upgrades during industry forums, emphasizing phased adoption strategies.

MARKET OPPORTUNITIES

Composite Wing Manufacturing and Lightweight Aircraft Programs Creating Growth Opportunities

The increasing use of carbon fiber reinforced polymer (CFRP) wings in modern aircraft is creating new opportunities for robotic assembly systems. Composite wing structures require specialized robotic handling, precision drilling, and automated inspection.

New aircraft programs focusing on fuel efficiency and lightweight designs are expected to drive further investments in robotic composite wing assembly systems.

- For instance, in 2023, Boeing continued automation expansion for 787 composite wing production, supporting higher throughput and precision control.

Segmentation Analysis

By Aircraft Type

Commercial Aircraft Segment Dominates the Market Due to High-Volume Production Programs

Based on aircraft type, the market is segmented into commercial aircraft, military aircraft, and others.

The commercial aircraft segment holds the largest market share, driven by high-volume production programs such as single-aisle and wide-body aircraft, which require automated precision assembly systems.

- For instance, Airbus and Boeing continue ramping up commercial aircraft production, reinforcing demand for robotic wing-assembly infrastructure.

The commercial aircraft segment is also projected to register the highest CAGR of 7.9% during the forecast period, supported by sustained airline fleet expansion.

To know how our report can help streamline your business, Speak to Analyst

By Automation Level

Fully Automated Systems Leads the Segmental Growth Due to Strong Demand for Precision in Aerospace Manufacturing

Based on automation level, the market is segmented into fully automated systems, semi-automated systems, and others.

The fully automated systems segment holds the largest market share, driven by demand for precision, scalability, and reduced human intervention in aerospace manufacturing.

- For instance, KUKA AG has deployed fully automated robotic drilling solutions in aerospace manufacturing facilities, supporting advanced wing assembly.

The fully automated systems segment is also expected to record the highest CAGR of 8.1%, due to the rapid adoption of smart factory initiatives.

By Application

Wing Skin Drilling & Fastening Dominates Due to Structural Precision Requirements

Based on application, the market is segmented into wing skin drilling & fastening, wing panel & spar assembly, composite wing assembly, and others.

The wing skin drilling & fastening segment holds the largest robotic wing assembly systems market share, as precision drilling and fastening operations are critical to structural integrity.

- For instance, Electroimpact supplies automated drilling and fastening systems to major aircraft OEMs, supporting high-precision wing assembly.

The composite wing assembly segment is projected to register the highest CAGR of 8.6% over the forecast period, driven by increasing adoption of lightweight composite materials.

Robotic Wing Assembly Systems Market Regional Outlook

By region, the market is categorized into North America, Europe, Asia Pacific, South America, and the Middle East and Africa.

North America

North America Robotic Wing Assembly Systems Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America holds the largest share in the global robotic wing assembly systems market, supported by the presence of major aircraft OEMs, advanced aerospace manufacturing ecosystems, and strong defense spending. The region benefits from early adoption of Industry 4.0 technologies, robotic drilling systems, and fully automated fastening platforms integrated into high-volume aircraft production lines.

Additionally, strong investments in next-generation commercial aircraft programs and defense aviation modernization initiatives continue to drive demand for high-precision robotic wing assembly systems across the region.

U.S. Robotic Wing Assembly Systems Market

The U.S. market in 2026 is estimated at around USD 205.6 million, representing approximately 33.7% of global revenues. The presence of Boeing's large-scale commercial and military aircraft production facilities drives strong demand for advanced wing automation systems.

Increased automation solutions to support production ramp-ups and structural precision requirements further strengthen robotic system deployment across U.S. aerospace facilities.

Europe

Europe represents a mature aerospace manufacturing hub driven by Airbus production facilities and a strong robotics engineering base. The region has invested significantly in automated composite wing assembly systems, digital manufacturing platforms, and smart factory initiatives to enhance production efficiency and structural accuracy.

Cross-border aerospace collaboration across EU member states, along with sustainability-focused aircraft programs, continues to support automation upgrades in wing manufacturing lines.

U.K. Robotic Wing Assembly Systems Market

The U.K. market in 2026 is estimated at around USD 40.9 million, representing approximately 6.7% of global revenues. Airbus's wing manufacturing operations in Broughton significantly contribute to regional demand for automation.

Ongoing modernization of wing assembly lines with robotic drilling and fastening systems reinforces the country's strategic importance in global aircraft production.

Germany Robotic Wing Assembly Systems Market

Germany's market in 2026 is estimated at around USD 32.2 million, representing approximately 5.3% of global revenues. Strong robotics expertise and aerospace supply chain capabilities support the growth of automation.

Advanced manufacturing initiatives and integration of fully automated systems continue to strengthen robotic wing assembly deployment.

Asia Pacific

The Asia Pacific region is expected to register the highest CAGR of 8.7% during the forecast period, driven by expanding commercial aviation manufacturing programs and government-backed aerospace development initiatives. Increasing regional aircraft production and supply chain localization are encouraging investments in advanced robotic assembly systems.

The region is also witnessing strong adoption of composite wing technologies, which require specialized robotic drilling, fastening, and inspection systems to ensure structural reliability.

Japan Robotic Wing Assembly Systems Market

Japan's market in 2026 is estimated at around USD 19.2 million, representing approximately 3.1% of global revenues. The country's strong robotics manufacturing capabilities support the development of aerospace automation.

Collaborations between aerospace OEMs and industrial robotics companies further enhance wing assembly precision and efficiency.

China Robotic Wing Assembly Systems Market

China's market in 2026 is estimated at around USD 49.5 million, representing approximately 8.1% of global revenues. The expansion of domestic commercial aircraft programs and government-backed aerospace investments support demand for automation.

Rising localization of advanced manufacturing technologies further strengthens robotic assembly integration in Chinese aerospace facilities.

India Robotic Wing Assembly Systems Market

India's market in 2026 is estimated at around USD 32.6 million, representing approximately 5.3% of global revenues. Growing defense aviation programs and increasing support for aerospace manufacturing localization and automation investments.

Government initiatives promoting domestic aircraft production and strategic aerospace partnerships are gradually strengthening demand for robotic wing assembly systems.

South America and the Middle East & Africa

The Middle East & Africa and South America collectively represent emerging markets for robotic wing assembly systems. Growth is supported by defense modernization programs, aerospace manufacturing ambitions, and investments to strengthen domestic aviation capabilities. Although production volumes remain lower compared to North America and Europe, strategic industrial diversification initiatives are gradually increasing automation adoption.

Additionally, regional efforts to expand aerospace supply chains and attract foreign OEM partnerships are contributing to long-term demand for robotic assembly technologies, particularly in structural and composite wing applications.

GCC Robotic Wing Assembly Systems Market

The GCC market in 2026 is estimated at around USD 23.9 million, representing approximately 3.9% of global revenues. Defense aerospace modernization and investments in advanced manufacturing capabilities support automation growth.

National diversification strategies and partnerships with global aerospace manufacturers further encourage the gradual adoption of robotic wing assembly technologies.

COMPETITIVE LANDSCAPE

Key Industry Players

Automation Innovation and Strategic Aerospace Partnerships Strengthening Competitive Positioning

The global robotic wing assembly systems market is characterized by strong collaboration between aerospace OEMs and industrial robotics providers to enhance efficiency, precision, and scalability in wing manufacturing. Leading companies are investing in advanced robotic drilling and fastening systems, automated composite handling solutions, and integrated digital manufacturing platforms to support rising aircraft production rates. Continuous innovation in automation architecture is helping manufacturers improve structural accuracy while reducing assembly cycle times.

In addition, strategic partnerships and long-term supply agreements between aircraft manufacturers and automation specialists are strengthening competitive positioning. Companies are increasingly integrating smart factory technologies, real-time monitoring systems, and predictive maintenance tools to optimize wing assembly operations. Technological capability, system reliability, and integration expertise remain key differentiators in this evolving aerospace automation landscape.

LIST OF KEY ROBOTIC WING ASSEMBLY SYSTEMS COMPANIES PROFILED

- Airbus SE (Netherlands)

- The Boeing Company (U.S.)

- KUKA AG (Germany)

- ABB Ltd. (Switzerland)

- FANUC Corporation (Japan)

- Electroimpact Inc. (U.S.)

- Broetje-Automation GmbH (Germany)

- MTorres (Spain)

- Kawasaki Heavy Industries (Japan)

- Fives Group (France)

KEY INDUSTRY DEVELOPMENTS

- February 2025: Airbus expanded automation at its Broughton wing manufacturing facility to support increased A320 production rates.

- September 2024: Boeing advanced robotic wing assembly processes for the 777X program to enhance structural precision and throughput.

- June 2024: Broetje-Automation secured contracts for automated drilling systems supporting major commercial aircraft

- April 2024: KUKA AG showcased aerospace robotic drilling solutions at international aerospace manufacturing exhibitions.

- July 2023: Airbus inaugurated its new automated wing assembly line in the U.K., integrating robotics and digital manufacturing technologies.

REPORT COVERAGE

The global report on the robotic wing assembly systems market analysis includes a comprehensive study of market size & forecast across all key segments. It provides insights into market trends, drivers, restraints, opportunities, and challenges expected to influence the growth of the robotic wing assembly systems market over the forecast period. The report also covers technological advancements in digital identity and verification platforms, compliance considerations, and key strategic developments, including partnerships and M&A activity, alongside regional insights and competitive landscape analysis. Additionally, it includes regional insights and competitive landscape analysis, highlighting the market positioning and strategic initiatives of leading companies.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.5% from 2026-2034 |

| Unit | Value (USD Million) |

| Segmentation | By Aircraft Type, Automation Level, Application, and Region |

| By Aircraft Type |

|

| By Automation Level |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 558.8 million in 2025 and is projected to reach USD 1,085.9 million by 2034.

In 2025, North Americas market value stood at USD 215.9 million.

The market is expected to exhibit a CAGR of 7.5% during the forecast period.

By application, the composite wing assembly segment is expected to lead the market.

Rising commercial aircraft production and precision manufacturing are the key factors driving the market growth.

Airbus SE, The Boeing Company, KUKA AG, and ABB Ltd. are among the major players in the robotic wing assembly systems market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us