Runway Sensor Suite Market Size, Share & Industry Analysis, By Type (Runway Surface Condition & Friction, Meteorological, Visibility, FOD Detection, and Others), By Design (Embedded Sensors, Non-Invasive Sensors, and Mobile/Vehicle Mounted Sensors), By Technology (Optical, Infrared / Thermal, and Radar), By Airport Type (International Airports, Regional Airports, Military Air Bases, General Aviation/Private Airports), By Installation (New-Build, and Retrofit/Upgrade), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

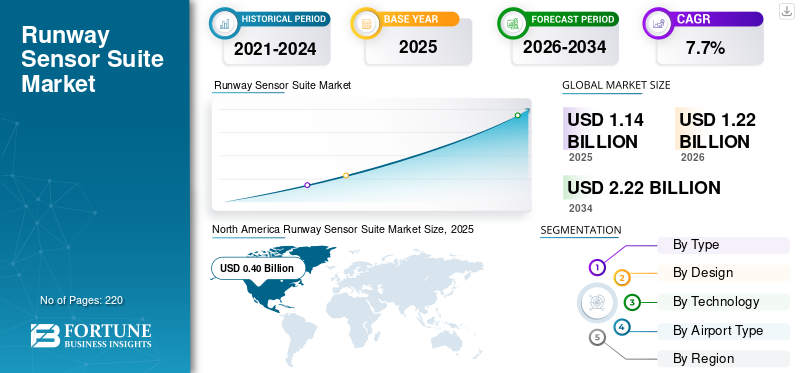

The global runway sensor suite market size was valued at USD 1.14 billion in 2025. The market is projected to grow from USD 1.22 billion in 2026 to USD 2.22 billion by 2034, exhibiting a CAGR of 7.7% during the forecast period. North America dominated the global market with a market share of 35.09% in 2025.

The global runway sensor suite market is expected to grow due to rise in airport infrastructure investments, stringent aviation safety regulations, and the adoption of smart airport technologies across the globe. The demand for runway sensors is increasing as there is requirement of standardized, real-time assessments of runway conditions such as ice, snow, and friction to prevent excursions. Moreover, airports globally are increasingly installing and upgrading advanced runway sensor and safety systems to enhance aviation safety.

- For instance, in December 2025, Vaisala received a contract to upgrade Runway Visual Range (RVR) systems at seven Greek airports Athens, Rhodes, Kos, Alexandroupolis, Kavala, Kozani, and Ioannina over two years to modernize the Hellenic Civil Aviation Authority’s infrastructure.

Furthermore, key industry players in the market, such as Saab, Thales, Indra, Vaisala, and others, prioritize developing advanced sensor integrations such as AI-enhanced LiDAR/radar fusion, automated runway monitoring system for FOD detection and incursion prevention to enhance airport safety.

Download Free sample to learn more about this report.

Runway Sensor Suite Market KEY TAKEAWAYS

- 2025 Market Size: USD 1.14 billion

- 2026 Market Size: USD 1.22 billion

- 2034 Forecast Market Size: USD 2.22 billion

- CAGR: 7.7% from 2026–2034

- North America dominated the runway sensor suite market with a 35.09% share in 2025.

- The non-invasive sensors segment is anticipated to account for the largest market share.

- The runway surface condition and friction segment is anticipated to account for the largest market share.

North America

North America led the market in 2025 with a valuation of USD 0.40 billion and is projected to reach USD 0.43 billion in 2026.

Asia Pacific

Asia Pacific was the second-largest regional market, valued at USD 0.31 billion in 2025.

Europe

Europe is projected to grow at a 7.3% CAGR during 2026–2034, making it the third-fastest growing regional market.

U.S.

U.S. The U.S. runway sensor suite market was valued at approximately USD 0.36 billion in 2025, supported by continued investments in airport safety infrastructure.

Japan

Japan The Japan runway sensor suite market was valued at approximately USD 0.04 billion in 2025, accounting for around 3.2% of global market revenue.

Read More

RUNWAY SENSOR SUITE MARKET TRENDS

Advancements in Sensor Fusion Technology is a Prominent Trend Observed in Market

Advancements in sensor fusion technology have emerged as a prominent trend in the global runway sensor suite industry. Manufacturers are integrating AI-driven multi-sensor arrays, combining millimeter-wave radar, infrared imaging, LiDAR, and electro-optical systems to deliver all-weather detection of Foreign Object Debris (FOD), precise surface condition monitoring, and real-time incursion prevention. In addition, there is an increase in development and testing hybrid sensor architectures to enhance accuracy.

- For instance, in December 2025, the Indian Institute of Tropical Meteorology (IITM) launched WiFEX-II, expanding its Winter Fog Experiment to deliver runway-specific fog forecasts. The program installs advanced sensors such as ceilometers for real-time data on fog onset.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Increase in Airport Expansions and Air Traffic is Expected to Drive Market Growth

A key driver for the runway sensor suite industry is the steady rise in global airport infrastructure expansions and air traffic volumes.

- For instance, according to International Air Transport Association (IATA), the total full-year traffic in 2024, rose 10.4% compared to 2023. Moreover, as per International Civil Aviation Organization (ICAO), global air passenger traffic is forecast to exceed 12 billion by 2030.

As the air traffic rises, there is an increase in the development of advanced runway safety systems which further supports demand for runway sensor suites. Major aviation authorities and airport operators are increasing investments in surface surveillance systems to enhance runway safety and prevent incursions, directly boosting procurement of advanced sensor technologies.

MARKET RESTRAINTS

High Development and Maintenance Costs to Limit Market Expansion

The design, certification, and deployment of advanced runway sensor suites involve high capital and technical complexity. OEMs must invest heavily in R&D for integrating radar, ADS-B, multilateration, and cloud-based analytics to meet stringent FAA and ICAO safety standards. Operators face elevated maintenance costs from specialized sensors, data fusion systems, and continuous software updates for all-weather reliability. All these factors are expected to hamper the runway sensor suite market growth.

MARKET OPPORTUNITIES

Evolving Standards and Runway Safety Lighting Advancements Presents Growth Opportunities for Market Growth

The aviation standards are accelerating the demand for next-generation runway sensor suites by mandating enhanced surface surveillance to prevent incursions during increased booming air traffic. Regulatory frameworks require seamless integration of radar, ADS-B, and multilateration technologies for real-time aircraft tracking. Thus it is expected to drive the investments in cloud-based, all-weather systems. Moreover, regulatory authorities are moving toward structured, fundable, and advanced deployment, which directly accelerates adoption of runway sensor suites.

- For instance, in May 2025, U.S. Federal Aviation Administration FAA issued Part 139 CertAlert 25-01, promoting the deployment of Vehicle Movement Area Transmitters (ADS-B) and Runway Incursion Warning Systems (RIWS).

In addition, stringent standards standardized procedures are being implemented by aviation regulatory bodies for checking and reporting runway surface conditions which increases the demand for advanced runway sensor suites, creating lucrative opportunities for the players in the market.

- For instance, in 2024, Civil Aviation Safety Authority (CASA) released Multi-Part AC 91-32 and AC 139-22, formalizing implementation of the ICAO Global Reporting Format (GRF) for runway surface condition assessment, reinforcing demand for runway condition sensing, friction monitoring, and data reporting solutions at aerodromes.

MARKET CHALLENGES

Supply Chain and Raw Material Volatility Acts as a Challenge for Market

Persistent supply chain disruptions and raw material shortages remain critical challenges for runway sensor suite manufacturers. The availability of rare earth elements for magnetometers and gyroscopes, high-purity semiconductors for SWIR imagers and photonic sensors, and advanced composites for weather-resistant enclosures has been disrupted by geopolitical tensions, export controls on critical minerals from various countries which is expected to present challenges for the market growth.

Segmentation Analysis

By Type

Stringent Standards and Mandatory Runway Inspections to Propel Runway Surface Condition & Friction Segmental Growth

Based on the type, the market is divided into runway surface condition & friction, meteorological, visibility, FOD detection, and others.

The runway surface condition and friction segment is anticipated to account for the largest market share in the runway sensor suite market. This dominant position stems from stringent International Civil Aviation Organization, Global Reporting Format mandates and regulatory frameworks by authorities such as Civil Aviation Safety Authority, Federal Aviation Administration, and European Union Aviation Safety Agency for precise Runway Condition Code reporting. Moreover, strict safety regulations from aviation authorities for mandatory runway inspections drive the requirement of advanced sensors such as FOD detection radars, infrared systems which drives the segment growth.

- For instance, in November 2025, Directorate General of Civil Aviation (DGCA) of India ordered all airports to perform mandatory runway inspections due to contamination concerns, potentially leading to operational restrictions or temporary suspensions.

The FOD detection segment is anticipated to rise with a CAGR of 10.2% over the forecast period.

By Design

Adoption of Automated Runway Monitoring System to Propel Non-Invasive Sensors Segmental Growth

By design, the market is segmented into embedded sensors, non-invasive sensors, and mobile/vehicle mounted sensors.

The non-invasive sensors segment is anticipated to account for the largest market share. The dominant position is due to minimal runway disruption during high-traffic operations, expansion of airports and runway programs. Moreover the segment growth is driven by adoption of real-time, automated runway monitoring systems as per ICAO GRF standards to avoid manual inspections and closures.

- For instance, in January 2025, Boschung published the Paris-Orly ATLAS case which highlighted that the Aéroport de Paris SA selected Boschung's ATLAS system to modernize runway condition surveillance at Paris-Orly Airport. The Boschung ATLAS upgrade at Paris-Orly Airport happened in phases: first runway (06-24) in 2021, second (07-25) in 2022, and third (02-20) for 2024.

The embedded sensors segment is projected to grow at a CAGR of 8.5% over the forecast period.

By Technology

Advancements in High-Resolution Imaging and AI Integration to Propel Optical Segment Growth

Based on technology, the market is segmented into optical, infrared / thermal, and radar.

Optical account for the largest market share of the industry due to its advantages such as high precision in detecting runway conditions such as Foreign Object Debris (FOD), water, or ice under varying weather. Advancements in high-resolution imaging and AI integration in sensor systems enable real-time monitoring with minimal false positives, enhancing aviation safety, which propels segment growth.

- For instance, in October 2025, Dallmeier electronic and Navtech Radar announced a strategic partnership at inter airport Europe 2025 in Munich, Germany, showcasing integrated video-radar solutions for enhanced airport security and operational efficiency. The Panomera S8 Runway sensor provides seamless multifocal optical coverage of entire runways, complementing radar for AI-driven incursion detection.

The radar segment is expected to grow with a steady growth rate of CAGR of 8.5% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Airport Type

Rapid Modernization of Airport Hubs and Investment in Smart Airport Technology Support Segment Growth

Based on airport type, the market is segmented into international airports, regional airports, military air bases, and general aviation/private airports.

The international airports segment is projected to capture the largest market share. Increase in regulatory mandates from ICAO and FAA for advanced FOD detection and surface surveillance systems propel adoption. Moreover, the rapid modernization in Asia Pacific and Middle East hubs and huge investments in smart airport tech such as sensor fusion drives segment growth.

The general aviation/private airports segment is projected to emerge as the fastest-growing at a CAGR of 9.5% over the forecast period.

By Installation

Cost Effectiveness and Less Upgrade Cost Fuel Retrofit/Upgrade Segment Growth

Based on installation, the market is segmented into new-build and retrofit/upgrade.

The retrofit/upgrade segment is expected to hold the largest runway sensor suite market share in 2025. Retrofit installations of runway sensor suites grow due to their cost-effectiveness, reduced upgrade expenses compared to full runway replacements while integrating radar, LiDAR, and optical sensors onto existing infrastructure.

The new-build segment is projected to grow with a steady growth rate at a CAGR of 7.0% over the forecast period.

Runway Sensor Suite Market Regional Outlook

By geography, the market is segmented into North America, Europe, Asia Pacific, Latin America and Middle East & Africa.

North America

North America Runway Sensor Suite Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

North America dominated the runway sensor suite market in 2025 with a valuation of USD 0.40 billion, growing to USD 0.43 billion in 2026, driven by stringent FAA safety mandates and extensive upgrades at major hubs such as various airports for FOD detection and surface condition monitoring. The U.S. leads due to high air traffic volumes, retrofit programs integrating radar-LIDAR fusion, and investments in AI-enhanced runway incursion prevention. The U.S. runway sensor suite market expands due to FAA's NextGen program mandating advanced sensors for runway safety, including real-time FOD detection and incursion prevention. Moreover, increase in investment in airport upgrades fuels deployments of runway weather information system and RVR (Runway Visual Range) systems.

U.S Runway Sensor Suite Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 0.36 billion in 2025. The country maintains its leading position due to increase in funding for military airfield sensors, and expansion of commercial airport runways in different cities and counties of the country, which drives the demand for cost effective and advanced runway sensor suites.

- For instance, in December 2025, Onslow County approved funding for Albert J. Ellis Airport's 900-foot runway extension, backed by a USD 29 million state grant. Moreover, Blue Ridge Regional Airport in Henry County, VA, completed its runway expansion boosting operational capacity for larger aircraft and enhancing regional connectivity.

Asia Pacific

Asia Pacific is estimated to reach USD 0.31 billion in 2025 and secure the position of the second-largest region in the market. In the region, India and China are both estimated to reach USD 0.07 billion and USD 0.12 billion, respectively in 2025.

Japan Runway Sensor Suite Market

The Japan runway sensor suite market in 2025 is estimated at around USD 0.04 billion, accounting for roughly 3.2% of global runway sensor suite revenues.

China Runway Sensor Suite Market

China’s runway sensor suite market is projected to be one of the largest worldwide, with 2025 revenues estimated at around USD 0.12 billion, representing roughly 10.8% of global runway sensor suite sales.

India Runway Sensor Suite Market

The India runway sensor suite market in 2025 is estimated at around USD 0.07 billion, accounting for roughly 6.1% of global runway sensor suite revenues.

Europe

Europe is projected to record a growth rate of 7.3% during 2026 to 2034, which is the third highest among all region. The growth in the region is supported by stringent EASA regulations on real-time hazard detection and retrofits for runways due to increasing low-cost carrier traffic. EU green aviation goals accelerate sensor adoption for predictive maintenance and emissions-compliant operations.

U.K Runway Sensor Suite Market

The U.K. runway sensor suite market in 2025 is estimated at around USD 0.05 billion, representing roughly 4.7% of global runway sensor suite revenues.

France Runway Sensor Suite Market

France runway sensor suite market is projected to reach approximately USD 0.04 billion in 2025, equivalent to around 3.4% of global runway sensor suite sales.

Latin America and Middle East & Africa

The Latin America and Middle East and Africa regions are expected to witness moderate growth in this market space during the forecast period. The Latin America market is set to reach a valuation of USD 0.08 billion in 2025, driven by surging commercial aviation in Brazil and Mexico, where airports undergo modernization to handle annual passenger growth. The Middle East drives growth through mega-airport projects under Saudi Vision 2030 and UAE expansions at Dubai and Riyadh, integrating advanced multi-sensor suites for extreme weather resilience and 24/7 operations. High air traffic from tourism and cargo hubs necessitates AI-enhanced incursion prevention

Saudi Arabia Runway Sensor Suite Market

The Saudi Arabia runway sensor suite market is projected to reach around USD 0.04 billion in 2025, representing roughly 3.4% of global runway sensor suite revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Advanced Sensor Fusion and Retrofit Solutions by Key Players to Propel Market Progress

The global runway sensor suite market remains consolidated, led by major players such as Saab, Vaisala, Thales, Indra, which hold significant shares through innovations in radar-LIDAR integration and AI-driven FOD detection systems. These firms advance market growth with the help of strategic partnerships with airport authorities and OEM collaborations to deploy runway weather monitoring systems and FOD detection sensor systems.

For instance, in December 2023, Vaisala secured approximately USD 23.44 million contract with Kuwait's DGCA to deploy its AviMet AWOS across three runways at Kuwait International Airport, enhancing real-time weather monitoring for safer operations. The system, upgrading prior Vaisala installations will deliver ICAO/WMO-compliant data on conditions such as runway status, lightning, and windshear to aid pilots and controllers.

Other prominent players include Luft, Leonardo, Xsights Systems, and others, prioritizing R&D in predictive analytics, joint ventures for regional airport modernizations, and scalable production to capture rising demand from high-traffic expansions.

LIST OF KEY RUNWAY SENSOR SUITE COMPANIES PROFILED

- Saab (Sweden)

- Thales (France)

- Indra (Spain)

- Leonardo (Italy)

- ADB SAFEGATE (Belgium)

- Frequentis (Austria)

- Terma (Denmark)

- Vaisala (Finland)

- Lufft (Germany)

- Xsights Systems (U.S.)

KEY INDUSTRY DEVELOPMENTS

- December 2025: Vaisala will modernize Runway Visual Range (RVR) systems at seven Greek airports Athens, Rhodes, Kos, Alexandroupolis, Kavala, Kozani, and Ioannina. It aims to supply LT31 transmissometers and AviMet RVR software over a two-year project for the Hellenic Civil Aviation Authority.

- June 2025: Saab announced the FAA selected its Aerobahn Runway and Surface Safety service for 26 additional U.S. airports under SAI Block 3.

- March 2025: Babasaheb Ambedkar International Airport in Nagpur installed two state-of-the-art Runway Visual Range (RVR) systems at runway ends, with a third at the midpoint nearing commissioning. These automated, high-accuracy sensors replace manual visibility checks, relaying real-time data to air traffic controllers ATC and pilots for safer low-visibility operations matching global standards.

- March 2025: GMR Hyderabad International Airport commissioned a Category II Instrument Landing System (ILS) on its primary runway, enabling safe landings in visibility as low as 300m RVR during fog, with upgraded runway lighting for precision guidance.

- February 2025: Netaji Subhash Chandra Bose International Airport in Kolkata was equipped with India's state-of-the-art Automated Weather Observing System (AWOS), featuring sensors at six met parks along the runway to measure temperature, wind speed/shear, humidity, runway visibility range, and cloud height.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.7% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type, By Design, By Technology, By Airport Type, By Installation, and Region |

|

By Type |

· Runway Surface Condition & Friction · Meteorological · Visibility · FOD Detection · Others |

|

By Design |

· Embedded Sensors · Non-Invasive Sensors · Mobile/Vehicle Mounted Sensors |

|

By Technology |

· Optical · Infrared / Thermal · Radar |

|

By Airport Type |

· International Airports · Regional Airports · Military Air Bases · General Aviation/Private Airports |

|

By Installation |

· New-Build · Retrofit/Upgrade |

|

By Region |

· North America ( By Type, By Design, By Technology, By Airport Type, By Installation, and Country) o U.S. (By Airport Type) o Canada (By Airport Type) · Europe ( By Type, By Design, By Technology, By Airport Type, By Installation, and Country) o U.K. (By Airport Type) o Germany (By Airport Type) o France (By Airport Type) o Russia (By Airport Type) o Rest of Europe (By Airport Type) · Asia Pacific ( By Type, By Design, By Technology, By Airport Type, By Installation, and Country) o China (By Airport Type) o Japan (By Airport Type) o India (By Airport Type) o South Korea (By Airport Type) o Rest of Asia Pacific (By Airport Type) · Latin America ( By Type, By Design, By Technology, By Airport Type, By Installation, and Country) o Brazil (By Airport Type) o Mexico (By Airport Type) o Rest of Latin America( By Aircraft Type) · Middle East & Africa ( By Type, By Design, By Technology, By Airport Type, By Installation, and Country) o UAE (By Airport Type) o Saudi Arabia (By Airport Type) o Rest of Middle East & Africa (By Airport Type) |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 1.14 billion in 2025 and is projected to reach USD 2.22 billion by 2034.

In 2025, the market value stood at USD 0.40 billion.

The market is expected to exhibit a CAGR of 7.7% during the forecast period of 2025-2034.

By type, the runway surface condition & friction segment is expected to lead the market.

The increase in airport expansions and air traffic are driving market expansion.

Saab, Vaisala, Thales, Indra, and among others are some of the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 220

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us