Thermosetting Plastics Market Size, Share & Industry Analysis, By Type (Polyurethane, Unsaturated Polyester Resins, Urea Formaldehyde Resins, Epoxy, Phenolic, and Others), By Application (Building & Construction, Adhesives & Sealants, Automotive & Transportation, Electrical & Electronics, Consumer Goods, and Others), and Regional Forecast, 2026-2034

THERMOSETTING PLASTICS MARKET SIZE AND FUTURE OUTLOOK

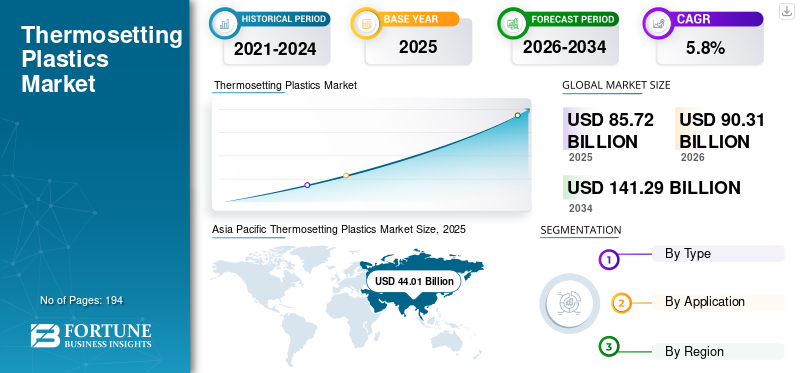

The global thermosetting plastics market size was valued at USD 85.72 billion in 2025 and is projected to grow from USD 90.31 billion in 2026 to USD 141.29 billion by 2034 at a CAGR of 5.8% during the forecast period. Asia Pacific dominated the thermosetting plastics market with a market share of 51.34% in 2025.

Thermosetting plastics are polymers that permanently cure into a cross-linked structure when exposed to heat, catalysts, radiation, or pressure. Once cured, they do not remelt, which gives them strong dimensional stability, heat resistance, chemical resistance, adhesion, and electrical insulation performance. This makes them highly suitable for demanding uses across building & construction, adhesives & sealants, automotive & transportation, electrical & electronics, consumer goods, and industrial composites. Major thermosetting resin families include polyurethane, unsaturated polyester, urea formaldehyde, epoxy, phenolic, melamine, and other specialty thermosets.

The growth of the thermosetting plastics market is driven by rising demand for engineered wood products, insulation materials, coatings, electrical components, lightweight transportation parts, and high-performance composites. The market also benefits from thermosets' ability to deliver long-term durability and structural performance in applications where conventional thermoplastics are often less suitable. Key players in the market include Covestro, Huntsman, Westlake, Hexion, BASF, and Hexcel, as well as regional formulators and specialty resin suppliers serving construction, electronics, transportation, coatings, and composite applications.

Download Free sample to learn more about this report.

THERMOSETTING PLASTICS MARKET TRENDS

Shift Toward Higher-Performance and More Sustainable Thermoset Systems Curates New Market Trend

A clear market trend is the move from conventional formulations toward higher-performance, more sustainability-oriented systems. Suppliers are increasingly emphasizing faster cure, improved processability, better toughness, and application-specific performance rather than competing only on bulk resin volume. ExxonMobil’s Proxxima platform, for example, is positioned as a thermoset system aimed at improving the strength-toughness balance and producing lighter-weight materials.

At the same time, sustainability pressures are driving innovation in end-of-life management and chemical design. Swancor’s recyclable thermosetting epoxy for wind applications illustrates how suppliers are trying to solve one of the category’s biggest long-term weaknesses. This does not remove the recycling challenge overnight, but it signals where R&D and product differentiation are moving.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Strong Demand from Building Materials and Engineered Wood Products Boosts Market Growth

A major driver of demand for thermosetting plastics is their deep integration into engineered wood and construction applications. Product manufacturers state that urea, phenolic, and melamine resins are widely used in plywood, particleboard, and fiberboard. At the same time, BASF notes that melamine- and urea-based impregnating resins are designed for overlay, décor paper, laminate flooring, and related surfaces. This makes thermosets structurally tied to panel products, laminates, decorative surfaces, and insulation systems used throughout residential and non-residential construction. Since thermosetting resins are core binders in many applications, rising panel output directly supports resin consumption, especially for urea-formaldehyde, melamine-formaldehyde, and phenolic systems. This leads to a positive thermosetting plastics market growth.

MARKET RESTRAINTS

Stringent Environmental and Chemical Regulations Increase Compliance Burden

Stringent environmental and chemical regulations are emerging as a major restraint on the market, as they increase costs and complexity across manufacturing, formulation, and downstream compliance. In Europe, REACH is the EU’s main chemicals regulation and requires companies to manage obligations for the registration, evaluation, authorization, and restriction of substances to protect human health and the environment. For thermosetting plastics producers, this can affect resin systems, additives, curing agents, and intermediates, while also increasing documentation, testing, and traceability requirements, as well as reformulation requirements. These obligations can lengthen product approval timelines and raise operating costs, especially for suppliers serving multiple end-use sectors with region-specific compliance needs.

MARKET OPPORTUNITIES

Growth in Renewable Energy, Electrical Systems, and Advanced Composites Curates Growth Opportunities

Thermosetting plastics have significant opportunities in energy transition and lightweighting applications. Westlake Epoxy states that its epoxy technology supports wind turbine blade production and resin infusion processes, directly tying thermosets to wind-capacity expansion and larger blade formats. In parallel, thermoset composites remain attractive for electrical insulation, heavy-duty industrial parts, and high-performance composite systems that require long-term strength and thermal resistance.

The opportunity also extends to transportation and aerospace-adjacent lightweighting. Manufacturers such as Hexcel and Toray position thermoset-based composite materials as lighter, stronger alternatives for aerospace and advanced industrial applications. As OEMs continue to pursue weight reduction, durability, and thermal performance, epoxy and other specialty thermosets should retain a premium role in higher-value applications even if bulk resin markets remain cyclical.

MARKET CHALLENGES

Environmental Scrutiny Around Formaldehyde-Based Systems Leads to Market Challenges

A major challenge for the market is that several large-volume thermoset families are formaldehyde-based, particularly urea-, phenolic-, and melamine-based systems. These resins remain essential in wood panels, coatings, and industrial binders, but they also face ongoing scrutiny related to emissions, handling, and regulatory expectations. BASF’s and Hexion’s product positioning underscores the continuing importance of these chemistries and highlights the need for low-emission, performance-optimized grades.

The market also faces a broader waste-management challenge because cured thermosets do not fit easily into conventional recycling systems. As circularity targets become more important for plastics overall, thermosets risk being disadvantaged in procurement and policy discussions unless recycling, reuse, or alternative recovery pathways improve. That makes innovation in recyclable formulations and more efficient recovery routes strategically important for long-term competitiveness.

TRADE PROTECTIONISM AND GEOPOLITICAL IMPACT

Trade protectionism and geopolitical tensions are restraining the global market by making feedstock sourcing, cross-border resin trade, and downstream manufacturing more volatile and expensive. Thermosetting plastics rely on globally interconnected chemical value chains for petrochemical inputs, intermediates, additives, curing agents, and formulated systems. When tariffs rise, sanctions risks increase, or export controls tighten, producers can face higher landed raw-material costs, longer lead times, disrupted contract execution, and reduced sourcing flexibility. OECD notes that global supply chains are under mounting pressure from geopolitical tensions, regulatory uncertainty, and economic volatility. At the same time, export restrictions on industrial raw materials have risen sharply over the past decade. For thermosetting plastics manufacturers, this means more frequent input-price fluctuations and greater pressure to regionalize procurement or build buffer inventories, which can weaken margins and reduce operational efficiency.

RESEARCH AND DEVELOPMENT (R&D) TRENDS

Research and development in the global market is increasingly focused on making these materials more sustainable without losing their core performance advantages. A major area of innovation is recyclable thermoset chemistry, especially in epoxy systems used in wind-energy composites. Swancor announced the commercial-scale use of its recyclable epoxy resin at the Sofia Offshore Wind Farm, where 50 turbine blades use the technology, and also signed an MoU with Adani to support the development of recyclable wind-blade technology in India. These developments show that R&D is moving beyond laboratory work toward industrial deployment in applications that historically faced severe end-of-life challenges.

SEGMENTATION ANALYSIS

By Type

Polyurethane Segment Dominates Due to Strong Mechanical Properties and Durability Across High-Volume End Uses

Based on type, the market is segmented into polyurethane, unsaturated polyester resins, urea formaldehyde resins, epoxy, phenolic, and others.

Among these, the polyurethane segment has the dominant thermosetting plastics market share. This dominance is driven by its broad use across insulation, coatings, adhesives, sealants, automotive components, construction materials, and industrial applications. Its strong mechanical properties, design flexibility, thermal insulation performance, and durability make it suitable for a wide range of high-volume end uses. In addition, polyurethane systems offer formulation versatility in both rigid and flexible forms, which supports their adoption across multiple industries. This wide application base and performance advantage continue to strengthen polyurethane’s leading position in the global market.

Unsaturated polyester resins hold a significant market share due to their widespread use in composite applications, including construction panels, pipes, tanks, transportation parts, and marine components. The segment is expected to register 6.0% CAGR during the forecast period. These resins are valued for their good mechanical strength, corrosion resistance, easy processing, and cost-effectiveness, making them suitable for large-volume molded and reinforced plastic products.

Urea-formaldehyde resins are in strong demand due to their extensive use in wood adhesives, particleboard, plywood, medium-density fiberboard, and decorative laminates. Their popularity stems from their low cost, strong bonding performance, fast curing, and suitability for mass-scale panel production, especially in the building and furniture industries.

The others segment includes materials such as melamine formaldehyde resins, vinyl ester resins, alkyd thermosets, and other specialty thermosetting systems. Melamine formaldehyde resins are primarily used in laminates, tableware, coatings, and decorative surfaces due to their hardness and scratch resistance.

By Application

To know how our report can help streamline your business, Speak to Analyst

Building & Construction Leads Due to the Extensive Usage of Thermosetting Plastics in Several Materials

Based on application, the market is segmented into building & construction, adhesives & sealants, automotive & transportation, electrical & electronics, consumer goods, and others.

The building & construction segment is expected to hold the major market share during the forecast period. The growth is due to the extensive use of thermosetting plastics in insulation materials, laminates, panels, pipes, coatings, flooring, roofing components, and wood-based boards. These materials are preferred in construction applications because they offer strong bonding performance, thermal stability, moisture resistance, durability, and structural reliability. Rising infrastructure development, residential construction, and demand for high-performance building materials continue to support the segment’s leading position.

The adhesives & sealants segment is expected to register significant growth during the forecast period. The segment register 5.9% growth rate during the study period. The growth is due to thermosetting plastics offering strong adhesion, chemical resistance, and long-term bonding performance. They are widely used in structural bonding, assembly processes, industrial sealing, and construction-related applications where durability and resistance to harsh environments are essential.

The automotive & transportation segment is experiencing strong market growth supported by the use of thermosetting plastics in lightweight components, under-the-hood parts, coatings, brake materials, interiors, and composite structures. Their heat resistance, dimensional stability, and mechanical strength make them suitable for demanding vehicle applications, while the push for lightweighting also supports their use.

The others segment includes applications such as industrial equipment, aerospace, marine, wind energy, and general composites. These areas use thermosetting plastics for corrosion-resistant parts, high-strength structures, blades, tanks, pipes, and performance components where durability, chemical resistance, and thermal performance are important.

THERMOSETTING PLASTICS MARKET REGIONAL OUTLOOK

By region, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Thermosetting Plastics Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates the global market due to its large manufacturing base, strong construction activity, broad electronics production, and extensive automotive and industrial output. The region benefits from the scale of China, Japan, India, and other Asian manufacturing hubs, which support high demand for polyurethane, epoxy, phenolic, and formaldehyde-based thermosetting resins across building materials, electrical systems, transportation parts, laminates, and industrial applications.

China Thermosetting Plastics Market

China’s market is one of the largest country, with 2025 revenue at USD 23.62 billion, representing roughly 27.6% of global sales.

To know how our report can help streamline your business, Speak to Analyst

North America

North America holds a significant market share due to strong demand across construction, insulation, adhesives, transportation, electrical components, and industrial applications, with the U.S. serving as the main regional growth engine.

U.S. Thermosetting Plastics Market

In 2025, the U.S. represented a USD 13.79 billion market in North America, driven primarily by strong demand from the industrial sector. The U.S. accounts for roughly 16.1% of global market sales.

Europe

Europe registers positive growth during the forecast period. The growth is due to its established automotive, electrical, coatings, industrial, and engineered materials base, although its relative share has weakened compared with faster-growing Asian markets.

Germany Thermosetting Plastics Market

The Germany market in 2025 valued at around USD 3.53 billion, representing roughly 4.1% of global market revenues.

U.K. Thermosetting Plastics Market

The U.K. market in 2025 was valued at around USD 1.22 billion, representing roughly 1.4% of global market revenues.

Latin America

Latin America is supported by growing demand from packaging-related conversion, construction materials, automotive production, and industrial manufacturing, especially in Brazil and Mexico.

Brazil Thermosetting Plastics Market

Brazil market in 2025 was valued at around USD 1.60 billion, representing roughly 1.9% of global market revenues.

Middle East & Africa

The Middle East & Africa benefit from expanding petrochemical integration, infrastructure activity, and industrial development, particularly across GCC countries and selected African economies.

GCC Thermosetting Plastics Market

GCC market in 2025 valued at around USD 3.65 billion, representing roughly 4.3% of global market revenues.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key Players Are Adopting an Expansion Strategy to Maintain Their Dominance in the Market

The market is moderately consolidated around global chemical producers and specialized resin suppliers with strong positions in particular thermoset families. Key participants include Covestro, Huntsman, Westlake, Hexion, BASF, and Hexcel, depending on the resin family and end-use segment involved. These companies compete through product performance, formulation expertise, processing support, and application-specific solutions rather than on commodity scale alone.

The competition is also increasingly shaped by the ability to offer lower-emission chemistries, better cure performance, and improved sustainability credentials. In higher-value areas such as wind energy, aerospace composites, and premium coatings, technical support and system-level performance are often more decisive than resin price alone.

LIST OF KEY THERMOSETTING PLASTICS COMPANIES PROFILED IN REPORT

- BASF SE (Germany)

- Covestro AG (Germany)

- Hexion Inc. (U.S.)

- Huntsman Corporation (U.S.)

- Westlake Corporation (U.S.)

- DIC Corporation (Japan)

- Allnex (Germany)

- Sumitomo Bakelite Co. Ltd. (Japan)

- Hexcel Corporation (U.S.)

- Swancor Holding Co., Ltd. (Taiwan)

KEY INDUSTRY DEVELOPMENTS

- July 2025: Covestro launched an advanced flame-retardant polyurethane encapsulation foam for EV batteries and also reported that photovoltaic module shipments using its PU composite frame technology surpassed 3 GW, reinforcing its position in energy-transition applications.

- May 2025: Hexion and Smartech introduced SmartQuality, an AI-powered operating platform for wood panel manufacturing, extending Hexion’s role beyond resin supply into process optimization for thermoset-intensive panel applications.

- March 2025: Westlake Epoxy announced the EpoVIVE portfolio, a new sustainable epoxy range spanning epoxy phenolic resins and curing agents, and used JEC World / ECS 2025 to launch additional composite and coatings-focused products.

- February 2025: BASF introduced Basotect EcoBalanced, with transparent product carbon footprint data for its melamine-resin foam, strengthening its position in lower-carbon thermoset solutions for transportation and construction applications.

- February 2025: allnex used JEC World 2025 to showcase new VIAPAL vinyl ester grades and gelcoat/composites technologies, underscoring its focus on specialty thermosets for transport and industrial composites.

REPORT COVERAGE

The thermosetting plastics market report provides a detailed analysis of the market. It focuses on key aspects, such as leading companies, type, and application. Besides this, it offers insights into the market and current industry trends and highlights key industry developments. In addition to the factors mentioned above, the report also covers several factors contributing to market growth.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Unit | Value (USD Billion), Volume (Kiloton) |

| Growth Rate | CAGR of 5.8% from 2026 to 2034 |

| Segmentation | By Type, By Application, By Region |

| By Type |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 85.72 billion in 2025 and is projected to reach USD 141.29 billion by 2034.

Recording a CAGR of 5.8%, the market is slated to exhibit steady growth during the forecast period.

The building & construction application segment is expected to lead the market.

Asia Pacific held the largest market share in 2025.

Strong product demand from building materials and engineered wood products drives the market.

- 2021-2034

- 2025

- 2021-2024

- 194

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us