Waste Derived Biogas Market Size, Share & Industry Analysis, By Feedstock (Agricultural Residues, Industrial Organic Waste, Municipal Solid Waste, Animal Manure, Sewage Sludge, and Others), By Technology (Biogas Upgrading Systems, Anaerobic Digestion, Landfill Gas Recovery, and Others), By End User (Biomethane, CHP, Power Generation, and Others), and Regional Forecast, 2026-2034

Waste Derived Biogas Market Size and Future Outlook

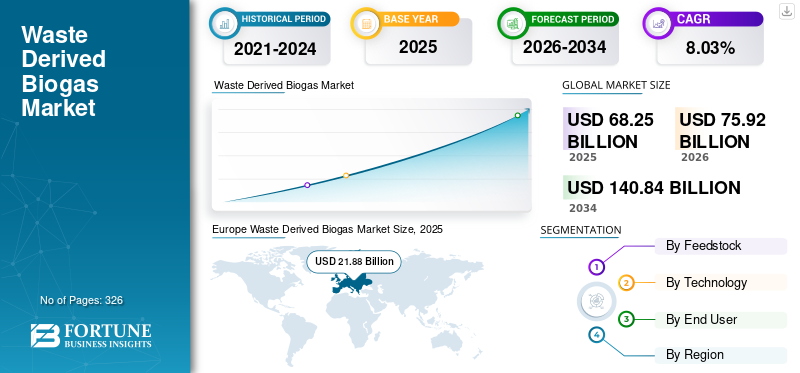

The global waste-derived biogas market size was valued at USD 68.25 billion in 2025. The market is projected to grow from USD 75.92 billion in 2026 to USD 140.84 billion by 2034, with a CAGR of 8.03% over the forecast period. Europe dominated the waste-derived biogas market with a market share of 32.05% in 2025.

Waste-derived biogas is a technique of producing biogas through the anaerobic digestion or decomposition of organic waste materials such as food waste, agricultural residues, animal manure, sewage sludge, and landfill waste. In oxygen-free conditions, microorganisms break down the organic matter and generate a methane-rich gas mixture primarily composed of Methane (CH₄) and Carbon Dioxide (CO₂). The biogas can be used directly for heat and electricity generation or upgraded to biomethane for injection into natural gas grids and use as vehicle fuel. Waste-derived biogas helps reduce landfill emissions, diverts organic waste from disposal, and lowers greenhouse gas emissions compared to fossil fuels.

The growth of the market is primarily driven by stringent emission reduction targets and renewable fuel mandates across major economies such as the U.S., Germany, and others. Rising concerns over landfill overflow and plastic waste management are encouraging governments and industries to convert waste streams into valuable fuels. Increasing demand for low-carbon transportation fuels, particularly in heavy-duty and aviation sectors, further supports adoption. Additionally, advancements in pyrolysis and hydrotreatment technologies are improving conversion efficiency and commercial viability.

Veolia Environnement, Engie, EnviTec Biogas, Ameresco, and Air Liquide are among the leading companies in this market. These companies are innovating and scaling technologies (e.g., hydroprocessing, pyrolysis, gasification) to convert waste feedstocks such as used cooking oils, plastics, and organic residues into renewable diesel. They invest in expanding production capacity, optimizing conversion efficiency, partnering with waste suppliers, and reducing greenhouse gas emissions by replacing fossil diesel with low-carbon, drop-in fuels.

Download Free sample to learn more about this report.

Waste Derived Biogas Market Trends

Integration of Waste-to-Fuel in Refinery Infrastructure Are Amplifying Market Growth

A key trend in the market is the integration of waste-based feedstocks into existing petroleum refining infrastructure. Major energy companies such as Neste and Shell are retrofitting conventional refineries to co-process used cooking oil, animal fats, and other residues alongside fossil feedstocks. This approach reduces capital expenditure compared to building standalone plants while accelerating commercialization. For instance, several European refineries have shifted portions of their hydroprocessing units toward renewable diesel production to meet the European Union’s Renewable Energy Directive targets, which mandate at least 14% renewable energy in transport. Co-processing also enables drop-in fuel compatibility with existing diesel engines and logistics systems. The trend reflects a broader transition strategy where traditional oil majors leverage infrastructure, distribution networks, and hydrogen supply systems to scale waste-derived biogas faster, improving lifecycle carbon intensity while maintaining fuel reliability and supply stability.

MARKET DYNAMICS

Market Drivers

Download Free sample to learn more about this report.

Stringent Carbon Reduction and Renewable Fuel Policies to Push the Market Growth

Stringent decarbonization policies are primary growth drivers for waste-derived biogas. Governments are implementing low-carbon fuel standards and renewable blending mandates to curb transport emissions, which account for roughly 20–25% of global CO₂ emissions. In the U.S., the Renewable Fuel Standard (RFS) and California’s Low Carbon Fuel Standard provide tradable credits for fuels with lower carbon intensity, directly incentivizing waste-based diesel production. Similarly, the European Union requires member states to increase renewable energy use in transportation under its climate framework. Waste-derived biogas offers lifecycle greenhouse gas reductions of up to 60–85% compared to conventional diesel, depending on feedstock type, making it attractive for compliance. These regulatory mechanisms create predictable demand, improve project bankability, and encourage investment in advanced conversion technologies. As carbon pricing mechanisms expand globally, policy-backed demand is expected to remain a foundational driver of market expansion.

Market Restraints

High Capital Investment and Technology Risks to Limit the Market Growth

High capital requirements and technology uncertainties act as significant restraints on market growth. Advanced waste-to-diesel facilities, particularly those using pyrolysis or gasification followed by Fischer–Tropsch synthesis, require substantial upfront investment, often running into hundreds of millions of dollars per plant. Complex process integration, catalyst performance issues, and operational scaling risks can delay commercialization. For instance, several early-stage plastic-to-fuel ventures globally have struggled to achieve consistent commercial output due to technical and economic hurdles. Even established players such as Chevron have proceeded cautiously, prioritizing partnerships and phased capacity expansions to mitigate risk. Moreover, financing can be challenging without long-term policy certainty or offtake agreements. Fluctuations in crude oil prices also impact the competitiveness of waste-derived biogas relative to fossil diesel, potentially affecting return on investment and slowing new project development in uncertain market conditions.

Market Opportunities

Aviation and Heavy-Duty Transport Decarbonization to Create New Growth Avenues

A major opportunity for the market lies in decarbonizing hard-to-electrify sectors such as aviation, marine, and long-haul trucking. Sustainable Aviation Fuel (SAF), often produced from similar waste-based feedstocks via hydrotreatment or Fischer–Tropsch synthesis, is gaining policy and airline support. The International Air Transport Association projects that aviation must cut net emissions by 50% from 2005 levels by 2050, creating strong demand for sustainable energy biofuels. Companies such as BP and TotalEnergies are investing in integrated renewable fuel hubs that produce both renewable diesel and SAF from waste oils and residues. Heavy-duty trucking fleets are also adopting renewable diesel as it requires no engine modification and offers immediate emission reductions. As electrification remains challenging for long-distance freight due to battery weight and range constraints, waste-derived biogas provides a near-term, scalable solution, positioning the market for expansion in premium low-carbon fuel segments.

Market Challenges

Feedstock Availability and Price Volatility to Limit Market Growth

One of the main challenges facing the market is the limited and volatile supply of sustainable waste feedstocks such as Used Cooking Oil (UCO) and animal fats. Global UCO supply is finite and geographically concentrated, while demand has surged due to expanding renewable diesel capacity. For example, renewable diesel production capacity in North America has grown rapidly over the past five years, intensifying competition for feedstocks and pushing prices upward. Import reliance also raises traceability and fraud concerns in international supply chains. Companies such as Valero Energy have highlighted feedstock sourcing as a key operational risk in renewable diesel expansion. Additionally, seasonal variations and competing uses in biodiesel and oleochemical industries further constrain availability. This imbalance between capacity growth and sustainable feedstock supply can compress margins and delay project timelines, making supply chain security a critical strategic priority for producers.

Segmentation Analysis

By Feedstock

High Volume Presence of Municipal Solid Waste to Lead the Segment Growth

Based on feedstock, the market is segmented into agricultural residues, industrial organic waste, municipal solid waste, animal manure, sewage sludge, and others.

Municipal solid waste segment accounted for 29.81% of the waste derived biogas market share in 2025. The segment holds the largest market share due to its sheer volume. MSW accounts for nearly 47–48% of waste-to-diesel feedstock globally, driven by abundant urban waste generation, landfill diversion policies, and increasing adoption of thermochemical conversion technologies such as pyrolysis and gasification. Since cities produce vast amounts of MSW daily, its prevalence and availability make it the dominant feedstock category, often exceeding the combined contributions of other organic sources.

Animal manure segment is expected to grow at a CAGR of 8.62% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Technology

High Efficiency and Compatibility of Anaerobic Digestion to Lead the Segment Growth

Based on technology, the market is segmented into biogas upgrading systems, anaerobic digestion, landfill gas recovery, and others.

Anaerobic digestion segment accounts for approximately 42.10% of the market share. Anaerobic Digestion (AD) remains the dominant segment in the market due to its scalability, efficiency, and compatibility with a wide range of organic wastes such as manure, crop residues, and food waste. AD is central to modern waste-to-energy systems: nearly nine out of ten biogas facilities use it as the core conversion process. Its strong presence is supported by large-scale installations across Europe, North America, and Asia, driven by renewable incentives, rural energy programs, and circular waste management strategies. As AD feeds the raw biogas that upgrading systems purify and landfill gas recovery captures, its market share underpins the rest of the renewable gas value chain and broadly dominates total biogas capacity globally.

Biogas upgrading systems segment is expected to grow at a CAGR of 8.73% during the forecast period.

By End User

Heavy Reliance on the Diesel by the Biomethane Sector to Propel the Segment Growth

Based on end user, the market is segmented into Biomethane, CHP, power generation, and others.

Power generation segment represented the largest market share of around 36.87% in 2025. Multiple industry tracking sources indicate that electricity generation from biogas makes up roughly 54% or more of the end-use market, as plants convert methane into electricity either directly or through CHP systems. This dominance is driven by the consistent demand for renewable power, feed-in tariffs, renewable portfolio standards, and incentives that make biogas-to-electricity projects financially attractive, especially in Europe, North America, and China. The abundant supply of municipal and agricultural organic waste boosts this segment, reducing fossil fuel dependence and contributing to grid stability. As power generation absorbs a large share of biogas output, it remains the cornerstone of the renewable gas market.

Biomethane segment is the fastest growing expected to grow with a CAGR of 9.28% in 2025.

Waste Derived Biogas Market Regional Outlook

By geography, the market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Europe

Europe Waste Derived Biogas Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Europe accounted for USD 21.28 billion in 2025, representing approximately 31.18% of global revenues. The region dominated the market for renewable fuels, especially in biogas, biomethane, and renewable diesel applications. In the biogas/biomethane space, Europe often commands the largest regional share, around 40–42% of global activity, reflective of long-standing renewable gas directives, grid injection mandates, and strong decarbonization policies. Germany, France, Sweden, and the U.K. are among the leading producers, while public transport and municipal fleets increasingly use biomethane and renewable diesel blends. European countries also lead in recycling organic waste and deploying anaerobic digestion at scale, supporting high installed capacity relative to other regions. The region’s comprehensive regulatory alignment makes it a cornerstone of the waste derived biogas market growth worldwide.

Germany Waste Derived Biogas Market

Germany was estimated at USD 5.40 billion in 2025 and is set to reach USD 6.06 billion in 2026. The country is widely recognized for its advanced biogas and biomethane infrastructure, supported by long-standing renewable energy legislation. It operates thousands of biogas plants, primarily utilizing agricultural residues and energy crops. Germany’s energy transition strategy emphasizes renewable integration into power grids and gas networks, with strong technical expertise in anaerobic digestion and CHP systems. Industrial decarbonization goals and renewable transport policies continue to support renewable fuel consumption. Germany’s well-developed engineering base and established waste-to-energy ecosystem reinforce its leadership role in bioenergy deployment.

U.K. Waste Derived Biogas Market

The U.K. market was valued at USD 3.17 billion in 2025 and is expected to reach USD 3.55 billion in 2026. The country plays an active role in renewable fuels, particularly in biomethane grid injection and sustainable aviation fuel development. The U.K. expanded its anaerobic digestion facilities significantly over the past decade, supporting agricultural and food-waste-based gas production. Government transport decarbonization policies and renewable transport fuel obligations continue to stimulate demand. However, domestic production capacity has faced structural adjustments due to global competition and policy shifts. Despite this, the U.K. remains an important European contributor to renewable gas integration and low-carbon fuel transition initiatives.

North America

North America was valued at USD 17.15 billion in 2025, accounting for approximately 25.12% of the global market. The region holds a significant share of the market, driven by strong policy frameworks such as renewable fuel standards, clean fuel tax incentives, and major renewable diesel production capacity. North America’s waste-to-diesel and RNG sectors are supported by advanced landfill gas capture, agricultural biogas utilization, and state-level clean fuel mandates that boost adoption. For example, evolving U.S. policies under the Renewable Fuel Standard and the Inflation Reduction Act are accelerating investment in renewable fuel facilities and RNG projects, reinforcing North America’s leadership position in clean fuel deployment.

U.S. Waste Derived Biogas Market

The U.S. market was estimated at USD 14.88 billion in 2025 and is likely to reach USD 16.50 billion in 2026. The U.S. is one of the most influential markets in renewable fuels, driven by strong federal and state-level policy frameworks such as renewable fuel blending mandates and low-carbon fuel programs. The country has rapidly expanded renewable diesel refining capacity through refinery conversions and new project developments, while also leading in Renewable Natural Gas (RNG) production from landfill gas and agricultural waste. The U.S. Environmental Protection Agency reports thousands of operational biogas systems nationwide, reflecting a mature waste-to-energy ecosystem. Strong demand from heavy-duty transport, aviation fuel initiatives, and corporate decarbonization strategies continues to reinforce the country’s dominant global position.

Asia Pacific

Asia Pacific market was valued at USD 18.78 billion in 2025, accounting for approximately 27.52% of global revenues. Asia Pacific’s growth is underpinned by its large population, rising energy demand, and expanding industrial and transport sectors. Countries such as China, India, Japan, and South Korea are accelerating investments in waste-to-energy projects, agricultural biogas plants, and renewable diesel adoption to reduce import dependence and cut emissions. Agricultural residues and organic waste conversion are major feedstock drivers in rural regions, while urban centers push toward cleaner transport fuels. Although regulatory frameworks in the Asia Pacific vary by country, strong government initiatives and infrastructure development are closing the gap with Western markets, making this region one of the fastest-growing globally.

China Waste Derived Biogas Market

China remains the dominant contributor in the Asia Pacific, valued at USD 7.48 billion in 2025 and is likely to hit USD 8.43 billion in 2026. China is a major force in renewable fuels, driven by rural energy programs, waste management reforms, and energy security priorities. The country has implemented large-scale biogas initiatives, particularly in agricultural regions, to convert livestock manure and organic waste into energy. Urban waste-to-energy plants also contribute to renewable gas and power generation. National carbon neutrality targets have accelerated interest in biomethane and advanced biofuels. China’s vast feedstock availability and expanding clean energy infrastructure position it as a central growth engine in the global renewable fuels landscape.

India Waste Derived Biogas Market

India was estimated at USD 3.49 billion in 2025 and is set to reach USD 3.93 billion in 2026. India’s renewable fuel sector is expanding through government-backed initiatives promoting Compressed Biogas (CBG), ethanol blending, and rural biogas deployment. Programs encouraging the conversion of agricultural residues and municipal waste into energy aim to reduce pollution and improve energy access. India has scaled up waste-to-energy installations in urban areas while promoting decentralized digesters in rural communities. Strong policy alignment with climate and air-quality goals continues to attract investment into biomethane and sustainable transport fuels, positioning India as an emerging growth market.

Japan Waste Derived Biogas Market

Japan was valued at USD 2.05 billion in 2025 and is expected to hit USD 2.30 billion in 2026. Japan’s renewable fuel strategy emphasizes energy security, waste utilization, and decarbonization. The country has developed advanced waste-to-energy infrastructure, including municipal solid waste gasification and biogas recovery facilities. Japan is also investing in sustainable aviation fuel and renewable diesel partnerships to reduce transport emissions. With limited domestic fossil fuel resources, Japan prioritizes efficient waste conversion technologies and grid integration of renewable gases. Its strong industrial base and technology innovation capacity support the steady expansion of renewable fuel deployment.

Latin America

Latin America accounted for USD 6.01 billion in 2025, or approximately 8.81% of global revenues. In Latin America, the market is progressing with activity concentrated in biodiesel/renewable diesel and biogas adoption. Nations such as Brazil and Argentina are increasing biofuel blend mandates (e.g., higher biodiesel content in diesel), helping to spur local feedstock utilization and production. Brazil, in particular, is drawing attention for boosting biofuel levels to improve energy independence and reduce petroleum imports, while other countries explore biomethane and RNG in rural and transport segments. Infrastructure limitations and investment variability mean Latin America’s share remains modest, but supportive energy policies and natural resource availability point to strong growth potential.

Middle East & Africa

The Middle East & Africa were valued at USD 5.03 billion in 2025. Limited infrastructure and historically high reliance on fossil fuels have constrained rapid uptake, but recent diversification efforts, including renewable diesel co-processing trials and community-scale biogas programs, are emerging. Governments in the UAE, Saudi Arabia, and South Africa are exploring bioenergy projects as part of broader clean energy strategies, while some African countries leverage agricultural waste to expand decentralized renewable gas solutions. Although the Middle East & Africa’s current share is relatively low, the region’s energy transition goals suggest potential for increased participation as supportive frameworks develop.

GCC Waste Derived Biogas Market

The GCC market was estimated at USD 2.03 billion in 2025 and is set to reach USD 2.22 billion in 2026. The GCC region, including Saudi Arabia, the UAE, and others, is gradually expanding its renewable fuels footprint as part of broader economic diversification strategies. Historically dependent on oil and gas exports, GCC countries are investing in waste-to-energy facilities, landfill gas capture, and pilot renewable diesel projects. National sustainability agendas emphasize circular economy practices and emissions reduction. While renewable fuel deployment remains at an early stage compared to Western and Asian leaders, increasing infrastructure investments and policy support signal a growing commitment to low-carbon fuel development across the region.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

High Focus Toward Decarbonization Boosts the Key Players’ Market Share

Veolia Environment, Engie, EnviTec Biogas, Ameresco, and Air Liquide are some of the leading key players in this industry. Companies focus on expanding anaerobic digestion capacity, improving biogas upgrading efficiency, capturing methane from waste streams, and supporting grid-injected biomethane and low-carbon transport fuels. Moreover, they emphasize decarbonization, circular economy integration, and long-term infrastructure investments to accelerate renewable gas adoption globally.

- In 2022, Solvay and Veolia Environnement initiated the “Dombaslé Energie” project to decarbonize the Dombasle-sur-Meurthe facility by replacing coal with Refuse-Derived Fuel (RDF). The plan involves shutting down three coal-fired boilers and installing two new furnaces powered by non-recyclable waste. This transition is expected to cut the plant’s CO₂ emissions by half while eliminating the need to import roughly 200,000 tons of coal each year. The project strengthens the site’s long-term competitiveness while advancing industrial energy transition goals.

List of Key Waste Derived Biogas Companies Profiled:

- Veolia Environnement S.A. (France)

- ENGIE SA (France)

- EnviTec Biogas AG (Germany)

- Ameresco, Inc. (U.S.)

- Air Liquide SA (France)

- Wartsila Corporation (Finland)

- PlanET Biogas Global GmbH (Germany)

- Greenlane Renewables Inc. (Canada)

- WELTEC BIOPOWER GmbH (Germany)

- Gasum Oy (Finland)

KEY INDUSTRY DEVELOPMENTS

- January 2026: Ameresco, Inc. announced the operation of a 5.2 MWe landfill gas-to-RNG facility in East Moline, Illinois, U.S., converting raw landfill gas into pipeline-quality renewable natural gas and reducing over 27,000 metric tons of CO₂ annually.

- November 2025: Veolia activated a digital solution at its industrial ecology hub in Gironde, France, enabling electricity from waste-to-biogas conversion to provide fast-response grid balancing services, reflecting innovative integration of biogas recovery with power system needs

- October 2025: EnviTec Biogas AG secured its first contract to construct a biogas upgrading plant with CO₂ liquefaction in Belgium, set for completion in July 2026, enabling biomethane injection into the national grid and daily bio-LCO₂ output for circular economy use.

- May 2024: Veolia Environnement S.A. joined ENGIE SA and Waga Energy in France to formalize a 13-year Biomethane Purchase Agreement (BPA) enabling ENGIE to market renewable natural gas produced from Veolia’s landfill biogas without government feed-in tariffs, strengthening market financing and long-term off-take visibility.

- April 2024: Air Liquide SA revealed construction of two new biomethane production units in Pennsylvania and Michigan to treat dairy farm waste into purified RNG for grid injection, supporting circular economy principles and expanded low-carbon gas deployment.

REPORT COVERAGE

The report provides a comprehensive analysis of the market, focusing on key aspects such as leading companies, product processes, and Porter’s Five Forces. Additionally, the report provides valuable insights into market trends and highlights key industry developments. In addition to the factors mentioned above, the report also encompasses several factors that contributed to the market's growth in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 8.03% from 2026 to 2034 |

| Unit | Value (USD Billion) |

|

Segmentation |

By Feedstock

|

|

By Technology

|

|

|

By End User

|

|

|

By Region

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 68.25 billion in 2025 and is projected to reach USD 140.84 billion by 2034.

In 2025, the Europes market value stood at USD 21.28 billion.

The market is expected to exhibit a CAGR of 8.03% during the forecast period.

By feedstock, municipal solid waste segment dominated the market in 2025.

Stringent carbon reduction and renewable fuel policies are the key factors driving the market.

Veolia Environment, Engie, EnviTec Biogas, Ameresco, and Air Liquide are the major players in the global market.

Europe dominated the market in 2025 with the largest share.

- 2021-2034

- 2025

- 2021-2024

- 326

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us