Smart Food Packaging Market Size, Share & Industry Analysis, By Technology Type (Active Packaging, Intelligent Packaging, Connected/Digital Packaging, and MAP/CAP Smart Systems), By Packaging Format (Flexible Packaging, Rigid Packaging, and Semi-rigid Packaging), By Material Type (Plastic, Paper & Paperboard, Metal, and Others), By Application (Fresh & Perishable Foods, Prepared & Ready Meals, Dairy Products, Beverages, Snack Foods, Bakery & Confectionery, and Pet Food), and Regional Forecast, 2026-2034

(Offer valid till 31st Jul 2026)

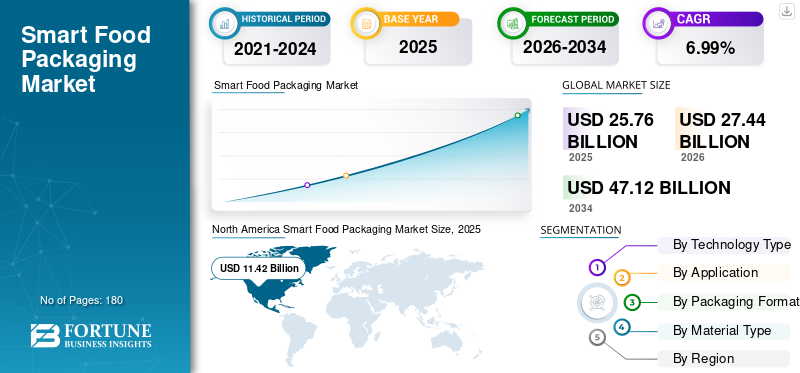

Smart Food Packaging Market Size and Future Outlook

The smart food packaging market size was valued at USD 25.76 billion in 2025. The market is projected to grow from USD 27.44 billion in 2026 to USD 47.12 billion by 2034, exhibiting a CAGR of 6.99% during the forecast period. North America dominated the smart food packaging market with a market share of 44.33% in 2025.

Smart packaging materials are designed to help keep food fresh and share information to the related stakeholders about the product’s condition as it moves through the supply chain. Smart packaging uses features such as oxygen scavengers, antimicrobial coatings, moisture absorbers, freshness indicators, RFID tags, conductive inks, among others to maintain food quality. These materials are widely used in meat, seafood, dairy, bakery, frozen foods, and ready-to-eat meals, where shelf-life stability and contamination control are critical. The market is growing rapidly as expansion of global supply chains, movement of goods across temperature-sensitive areas, and increasing dependency on cold-chain logistics and e-commerce food delivery networks.

Companies such as Amcor plc, Sealed Air, Tetra Laval, Mondi Group and others are some of the key players operating in this market. New product launch is boosting product sales and supporting the smart food packaging market growth.

Download Free sample to learn more about this report.

SMART FOOD PACKAGING MARKET TRENDS

Shift Toward Sustainable Smart Materials Reshaping Packaging Innovation

Increasing number of food brands currently use QR codes, NFC tags, and smartphone-scannable packaging to provide consumers information about traceability, sourcing details, promotions, and real-time product information enhancing consumer trust. Active packaging technologies are combined with eco-friendly materials, such as recyclable single-material packaging and biodegradable films that include antimicrobial or oxygen-absorbing features. Smart freshness indicators are also becoming common in seafood, meat, and dairy packaging, helping retailers reducing food waste.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Food Waste Pressure Accelerating Adoption of Freshness-Monitoring Packaging

The market is being strongly driven by rising pressure on food manufacturers and retailers to reduce spoilage losses across complex global supply chains. Growth in temperature-sensitive food categories such as ready meals, seafood, dairy, and plant-based products has increased adoption of time-temperature indicators, oxygen scavengers, and antimicrobial films. The rapid growth of e-commerce grocery delivery is also increasing demand for smart packaging that can track shipping conditions and detect food tampering. Stricter rules on food traceability, especially in North America, Europe, and East Asia, are some of the ley factors which are boosting the smart food packaging market growth.

MARKET RESTRAINTS

High Technology Costs Limiting Adoption Among Price-Sensitive Food Manufacturers

Implementation cost of this technology is high which acts as a barrier to the adoption of smart food packaging. Advanced packaging features such as biosensors, RFID chips, conductive inks, and specialized barrier materials make packaging expensive than traditional options. Unclear regulations about the safety and recyclability of active packaging materials are also slowing down commercialization in some areas. Another major challenge is the lack of recycling facilities for multi-layer smart packaging that contains electronic or chemical components. In developing countries, unreliable cold-chain systems and low consumer awareness also decreasing the demand for smart packaging.

MARKET OPPORTUNITIES

Expansion of Digital Traceability Creating Growth Potential for Market

The market presents significant opportunities through the convergence of smart packaging with digital food supply-chain ecosystems and sustainability-focused innovation. Growing investment in biodegradable intelligent packaging materials creates strong commercial potential for companies developing compostable sensor-integrated films and bio-based active packaging systems. The expansion of personalized nutrition and premium fresh-food delivery services is creating opportunities for packaging formats that enable real-time freshness communication and product authentication.

Segmentation Analysis

By Technology Type

Direct Shelf-Life Extension Benefits Increasing Adoption of Active Packaging Across High-Volume Food Categories

The market is segmented by technology type active packaging, intelligent packaging, connected/digital packaging, and MAP/CAP Smart Systems.

The active packaging solutions held the largest smart food packaging market share in 2025. It offers benefits such as longer shelf life, improved food safety, and help reduce waste, for high-volume food products. Technologies such as oxygen scavengers, moisture absorbers, antimicrobial coatings, ethylene absorbers, and modified atmosphere packaging are widely used in food processing. Meat, seafood, dairy, bakery, and ready-to-eat foods choose active packaging remain fresh in this packaging condition.

Intelligent packaging is another major segment, accounting for 7.21% CAGR during the forecast period. Technologies such as RFID tags, freshness indicators, time-temperature indicators, QR tracking, and sensor-based packaging are becoming increasingly popular as more companies seek supply-chain transparency and real-time product monitoring.

By Application

High Spoilage Risk and Cold-Chain Sensitivity Driving Dominance of Fresh & Perishable Foods Segment

Based on the application the market is segmented into fresh & perishable foods, prepared & ready meals, dairy products, beverages, snack foods, bakery & confectionery, and pet food.

Fresh & perishable foods accounted for the largest market share in 2025. It requires continuous preservation of freshness and strict cold-chain monitoring to maintain quality and regulatory compliance. Smart packaging technologies, including oxygen scavengers, antimicrobial films, freshness indicators, and time-temperature sensors, are therefore extensively used to extend shelf life, reduce spoilage losses, and improve inventory efficiency for retailers and exporters.

Prepared & ready meals are another major segment, and is predicted to account for 7.06% CAGR during the forecast period. Smart packaging for these meals helps control the package's atmosphere and share real-time information about freshness.

By Packaging Format

Superior Product Protection and Sensor Integration Capability Driving Dominance of Rigid Packaging Segment

The market is segmented, by packaging format into flexible packaging, rigid packaging, and semi-rigid packaging.

The flexible packaging led the global market in 2025. Trays, containers, bottles, cartons, and jars are commonly used in dairy, meat, seafood, beverages, and ready-to-eat foods. Rigid packaging is suitable to add smart features such as RFID tags, freshness sensors, QR labels, and time-temperature monitors. Rigid packaging also protects products during long-distance shipping and cold-chain logistics, making it often the choice for retail and export-focused food supply chains.

Flexible packaging is another major category that has a CAGR of 7.24% during the forecast period. It is used due to its lightweight structure, lower material consumption, and growing use in convenience food and snack packaging applications. Pouches, films, wraps, and sachets are increasingly integrated with active packaging technologies such as oxygen scavengers and antimicrobial coatings to improve shelf life while reducing packaging costs.

By Material Type

To know how our report can help streamline your business, Speak to Analyst

High Barrier Performance and Smart Technology Compatibility Driving Dominance of Plastic Segment

The market is segmented, by material type, into plastic, paper & paperboard, metal, and others.

The plastic segment led in the global market in 2025. Materials such as polyethylene (PE), polyethylene terephthalate (PET), polypropylene (PP), and polyamide are widely used because they resist moisture, block oxygen, are lightweight, and are cost-effective. Plastic packaging makes it easier to add smart features such as antimicrobial coatings, oxygen scavengers, RFID tags, freshness indicators, and sensor-enabled films, all while keeping packaging flexible and safe.

Paper & paperboard segment accounted for the second largest market share in 2025 and are expected to register a growth rate of 6.75% CAGR during the forecast period. More food brands are choosing paper-based smart packaging that uses printed sensors, QR codes, and bio-based coatings. This type of packaging is growing rapidly across dry foods, bakery items, takeaway containers, and secondary retail packaging. But compared to plastic, paper-based materials do not resist moisture as well and are less durable.

Smart Food Packaging Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

Asia Pacific

North America Smart Food Packaging Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific market was valued at USD 5.60 billion in 2025. The market growth in the Asia Pacific is driven by urbanization, more organized retail, and higher demand for convenience foods. China and Japan are key markets as it uses advanced sensor-enabled packaging for seafood, ready meals, and pharmaceutical-grade food logistics. Japan’s aging population and emphasis on food freshness are driving up demand for time-temperature indicators and antimicrobial packaging in high-value perishables. In China, more e-commerce food delivery platforms are adopting smart packaging to enhance traceability and detect tampering. India and Southeast Asian countries are increasingly investing in low-cost, intelligent packaging solutions to address supply chain inefficiencies and post-harvest food losses.

India Smart Food Packaging Market

The India market in 2025 was around USD 0.61 billion, accounting for roughly 2.36% of global market revenues. India’s market is witnessing strong growth due to rapid urbanization, expansion of organized retail, and increasing consumption of packaged convenience foods.

China Smart Food Packaging Market

China’s market in 2025 was around USD 1.79 billion, representing roughly 6.96% of market share. China’s market is expanding rapidly due to rising consumer preferences for packaged food, growth in e-commerce food delivery, and increasing government focus on food safety traceability. Intelligent packaging technologies such as QR-enabled authentication, RFID tracking, and freshness-monitoring labels are widely adopted in seafood, dairy, infant nutrition, and premium imported food products.

Japan Smart Food Packaging Market

The Japan market in 2025 reached around USD 1.32 billion, accounting for roughly 5.11% of global market revenues.

North America

The market in North America reached USD 11.42 billion in 2025 and is the leading region. The North American market is being shaped by the rapid commercialization of active and intelligent packaging technologies across meat, dairy, and ready-to-eat food categories. U.S. retailers are increasingly integrating freshness indicators, RFID-enabled traceability, and oxygen scavenger systems to reduce food waste and comply with stringent FDA food safety regulations. Major food manufacturers are investing in connected packaging that supports real-time inventory monitoring and cold-chain validation, particularly for e-commerce grocery distribution. Demand is also rising for recyclable smart materials that align with ESG commitments from multinational consumer packaged goods companies.

U.S. Smart Food Packaging Market

In 2025, the U.S. market was valued at USD 9.61 billion. The market is driven by large-scale adoption of intelligent and active packaging technologies across packaged meat, dairy, frozen food, and ready-to-eat meal industries. Major food manufacturers and retailers are investing heavily in RFID-enabled traceability, freshness indicators, and antimicrobial packaging to reduce food waste and improve cold-chain visibility. Growth of online grocery platforms and direct-to-consumer meal delivery services is also accelerating demand for tamper-evident and temperature-monitoring packaging solutions.

Europe

The European market reached USD 6.25 billion in 2025. It is one of the most regulated markets for smart food packaging. Germany, France, and other markets are using smart packaging solutions to help supermarkets track shelf life and reduce food waste. Modified atmosphere packaging integrated with freshness sensors is gaining traction in premium dairy, organic produce, and processed meat applications. European consumers show strong acceptance of QR-enabled transparency tools that provide sourcing, carbon footprint, and allergen information. The region is also witnessing extensive R&D collaboration between packaging converters, chemical companies, and food processors to develop compostable smart films and bio-based active packaging materials that meet recyclability standards without compromising barrier performance.

Germany Smart Food Packaging Market

The market in Germany in 2025 reached USD 1.44 billion, representing roughly 5.59% of global market revenues. Germany is a leading in European market due to strong sustainability and eco-friendly solutions and regulations, advanced food processing industries, and high adoption of intelligent packaging technologies in retail supply chains.

U.K. Smart Food Packaging Market

U.K. market reached USD 1.10 billion in 2025, equivalent to around 4.29% of global market sales. The market is driven by rising demand for sustainable packaging, strict food safety monitoring, and rapid growth in convenience food consumption.

South America and Middle East & Africa

Over the forecast period, South America is expected to experience significant growth in this market. The South America market in 2025 was recorded at USD 1.35 billion. The South American market is evolving gradually, supported by growth in processed food exports and the modernization of regional cold-chain infrastructure. Brazil dominates the market due to its large meat processing and agricultural export industries, where intelligent packaging technologies are used to monitor product integrity during long-distance transportation.

Middle East & Africa reached USD 1.15 billion in 2025. The market is being driven primarily by food import dependence, climate-related storage challenges, and investments in modern retail infrastructure. Gulf countries, particularly the UAE and Saudi Arabia, are adopting intelligent packaging technologies for imported dairy, poultry, and frozen foods to strengthen shelf-life monitoring under extreme temperature conditions. Premium food retailers and distributors of halal-certified products are using more smart labels and tamper-evident packaging.

In Africa, smart packaging is still new but is slowly spreading through urban retail chains and the packaged beverage sector in countries such as South Africa, Kenya, and Nigeria. Multinational food companies are offering affordable active packaging to help reduce spoilage during transport and make supply chains more efficient, especially where refrigeration is unreliable.

UAE Smart Food Packaging Market

UAE market is set to grow at a CAGR of 5.83% during the forecast period. Expansion of packaged protein snacks and supplements is supporting growth. The market is expanding due to high dependence on imported food products, rapid retail modernization, and growing investment in food security infrastructure.

COMPETITIVE LANDSCAPE

Key Industry Players

Rising Demand for Integrated Shelf-Life Extension and Digital Traceability Intensifying Competition

In the smart food packaging market, packaging manufacturers, materials science companies, printed electronics firms, and food technology providers are working together to create integrated, active, and intelligent packaging solutions. Top companies including Amcor plc, Sealed Air, Avery Dennison, Berry Global, Multisorb Technologies, and Crown Holdings, Inc., are developing high-barrier active packaging to extend the shelf life of meat, seafood, dairy, and ready meals. Competition are transforming from basic packaging towards smart systems that combine sustainability, preservation, and digital engagement. Food producers and packaging innovators are partnering to bring recyclable active films and affordable intelligent labels to market their products and enhance consumer engagement.

LIST OF SMART FOOD PACKAGING COMPANIES PROFILED

- Amcor plc (Switzerland)

- Sealed Air (U.S.)

- Tetra Laval (Switzerland)

- Mondi Group (U.K.)

- Toyo Seikan Group Holdings, Ltd. (Japan)

- Crown Holdings, Inc. (U.S.)

- 3M (U.S.)

- MITSUBISHI HEAVY INDUSTRIES, LTD. (Japan)

- Huhtamäki Oyj (Finland)

- StePac PPC (Israel)

KEY INDUSTRY DEVELOPMENTS

- January 2026: DCGpac.COM, a packaging company inaugurated its first 20,000 sq. ft. Smart Manufacturing Plant in Noida to produce eco-friendly, biodegradable, and export-grade packaging. The new facility has a 250-tonne monthly capacity, focusing on AI-powered ProPac platform technology, advanced extrusion, and circular economy initiatives.

- September 2025: GreenPack Innovations launched a new line of eco-friendly, flexible packaging solutions to meet rising demand for sustainable packaging across industries such as food and beverage, pharmaceuticals, and consumer goods. These new solutions help to minimize environmental impact, maximize product performance, and increase shelf life.

- November 2024: Mondelēz International, in partnership with Amcor and Jindal Films, launched new, recycle-ready packaging for Cadbury sharing bars in the UK and Ireland. The packaging, named Amcor's AmFiniti recycled plastic, features 80% recycled content.

- November 2024: VarieT Technology introduced a new revolutionary Smart Heat Battery that could transform food and beverage packaging. Its Smart Heat Battery is designed to heat cans on demand, supporting diverse applications such as food delivery, camping, and more.

- April 2023: Packaging solutions manufacturer Huhtamaki developed mono-material technology for packaging products. Products such as Paper, PE, and PP Retort are transformational and meet the demands of both its customers and their consumers.

REPORT COVERAGE

The global smart food packaging market research provides an in-depth study of market sizes & forecast by all the market segments included in the report. The market analysis includes details on the market dynamics and market trends expected to drive the market forecast. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market industry also encompasses detailed competitive landscape with information on the market segmentation, market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.99% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Technology Type, By Application, By Packaging Format, By Material Type, and Region |

| By Technology Type |

|

| By Application |

|

| By Packaging Format |

|

| By Material Type |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 25.76 billion in 2025 and is projected to reach USD 47.12 billion by 2034.

In 2025, the North America market value stood at USD 11.42 billion.

The market is expected to exhibit a CAGR of 6.99% during the forecast period

By material type, plastic segment led the global market.

Rising food waste pressure accelerating adoption of freshness-monitoring packaging.

Amcor plc, Sealed Air, Tetra Laval, and Mondi Group are a few of the players in the market.

North America held the largest market share in 2025.

Shift toward sustainable smart materials reshaping packaging innovation.

- 2021-2034

- 2025

- 2021-2024

- 180

-

(Offer valid till 31st Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us