Oncology Drugs Market Size, Share & Industry Analysis, By Drugs Class (Cytotoxic Drugs {Alkylating Agents, Antimetabolites, & Others}, Targeted Drugs {Monoclonal Antibodies & Others}, Hormonal Drugs, & Others), By Therapy (Chemotherapy, Targeted Therapy, Immunotherapy, & Others), By Indication (Lung Cancer, Stomach Cancer, Colorectal Cancer, Breast Cancer, Prostate Cancer, & Others), By Dosage Form (Solid {Tablets & Capsules}, Liquid, & Injectable {Prefilled Syringes & Others}), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, & Others), and Regional Forecast, 2026-2034

Oncology Drugs Market Size and Future Outlook

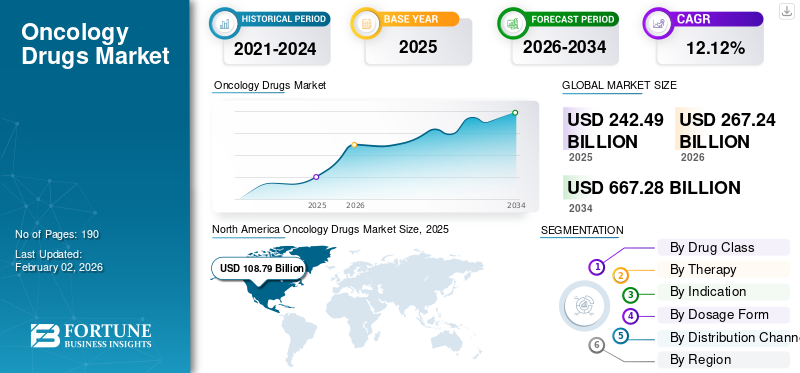

The global oncology drugs market size was valued at USD 256.46 billion in 2025. The market is projected to grow from USD 286.36 billion in 2026 to USD 697.59 billion by 2034, exhibiting a CAGR of 11.77% during the forecast period. North America dominated the oncology drugs market with a market share of 45.44% in 2025.

Oncology drugs refers to the prescription medications that are utilized to treat various forms of cancers such as solid tumors and hematologic malignancies. The global market is projected to grow at a considerable growth rate particularly driven by a substantial cancer patients burden coupled with breakthrough product launches. Another important factor is the increasing trend of treatment initiation in the earlier stages of cancer due to innovations in diagnostic technologies such as biomarker testing. Moreover, in recent times, there have been several launches of blockbuster drugs, with a considerable proportion of total cancer spend focused on these therapies, again leading to market growth. Additionally, other factors such as drug uptake increasingly based on companion diagnostics, real-world evidence, and payers’ cost-effectiveness, is also expected to further provide impetus to the market growth.

- For instance, in December 2025, the U.S. Food and Drug Administration approved pharmaand GmbH’s targeted therapy of rucaparib (Rubraca) for adults with a deleterious BRCA mutation (BRCAm) (germline and/or somatic)-associated metastatic castration-resistant prostate cancer (mCRPC) that was previously treated with an androgen receptor-directed therapy. Moreover, the patients should be selected for therapy using an FDA-approved companion diagnostic (CDx).

Also, several pharmaceutical companies such as Merck & Co., Inc., AstraZeneca, and Bristol-Myers Squibb Company, and others, are amongst the major players in the market. These companies are focusing on strategic initiatives such as acquisitions of smaller players coupled with bolstering their product pipeline for innovative drug launches.

Download Free sample to learn more about this report.

ONCOLOGY DRUGS MARKET TRENDS

Early Use of High Value Targeted Drugs with Innovative Delivery Pose as Market Trends

Some of the most important trends witnessed in the global market is the increasing utilization of premium medications in the initial stages of the disease. The market is transitioning from the treatment of only metastatic disease to treating the earlier stages of the disease where cure is probable, as prevention of recurrent cancer helps reduce the economic burden of cancer. If any targeted therapy shows the promise of event-free survival or recurrence reduction, then that therapy can be part of the standard perioperative pathways, substantially increasing the therapy uptake. Another critical trend is the development of advanced subcutaneous formulations, that improve throughput in infusion centers, reduce nursing time, and boost the patient experience, which can support swifter product adoption even when the medication is the same and faces generic competition.

- In December 2025, the European Medicines Agency validated for review a Type II variation application for PADCEV (enfortumab vedotin), in combination with KEYTRUDA (pembrolizumab), a PD-1 inhibitor, for adults suffering from muscle-invasive bladder cancer (MIBC) who are ineligible for cisplatin-containing chemotherapy. This approval was for a perioperative regimen.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Considerable Patient Population Burden with Advanced Product Launches to Drive Market Growth

The prevalence and incidence of various cancers, such as breast cancer, lung cancer, among others, is increasing tremendously among the population in both developed as well as emerging countries globally. Some of the major factors for the rising prevalence of the condition are tobacco smoking, higher exposure to ultraviolet radiation, rising pollution levels, and changing diet patterns, among others. Furthermore, several advanced forms of therapies are being launched in the market such as antibody drug conjugates. These therapies are combining the specificity of targeted drugs with the tumor-killing power of cytotoxics, leading to strong efficacy even after prior therapies. All these factors collectively drive the oncology drugs market growth across the forecast period.

- According to the American Cancer Society statistics for 2026, an estimated 2,114,850 new cancer cases and 626,140 cancer deaths are projected to occur in the U.S. in 2026.

- According to the 2026 statistics by the European Commission, there were an estimated 3.7 million new cancer cases in the European Union every year.

MARKET RESTRAINTS

Reimbursement Pressures to Restrict Wider Market Growth

The most important parameter that restrains the higher growth rate of this market is the fact that certain high cost cancer drugs often require clear survival or quality-of-life benefits relative to price by the healthcare payers. In cases of premium drugs where the clinical efficacy evidence is lacking or when comparative drug options are considered, reimbursement decisions often slow down, leading to slower uptake. Even when these drugs gain reimbursement support, the access to them is restricted with the need of prior authorization, limited number of centers providing access to these drugs and line-of-therapy rules. This is particularly relevant for the most cutting edge therapies such as radioligand therapies and cell therapies, which require specialized infrastructure. This leads to an uneven product adoption, restricting the market growth across the forecast period.

- For instance, in February 2026, National Institute for Health and Care Excellence (NICE) in the U.K., rejected Pfizer’s Ibrance in the first draft guidance by explicitly citing the high costs of the drug, illustrating the access barriers due to cost-effectiveness limits.

MARKET OPPORTUNITIES

Growth in Combination Therapies to Provide Avenues for Market Growth

The next set of therapies that have considerable proportion for the market growth are the combination regimes for cancer care such as immunotherapy used together with targeted therapies. These therapies, when used together, hold the potential for creating clinical outcomes that improve the depth and the durability of response. When the two drugs used in combination therapies are mechanistically complementary, these combinations can convert non-responders into responders, potentially expanding the eligible patient population. This is expected to create the next wave of oncology value growth.

- For instance, in November 2025, the U.S. FDA approved the combination of durvalumab (Imfinzi, AstraZeneca) with fluorouracil, leucovorin, oxaliplatin, and docetaxel (FLOT) chemotherapy as a neoadjuvant and adjuvant treatment, followed by the single agent durvalumab, for adults with resectable gastric or gastroesophageal junction adenocarcinoma (GC/GEJC).

MARKET CHALLENGES

Manufacturing & Supply Constraints for Complex Therapies to Pose Challenges to Market Growth

Some of the challenges associated with the oncology drugs market is the fact that several newer formulations of oncology medications require complex production. This is particularly relevant for the antibody drug conjugates and radioligand therapies. These complex therapies need conjugation chemistry, sterile fill-finish, radioisotope handling requirements. Furthermore, in the case of radiopharmaceuticals, the isotopes decay quickly, so production and distribution must be tightly coordinated. This considerably reduces the market growth as it hinders the patient’s access to key drugs and also eliminates the possibility of early adoption of key therapeutics. Such challenges reduce the probability of a greater market growth rate.

- For instance, in May 2025, ITM Isotope Technologies Munich SE (ITM), a leading radiopharmaceutical biotech company, and Radiopharm Theranostics, announced an agreement to secure capacity for lutetium-177.

Segmentation Analysis

By Drug Class

Considerable Costs of Targeted Drugs and Robust Adoption Rates to Lead to Segmental Dominance

On the basis of the drug class segment, the market is segmented into cytotoxic drugs, targeted drugs, hormonal drugs, and others. The cytotoxic drugs segment can be further sub-segmented into alkylating agents, antimetabolites, and others. The targeted drugs segment is further classified into monoclonal antibodies, and others.

In terms of drug class segment, the targeted drugs segment is estimated to account for the largest oncology drugs market share. The segment’s dominating market share is owing to the fact that several targeted drugs such as Keytruda (pembrolizumab) and Opdivo (nivolumab), are often at the forefront of innovative cancer treatments. Furthermore, the targeted drugs segment is also the drug class under which most valuable innovation is being undertaken.

- For instance, in April 2024, AstraZeneca and Daiichi Sankyo, received the U.S. FDA approval for Enhertu (trastuzumab deruxtecan) for the treatment of adult patients suffering from unresectable or metastatic HER2-positive (IHC 3+) solid tumors, who have been administered prior systemic treatment and have no satisfactory alternative treatment options. Such key product approvals significantly drive the segmental growth across the forecast period.

The cytotoxic drugs segment is anticipated to rise with a CAGR of 11.43% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Therapy

Strong Adoption of Targeted Therapies to Enable Segmental Dominance

On the basis of therapy, the market is segmented into chemotherapy, targeted therapy, immunotherapy, and others.

In 2025, the targeted therapy segment accounted for the dominant revenue share of the global market. The segmental dominance is attributed to certain benefits of this therapy including heightened precision in attacking of cancer cells which increases the chances of survival among the patients, and targeting of specific genes and proteins that help cancer cells to grow.

- For instance, in February 2026, the U.S. FDA approved pembrolizumab (Keytruda, Merck) as well as pembrolizumab and berahyaluronidase alfa-pmph (Keytruda Qlex, Merck) in combination with paclitaxel, with or without bevacizumab, for adult patients with platinum-resistant epithelial ovarian, fallopian tube, or primary peritoneal carcinoma whose tumors express PD-L1 (CPS≥1) as determined by an FDA-authorized test, and who have received one or two prior systemic treatment regimens.

The immunotherapy segment is projected to grow at a CAGR of 12.79% over the forecast period.

By Indication

Substantial Case Burden of Lung Cancer to Allow for Segment’s Dominance

In terms of indication, the market is segmented into lung cancer, stomach cancer, colorectal cancer, breast cancer, prostate cancer, and others.

The lung cancer segment accounted for the dominant market share over the forecast period. The dominance of the segment is attributed to increasing prevalence of lung cancer due to the growing diagnosis rate among the patient population. Furthermore, the increasing focus of key players toward research and development activities for launching innovative oncology drugs in this indication, is anticipated to support the growing adoption for these drugs in the market.

- For instance, in May 2024, the U.S. FDA granted an accelerated approval to Amgen Inc.’s, tarlatamab-dlle (Imdelltra, Amgen, Inc.) for the treatment of extensive stage small cell lung cancer (ES-SCLC) with disease progression on or after platinum-based chemotherapy.

The breast cancer segment is projected to grow at a CAGR of 13.25% over the forecast period.

By Dosage Form

Strong Administration of Injectable Drugs to Boost Segment’s Dominance

On the basis of dosage form, the market is trifurcated into solid, liquid, and injectable. The solid segment is further classified into capsules and tablets. The injectable segment is further sub-segmented into prefilled syringes and others.

The injectable segment accounted for the largest market share over the forecast period. The advantages and clinical benefits of injectable oncology drugs such as an availability of a wide range of polymer structures, high chemical versatility, and others, is leading to an increasing preference of healthcare providers and patients toward these drugs. This combined with emphasis of market players on launching medicines in the injectable form, is projected to drive the growth of the segment during the forecast period.

- For instance, in January 2025, Johnson & Johnson’s injectable therapy of RYBREVANT (amivantamab for injection) in combination with carboplatin and pemetrexed (platinum-based chemotherapy) for the treatment of patients with locally advanced or metastatic non-small cell lung cancer (NSCLC) with activating epidermal growth factor receptor (EGFR) Exon 19 deletions or Exon 21 L858R substitution mutations, whose disease has progressed on or after treatment with osimertinib, was approved in Canada.

The solid segment is projected to grow at a CAGR of 11.22% over the forecast period.

By Distribution Channel

Considerable Administration in Hospital Settings to Lead to Hospital Pharmacies’ Market Dominance

In terms of distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, and online pharmacies.

The hospital pharmacies accounted for the largest global market share. The hospital pharmacies held a significant proportion of the market value as oncology is a condition where the drugs especially the injectable medications are administered in the hospital settings. Furthermore, the segment is set to hold 51.92% share in 2026.

- For instance, in September 2025, BD (Becton, Dickinson and Company) and Henry Ford Health, announced a pharmacy automation partnership for the development of a health system pharmacy of the future that will go on to create initially, a robotic solution enabling patients to pick up select prescriptions at their ease, 24 hours a day, seven days a week.

Moreover, the online pharmacies segment is projected to grow at a CAGR of 12.41% across the forecast period.

Oncology Drugs Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Oncology Drugs Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America recorded a market size of USD 108.79 billion in 2025, capturing 44.86% of the global market share, and is projected to reach USD 118.41 billion in 2026. The market in North America is projected to grow significantly across the forecast period owing to adoption of cutting edge therapeutics, strong spending capacity for oncology drugs, swift adoption of biomarker testing, dense clinical trial networks, and broad availability of specialty centers for advanced modalities. These factors, coupled with innovative product approvals from the U.S. FDA, is to drive the market growth in the region.

U.S. Oncology Drugs Market

Based on North America’s regional dominance and the U.S.’ largest share within the region, the U.S. market can be analytically approximated at around USD 121.82 billion in 2026, accounting for roughly 42.5% of global sales.

Europe

In 2025, Europe represented USD 56.86 billion, accounting for 23.45% of the worldwide market, and is projected to grow to USD 63.69 billion in 2026. Some of the parameters to the region’s strong market share includes the presence of key regulatory pathways, strong local reimbursement support, and advanced treatment adoption rates.

U.K. Oncology Drugs Market

The U.K. market in 2025 was valued at around USD 7.97 billion, representing roughly 3.1% of global revenues.

Germany Oncology Drugs Market

Germany’s market reached approximately USD 14.47 billion in 2025, equivalent to around 5.6% of global sales.

Asia Pacific

The Asia Pacific market generated USD 50.95 billion in 2025, representing 21.01% of the global market landscape, and is expected to reach USD 57.82 billion in 2026 and has secured the position of the third-largest region in the market. In the region, India and China both reached USD 6.21 billion and USD 13.32 billion, respectively in 2025.

Japan Oncology Drugs Market

The Japan market size in 2025 was recorded at around USD 14.73 billion, accounting for roughly 5.7% of global revenues. Japan has a large share in the global market owing to the country’s strong approvals for landmark drugs, coupled with strong healthcare spending and patient population base.

China Oncology Drugs Market

China’s market is projected to be one of the largest worldwide, with 2025 revenues valued at around USD 13.32 billion, representing roughly 5.2% of global sales.

India Oncology Drugs Market

The India market size in 2025 was valued at around USD 6.21 billion, accounting for roughly 2.4% of global revenues.

Latin America and Middle East & Africa

Latin America and the Middle East & Africa regions are expected to witness steady positive growth rates in this market space during the forecast period. The Latin America market reached a valuation of USD 16.09 billion in 2025. Increasing healthcare expenditure and reimbursement support, coupled with a substantial patient population demographic is to drive the market growth in these regions. In the Middle East & Africa, the GCC reached a valuation of USD 5.73 billion in 2025. Middle East & Africa accounted for USD 10.61 billion in 2025, representing 4.37% of the global market share, and is projected to reach USD 11.17 billion in 2026. In 2025, Latin America held 6.30% of the global market, reaching a valuation of USD 15.28 billion, and is projected to grow to USD 16.15 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Cutting Edge Oncology Drugs Pipeline and Industry Leading Product Portfolio to Contribute to Players’ Market Dominance

The global market reflects a semi-fragmented competitive landscape, consisting of pharmaceutical giants such as Merck & Co., Inc., AstraZeneca, and Bristol-Myers Squibb Company, among others. The considerable company revenue share accounted by these companies is owing to the presence of blockbuster cancer drugs in their product portfolio, established geographical reach, and an oncology drug pipeline consisting of revolutionary drugs. Furthermore, these players are also engaged in strategic initiatives such as acquisition of other key companies to expand their market presence across the forecast period.

- For instance, in December 2025, the U.S. FDA approved Lunsumio VELO (subcutaneous mosunetuzumab) for R/R follicular lymphoma after ≥2 prior lines, reducing administration time to ~1 minute.

Other major companies present in the global market include Novartis AG, F. Hoffmann-La Roche Ltd., Bayer AG, and Sanofi, among others. These companies hold diverse oncology drugs portfolios, and are focusing on the launches of novel drugs and therapies for several types of cancer across the forecast period in addition to strategic initiatives.

LIST OF KEY ONCOLOGY DRUGS COMPANIES PROFILED

- Hoffmann-La Roche Ltd. (Switzerland)

- AbbVie Inc. (U.S.)

- Novartis AG (Switzerland)

- Pfizer Inc. (U.S.)

- AstraZeneca (U.K.)

- GSK plc (U.K.)

- Eli Lilly and Company (U.S.)

- Sanofi (France)

- Bayer AG (Germany)

- Merck & Co., Inc. (U.S.)

- Bristol-Myers Squibb Company (U.S.)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Eli Lilly entered a definitive agreement for the acquisition of Orna Therapeutics.

- January 2026: Eisai and Nuvation Bio entered into an exclusive licensing agreement for Taletrectinib in Europe and additional countries outside the U.S., China and Japan.

- January 2026: The U.S. FDA approved daratumumab and hyaluronidase-fihj (Darzalex Faspro) in combination with bortezomib, lenalidomide, and dexamethasone (VRd) for adults with newly diagnosed multiple myeloma who are ineligible for autologous stem cell transplant (ASCT).

- January 2026: AbbVie and RemeGen announced an exclusive licensing agreement to develop a novel bispecific antibody for advanced solid tumors.

- January 2026: Amgen acquired Dark Blue Therapeutics to strengthen their oncology pipeline, especially for protein degraders.

REPORT COVERAGE

The global oncology drugs market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It comprises of details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of pipeline of key companies, the most common types of cancers and their number of patients, the regulatory and reimbursement scenario, and new product launches. Additionally, it includes data on the partnerships, mergers & acquisitions, as well as key industry developments in the market. The global market forecast report also provides a depth competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 11.77% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Drug Class, Therapy, Indication, Dosage Form, Distribution Channel, and Region |

| By Drug Class |

|

| By Therapy |

|

| By Indication |

|

| By Dosage Form |

|

| By Distribution Channel |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 256.46 billion in 2025 and is projected to reach USD 697.59 billion by 2034.

In 2025, the North America market value stood at USD 116.56 billion.

Growing at a CAGR of 11.77%, the market will exhibit steady growth during the forecast period.

By drug class, the targeted drugs segment is expected to be the leading segment in the market during the forecast period.

The increasing prevalence of cancer and the presence of strong pipeline candidates are major factors driving the growth of the market.

Merck & Co., Inc., AstraZeneca, and Bristol-Myers Squibb Company are major players in the global market.

North America dominated the market share in 2025.

The launch of advanced drug therapies by market players is a key trend in the market.

- 2021-2034

- 2025

- 2021-2024

- 270

-

(Offer valid till 15th Apr 2026)

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us