Counter Rocket, Artillery, and Mortar (C-RAM) Market Size, Share & Industry Analysis, By System Type (Missile-based C-RAM, Gun-based C-RAM, and Others), By Component (Counter-RAM radar, EO/IR and acoustic sensors, FAAD/IBCS-type software, and Others), By Threat Type (Rockets, Mortars, Artillery shells, and Others), By Deployment Mode (Fixed-site, Mobile / deployable, and others), By Application (Military base protection, Airbase protection, Critical infrastructure, and Others), By End User (Army, Air Force, Joint air defense commands, and Others), and Regional Forecast, 2026-2034

Counter Rocket, Artillery, and Mortar (C-RAM) Market Size and Future Outlook

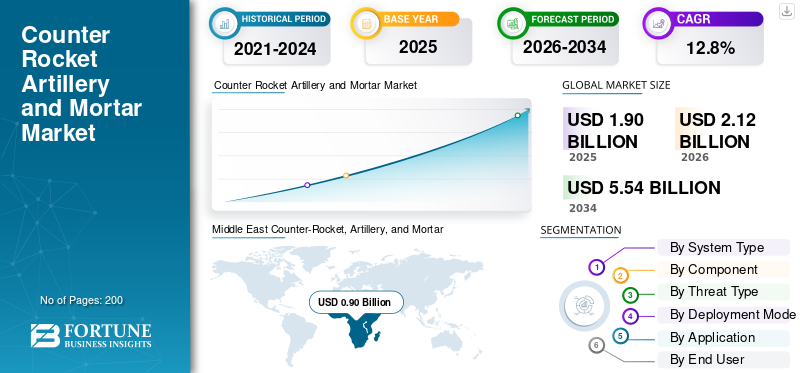

The global counter rocket, artillery, and mortar (C-RAM) market size was valued at USD 1.90 billion in 2025. The market is projected to grow from USD 2.12 billion in 2026 to USD 5.54 billion by 2034, exhibiting a CAGR of 12.8% during the forecast period. Middle East dominated the global market with a market share of 47.37% in 2025.

counter rocket, artillery, and mortar (C-RAM) are integrated weapon systems used to detect, track, warn, and intercept incoming rockets, artillery shells, and mortar rounds before they hit military bases, critical infrastructure, or deployed forces. Unlike broader air defense systems, a RAM system operates within very short reaction windows, making sensor fusion, automated command-and-control, and rapid fire response important. Market growth is being driven by rising rocket artillery and mortar systems threats, drone-enabled targeting, and the need to protect an artillery regiment and forward forces from indirect-fire attacks.

Key players in market include RTX/Raytheon, Northrop Grumman, Rheinmetall, Leonardo DRS, Saab, Thales, Hanwha Aerospace, Kongsberg, and Rafael. These companies are driving the market through advanced radars, command networks, interceptors, cannon-based systems, and directed-energy solutions.

Download Free sample to learn more about this report.

counter rocket, artillery, and mortar (C-RAM) Market Key Takeaways

- 2025 Market Size: USD 1.90 billion

- 2026 Market Size: USD 2.12 billion

- 2034 Forecast Market Size: USD 5.54 billion

- CAGR: 12.8% from 2026–2034

- Middle East dominated the global market with a market share of 47.37% in 2025.

- The Directed-energy C-RAM segment is expected to grow at the highest CAGR of 32.6% over the forecast period.

- The FAAD/IBCS-type software segment is expected to show the fastest growth, registering a CAGR of 17.9% over the forecast period.

Middle East

The region led the global market with 47.37% of total revenue in 2025, driven by sustained investments in advanced air and missile defense systems.

North America

The region accounted for the second-largest market share and is projected to expand at a 11.4% CAGR, supported by increasing deployment of networked and layered C-RAM solutions.

Europe

The market is anticipated to grow at a 15.0% CAGR, fueled by rising investments in short-range air defense systems amid evolving regional security threats.

U.S.

The U.S. market was valued at approximately USD 0.34 billion in 2025 and is expected to grow at a 11.3% CAGR, supported by continuous modernization of air defense capabilities.

Japan

Japan is expected to witness steady demand for C-RAM systems as the country strengthens integrated air and missile defense capabilities to address evolving regional security challenges.

Read More

counter rocket, artillery, and mortar (C-RAM) Market Trends

Convergence of C-RAM and Counter-UAS Capabilities Emerges as a Major Market Trend

Major trend in the market is the shift from standalone mortar C RAM protection toward layered systems that can counter rockets, artillery rounds, mortars, and unmanned aerial threats through the same command-and-control architecture. Moreover, armed forces are no longer treating a RAM system only as a base-defense asset, they are integrating it with short-range air defense systems, electronic warfare, radar networks, and rapid fire interceptors. This trend is important as the modern battlefield now combines rocket artillery and mortar systems fire with drones used for surveillance, targeting, and saturation attacks, prompting air defense artillery units and every forward artillery regiment to adopt faster, networked, and more flexible weapon systems.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Indirect-Fire and Drone-Linked Saturation Threats Drive Market Growth

The primary factor that drives the global counter rocket, artillery, and mortar (C-RAM) market growth is the increasing need for the protection of bases, logistics hubs, airfields, and forward-deployed forces against cheap, mobile, and high-frequency indirect-fire attacks. Rocket artillery and mortar threats remain difficult to neutralize before launch, and drones are making targeting faster, more accurate, and more persistent. This is pushing militaries to invest in layered air defense systems that combine radar, warning networks, rapid fire interceptors, and automated command systems.

MARKET RESTRAINTS

High Sustainment and Integration Costs Restrain Market Growth

The cost of keeping these systems operational and ready for routine deployment is a primary restraint for the market. A RAM system needs sensors, command-and-control, fire-control software, ammunition supply, field service support, training, mobility equipment, and sustainment teams all operating in coordination. This increases the procurement and lifecycle costs, particularly for those nations that require protection of multiple bases, airfields, logistics hubs, or an artillery regiment dispersed across distant locations.

MARKET OPPORTUNITIES

Low-Cost Layered Defense Creates New Growth Opportunities

A major opportunity in the market is the rising demand for lower-cost, layered defense against mixed attacks involving rockets, mortars, artillery rounds, and unmanned aerial threats. Missile-only interception is expensive against cheap drones or repeated rocket artillery and mortar fire, so militaries are actively looking at rapid fire guns, programmable ammunition, directed energy, electronic warfare, and networked sensors as part of a wider RAM system. This opens strong opportunity for companies offering modular weapon systems that can plug into existing air defense systems and support air defense artillery units without forcing customers to rebuild their full defense architecture.

MARKET CHALLENGES

Fast-Evolving Saturation Threats Challenge System Effectiveness

Major challenge in the market is keeping weapon systems effective against mixed, fast-changing attacks where rockets, mortars, artillery rounds, and unmanned aerial threats are used together. A RAM system must identify the threat, calculate impact risk, and respond within seconds, but combined attacks can overload sensors, interceptors, ammunition stocks, and command networks. This creates pressure on air defense artillery units to move beyond single-purpose mortar C-RAM assets and adopt integrated air defense systems that can support rapid fire response, counter rocket artillery, and protection for an artillery regiment in conflict environments.

Impact of Russia-Ukraine and Middle East Conflicts

Russia-Ukraine and Middle East Conflicts Accelerate Demand for Layered C-RAM Protection

The Russia-Ukraine war and Middle East conflicts are directly reshaping the market by proving that modern forces need protection against mixed attacks, not single-threat scenarios. In Ukraine, drones, cruise missiles, rocket artillery and mortar systems, and precision-guided strikes have made lower-tier air defense systems a frontline requirement rather than a rear-area asset. In the Middle East, repeated drone, missile, and indirect-fire threats against bases, ships, and infrastructure are pushing militaries toward layered weapon systems that combine radar, command-and-control, rapid fire effectors, electronic warfare, and mortar C-RAM capability. This conflict environment is increasing demand for deployable RAM system architectures that can support air defense artillery, protect an artillery regiment, and strengthen counter rocket artillery coverage around high-value military and civil assets.

Segmentation Analysis

By System Type

Due to Proven Intercept Reliability, Missile-based C-RAM Dominated System Type Segment

In terms of system type, the market is categorized into missile-based C-RAM, gun-based C-RAM, directed-energy C-RAM, hybrid X layered C-RAM, and warning-only / soft-kill.

Missile-based C-RAM held the largest global counter rocket, artillery, and mortar (C-RAM) market share in 2025, as it provides more engagement capability than gun-only or sensor-only options and is better suited to defeating rockets, artillery shells, mortars, cruise missiles, and some unmanned aerial threats than gun-only or sensor-only configurations. These weapon systems are preferred for high-value base defense, city protection, and layered air defense systems, especially in situations where forces require selective interception of individual threats and do not want to fire at every round detected.

Directed-energy C-RAM segment is expected to grow at a highest CAGR of 32.6% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Component

Due to Multi-Threat Interception Demand, Missile Interceptors Dominated Component Segment

On the basis of component, the market is classified into counter-RAM radar, EO/IR and acoustic sensors, FAAD/IBCS-type software, missile interceptors, gun ammunition, launchers / firing units, and services.

Missile interceptors led the component segment in 2025, as this system is actual kill mechanism in missile-based C-RAM architectures and need recurring procurement, replacement and upgrade cycles. Unlike radars or command systems, interceptors are consumed/destroyed during live engagements, creating sustained demand as militaries build larger stockpiles against rockets, artillery shells, mortars, cruise missiles, and unmanned aerial threats.

FAAD/IBCS-type software segment is expected to show the fastest growth, registering a CAGR of 17.9% over the forecast period.

By Threat Type

Due to High-Frequency Indirect-Fire Threats, Rockets Dominated Threat Type Segment

On the basis of threat type, the market is classified into rockets, mortars, artillery shells, and mixed RAM + UAS.

Rockets segment held the largest market size in 2025, as they are widely used, relatively low-cost, mobile, and capable of creating repeated saturation pressure on military bases, border areas, airfields, cities, and critical infrastructure. Compared with conventional artillery shells and mortars, rocket attacks can be launched in larger salvos and from dispersed positions, making them harder to neutralize before launch. Resulting, many C-RAM and short-range air defense systems are being shaped around rapid detection, threat discrimination, and interceptor availability against rocket-heavy attack profiles.

Mixed RAM + UAS segment is expected to show the fastest growth, registering a CAGR of 21.4% over the forecast period.

By Deployment Mode

Due to Critical Infrastructure and Base Protection Needs, Fixed-site Deployment Dominated Deployment Mode Segment

On the basis of deployment mode, the market is classified into fixed-site, mobile / deployable, containerized/modular, and vehicle-mounted.

The fixed site deployment segment held the largest market share in 2025, as there is an existing high dependence of the C-RAM for protection of air fields, logistic centers, command centers, ammunition storages, border crossings, and any other stationary targets. Continuous monitoring by the radar systems, ready interceptors, reliable energy sources, and a command-and-control center are the features that make fixed site architecture more convenient and effective than the mobile one. Additionally, the fixed site weapon systems can provide better coverage of the areas in case of an attack with rockets and mortars as military operations require permanent air defense systems instead of temporary ones.

Mobile / deployable segment is expected to show the fastest growth, registering a CAGR of 18.6% over the forecast period.

By Application

Due to Persistent Force-Protection Requirements, Military Base Protection Dominated Application Segment

The market is further divided by application, into military base protection, airbase protection, critical infrastructure, border defense, urban defense, naval base defense, and others.

Military base protection segment dominated the market in 2025, as C-RAM was developed specifically for the protection of forward operating bases, airstrips, logistics centers, command posts, and concentration of troops against any form of indirect attack. Military bases are valuable, stationary targets that are susceptible to attacks by rocket artillery, mortar bombardments, mortars, artillery shells, and even unmanned aerial vehicles that conduct surveillance and coordinate attacks. As a result, army prefer to apply C-RAM to fixed and semi-fixed bases before using these weapon systems in a mobile context.

Urban defense segment is expected to show the fastest market growth, registering a CAGR of 17.1% over the forecast period.

By End User

Due to Frontline Force-Protection Requirements, Army Dominated End User Segment

Based on end user, the market is segmented into army, air force, joint air defense commands, homeland/security agencies, and others.

Army dominated the end user segment in 2025, as C-RAM is primarily required where land forces operate, deploy, and sustain combat power. Forward bases, logistics nodes, ammunition areas, command posts, and an artillery regiment are exposed to rocket artillery and mortar fire, artillery rounds, and low-altitude unmanned aerial threats, making the Army the natural lead customer for C-RAM capability.

Joint air defense commands segment is expected to show the fastest market growth, registering a CAGR of 17.4% over the forecast period.

counter rocket, artillery, and mortar (C-RAM) Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Middle East, and rest of the world.

North America

Middle East Counter-Rocket, Artillery, and Mortar (C-RAM) Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America holds the second largest market share for C-RAM solutions, and is anticipated to grow at a CAGR of 11.4% over the forecast period. North America remains a technology-led region in the market, mainly as the U.S. has long operational experience with air defense artillery, LPWS, and layered RAM system architectures. The region’s demand is moving from static base defense toward more deployable, networked weapon systems that can protect fixed and semi-fixed assets against rockets, mortars, cruise missiles, and unmanned aerial threats.

U.S. Counter Rocket, Artillery, and Mortar (C-RAM) Market

Based on the strong contribution of North America to the market and the dominance of U.S. within the region, the U.S. market stood at around USD 0.34 billion in 2025, growing at a CAGR of 11.3% over the forecast period.

Europe

Europe market is anticipated to grow at a second fastest pace with registering a CAGR of 15.0% during the forecast period. The Russia-Ukraine war has exposed the scale of drone, cruise missile, rocket artillery and mortar, and loitering-munition threats against cities, energy infrastructure, airfields, and frontline logistics. Germany, Denmark, Austria, and other European buyers are strengthening short- and very-short-range air defense systems, with strong interest in mobile cannon-missile hybrids and programmable ammunition.

France Counter Rocket, Artillery, and Mortar (C-RAM) Market

France market reached approximately USD 0.02 billion in 2025, anticipated to grow at the CAGR of 16.2% during the forecast period.

Asia Pacific

Asia Pacific is anticipated to grow at a CAGR of 18.5% over the forecast period. Region, led by South Korea’s need to defend Seoul and critical military facilities against North Korean long-range artillery, rockets, and missiles. The region’s C-RAM demand is not uniform, but the threat picture is noticeable, Korean Peninsula artillery risk, Taiwan Strait tensions, Indian border and air-base protection requirements, and wider counter-drone modernization are pushing governments toward layered counter rocket artillery and short-range air defense solutions. South Korea is the clearest C-RAM-linked case. In January 2025, DAPA held the kickoff meeting for the LAMD system development project, widely described as a “Korean Iron Dome,” intended to protect the capital region’s key national and military facilities from simultaneous North Korean long-range artillery threats.

China Counter Rocket, Artillery, and Mortar (C-RAM) Market

The Chinese market revenues stood at around USD 0.04 billion in 2025, anticipated to grow at the CAGR of 17.0% during the forecast period.

South Korea Counter Rocket, Artillery, and Mortar (C-RAM) Market

The South Korean market stood at around USD 0.07 billion in 2025, accounting for roughly 31.84% of Asia Pacific revenues.

Middle East

The Middle East dominates the regional segment and is anticipated to grow at a CAGR of 10.1% over the forecast period, as the region has one of the highest operational needs for C-RAM protection across military bases, border zones, energy infrastructure, ports, and population centers. Repeated rocket artillery and mortar attacks, drone strikes, missile threats, and proxy-force activity have pushed Israel, Saudi Arabia, the UAE, and Iraq to strengthen layered air defense systems. The region’s demand is not limited to one RAM system type, buyers are investing in missile interceptors, rapid fire guns, radars, command networks, and counter-unmanned aerial solutions. This makes the Middle East a leading market for air defense artillery, mortar C-RAM, and broader counter rocket artillery protection.

Israel Counter Rocket, Artillery, and Mortar (C-RAM) Market

The Israel market revenues stood at around USD 0.31 billion in 2025, and is anticipated to grow at the CAGR of 9.1% during the forecast period.

Saudi Arabia Counter Rocket, Artillery, and Mortar (C-RAM) Market

The Saudi Arabia market stood at around USD 0.18 billion in 2025, accounting for roughly 19.82% of Middle East revenues.

Rest of the World

Rest of the World (Africa and Latin America) holds a comparatively smaller market share but is expected to grow at a 14.9% CAGR during the forecast period. Africa’s demand is stronger in North Africa, the Sahel, and the Horn of Africa, where drones, rockets, and mortar threats are becoming more visible, while Latin America is moving mainly through counter-UAS procurement and broader air defense artillery modernization.

Latin America Counter Rocket, Artillery, and Mortar (C-RAM) Market

The market in Latin America reached around USD 0.04 billion in 2025 and is anticipated to grow at the CAGR of 13.6% during the forecast period.

Africa Counter Rocket, Artillery, and Mortar (C-RAM) Market

Africa’s market stood at around USD 0.06 billion in 2025 and is expected to reach USD 0.21 billion in 2034.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Industry Players Strengthen Market through Layered and Networked C-RAM Solutions

The global counter rocket, artillery, and mortar (C-RAM) market is dominated by players with the ability to integrate radars, interceptors, rapid fire guns, command systems and counter unmanned aerial capabilities into a layered defense architecture. Key players include RTX/Raytheon, Rafael, Northrop Grumman, Rheinmetall, Leonardo DRS, Saab, Thales, Hanwha Aerospace and Kongsberg. RTX/Raytheon and Rafael remain strong players in missile based RAM system solutions while Northrop Grumman supports networked air defense systems through IBCS.

Competition is shifting from standalone weapon systems to modular, connected solutions that can counter rocket, artillery, and mortar attacks, drones, artillery rounds, and cruise missiles together. Rheinmetall’s Skynex and Skyranger families reflect this trend through cannon-based air defense artillery and programmable ammunition, while Leonardo DRS and others are expanding into directed energy and electronic-warfare options.

LIST OF KEY counter rocket, artillery, and mortar (C-RAM) COMPANIES PROFILED IN REPORT

- RTX Corporation / Raytheon (U.S.)

- Lockheed Martin Corporation (U.S.)

- Northrop Grumman Corporation (U.S.)

- Leonardo S.p.A. (Italy)

- Thales Group (France)

- MBDA (France)

- Saab AB (Sweden)

- Kongsberg Gruppen ASA (Norway)

- Rafael Advanced Defense Systems Ltd. (Israel)

- Rheinmetall AG (Germany)

- Hanwha Aerospace Co., Ltd. (South Korea)

- ASELSAN A.Ş. (Turkey)

- Elbit Systems Ltd. (Israel)

- BAE Systems plc (U.K.)

- KNDS N.V. (Netherlands)

KEY INDUSTRY DEVELOPMENTS

- November 2025: Raytheon-Rafael Protection Systems received a USD 1.25 billion contract to supply Israel with Tamir surface-to-air missiles for the Iron Dome Weapon System, including missiles, missile kits, and test equipment.

- June 2025: The U.S. Department of War awarded Raytheon a USD 279.20 million contract to provide functional management support for the Land-Based Phalanx Weapon System, a key C-RAM capability used for protection against rockets, artillery, and mortar threats.

- January 2025: South Korea’s Defense Acquisition Program Administration formally launched development of the Low-Altitude Missile Defense system, known as the Korean Iron Dome, to counter North Korean long-range artillery threats. The program value was reported at about USD 329.00 million through 2028.

- November 2024: The U.S. Army awarded Dynetics, Inc. an Indirect Fire Protection Capability Increment 2 contract valued at up to USD 4.10 billion. The initial procurement covers 18 IFPC Inc. 2 launchers, supporting layered defense for forward operating bases and critical infrastructure.

- October 2024: RTX’s Raytheon demonstrated KuRFS radar and Coyote Block 2 and Block 3 effectors against complex unmanned aerial threats during U.S. Army testing at Yuma Proving Ground. RTX stated that recent U.S. Army LIDS contracts totaled USD 374.80 million, supporting integrated counter-UAS and C-RAM-style base defense capability.

- July 2024: South Korea’s Defense Acquisition Program Administration started mass production of the Laser-Based Anti-Aircraft Weapon Block-I with Hanwha Aerospace. The contract was worth about USD 72.00 million, supporting low-cost counter-drone defense as part of layered short-range air defense modernization.

- February 2024: Rheinmetall received a Bundeswehr order for Skyranger 30 mobile air defense systems on Boxer vehicles. The contract was valued at approximately USD 645.00 million, covering one prototype and 18 series-production vehicles, with an option for 30 more systems.

- December 2022: Rheinmetall received an order from an international customer for two Skynex air defense systems worth approximately USD 205.00 million. Deliveries were scheduled for early 2024, supporting modular cannon-based air defense against aerial threats.

REPORT COVERAGE

The global counter rocket, artillery, and mortar (C-RAM) market analysis provides an in-depth study of market size, market segmentation, company profiling & forecast by all the market segments included in the report. It includes details on the market dynamics and trends that are expected to drive the market during the forecast period. It offers information on the technological advancements, new product launches, key industry expert’s developments, and details on strategic partnerships, mergers & acquisitions. The market research report also encompasses detailed competitive landscape with information on the market share and profiles of market key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 12.8% from 2026 to 2034 |

| Unit | Value (USD Billion) |

|

Segmentation

|

By System Type

|

|

By Component

|

|

|

By Threat Type

|

|

|

By Deployment Mode

|

|

|

By Application

|

|

|

By End User

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stands at USD 2.12 billion in 2026 and is projected to reach USD 5.54 billion by 2034.

In 2025, the Middle East market value stood at USD 0.90 billion.

The market is expected to exhibit a CAGR of 12.8% during the forecast period.

Missile-based C-RAM led the market by system type.

Rising indirect-fire and drone-linked saturation threats drive market growth.

Key players in the market include RTX Corporation, Northrop Grumman Corporation, Lockheed Martin Corporation, Leonardo DRS, Inc., Rafael Advanced Defense Systems Ltd., Rheinmetall AG, Saab AB, Thales Group, Kongsberg Gruppen ASA, Hanwha Aerospace Co., Ltd., ASELSAN A.Ş., Elbit Systems Ltd., MBDA, BAE Systems plc, and KNDS N.V.

Middle East held the largest share of the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us