Foot and Ankle Devices Market Size, Share & Industry Analysis, By Product Type (Fixation Devices {Plates, Screws, Staples, Intramedullary Nails, Pins & Wires, and External Fixators}, Joint Replacement Devices {Total Ankle Replacement Systems, Partial Ankle Replacement Systems, & Toe Joint Replacement Systems}, Orthobiologics {Demineralized Bone Matrix, Synthetic Bone Substitutes, Bone Growth Factors, & Others}, Bracing & Support Devices, & Other), By Application (Trauma & Fractures, Osteoarthritis & Rheumatoid Arthritis, Sports Injuries, & Others), By End-user, & Regional Forecast, 2026-2034

Foot and Ankle Devices Market Size and Future Outlook

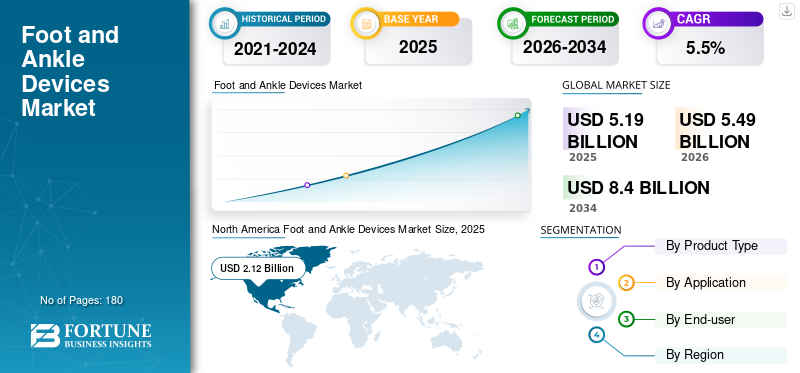

The global foot and ankle devices market size was valued at USD 5.19 billion in 2025. The market is projected to grow from USD 5.49 billion in 2026 to USD 8.40 billion by 2034, exhibiting a CAGR of 5.5% during the forecast period. North America dominated the foot and ankle devices market with a market share of 40.84% in 2025.

The foot and ankle devices market covers implants and tools used to treat fractures, deformities, tendon/ligament injuries, arthritis, and diabetic foot complications. It spans fixation hardware, such as plates, screws, staples, nails, pins/wires, external fixators, joint replacement systems, and select orthobiologics used to support fusion/reconstruction, as well as bracing and procedure-support equipment. Growth is being fueled by rising surgical volumes from trauma and sports injuries, an aging population with degenerative joint disease, and increasing diabetes-related foot complications. Technology upgrades are also nudging adoption, and surgeons increasingly expect better planning, alignment, and reproducibility in complex cases.

Furthermore, Arthrex, Stryker, Zimmer Biomet, Johnson & Johnson, and Smith+Nephew holds the leading market share, driven by growing investments and strategic initiatives, including new product launches, collaborations, and partnerships.

Download Free sample to learn more about this report.

Foot and Ankle Devices Market Key Takeaways

- 2025 Market Size: USD 5.19 billion

- 2026 Market Size: USD 5.49 billion

- 2034 Forecast Market Size: USD 8.40 billion

- CAGR: 5.5% from 2026–2034

- North America dominated the foot and ankle devices market with a 40.84% share in 2025.

- Fixation devices held the largest market share due to their broad usage across trauma, fractures, and deformity correction procedures.

- Hospitals & ASCs accounted for a leading 67.3% market share in 2026 owing to high surgical procedure volumes.

North America

North America was valued at USD 2.12 Billion in 2025.

Europe

Europe is projected to reach USD 1.50 Billion in 2026.

Asia Pacific

Asia Pacific is projected to reach USD 1.22 Billion in 2026.

U.S.

The U.S. market is projected to reach USD 2.02 Billion in 2026.

Japan

The Japan market is projected to reach USD 0.20 Billion in 2026.

Read More

FOOT AND ANKLE DEVICES MARKET TRENDS

Precision Planning and Navigation Systems Move into Foot & Ankle Surgeries Likely to Boost Market Trend

Foot and ankle surgery is increasingly adopting the playbook already seen in large joints, which is better in preoperative planning, patient-specific tools, and intraoperative guidance to improve alignment and execution, especially in ankle arthroplasty and complex deformity cases. A visible trend is the spread of planning-to-execution platforms that tie imaging and templating to guides or navigation. Navigation also involves entering the category in a more procedure-specific way and providing real-time guidance to a joint that historically relied heavily on surgeon experience and conventional jigs.

Another significant trend is system consolidation in surgeon preference; many surgeons and hospitals increasingly prefer a single coherent platform rather than piecemeal SKUs. This encourages suppliers to refresh portfolios with compatible instruments, minimally invasive options, and standardized technique kits to support repeatable outcomes. Over time, this trend tends to lift the share of premium constructs within fixation and replacement, while also increasing the importance of education, service, and procedural support as differentiators.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rise in Procedure Due to Trauma, Diabetes, and Elective Reconstruction to Fuel the Market Growth

A key driver is the steady expansion of the addressable patient pool across both urgent and elective indications. Trauma remains a foundational demand engine, and road traffic injuries continue to generate a high burden of lower-extremity fractures. The World Health Organization notes that 92% of global road fatalities occur in low- and middle-income countries, even though these countries have around 60% of the world’s vehicles, which is an indicator of persistent trauma volume and downstream reconstructive need. At the same time, diabetes is reshaping complex foot and ankle caseloads. The IDF’s latest global factsheet in 2024 highlights 589 million adults living with diabetes globally, with a large share in lower-resource settings, conditions that often correlate with diabetic foot ulcers, Charcot changes, and higher-intensity reconstruction/fusion pathways.

Elective and semi-elective procedures are also becoming more standardized and systematized, which supports the predictable use of fixation, soft-tissue repair constructs, and orthobiologic adjuncts. Manufacturers continue to reinforce this driver through system-based innovation, highlighting continued investment in precision planning and instrumentation to broaden surgeon adoption.

MARKET RESTRAINTS

Reimbursement Pressure and Affordability Gaps to Restrain Market Growth

Reimbursement and affordability constraints remain major restraints, particularly as markets move beyond basic fixation into premium implants, navigation, and patient-specific solutions. In many systems, hospitals operate under bundled or tightly controlled payments, where implants are an extensive, visible cost line; that environment can slow upgrades to newer constructs, limit the use of orthobiologics, and delay adoption of enabling technologies that lack clear payment pathways. The challenge is amplified in public tenders where the lowest compliant bid can dominate purchasing, compressing prices and discouraging broad portfolio diversification.

Another constraint is that foot and ankle care is not always one-size-fits-all. Deformity correction, Charcot reconstruction, and revision surgery can require costly, highly customized implant strategies and skilled teams; outside major centers, access to that expertise can be uneven, which limits the addressable market for advanced systems. Even in developed markets, the incremental benefit of premium solutions must be proven in outcomes and workflow efficiency before procurement teams will approve widespread rollouts. The market’s push toward navigation and planning illustrates this tension, showing innovation momentum, but scaling these platforms broadly depends on cost justification, training, and purchasing models.

MARKET OPPORTUNITIES

Enabling Tech, Minimally Invasive Workflows, and Outpatient Shift to Create Significant Market Opportunities

A clear opportunity is the convergence of enabling technologies, such as planning, navigation, and patient-specific instrumentation, with minimally invasive, outpatient-friendly procedure design. As more foot and ankle interventions shift to ambulatory settings, stakeholders value tools that reduce intraoperative variability, shorten procedure time, and improve reproducibility, especially for technically demanding procedures such as reconstruction and ankle arthroplasty. This creates whitespace for integrated ecosystems that combine implants, instrumentation, and software-driven planning.

Another opportunity is the continuing evolution of bunion and midfoot correction into more instrumented, standardized approaches. Companies are building platforms based on reproducible 3D correction concepts to increase the utilization of dedicated fixation constructs and support tools.

Finally, emerging markets offer opportunity through access expansion rather than pure pricing: as trauma and diabetes burdens rise and surgical capacity improves, demand for reliable fixation, external stabilization, and reconstruction toolkits can scale quickly, particularly when suppliers tailor pricing tiers and training programs to local procurement realities.

MARKET CHALLENGES

Training Intensity, Evidence Expectations, and Uneven Access to Create Challenges in the Market

Foot and ankle is a technically demanding orthopedic subspecialty, and that creates practical scaling challenges. Many high-value procedures, such as ankle replacement, complex deformity reconstruction, and Charcot recon, require specialized training and consistent case volume to achieve predictable outcomes. When access to experienced surgeons is concentrated in urban referral centers, adoption of advanced systems can lag in smaller hospitals, even if patient demand exists.

A second challenge is evidence and procurement scrutiny. Hospitals increasingly expect clear clinical and economic justification for premium implants, navigation, and orthobiologic adjuncts, particularly where reimbursement is bundled or constrained. That means suppliers must invest in training, outcomes data, and workflow proofs, not just device innovation.

The foot and ankle devices market is exposed to macro injury drivers that are unevenly distributed geographically. Still, those same settings may face constraints in surgical capacity and device affordability, creating a paradox of high need yet slower monetization.

Finally, diabetes prevalence is rising globally, which increases the pool of patients at risk for complex foot problems. Still, these cases can be resource-intensive, requiring multidisciplinary care pathways and specialized implants that are not evenly available across regions.

Segmentation Analysis

By Product Type

Wide Adoption of Fixation Devices in Several Foot and Ankle Procedures to Drive the Segment Growth

Based on product type, the market is segmented into fixation devices, joint replacement devices, orthobiologics, bracing & support devices, and other foot & ankle devices. Further, fixation devices are segmented into plates, screws, staples, intramedullary nails, pins & wires, and external fixators. Moreover, joint replacement devices are segmented into total ankle replacement systems, partial ankle replacement systems, and toe joint replacement systems. Additionally, orthobiologics are segmented into demineralized bone matrix (DBM), synthetic bone substitutes, bone growth factors, and others.

To know how our report can help streamline your business, Speak to Analyst

Fixation devices hold the largest market share as they serve the broadest set of indications, including ankle and foot fractures, osteotomies for bunion/deformity correction, and most fusion constructs, that rely on plates, screws, staples, and pins/wires. Compared with ankle replacement, fixation is used across both urgent trauma and high-volume elective forefoot procedures, and it is purchased in virtually every orthopedic setting from tertiary centers to community hospitals. Trauma burden remains a structural tailwind, as road traffic injuries continue to drive global demand for fracture fixation.

Additionally, the joint replacement devices segment is projected to grow at a CAGR of 8.5% during the forecast period.

By Application

Immediate Surgical Demand in Trauma and Fracture Cases Leads to Segmental Growth

By application, the market is classified into trauma & fractures, osteoarthritis & rheumatoid arthritis, sports injuries, diabetic foot disorders, congenital & acquired deformities, and others.

Trauma and fractures account for the largest foot and ankle devices market share as they generate immediate surgical demand and consistent utilization of core implants, such as plates, screws, nails, and external fixators, with less reliance on discretionary reimbursement than elective reconstruction. Ankle fractures and mid-foot injuries are common in falls, sports, and traffic-related trauma. Moreover, the segment is projected to hold a 38.4% share in 2026.

Additionally, the diabetic foot disorders segment is estimated to grow at a CAGR of 7.6% during the forecast period.

By End-user

Growing Outpatient Pipeline Performed in Hospitals & ASCs to Propel the Segment Growth

Based on end user, the market is classified into hospitals & ASCs, specialty orthopedic clinics, trauma centers, and others.

Hospitals and ASCs dominate the market share, capturing both ends of the case mix: high-acuity trauma and a growing outpatient pipeline of bunion correction, ligament repair, and certain fusions performed in ASCs. As enabling technologies mature, ASCs are becoming increasingly relevant for standardized elective procedures that benefit from efficient workflows. Furthermore, the segment is set to hold a 67.3% share in 2026.

In addition, the specialty orthopedic clinics segment is projected to grow at a CAGR of 9.6% during the forecast period.

Foot and Ankle Devices Market Regional Outlook

Based on region, the market is classified into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Foot and Ankle Devices Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the largest revenue share in 2024, at USD 2.00 billion, and accounted for USD 2.12 billion in 2025. The growth in North America is supported by a large and steady procedural base spanning trauma fixation, elective forefoot correction, sports-medicine repairs, and complex reconstruction. The region also benefits from well-established ambulatory surgery and orthopedic care pathways, which help maintain high case throughput and support the continued shift of suitable procedures to ASCs. Chronic disease adds another layer of demand: diabetes increases the risk of diabetic foot complications and complex fusion/reconstruction cases.

U.S Foot and Ankle Devices Market

In 2026, the U.S. market is projected to reach USD 2.02 billion, set to capture 36.8% of total global revenue.

Europe

Europe is expected to achieve a 4.4% growth rate during the forecast period, the second-highest globally, and is set to reach USD 1.50 billion by 2026. Europe’s growth is shaped by demographics and a broad trauma-and-degenerative disease mix, with aging populations increasing the incidence of arthritis, deformity, and fragility fractures that require fixation, fusion, or selected joint replacement interventions. In higher-adoption markets, the ankle arthroplasty segment is also expanding as planning and instrumentation improve, contributing incremental growth in a category that historically relied heavily on fixation and fusion.

U.K Foot and Ankle Devices Market

The U.K. market is projected to reach USD 0.21 billion by 2026, set to account for 3.8% of the global market revenue.

Germany Foot and Ankle Devices Market

Germany's market is forecasted to reach USD 0.30 billion by 2026, set to represent roughly 5.4% of global revenue.

Asia Pacific

In 2026, the Asia Pacific foot and ankle devices market is expected to be valued at USD 1.22 billion, ranking third globally. Asia Pacific is typically the fastest-growing region in volume terms, owing to expanding healthcare capacity and access, particularly in large markets such as China, India, and parts of Southeast Asia, which bring more patients into surgical care for fractures, deformities, and sports-related injuries. The region also faces a rapidly rising chronic disease load that increases the severity and complexity of foot and ankle caseloads.

Japan Foot and Ankle Devices Market

Japan is projected to generate USD 0.20 billion in revenue by 2026, accounting for nearly 3.7% of the global market.

China Foot and Ankle Devices Market

China’s market is forecast to reach USD 0.37 billion by 2026, accounting for about 6.7% of global revenues.

India Foot and Ankle Devices Market

India is expected to reach USD 0.13 billion in the market by 2026, corresponding to about 2.3% of global revenues.

Latin America and the Middle East & Africa

Both Latin America and the Middle East & Africa are anticipated to witness moderate foot and ankle devices market growth, with Latin America expected to reach around USD 0.27 billion by 2026. Latin America’s growth is driven by a catch-up dynamic in orthopedic access, where expanding capacity in urban hospitals and the private sector translates into higher procedure volumes for trauma fixation, elective corrections, and sports-injury repairs. The region’s growth profile is also reinforced by the expanding diabetes burden, which can shift the case mix toward more complex diabetic foot and reconstruction pathways that are typically more device-intensive per procedure. The growth in the Middle East and Africa is largely driven by the combination of high underlying need and incremental expansion of surgical capacity, meaning that even modest improvements in access can translate into relatively high percentage growth from a smaller base.

GCC Foot and Ankle Devices Market

By 2026, the GCC is expected to generate USD 0.07 billion in the market, accounting for nearly 1.2% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Robust Product Innovation to Reinforce the Market Position of Prominent Players

The global foot and ankle devices market is moderately consolidated at the top, with large orthopedic multinationals such as Arthrex, Stryker, Zimmer Biomet, Johnson & Johnson, and Smith+Nephew competing alongside specialists that win share through depth in surgeon relationships, procedure-specific systems, and focused innovation.

Moreover, Other key players, such as Enovis, Össur, Ottobock, and Acumed, compete through ongoing technological developments, the growing demand for improved healthcare infrastructure, and efforts to improve therapy outcomes.

LIST OF KEY FOOT AND ANKLE DEVICES COMPANIES PROFILED

- Arthrex (U.S.)

- Stryker (U.S.)

- Zimmer Biomet (U.S.)

- Johnson & Johnson (U.S.)

- Smith+Nephew (U.K.)

- Enovis (U.S.)

- Össur (Iceland)

- Ottobock (Germany)

- Acumed (U.S.)

- Bauerfeind (Germany)

KEY INDUSTRY DEVELOPMENTS

- January 2026: Zimmer Biomet Holdings, Inc., together with its wholly owned subsidiary Paragon 28, announced the commercial launch of the Brachiator Mini-Rail External Fixation System, a platform designed for precise, multi-planar correction, rapid construct assembly, and workflow efficiency for the correction of bone deformities and stabilization of fractures of the foot and ankle.

- October 2025: Zimmer Biomet Holdings, Inc. and Paragon 28, a wholly owned subsidiary, announced the full commercial launch of two innovative solutions for complex foot and ankle trauma to offer surgeons advanced tools to address challenging pilon fractures and hindfoot injuries with precision and efficiency.

- April 2025: Zimmer Biomet Holdings, Inc. announced it has completed the acquisition of Paragon 28, Inc., a leading medical device company focused exclusively on the fast-growing foot and ankle orthopedic industry.

- October 2024: Paragon 28, Inc. announced the addition of a novel Right-Angle Drill to the APEX 3D Total Ankle Replacement System, designed to improve tibia preparation before the implantation of the APEX 3D tibia implant.

- September 2024: 3D Systems announced the Food and Drug Administration (FDA) has provided 510(k) clearance for TOTAL ANKLE Patient-Matched Guides to be used with Smith+Nephew’s SALTO TALARIS Total Ankle Prosthesis and CADENCE Total Ankle System.

- February 2024: Paragon 28 announces the launch of the PRECISION MIS Bunion System, which allows surgeons to complete a distal metatarsal osteotomy using a minimally invasive (MIS) surgical technique.

- January 2024: Stryker announced the launch of Prophecy Footprint, an expansion of the Prophecy Surgical Planning system that offers comprehensive surgical planning across the entire foot.

REPORT COVERAGE

The report provides an in-depth analysis of all market segments, highlighting key drivers, trends, opportunities, restraints, and challenges. It also provides insights into technological advancements, key industry developments, company market share analysis, and profiles of leading companies.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.5% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product, Application, End-user, and Region |

| By Product Type |

|

| By Application |

|

| By End-user |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 5.19 billion in 2025 and is projected to reach USD 8.40 billion by 2034.

In 2025, the market value stood at USD 2.12 billion.

The market is expected to grow at a CAGR of 5.5% over the forecast period.

The fixation devices segment led the market by product type.

The key factors driving the market are the rising number of procedures for trauma, diabetes, and elective reconstruction.

Arthrex, Stryker, Zimmer Biomet, Johnson & Johnson, and Smith+Nephew are some of the major players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us