Hydrogen Liquefaction Equipment Market Size, Share & Industry Analysis, By Equipment Type (Compressors, Cryogenic Heat Exchangers, Turboexpanders, Refrigeration Systems, Cryogenic Pumps, and Others (Cold Boxes, Valves, & Insulation Systems)), By Liquefaction Technology (Claude Cycle, Brayton Cycle, Mixed Refrigerant Cycle, and Helium-Based Liquefaction), By Plant Capacity (Scale (<10 TPD to >50 TPD)), By End-Use Industry (Hydrogen Production & Liquefaction Plants, Energy & Power, Transportation, Refining & Petrochemicals, Chemicals, and Aerospace & Defense) and Regional Forecast, 2026-2034

Hydrogen Liquefaction Equipment Market Size and Future Outlook

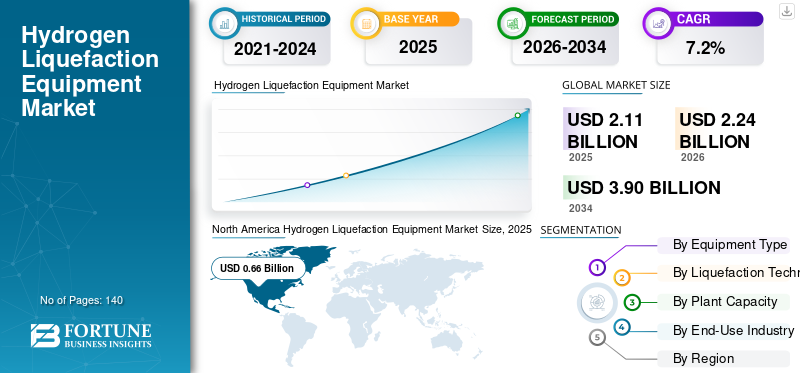

The global hydrogen liquefaction equipment market size was valued at USD 2.11 billion in 2025. The market is projected to grow from USD 2.24 billion in 2026 to USD 3.90 billion by 2034, exhibiting a CAGR of 7.2% during the forecast period. North America dominated the hydrogen liquefaction equipment market with a market share of 31.27% in 2025.

Hydrogen liquefaction equipment comprises specialized cryogenic systems designed to convert gaseous hydrogen into liquid form by cooling it to extremely low temperatures (approximately −253°C), enabling efficient storage and distribution, transportation, and large-scale industrial utilization. As hydrogen increasingly emerges as a key clean energy source and energy carrier, the market is witnessing steady growth, driven by rising demand for clean hydrogen, increasing investments in hydrogen infrastructure, and the global transition toward low-carbon energy systems across key regions, including Asia Pacific and North America. These systems are widely deployed across large-scale hydrogen production facilities, export terminals, and industrial hydrogen supply chains to ensure efficient handling and transport of hydrogen over long distances for energy, mobility, and industrial applications. They play a vital role in improving hydrogen energy density, optimizing logistics efficiency, and supporting compliance with stringent decarbonization and emission reduction targets. Current market trends indicate increasing adoption of advanced storage technologies and energy-efficient liquefaction processes such as mixed refrigerant and cryogenic cycles, along with integration of renewable energy sources such as solar and wind to reduce the overall carbon footprint of hydrogen production. The development of large-scale hydrogen export projects, supported by joint ventures and cross-border collaborations, is strengthening global supply chains and accelerating market expansion. Additionally, the growing adoption of hydrogen in mobility applications, including fuel cell electric vehicles and marine transport, is further driving equipment demand. Industry participants are increasingly focusing on lowering energy consumption, improving process efficiency, and enhancing system reliability to address the high operational intensity associated with hydrogen liquefaction, while enabling scalable deployment across evolving hydrogen ecosystems.

- For instance, in March 2026, Siemens Energy AG announced the deployment of advanced hydrogen liquefaction and cryogenic process technologies for a large-scale hydrogen infrastructure project in Europe. The initiative is aimed at improving energy efficiency and enabling a scalable low-carbon hydrogen supply for industrial and energy applications.

Air Liquide S.A., Linde plc, Air Products and Chemicals, Inc., Chart Industries, Inc., Mitsubishi Heavy Industries, Ltd., and Kawasaki Heavy Industries, Ltd. are among the key players holding a significant share of the market. Their competitive positioning is strengthened by strong expertise in cryogenic engineering and hydrogen processing technologies, the ability to deliver large-scale and application-specific liquefaction solutions, extensive global project execution capabilities, and continuous innovation in energy-efficient and low-emission hydrogen liquefaction systems to support the evolving hydrogen economy.

Download Free sample to learn more about this report.

HYDROGEN LIQUEFACTION EQUIPMENT MARKET TRENDS

Rising Adoption of Advanced Cryogenic Technologies is a key Market Trend

Demand for hydrogen liquefaction equipment is increasingly being influenced by the growing need for energy efficiency and the ability to operate under variable and intermittent energy input conditions across modern hydrogen production ecosystems. With the rising integration of renewable energy sources such as solar and wind in green hydrogen production, operators are focusing on deploying liquefaction systems capable of handling fluctuating power availability while maintaining optimal performance. This is driving the adoption of advanced cryogenic technologies, mixed refrigerant cycles, and modular liquefaction systems that can operate efficiently under partial loads and variable operating conditions. Unlike traditional large-scale continuous liquefaction systems, there is a growing emphasis on equipment that can support flexible operation, including load variation, intermittent operation, and rapid system adjustments without significant efficiency losses. Additionally, project developers are prioritizing systems that minimize energy consumption, enhance thermodynamic efficiency, and reduce overall operational costs, given the energy-intensive nature of hydrogen liquefaction processes.

- For instance, in March 2025, Air Products and Chemicals, Inc. announced continued construction progress of the NEOM Green Hydrogen Project in Saudi Arabia. This project includes large-scale hydrogen production and liquefaction infrastructure to enable global export of green hydrogen using advanced cryogenic technologies.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Emergence of Cross-Border Hydrogen Trade Corridors to Accelerate Product Demand

The hydrogen liquefaction equipment market is increasingly being shaped by the emergence of cross-border hydrogen trade corridors and the development of export-oriented hydrogen economies. Unlike conventional energy markets, hydrogen requires specialized cryogenic infrastructure to enable long-distance transportation, particularly in liquid form, making liquefaction a critical enabler of global hydrogen trade. Countries with abundant renewable resources, such as those in the Middle East and Oceania, are investing heavily in large-scale hydrogen production facilities integrated with liquefaction systems to support exports to major demand centers in Europe and Asia. This trend is driving demand for high-capacity, energy-efficient liquefaction equipment capable of operating at an industrial scale while maintaining process stability and minimizing energy losses. The increasing complexity of hydrogen supply chains, including storage, marine transport, and regasification, is further reinforcing the need for advanced liquefaction technologies that ensure consistent product quality and operational reliability. As a result, equipment manufacturers are focusing on developing systems with enhanced thermal efficiency, improved refrigeration cycles, and modular configurations suitable for deployment across geographically diverse projects.

- For instance, in Jan 2026, Kawasaki Heavy Industries, Ltd. announced the continued development of its liquid hydrogen supply chain infrastructure, including liquefaction and transport systems. The initiative is aimed at supporting large-scale hydrogen exports between Australia and Japan.

MARKET RESTRAINTS

Thermodynamic Efficiency Limits and Lack Of Standardized Liquefaction Technologies Across Regions to Hinder Market Expansion

The hydrogen liquefaction equipment market growth is significantly constrained by the inherent thermodynamic challenges associated with liquefying hydrogen, which requires extremely low temperatures and results in substantial energy consumption. Unlike other industrial gases, hydrogen has a low boiling point and high specific energy requirements for liquefaction, leading to an energy penalty that can account for a significant portion of the overall hydrogen production cost. This high energy intensity increases operational expenditure and raises concerns regarding the overall efficiency and sustainability of hydrogen supply chains, particularly when electricity is sourced from non-renewable energy systems. Furthermore, achieving high liquefaction efficiency requires complex multi-stage refrigeration cycles and advanced cryogenic engineering, which increases system complexity and capital costs. Any inefficiencies in process design or operational performance can lead to boil-off losses and reduced system reliability, impacting the economic feasibility of large-scale projects. In addition, the lack of standardized liquefaction technologies across regions creates challenges in scaling and replicating projects efficiently, leading to longer development timelines and higher project risks. These technical and economic constraints continue to limit the widespread adoption of the product, particularly in cost-sensitive markets and early-stage hydrogen economies.

MARKET OPPORTUNITIES

Emergence of Liquid Hydrogen Trade and Maritime Transport Infrastructure Creating New Growth Avenues

An emerging opportunity in the hydrogen liquefaction equipment market lies in the rapid development of liquid hydrogen (LH₂) trade routes and the expansion of maritime transport infrastructure designed for long-distance hydrogen movement. As hydrogen transitions from a localized industrial input to a globally traded energy commodity, liquefaction is becoming essential for enabling efficient bulk transport across continents. This is creating strong demand for large-scale, export-oriented liquefaction facilities integrated with port infrastructure, storage terminals, and specialized shipping systems. Countries with abundant renewable resources are actively investing in hydrogen export hubs, driving the need for high-capacity and energy-efficient liquefaction equipment capable of supporting continuous and large-volume operations.

- For instance, in November 2024, Linde plc announced the expansion of its hydrogen liquefaction capabilities at its U.S. Gulf Coast facilities. The project is aimed at increasing liquid hydrogen production capacity to support growing demand from mobility and industrial sectors.

MARKET CHALLENGES

Boil-Off Losses and Cryogenic Storage Limitations Impact Operational Efficiency

A key challenge in the hydrogen liquefaction equipment market is managing boil-off losses and maintaining cryogenic stability during storage and transportation. Since hydrogen must be kept at extremely low temperatures in liquid form, even minor heat ingress can lead to evaporation losses, directly affecting overall system efficiency and economic viability. This challenge becomes more critical in large-scale storage and long-distance transport scenarios, where maintaining consistent cryogenic conditions over extended periods is technically demanding. To address these challenges, operators must invest in advanced insulation systems, high-performance storage tanks, and continuous monitoring solutions, which significantly increase both capital and operating costs. Furthermore, the lack of standardized infrastructure and varying design specifications across regions creates additional complexity in scaling liquefaction and storage systems. Differences in safety regulations, material standards, and handling protocols can lead to inconsistencies in system performance and longer project development timelines. Moreover, the need for highly specialized materials and components capable of withstanding extreme cryogenic conditions limits supplier availability and increases dependency on a small number of established manufacturers.

Segmentation Analysis

By Equipment Type

Compressors Segment Led as It Represents the Core Component of Hydrogen Liquefaction Processes

By equipment type, the market is segmented into compressors, cryogenic heat exchangers, expanders/turboexpanders, refrigeration systems, cryogenic pumps, and others (cold boxes, valves, and insulation systems).

Compressors held the largest market share as they represent the primary component responsible for hydrogen gas compression prior to liquefaction, making them fundamental to the overall liquefaction process. These systems play a critical role in increasing hydrogen pressure across multiple stages of the liquefaction cycle, enabling efficient cooling and phase transformation under cryogenic conditions. Due to the low density and high diffusivity of hydrogen, compression is a highly energy-intensive and technically demanding process, which further reinforces the importance of high-performance compressor systems across large-scale hydrogen production facilities, export terminals, and industrial hydrogen supply chains.

- For instance, in June 2024, Atlas Copco announced the expansion of its hydrogen compression solutions portfolio, focusing on high-efficiency compressor systems designed for large-scale hydrogen applications, including liquefaction and storage infrastructure.

The cryogenic heat exchangers are the fastest-growing segment and are projected to expand at a CAGR of 7.6%. The growth of this segment is driven by the increasing need to enhance thermodynamic efficiency and reduce energy consumption in hydrogen liquefaction processes, which are inherently energy-intensive. These heat exchangers are critical in enabling effective heat transfer across multiple cooling stages, allowing hydrogen to reach the extremely low temperatures required for liquefaction.

To know how our report can help streamline your business, Speak to Analyst

By Liquefaction Technology

Claude Cycle Segment Led due to its Benefits

By liquefaction technology, the market is segmented into Claude Cycle, Brayton Cycle, Mixed Refrigerant Cycle, and Helium-based Liquefaction.

Claude Cycle held the largest market share as it remains one of the most established and widely implemented hydrogen liquefaction processes across large-scale industrial and commercial applications. This cycle combines expansion turbines and Joule-Thomson cooling to achieve the extremely low temperatures required for hydrogen liquefaction, offering a balance between efficiency, reliability, and scalability. Its proven performance and adaptability to continuous large-scale operations make it the preferred choice for hydrogen liquefaction plants, particularly in industrial hydrogen production facilities and export-oriented infrastructure.

Mixed Refrigerant Cycle is the fastest-growing segment and is projected to expand at a CAGR of 8.1%. The growth of this segment is driven by its superior energy efficiency and ability to reduce specific energy consumption in hydrogen liquefaction processes compared to conventional cycles. Moreover, it utilizes a combination of refrigerants to optimize heat exchange across multiple temperature ranges, enabling improved thermodynamic performance and lower operational costs.

By Plant Capacity

Medium-Scale (10–50 TPD) Segment Led due to its Ability to Reduce Financial Risk Associated with Large-Scale Investments

By plant capacity, the market is segmented into small-scale (<10 TPD), medium-scale (10–50 TPD), and large-scale (>50 TPD).

Medium-Scale (10–50 TPD) held the largest hydrogen liquefaction equipment market share as it represents the most commercially viable and widely deployed capacity range across current hydrogen liquefaction projects. This segment strikes an optimal balance between capital investment, operational efficiency, and scalability, making it suitable for a wide range of applications, including regional hydrogen distribution, industrial supply, and early-stage export infrastructure. Medium-scale liquefaction plants are increasingly being adopted in both developed and emerging markets as they allow phased capacity expansion while reducing financial risk associated with large-scale investments.

Large-Scale (>50 TPD) is the fastest-growing segment and is projected to expand at a CAGR of 7.8%. The growth of this segment is driven by the increasing development of export-oriented hydrogen projects and the emergence of global hydrogen trade, which require high-capacity liquefaction facilities capable of supporting bulk production and long-distance transportation. Large-scale plants are typically associated with integrated hydrogen production hubs and export terminals, where economies of scale and continuous operation are critical for achieving cost efficiency.

By End-Use Industry

Hydrogen Production & Liquefaction Plants Segment Led due to Increasing Development of Integrated Green Hydrogen Projects

By end-use industry, the market is segmented into hydrogen production & liquefaction plants, energy & power, transportation, refining & petrochemicals, chemicals, and aerospace & defense.

Hydrogen production & liquefaction plants held the largest market share as they represent the primary deployment area for large-scale liquefaction systems across the hydrogen value chain. These facilities require continuous and high-capacity liquefaction operations to support hydrogen storage, export, and industrial distribution, making them the largest consumers of cryogenic liquefaction equipment. The increasing development of integrated green hydrogen projects and export-oriented hydrogen hubs is further driving demand for advanced liquefaction systems capable of improving energy efficiency and supporting large-volume hydrogen processing.

Transportation is the fastest-growing segment and is projected to expand at a CAGR of 8.0%. The growth of this segment is driven by increasing adoption of hydrogen across mobility applications, particularly in fuel cell electric vehicles, heavy-duty transport, marine transport, and emerging hydrogen aviation initiatives. As hydrogen mobility infrastructure expands globally, there is a rising demand for liquid hydrogen to support efficient storage, refueling, and transportation over long distances.

Hydrogen Liquefaction Equipment Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

North America

North America Hydrogen Liquefaction Equipment Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North American market held the largest share, accounting for over USD 0.66 billion in revenue in 2025, supported by increasing investments in hydrogen infrastructure, growing development of liquid hydrogen supply chains, and the expansion of industrial hydrogen applications across the U.S., Canada, and Mexico. Regional demand is closely linked to the rising adoption of clean hydrogen, the development of hydrogen hubs, and increasing focus on enabling efficient hydrogen storage and long-distance transportation. Energy companies and project developers are increasingly deploying advanced hydrogen liquefaction equipment to improve process efficiency, reduce energy consumption, and support large-scale hydrogen production and distribution, particularly in applications such as hydrogen export facilities, mobility infrastructure, and industrial hydrogen supply networks.

U.S. Hydrogen Liquefaction Equipment Market

The U.S. is expected to dominate the market by 2026, holding revenue of about USD 0.55 billion, driven by its well-established hydrogen ecosystem, ongoing development of regional hydrogen hubs, and continuous investments in clean hydrogen infrastructure. Unlike many regions, U.S.-based companies are focusing on scaling up hydrogen liquefaction capacity to support both domestic demand and export opportunities. Strong emphasis is placed on improving energy efficiency, optimizing liquefaction processes, and reducing operational costs through the adoption of advanced cryogenic technologies and digital monitoring systems. The presence of leading equipment manufacturers and large-scale project developments further strengthens the country’s position in the market.

Europe

The European market is driven by a strong focus on decarbonization, expansion of green hydrogen projects, and the development of integrated hydrogen value chains across key economies such as Germany, the U.K., France, Italy, and the Netherlands. Demand for the product is closely linked to the region’s ambitious carbon neutrality targets and increasing investments in hydrogen production, storage, and export infrastructure. Governments and energy companies are prioritizing advanced liquefaction technologies that offer higher energy efficiency, reduced emissions, and compatibility with renewable-based hydrogen production systems. The growing need to support cross-border hydrogen trade and long-distance transportation is encouraging the deployment of large-scale liquefaction facilities, particularly in regions with strong renewable energy capacity.

U.K. Hydrogen Liquefaction Equipment Market

The U.K. market is estimated to reach around USD 0.09 billion by 2026, representing roughly 3.8% of global sales.

Germany Hydrogen Liquefaction Equipment Market

Germany’s market is projected to reach approximately USD 0.14 billion by 2026, equivalent to around 6.2% of global sales.

Asia Pacific

Asia Pacific remains the significant growing market, generating revenue of USD 0.44 billion globally in 2025. Asia Pacific continues to dominate the market, driven by rapid industrialization, rising electricity demand, and large-scale investments in hydrogen liquefaction infrastructure across key economies such as China, India, Japan, and Southeast Asian countries. The region’s growth is primarily supported by increasing government investments in energy capacity expansion, including thermal power plants, renewable energy projects, and grid modernization initiatives.

China Hydrogen Liquefaction Equipment Market

China’s market is projected to remain the dominant one in the Asia Pacific region, with 2026 revenue estimates at around USD 0.17 billion, representing roughly 7.5% of global sales.

Japan Hydrogen Liquefaction Equipment Market

The Japanese market is estimated to reach around USD 0.07 billion by 2026, accounting for roughly 2.9% of the global sales.

India Hydrogen Liquefaction Equipment Market

The Indian market is estimated at around USD 0.08 billion by 2026, accounting for roughly 3.6% of global sales.

Middle East & Africa

The Middle East & Africa market is driven by increasing investments in hydrogen infrastructure, the development of export-oriented hydrogen economies, and growing focus on energy diversification across GCC countries, South Africa, Israel, and North Africa. Demand for the product is closely linked to the region’s strategic shift toward becoming a global supplier of clean hydrogen, supported by abundant renewable energy resources and large-scale project developments. Countries in the region are actively investing in integrated hydrogen value chains, including production, liquefaction, storage, and export infrastructure, to enable long-distance transportation of hydrogen in liquid form.

GCC Hydrogen Liquefaction Equipment Market

The GCC market is projected to reach around USD 0.14 billion by 2026, representing roughly 6.2% of the global sales.

South America

The South American market is driven by increasing investments in hydrogen infrastructure, growing focus on renewable energy utilization, and the emergence of export-oriented hydrogen projects across key economies such as Brazil, Argentina, and Chile. Demand for hydrogen liquefaction equipment is closely linked to the region’s strong renewable energy potential, particularly in solar and wind, which is supporting the development of green hydrogen production integrated with liquefaction systems for storage and transportation. Countries in the region are actively exploring hydrogen as a key component of their long-term energy strategies, creating demand for scalable and efficient liquefaction technologies.

Brazil Hydrogen Liquefaction Equipment Market

The Brazilian market is projected to reach around USD 0.06 billion by 2026, representing roughly 2.8% of the global sales.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus on Offering Advanced Liquefaction Technologies to Improve Thermodynamic Efficiency

The hydrogen liquefaction equipment market is moderately consolidated, with competitive positioning driven by advanced cryogenic engineering capabilities, energy efficiency of liquefaction systems, and the ability to deliver high-performance hydrogen liquefaction solutions across large-scale industrial applications. Leading players such as Air Liquide S.A., Linde plc, Air Products and Chemicals, Inc., Chart Industries, Inc., and Mitsubishi Heavy Industries, Ltd. maintain strong market positions by offering advanced liquefaction technologies designed to improve thermodynamic efficiency, reduce energy consumption, and support large-scale hydrogen storage and transportation.

Competitive differentiation is increasingly shaped by the ability to develop energy-efficient liquefaction systems equipped with advanced refrigeration cycles, high-performance heat exchangers, and integrated digital monitoring solutions. As hydrogen producers and project developers focus on reducing operational costs and improving overall process efficiency, market players are investing in next-generation liquefaction technologies such as mixed refrigerant cycles, modular plant designs, and scalable cryogenic systems that enable efficient hydrogen liquefaction across varying capacity requirements.

- For instance, in May 2024, Iwatani Corporation announced the expansion of its liquid hydrogen supply capabilities in Japan, including investments in liquefaction and storage infrastructure to support growing hydrogen demand in mobility and industrial sectors.

LIST OF KEY HYDROGEN LIQUEFACTION EQUIPMENT COMPANIES PROFILED

- Air Liquide S.A. (France)

- Linde plc (Ireland)

- Air Products and Chemicals, Inc. (U.S.)

- Chart Industries, Inc. (U.S.)

- Mitsubishi Heavy Industries, Ltd. (Japan)

- Kawasaki Heavy Industries, Ltd. (Japan)

- NEL Hydrogen (Norway)

- Plug Power Inc. (U.S.)

- ITM Power plc (U.K.)

- Iwatani Corporation (Japan)

KEY INDUSTRY DEVELOPMENTS

- June 2025: Iwatani Corporation announced the expansion of its liquid hydrogen supply chain infrastructure in Japan, including investments in liquefaction and storage systems to support growing hydrogen demand.

- April 2025: Chart Industries, Inc. announced new orders and project deployments for its hydrogen liquefaction and cryogenic equipment solutions, supporting multiple hydrogen infrastructure projects across North America and Europe.

- March 2025: Air Products and Chemicals, Inc. reported continued construction progress of the NEOM Green Hydrogen Project, which includes large-scale hydrogen production and liquefaction infrastructure to enable global export of liquid hydrogen.

- February 2025: Linde plc announced the ongoing expansion of its clean hydrogen production and liquefaction capabilities in the U.S., focusing on increasing liquid hydrogen supply for industrial and mobility applications.

- January 2025: Plug Power Inc. announced further development of its green hydrogen network in North America, including scaling of liquefaction capacity within its hydrogen production plants to support distribution infrastructure.

REPORT COVERAGE

The global hydrogen liquefaction equipment market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, and key industry developments and prevalence by key regions. The global market research report also provides a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.2% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Equipment Type, Liquefaction Technology, Plant Capacity, End-Use Industry, and Region |

| By Equipment Type |

|

| By Liquefaction Technology |

|

| By Plant Capacity |

|

| By End-Use Industry |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 2.11 billion in 2025 and is projected to reach USD 3.90 billion by 2034.

In 2025, North America’s market value stood at USD 0.66 billion.

The market is expected to exhibit a CAGR of 7.2% during the forecast period (2026-2034).

By end-use industry, the hydrogen production & liquefaction plants segment dominated the market.

Emergence of cross-border hydrogen trade corridors is the key factor driving market growth.

Air Liquide, Linde plc, Air Products, Chart Industries, Mitsubishi Heavy Industries, and Kawasaki Heavy Industries are the top players in the market.

North America held the largest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 140

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us