Hydrogen-Powered Ships Market Size, Share & Industry Analysis, By Vessel Type (Passenger Ferries, Inland Waterway Vessels, Coastal & Short-Sea Shipping, Offshore Support Vessels, Deep-Sea Vessels, and Others), By Technology (Fuel Cell-Based, Hydrogen ICE, Hybrid Systems, and Others), By Hydrogen Storage (Compressed Hydrogen, Liquid Hydrogen, Material-Based Storage, and Others), By Application (Passenger Transport, Cargo & Logistics, Offshore Operations, Defense & Government, and Others), and Regional Forecast, 2026-2034

Hydrogen-Powered Ships Market Size and Future Outlook

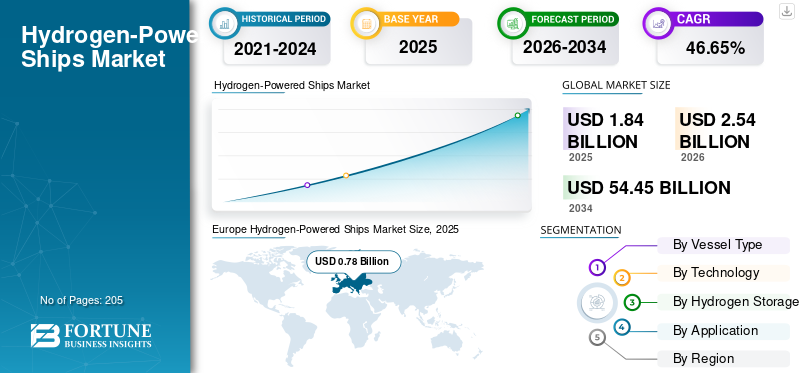

The global hydrogen-powered ships market size was valued at USD 1.84 billion in 2025. The market is projected to grow from USD 2.54 billion in 2026 to USD 54.45 billion by 2034, exhibiting a CAGR of 46.65% during the forecast period. Europe dominated the hydrogen-powered ships market with a market share of 42.39% in 2025.

Hydrogen-powered ships represent a critical pathway in maritime decarbonization, particularly for short-sea and coastal applications where zero-emission propulsion is increasingly mandated. Unlike conventional fuel transitions such as LNG or methanol, hydrogen-based systems, primarily fuel cells, enable true zero-emission operations at the point of use, making them highly relevant for regulated zones such as European fjords and California waterways. The market is currently driven by pilot-scale deployments and early commercial vessels, with growing integration of hydrogen storage, fuel cells, and hybrid propulsion architectures into vessel design. Support from the U.S. Department of Energy through funding and research initiatives, along with expanding hydrogen infrastructure and declining fuel cell costs, is expected to favor the product adoption.

Key drivers include tightening emissions regulations under the International Maritime Organization IMO and regional authorities, especially CO2 emissions intensity targets and zero-emission vessel mandates in ports and inland waterways, which are directly influencing the market share of hydrogen-powered ships within the broader alternative fuel segment. Additionally, government-backed funding programs in Europe, Japan, and North America are accelerating demonstration projects, reducing initial capital barriers for shipowners. The development of hydrogen corridors and port-side infrastructure is also enabling operational feasibility for coastal and ferry segments.

- For instance, in February 2025, CMB.TECH announced the deployment and expansion of its hydrogen-powered vessel fleet, including the operation of hydrogen dual-fuel ships in European inland and short-sea routes. The company highlighted the commercial viability of hydrogen propulsion by integrating onboard hydrogen storage and engine systems in working vessels rather than pilot-only projects. This initiative reflects a transition from demonstration to early commercialization, with a focus on reducing emissions in regulated European shipping corridors and strengthening hydrogen adoption in maritime operations.

Some of the leading companies operating in the global market include Ballard Power Systems, PowerCell Sweden AB, Wärtsilä, and MAN Energy Solutions. Ballard Power Systems is a key provider of proton exchange membrane (PEM) fuel cell solutions for hydrogen-powered ships, supplying zero-emission propulsion systems for ferries, inland vessels, and coastal applications. The company is actively involved in multiple marine projects globally, focusing on scalable fuel cell modules and system integration to support the transition toward clean energy transport. Rising concerns over high carbon emissions from fossil fuels and increasing pressure to decarbonize maritime transport are driving the shift toward hydrogen-powered ships.

Download Free sample to learn more about this report.

HYDROGEN-POWERED SHIPS MARKET TRENDS

Shift Toward Commercial Deployment in Short-Sea and Coastal Hydrogen Shipping is the Key Market Trend

The hydrogen-powered ships market growth is increasingly transitioning from experimental pilots to commercial deployment in short-sea, coastal, and inland waterway segments, where operational feasibility aligns with current technological constraints. A key trend is the standardization of modular fuel cell systems, enabling scalable integration across vessel classes such as ferries and feeder ships, thereby reducing design complexity and improving cost efficiency. Simultaneously, there is a growing shift toward liquid hydrogen storage solutions for higher-capacity vessels, addressing range limitations associated with compressed hydrogen.

The market is also witnessing increased adoption of hybrid propulsion configurations, combining hydrogen production with battery systems to optimize energy efficiency and operational flexibility. Another critical trend is the development of dedicated hydrogen shipping corridors and port-centric ecosystems, particularly in Europe and Asia Pacific, which are facilitating synchronized investments in vessels, bunkering infrastructure, and supply chains. The market remains in early stages of development, with ongoing advancements in fuel cell efficiency, storage systems, and vessel integration technologies gradually improving commercial readiness.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rapid Integration of Hydrogen Ecosystems across Maritime Value Chain is the Key Market Driver

The market is being driven by the rapid integration of hydrogen ecosystems across the maritime value chain, particularly linking production, storage, and end-use within shipping operations. A key driver is the increasing availability of dedicated green hydrogen supply from large-scale industrial projects, enabling more reliable fuel sourcing for maritime applications. The expansion of industrial clusters and export-oriented hydrogen hubs, especially in regions with abundant renewable resources, is also supporting maritime adoption by creating localized demand centers.

In addition, strategic collaborations between shipowners, technology providers, and port authorities are accelerating vessel deployment by aligning fuel availability with fleet operations. Another important factor is the declining cost trajectory of electrolyzers and hydrogen storage systems, which is gradually improving the economic viability of hydrogen-powered vessels compared to conventional alternatives. These factors are anticipated to boost the hydrogen-powered ships market share during the forecast period.

MARKET RESTRAINTS

High System Costs and Infrastructure Limitations to Hamper Market Growth

The market faces significant restraints due to the high capital cost associated with hydrogen propulsion systems, particularly fuel cells, cryogenic storage tanks, and onboard integration components. Compared to conventional marine engines or even alternative fuels such as LNG and methanol, hydrogen systems require substantial upfront investment, making large-scale commercial adoption financially challenging for shipowners.

Furthermore, constraint is the limited availability of hydrogen bunkering infrastructure, especially outside select pilot regions in Europe and parts of Asia, which restricts operational flexibility and route planning. Additionally, energy density limitations of hydrogen, particularly in compressed form, result in larger storage requirements, impacting vessel design, cargo capacity, and overall efficiency.

MARKET OPPORTUNITIES

Expansion of Hydrogen Shipping Corridors and Commercial Fleet Conversion to Create New Growth Opportunities

The hydrogen-powered ships industry presents strong opportunities through the development of dedicated hydrogen shipping corridors, particularly across Europe, Asia Pacific, and select transnational trade routes. These corridors are enabling synchronized deployment of vessels, bunkering infrastructure, and fuel supply chains, creating commercially viable ecosystems for hydrogen adoption.

In addition, opportunity lies in the conversion of existing coastal and short-sea fleets, where aging diesel-powered vessels can be retrofitted with hydrogen propulsion systems, offering a faster pathway to scale compared to newbuilds. The increasing focus on port decarbonization initiatives is also driving demand for hydrogen-powered harbor crafts, tugboats, and service vessels, expanding the addressable market beyond traditional shipping segments. Additionally, advancements in liquid hydrogen handling and storage technologies are opening opportunities for medium-range cargo vessels, gradually extending hydrogen’s applicability beyond ferries and inland vessels.

MARKET CHALLENGES

Operational Complexity in Hydrogen Integration to Challenge Market Expansion

The market faces critical challenges related to the operational complexity of integrating hydrogen systems into marine environments, particularly in terms of storage, handling, and onboard safety management. Hydrogen’s low volumetric energy density necessitates larger or more complex storage solutions, such as high-pressure tanks or cryogenic systems, which create design constraints and require specialized engineering. Also, ensuring safe handling of hydrogen fuel under varying maritime conditions, including vibration, temperature fluctuations, and confined onboard spaces, poses significant technical challenges.

Segmentation Analysis

By Vessel Type

Passenger Ferries Dominated Due to Strict Emission Norms in Ferry Routes

Based on the vessel type, the market is classified into passenger ferries, inland waterway vessels, coastal & short-sea shipping, offshore support vessels, deep-sea vessels, and others.

In 2025, passenger ferries dominated the market, accounting for 35.60% share, as they represent the most active adoption segment for hydrogen-powered ships due to their operation on fixed, short-distance routes within emission-regulated zones such as European fjords and urban waterways. These vessels are increasingly targeted by regional authorities enforcing zero-emission mandates, making hydrogen a viable compliance solution. Additionally, ferries typically return to the same port, simplifying hydrogen refueling logistics and reducing infrastructure challenges.

The coastal & short-sea shipping segment is experiencing the highest growth and is expected to grow at a CAGR of 48.49% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Technology

Fuel Cell-Based Segment Dominated Market Due to High Efficiency and Zero-Emission Propulsion Capability

Based on the technology, the market is classified into fuel cell-based, hydrogen ICE, hybrid systems, and others.

In 2025, the fuel cell-based segment accounted for 54.13% share of the global market. Fuel cell-based propulsion is a primary driver in the market due to its ability to deliver zero-emission energy conversion with higher efficiency compared to combustion-based systems. Proton exchange membrane (PEM) fuel cells, in particular, are gaining traction for maritime applications due to their quick start-up, modularity, and suitability for variable load conditions. These systems enable silent operations with minimal vibration, making them ideal for passenger and coastal vessels.

The Hydrogen ICE segment is expected to grow at a CAGR of 47.39% during the forecast period.

By Hydrogen Storage

Compressed Hydrogen Led Market Due to Simpler Storage and Lower Infrastructure Complexity

On the basis of hydrogen storage, the market is classified into compressed hydrogen, liquid hydrogen, material-based storage, and others.

In 2025, the compressed hydrogen segment accounted 49.11% share of the global market. Compressed hydrogen is widely adopted in early-stage hydrogen-powered ships due to its relatively simpler storage technology and lower system complexity compared to liquid hydrogen. It is particularly suitable for short-range applications such as ferries and inland vessels, where space constraints and range requirements are manageable. The use of high-pressure tanks (typically 350–700 bar) allows easier integration into existing vessel designs without requiring cryogenic handling systems.

The liquid hydrogen segment is expected to grow at a CAGR of 47.78% during the forecast period.

By Application

Passenger Transport Dominated Due to Urban Emission Mandates

On the basis of the application, the market is classified into passenger transport, cargo & logistics, offshore operations, defense & government, and others.

In 2025, the passenger transport segment accounted for 36.87% share of the global market. The passenger transport sector is a key application driving hydrogen-powered ships due to increasing regulatory pressure on urban and coastal mobility systems to reduce emissions. Ferries operating in densely populated regions are subject to strict environmental standards, pushing operators toward zero-emission alternatives such as hydrogen. The predictable routes and fixed schedules of passenger vessels make hydrogen integration more feasible, particularly in regions with established or developing refueling infrastructure.

The cargo & logistics segment is expected to grow at a CAGR of 48.93% during the forecast period.

Hydrogen-Powered Ships Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America and the Middle East & Africa.

Europe

Europe Hydrogen-Powered Ships Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Europe is projected to record a growth rate of 47.06% in the coming years, which is the highest among all regions, and reached a valuation of USD 0.78 billion in 2025. Europe leads the market due to strict zero-emission regulations in maritime zones such as Norwegian fjords, directly mandating clean vessel adoption. Countries such as Norway and the Netherlands are actively deploying commercial hydrogen ferries and inland vessels, supported by EU funding programs. The region is also advancing hydrogen shipping corridors and port-led ecosystems (e.g., Rotterdam), enabling fuel availability and operational viability.

Germany Hydrogen-Powered Ships Market

The German market in 2025 was valued at USD 0.17 billion 2025 and is estimated at around USD 0.23 billion in 2026, representing roughly 9.02% of the global revenues. Germany’s market is driven by government-backed pilot projects for inland waterway vessels along the Rhine corridor, focusing on retrofitting existing fleets. The country is also investing in integrating hydrogen propulsion with industrial hydrogen hubs, linking maritime applications with its broader hydrogen economy strategy.

North America

The North American market in 2025 was valued at USD 0.28 billion, and it also took a significant share in 2026 with USD 0.37 billion. North America’s market is primarily driven by state-level zero-emission mandates, particularly in California, where ferry electrification and hydrogen adoption are being actively funded. The region is seeing increased deployment of hydrogen fuel-cell ferries and pilot vessels, supported by agencies such as CARB. Additionally, public-private partnerships and grant-based funding models are accelerating early commercialization, especially in coastal and inland waterways. The U.S. is also focusing on integrating hydrogen vessels with port decarbonization strategies, creating localized adoption hubs.

U.S. Hydrogen-Powered Ships Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market was valued at USD 0.23 billion in 2025, accounting for roughly 12.42% of the global revenues.

Asia Pacific

Asia Pacific was valued at USD 0.53 billion in 2025. In the region, India and China were valued at USD 0.04 billion and USD 0.16 billion, respectively, in 2025.

Asia Pacific’s market is driven by large-scale shipbuilding capabilities in South Korea, China, and Japan, enabling a faster transition from pilot to commercial vessels. The region is also seeing strong momentum from national hydrogen roadmaps and export-oriented hydrogen strategies, supporting deployment across coastal and short-sea shipping segments.

India Hydrogen-Powered Ships Market

The India market accounted for roughly 2.38% of global revenues. India’s hydrogen-powered ships market is emerging through government-backed pilot projects led by Cochin Shipyard and inland waterway authorities, focusing on fuel-cell ferry deployment. The country is also aligning maritime adoption with its National Green Hydrogen Mission, targeting integration of hydrogen vessels in coastal and river transport systems.

China Hydrogen-Powered Ships Market

The market in China represents roughly 8.74% of the global revenues.

Japan Hydrogen-Powered Ships Market

The Japan market in 2025 was valued at USD 0.11 billion, accounting for roughly 6.01% of global revenues.

Latin America

Latin America is expected to witness moderate growth in this market space in the long term. The Latin America market was valued at USD 0.10 billion in 2025. Latin America’s market is gaining traction through green hydrogen export projects in Chile and Brazil, which are being linked to future maritime fuel applications.

Brazil Hydrogen-Powered Ships Market

Brazil's market was valued at USD 0.05 billion in 2025, representing roughly 2.71% of global revenues.

Middle East & Africa

The Middle East & Africa market is expected to witness significant growth in this market space during the forecast period. The Middle East & Africa market was valued at USD 0.16 billion in 2025. The Middle East & Africa market is developing through large-scale green hydrogen projects in the GCC, particularly NEOM and UAE initiatives, which are expected to support future maritime fuel demand. The region is also focusing on port-led hydrogen bunkering and export infrastructure, positioning itself as a key supplier of international fuel for shipping.

GCC Hydrogen-Powered Ships Market

The GCC market was valued at USD 0.07 billion in 2025, representing roughly 4.04% of the global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Major players are Actively Expanding Their Market Share via Partnerships, Business Expansion, and Technological Advancements

The global hydrogen-powered ships market holds a consolidated market structure, constituting prominent players such as Ballard Power Systems, PowerCell Sweden AB, Wärtsilä, and MAN Energy Solutions. Companies operating in the market are adopting targeted growth strategies focused on strengthening their product portfolio, technical capability, expanding manufacturing presence, and other areas.

- For instance, in March 2024, Ballard Power Systems announced the supply of its marine-grade PEM fuel cell modules for multiple hydrogen-powered vessel projects in Europe, including ferry and inland waterway applications. The initiative focuses on delivering scalable fuel cell systems designed for maritime conditions, supporting zero-emission propulsion. Ballard also expanded collaborations with shipbuilders and system integrators to accelerate deployment, reinforcing its position as a key technology provider in early-stage hydrogen vessel commercialization.

Other key players in the global market include Norled, Cummins Inc., Siemens Energy, Mitsubishi Heavy Industries (MHI), Kawasaki Heavy Industries, and others. These companies are expected to prioritize new product launches and collaborations to increase their global market share during the forecast period.

LIST OF KEY HYDROGEN-POWERED SHIP COMPANIES PROFILED

- Ballard Power Systems (Canada)

- ABB (Switzerland)

- PowerCell Sweden AB (Sweden)

- Cummins Inc. (U.S.)

- Wärtsilä (Finland)

- Mitsubishi Heavy Industries (MHI) (Japan)

- MAN Energy Solutions (Germany)

- Norled (Norway)

- Siemens Energy (Germany)

- Kawasaki Heavy Industries (Japan)

KEY INDUSTRY DEVELOPMENTS

- June 2024: Wärtsilä advanced its hydrogen strategy by testing ammonia and hydrogen-based marine engines and fuel systems, aiming for commercial readiness in shipping applications. The company is integrating hydrogen fuel capabilities into its existing propulsion portfolio, focusing on hybrid solutions combining fuel cells and engines.

- May 2024: ABB expanded its role in hydrogen-powered shipping by delivering integrated electric propulsion and fuel cell interface systems for a hydrogen ferry project in Europe. The initiative focuses on optimizing power distribution and energy management for fuel cell-based vessels. ABB’s involvement highlights its strength in electrification and system integration, enabling efficient operation of hydrogen-powered ships and supporting the transition toward zero-emission maritime solutions.

- April 2024: MAN Energy Solutions progressed its development of hydrogen-fueled marine engines, focusing on retrofitting existing vessels and enabling dual-fuel operations. The initiative includes testing hydrogen combustion technologies to complement fuel cell systems, providing shipowners with flexible decarbonization pathways.

- January 2024: PowerCell Sweden secured a contract to deliver its marine fuel cell system for a European hydrogen-powered vessel project, targeting coastal and ferry applications. The company emphasized its modular fuel cell platform, designed for integration into hybrid propulsion systems. This initiative supports the transition from pilot demonstrations to operational deployment, while strengthening PowerCell’s presence in the marine hydrogen segment through partnerships with shipyards and system integrators.

- August 2023: Norled launched one of the world’s first liquid hydrogen-powered ferry projects (MF Hydra) in Norway, marking a major milestone in commercial hydrogen vessel deployment. The ferry operates on fixed routes, demonstrating the feasibility of hydrogen propulsion in real-world conditions.

REPORT COVERAGE

The global hydrogen-powered ships market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and the market trends expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 46.65% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Vessel Type, Technology, Hydrogen Storage, Application, and Region |

| By Vessel Type |

|

| By Technology |

|

| By Hydrogen Storage |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 1.84 billion in 2025 and is projected to reach USD 54.45 billion by 2034.

In 2025, the market value in Europe stood at USD 0.78 billion.

The market is expected to exhibit a CAGR of 46.65% during the forecast period of 2026-2034.

The passenger ferries segment led the market by vessel type.

Rapid integration of hydrogen ecosystems across the maritime value chain is driving the market.

Ballard Power Systems, PowerCell Sweden AB, Wärtsilä, MAN Energy Solutions, and ABB are some of the prominent players in the market.

Europe dominated the market in 2025.

Expansion of hydrogen infrastructure, declining fuel cell costs, and rising demand for zero-emission maritime transport are expected to favor product adoption.

- 2021-2034

- 2025

- 2021-2024

- 205

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us