Italian Food Market Size, Share & Industry Analysis, By Food Type (Vegetarian and Non-Vegetarian), By Raw Material (Wheat and Gluten-Free), By Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores, Grocery Stores, and Online Retail), and Regional Forecast, 2026-2034

(Offer valid till 15th Jul 2026)

KEY MARKET INSIGHTS

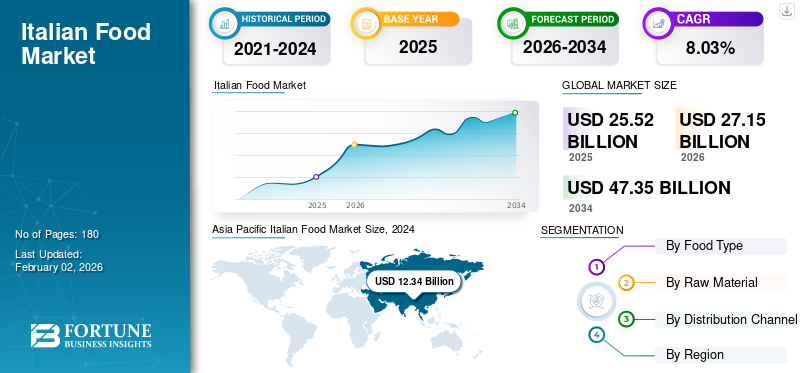

The global Italian food market size was valued at USD 25.52 billion in 2025. The market is projected to grow from USD 27.15 billion in 2026 to USD 47.35 billion by 2034, exhibiting a CAGR of 8.03% during the forecast period. Asia Pacific dominated the italian food market with a market share of 51.69% in 2025.

Italian food is prepared using the Mediterranean style of cooking, which comprises premium-quality and fresh ingredients (olives, herbs, and tomatoes). While pizza and pasta are highly recognized, Italian food encompasses an array of items such as lasagna, gnocchi, and arancini. Concerning consumption, Italy is the largest consumer of Italian dishes, and has considerably influenced other food cultures, specifically in Australia and the Americas. The popularity of Italian items is achieved due to increasing immigration and its adaptability. Moreover, these food items are known for their simplicity, with carefully chosen fresh ingredients, combined to develop flavorful food options. The surging trend of quick meals and increasing availability of authentic Italian items contribute to the market’s growing potential.

A few key players in the industry include Nestlé S.A., General Mills, Inc., and McCormick & Company, among others. These players are actively emphasizing multiplying their revenues in the market by acquisitions, brand strengthening through new product launches, and promoting their products through social media.

Download Free sample to learn more about this report.

Italian Food Market Snapshot & Highlights

Market Size & Forecast:

- 2025 Market Size: USD 25.52 billion

- 2026 Market Size: USD 27.15 billion

- 2034 Forecast Market Size: USD 47.35 billion

- CAGR: 8.03% from 2026–2034

Market Share & Segmentation:

- Asia Pacific dominated the Italian food market with a 51.69% share in 2025, driven by the demand for convenient, ready-to-cook meals like pizza and pasta due to hectic lifestyles, a rising premiumization trend, and expanding e-commerce access.

- By food type, the non-vegetarian segment held the largest market share, valued for its popularity, high consumption rates, and nutritional benefits like high-quality protein and essential vitamins.

- By distribution channel, supermarkets/hypermarkets led the market in 2024, thanks to their wide availability of international and local brands, bulk purchasing options, and discounted prices.

Key Regional Highlights:

- Asia Pacific: Leads the global market. Growth is fueled by consumers seeking easy-to-prepare meal options amidst increasingly busy lifestyles and the rising participation of women in the workforce.

- Europe: Ranks second, with growth supported by deep-rooted culinary traditions and cultural significance. A strong health and wellness trend is driving demand for organic, gluten-free, and fiber-enriched Italian products.

- North America: The third-largest market, driven by high demand for convenience products like pizza and lasagna. The large student population seeking cost-effective and easy-to-prepare meals also contributes to growth.

- South America: A nascent market with strong growth potential, fueled by an increasing trend in home cooking and growing tourism, which boosts the adoption of Italian cuisine.

MARKET DYNAMICS

Market Drivers

Increasing Global Appeal of Italian Products Escalates Market's Growing Potential

The rising appeal of Italian items is a pivotal driver strengthening the market's growing momentum. Although Italian cuisine is deeply ingrained in Italian culture, dishes such as ravioli, lasagna, and pasta/pizza have become staples in numerous countries. These dishes depend on fresh and easily available ingredients and are easy to adapt to various dietary needs, making them highly popular. Moreover, the rising immigration has led to the spread of cuisine globally, with most immigrants bringing their food recipes and traditions to different nations. Thus, due to its popularity, food operators are concentrating on introducing new Italian products for their customers.

Market Restraints

Health Ailments Associated with Italian Cuisine and Variations in Ingredient Costs Impede Market Growth

One of the critical challenges experienced by food producers/operators is the health risks associated with Italian food. While these food items are often linked with the Mediterranean diet, a few aspects can lead to health ailments. The extensive usage of sauces and high-fat cheese in pasta and pizza increases the risk of type 2 diabetes, cardiovascular challenges, and weight gain. Moreover, high cooking temperatures used in particular Italian dishes, such as fried foods, can create acrylamide, a carcinogen known for causing cancer. As a result, the aforementioned factors can hamper the global Italian food market growth.

Fluctuating raw ingredient prices are another obstacle for the global market. The industry depends on particular ingredients (wheat, yeast, cheese, and other condiments), and their cost can be volatile, ultimately affecting profitability and manufacturing costs.

Market Opportunities

sAdoption of Advanced Technologies Unlocks Growth Possibilities

The utilization of advanced technologies in Italian items production creates numerous growth opportunities. Modern food factories utilize automated lines with features such as continuous drying systems, vacuum extruders, and robotic arms for consistent product quality. Moreover, automated moisture extraction and ventilation systems can be used to avoid the breakage of food items. For pizza manufacturing, companies should opt for AI-powered dough stretching, where robots stretch pizza dough with speed and precision, minimizing labor work and streamlining the production process. Further, the emerging conveyor can make tables, strengthen consistency, and simplify the pizza topping process.

Italian Food Market Trends

Growing Inclination toward Culinary Tourism is a Current Trend

Culinary tourism is recognized as a notable and growing trend in the global market. This trend is no longer considered in the niche category, but is a substantial factor influencing the individual's travel decisions. In today's time, most tourists are always on the lookout to explore local cultures via authentic food, propelling the demand for Italian products. Food is considered a key aspect in choosing destinations, with a chunk of tourists picking locations based on the quality and authenticity of food. This ongoing gastronomic tourism trend supports the intake of Italian products.

SEGMENTATION ANALYSIS

By Food Type

Non-Vegetarian Segment Led Market, Owing to Its Popularity and High Consumption

On the basis of food type, the market is segmented into vegetarian and non-vegetarian.

The non-vegetarian segment dominated the market and held the dominant share in 2024. Compared to vegetarian food, non-vegetarian Italian food items are highly popular and consumed in larger amounts. Moreover, this food provides several essential vitamins, minerals, omega-3 fatty acids, and superior-quality protein. These nutrients aid in muscle repair and growth, weight management, and promote satiety. As a result, such advantages fuel the intake of non-veg-enriched Italian products.

The vegetarian segment is the fastest-growing segment and is expected to grow at the same pace in the future. The rising trend of veganism and improved emphasis on animal welfare can drive the segment's growth.

By Raw Material

Wheat Dominated Market Owing to Its Several Advantages and Wide Usage

Based on raw material, the market is distributed into wheat and gluten-free.

The wheat segment led the global Italian food market share in 2024. Wheat, particularly durum wheat, contains gluten, which is proven to offer texture, shape retention, and elasticity while cooking. Compared to gluten-free products, wheat-based Italian items have high carotenoid content, offering a golden yellow color. Moreover, wheat edibles cook more evenly than gluten-free items. As a result, such advantages augment its usage as a raw material.

The gluten-free segment, comprising ingredients such as starches and grains, ranked second in the market. These ingredients are gaining popularity due to the increasing awareness of celiac disease. Using gluten-free raw ingredients enhances digestive health and is a suitable alternative for vegans.

By Distribution Channel

Supermarkets/Hypermarkets Led Market Owing to Availability of International/Local Brands

Depending on the distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, grocery stores, and online retail.

The supermarkets/hypermarkets dominated the global market and generated the highest share in 2024. The major components supporting the segment's growth are the availability of international/local brands of packaged Italian items and the ease of shopping. Moreover, the option of bulk purchasing and discounted prices of Italian food products further drives the sales of Italian items.

The online retail segment exhibits a high CAGR, which makes it the fastest-growing segment. The convenience of ordering from the workplace/home and easy return/exchange option enhances the segment growth. Moreover, the rising adoption of quick commerce, such as Zepto and Blinkit, improves sales and consumer satisfaction.

Italian Food Market Regional Outlook

Based on region, the market is segmented into North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Italian Food Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific maintained a strong presence in the global market, reaching USD 13.19 billion in 2025, accounting for 51.69% share, and is expected to reach USD 14.12 billion in 2026. Asia Pacific is recognized as the leading region in the global market. In this region, most Asians are seeking easy-to-prepare meal options, especially as lifestyles become hectic. In recent years, women's workforce participation has increased, leaving women with minimal cooking time. To curb this burden, consumers opt for ready-to-cook/frozen Italian items such as pizza and pasta. These products can be easily prepared in a few minutes, making them an attractive option. Moreover, the rising premiumization trend has captivated affluent Asian consumers, resulting in innovation across the market. Additionally, the expanding e-commerce reach has provided access to various end products, boosting the regional growth.

Download Free sample to learn more about this report.

Europe

The Europe region captured 21.21% of the global market in 2025, generating USD 5.41 billion in revenue, and is projected to reach USD 5.73 billion in 2026. This growth is backed by an increasing number of Italian product manufacturers and robust culinary traditions. Italian products are deeply rooted in European cuisine, especially in Italy, where they hold substantial cultural importance. This cultural scenario drives the demand for Italian items across the region. Moreover, the region is witnessing a rapid health and wellness trend, directing consumers toward fiber-enriched pizza, gluten-free pasta, and other organic options. As a result, the food manufacturers are responding to this trend by introducing superior quality organic products. For instance, in December 2024, Realfoods Organico, a U.K.-based pasta manufacturer, introduced a new line of organic pasta, produced from durum wheat.

North America

In 2025, the North America market stood at USD 3.07 billion, representing 12.04% of global demand, and is projected to grow to USD 3.22 billion in 2026. The surging influence of Italian cuisine and increasing demand for convenience products are the pivotal factors fueling the market growth. Most Americans face highly busy schedules and are always looking for items that can be prepared easily. This trend strengthens the consumption of Italian products such as lasagna and pizza, owing to their lower cooking time and ability to be combined with numerous ingredients/sauces. In addition, the North American region comprises a large student population seeking cost-effective and convenient products. As a result, this aspect further drives the regional market's growth.

Among all the countries, the U.S. is considered the largest consumer of Italian items, following Canada and Mexico. The growing innovation in Italian products and the rising number of private label offerings enhance the market expansion potential in the country.

South America

The market in South America is at its nascent stage and is expected to grow faster in the near term. The increasing home cooking trend and growing tourism propel the acceptability rate of Italian products.

Middle East & Africa

The Middle East & Africa market accounted for USD 1.19 billion in 2025, representing 4.67% of the global industry, and is expected to reach USD 1.27 billion in 2026. The Middle East & Africa market is at a developing stage and is anticipated to maintain the same growth in the foreseeable years. The rising disposable income and increasing expansion of Italian food players in the region can boost the growth momentum.

Latin America

In 2025, Latin America represented USD 2.65 billion, accounting for 0.00% of the worldwide market, and is projected to grow to USD 2.81 billion in 2026.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Major Players Aim to Expand their Base to Increase their Market Share

Key players in the global market include Nestlé S.A., General Mills, Inc., McCormick & Company, Inc., and others. A number of prominent companies operating in the market are focusing on new Italian product launches to fulfil the evolving demands. Moreover, the firms are entering into partnerships that can strengthen their market reach.

List of Key Italian Food Companies Profiled

- Nestlé S.A. (Switzerland)

- Barilla Group (Italy)

- General Mills, Inc. (U.S.)

- McCormick & Company, Inc. (U.S.)

- B&G Foods (U.S.)

- Conagra Brands, Inc. (U.S.)

- Del Monte Foods Private Limited (India)

- MTR Foods Pvt. Ltd. (India)

- Rich Products Corporation (U.S.)

- Dr. Oetker (Germany)

KEY INDUSTRY DEVELOPMENTS

- May 2025: Nestlé S.A., a Swiss-based food conglomerate, unveiled a new frozen pizza, "Wood Fired Style Crust Pizza," through its DiGorno brand. This item is available in various options: Supreme Speciale, Four Cheese, Premium Pepperoni, and Italian Meat Trio across the U.S.

- May 2025: Tesco, a supermarket chain in the U.K., introduced its latest Italian range for U.K.-based consumers. This new range includes Tesco Finest Spaghetti Carbonara, Tesco Finest Spaghetti Bolognese, NEW Tesco Finest Truffle Carbonara Girasoli Pasta, and NEW Tesco Finest Truffle Carbonara Girasoli Pasta, among others.

- May 2025: Kellanova, a food manufacturer in the U.S., and Palermo Villa, a frozen pizza firm in the U.S., partnered to introduce Cheez-It frozen pizza. This 12-inch crust pizza is prepared using 100% real cheese and is available in numerous flavors across the U.S.

- November 2024: Barilla Group, an Italian pasta company, announced a limited edition of snowfall-shaped pasta in the U.S. This pasta is available on online channels and in Walmart stores across the U.S. market.

- August 2024: EQUII, a protein food tech startup in the U.S., released the news of their pasta innovation. The products, "Rigatoni" and "Mac & Cheese," are available in two boxes, offering fewer carbohydrates and a high amount of protein.

REPORT COVERAGE

The market research report includes quantitative and qualitative insights into the market. It also offers a detailed analysis of the market size and growth rate for all possible market segments. Key insights in the market report include an overview of related markets, a competitive landscape, recent industry developments such as mergers & acquisitions, the regulatory environment in critical countries, and current global market trends.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2019-2023 |

|

Unit |

Value (USD Billion) |

|

Growth Rate |

CAGR of 8.03% from 2026 to 2034 |

|

Segmentation |

By Food Type

|

|

By Raw Material

|

|

|

By Distribution Channel

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 27.15 billion in 2025.

The market is expected to grow at a CAGR of 8.03% during the forecast period (2026-2034).

By raw material, the wheat segment led the market.

The increasing global appeal of Italian products is a key factor driving the market.

Nestle S.A., General Mills, Inc., and McCormick & Company are a few of the top players in the market.

Asia Pacific held the highest share of the market.

The adoption of advanced technology for improving manufacturing processes offers key opportunities for market players.

- 2021-2034

- 2025

- 2021-2024

- 180

-

(Offer valid till 15th Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us