Lithium Ion Battery Anode Market Size, Share & Industry Analysis, By Battery Chemistry (Lithium-ion batteries {LIB} and Lithium-Ion Polymer Batteries {Li-Po}), By Anode Material (Graphite-based Anode {Natural & Synthetic graphite}, Silicon-based Anodes {Silicon oxide, Silicon carbon composites, & Blended graphite–silicon anodes}, Lithium Titanate, & Others), By Application (Electric Vehicles {Passenger EVs, Commercial EVs, & Others}, Consumer Electronics, {Smartphones, Laptops & Tablets, and Wearables & Portable Electronics}, Energy Storage Systems, & Others), & Regional Forecast, 2026-2034

Lithium Ion Battery Anode Market Size and Future Outlook

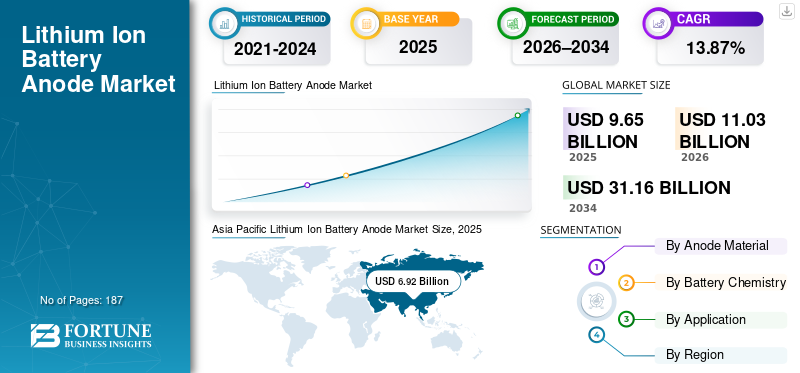

The global lithium ion battery anode market size was valued at USD 9.65 billion in 2025. The market is projected to grow from USD 11.03 billion in 2026 to USD 31.16 billion by 2034, with a CAGR of 13.87% over the forecast period. Asia Pacific dominated the lithium ion battery anode market with a market share of 71.70% in 2025.

Lithium-ion battery anodes are a core electrochemical component that store lithium during charging and discharging, directly influencing a battery’s energy density, power capability, cycle life, fast-charging performance, and overall safety. Commonly based on graphite, with increasing incorporation of silicon-based materials and niche use of lithium Titanate (LTO), anode materials play a decisive role in determining cell performance across key end-use sectors such as Electric Vehicles (EVs), consumer electronics, and Energy Storage Systems (ESS).

The global lithium-ion battery anode market is gaining momentum as the adoption of lithium-ion batteries across EVs, consumer electronics, and ESS increases. Anode materials, primarily graphite along with emerging silicon-based and lithium titanate (LTO) solutions, are essential for lithium storage during battery operation and directly influence energy densities, charging performance, and cycle life. The growing demand for higher-energy, fast-charging batteries is driving material innovation and the gradual adoption of silicon-enhanced anodes.

Leading players operating in the market, such as BTR New Material, Shanshan Technology, Hitachi Chemical (Resonac), POSCO Future M, Mitsubishi Chemical Group, and Showa Denko Materials, are focusing on capacity expansion and technological advancements to strengthen their presence. These companies are emphasizing improvements in material consistency, higher-capacity graphite formulations, and the development of silicon-enhanced anodes to address evolving performance requirements from battery manufacturers. Strategic collaborations, long-term supply agreements, and qualification with Tier-1 lithium-ion battery producers remain key priorities to secure stable demand across automotive and energy storage applications.

Download Free sample to learn more about this report.

Lithium Ion Battery Anode Market Trends

Fast-Charging and High-Energy Batteries are Driving Innovation in Anode Materials

The lithium ion battery anode market is witnessing a clear shift toward advanced anode materials and engineered formulations as battery manufacturers prioritize fast charging, higher energy density, and long-term cycling stability—particularly for EVs and Stationary ESS, where performance degradation and safety risks carry greater consequences. Conventional graphite anodes remain widely used; however, they face inherent limitations, including lithium plating risk, diffusion kinetics, and capacity constraints at high charging rates. As batteries are pushed to operate at higher power densities and shorter charging times, anode specifications are evolving from standard graphite formulations toward performance-optimized and silicon-enhanced designs.

Recent developments indicate that improved anode architectures can significantly enhance charge acceptance and durability compared to conventional graphite baselines, driving their adoption in high-demand applications. As OEMs and battery manufacturers continue to tighten performance and qualification standards, advanced anode materials are increasingly becoming a preferred choice in next-generation power and energy storage cells, supporting sustained demand growth across the battery value chain. For Instance, in May 2025, BASF and Group14 announced a market-ready silicon-anode solution: BASF and Group14 unveiled a “drop-in” silicon-anode solution (binder + silicon material), positioned around faster charging, higher energy density, and durability, reflecting continued formulation/process innovation for next-gen anodes.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Fast-charging Adoption and EV/ESS Scale-Up are Accelerating Demand for Advanced Anode Materials

The lithium ion battery anode market growth is driven by the rapid scale-up of EVs and stationary Energy Storage Systems (ESS), as OEMs and cell manufacturers increasingly prioritize shorter charging times and higher energy density. As battery packs operate at higher power levels and tighter thermal windows, the performance limitations of conventional graphite anodes—particularly under fast-charging conditions—are driving a shift toward engineered anode formulations that improve charge acceptance, cycle stability, and overall durability.

In addition, the growing deployment of high-energy cell platforms is pushing suppliers to develop next-generation anode materials that can deliver improved capacity without compromising lifecycle. This demand environment is supporting faster commercialization of silicon-enhanced and blended graphite–silicon anodes, alongside improved binder systems and process controls to meet qualification standards. For instance, in May 2025, BASF and Group14 announced a market-ready “drop-in” silicon anode solution combining BASF’s Licity binder and Group14’s SCC55 material, positioned to support faster charging, higher energy density, and durability, reinforcing the market’s shift toward performance-driven anode innovation.

Market Restraints

Performance Trade-offs and cost Pressures Continue to Limit the Rapid Substitution of Conventional Graphite

Despite strong interest in higher-capacity anode solutions, the market faces technical and cost challenges associated with silicon-enhanced materials. Silicon-based anodes are associated with issues such as volume expansion, structural degradation, and efficiency loss over repeated cycling, which can raise qualification timelines and increase manufacturing complexity. As a result, many cell producers continue to rely primarily on graphite for mass-market applications, adopting silicon in blended form or within selective platforms rather than shifting fully away from graphite.

Moreover, anode material economics remain sensitive to input costs, yield losses, and processing requirements—especially for consistent battery-grade quality. This dynamic can slow adoption in price-competitive segments and create cautious procurement behavior among battery manufacturers, particularly when suppliers cannot demonstrate stable performance at scale. Consequently, near-term growth in advanced anodes is often incremental and qualification-dependent rather than immediate across all cell categories.

Market Opportunities

Localization of anode Supply Chains and Commercial-Scale Silicon Investments Create new Growth Avenues

The lithium ion battery anode market is expected to witness expanding opportunities from ongoing battery supply chain localization initiatives, particularly in North America and Europe. As governments and OEMs seek to reduce reliance on single-region sourcing for critical battery materials, anode suppliers are increasingly evaluating regional production footprints and partnerships to support local cell manufacturing ecosystems. This trend opens opportunities for both established graphite suppliers and emerging silicon anode companies to secure long-term offtake agreements and accelerate customer qualification.

Additionally, strong investment activity in commercial-scale silicon anode production is creating new growth pathways for next-generation anode platforms. For instance, Sila announced the commissioning of its Moses Lake plant in April 2025 to produce silicon anode material at automotive scale, signaling increasing readiness of the silicon anode supply base for broader commercialization.

Market Challenges

Supply Risk, Policy Uncertainty, and Qualification Timelines Create Volatility in Anode Sourcing

A key challenge in the market is the high sensitivity of anode supply chains to trade policy, geopolitical risk, and upstream concentration—particularly for graphite and certain processed anode materials. Policy actions and tariff-related developments can influence procurement decisions, shift cost structures, and accelerate localization. Still, they may also introduce short-term pricing volatility and supply uncertainty for battery manufacturers. For example, in July 2025, the U.S. Department of Commerce announced a preliminary affirmative determination in an antidumping investigation of active anode material from China, reflecting heightened trade scrutiny in this supply chain.

Long qualification cycles remain a structural challenge because anode materials are highly sensitive to cell design and manufacturing conditions. Battery producers require extensive testing for cycle life, safety, and fast-charge performance before approving new anode formulations, which can slow the pace of supplier substitution and delay revenue ramp-up even when technologies appear commercially viable. As a result, the market continues to be shaped by a combination of technology readiness and qualification throughput, rather than innovation alone.

Segmentation Analysis

By Anode Material

Graphite-Based Anodes Lead, Driven by EV Scale-Up and Cost-Competitive Performance

Based on anode material, the market is segmented into graphite-based anode {natural graphite, synthetic graphite}, silicon-based anodes {silicon oxide (SiOx), silicon–carbon composites, blended graphite–silicon anodes}, lithium titanate (LTO), and others.

Graphite-based anodes account for approximately 91.09% of the lithium ion battery anode market share and remains the preferred choice for high-volume lithium-ion battery production owing to their established manufacturing ecosystem, stable electrochemical behavior, and favorable cost-to-performance profile. The dominance of graphite is strongly supported by the continued scale-up of EV cell production and expanding deployments of stationary ESS, where manufacturers prioritize proven cycle life, safety, and supply availability.

Silicon-based anodes will represent the highest growth driven by demand for higher energy density and improved fast-charging performance—particularly in passenger EVs and premium battery platforms. The segment is expected to grow at a CAGR of 22.69% during the forecast period.

By Battery Chemistry

Lithium-ion Battery Chemistry Leads the Market, Driven by EV and ESS Applications

Based on battery chemistry, the market is segmented into lithium-ion batteries (LIB) and lithium-ion polymer batteries (Li-Po).

Lithium-ion batteries (LIBs) account for ~92% of the market, supported by their dominant use in EVs and ESS, where higher capacity, longer cycle life, and scalable manufacturing economics are critical. The LIB segment continues to benefit from expanding EV battery production, increasing average battery pack sizes, and accelerating stationary storage deployments, which collectively reinforce sustained demand for anode materials—particularly graphite-based and blended graphite–silicon solutions.

Lithium-ion polymer (Li-Po) batteries account for a smaller but strategically relevant portion of overall demand, primarily driven by consumer electronics and portable applications where lightweight construction and flexible packaging formats are preferred. While Li-Po adoption remains stable, its growth is comparatively moderate relative to LIB, as the market’s largest incremental battery capacity additions are concentrated in EV and ESS deployments. The lithium-ion polymer batteries segment is expected to grow at a CAGR of 10.64% during the forecast period of 2021-2034.

To know how our report can help streamline your business, Speak to Analyst

By Application

Electric Vehicles Dominate Due to Rapid EV Adoption and Increasing Battery Capacity Per Vehicle

Based on application, the market is segmented into electric vehicles (passenger EVs, commercial EVs, others), consumer electronics (smartphones, laptops & tablets, wearables & portable electronics), Energy Storage Systems (ESS) {grid-scale ESS, residential ESS, commercial & industrial ESS}, and others.

The electric vehicles segment represents the largest share of the market, accounting for approximately 76.94% share in 2025, driven by rapid EV adoption, increasing battery capacity per vehicle, and continuous scale-up of lithium-ion cell manufacturing for automotive platforms. Passenger EVs contribute the majority of EV-related anode demand due to higher unit volumes and larger average pack sizes, while commercial EVs are expanding steadily as fleet electrification accelerates.

The Energy Storage Systems (ESS) segment is expected to witness the highest growth rate of 16.62% over the forecast period, supported by increasing renewable energy integration, grid modernization investments, and rising deployment of behind-the-meter storage across residential and commercial & industrial users. Grid-scale ESS, in particular, is emerging as a major driver of demand for battery materials as utilities deploy storage to improve reliability, manage peak load, and balance intermittent generation.

Lithium Ion Battery Anode Market Regional Outlook

By geography, the market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

Asia Pacific Lithium Ion Battery Anode Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America was valued at USD 1.11 billion in 2025, accounting for approximately 11.55% of the global market. The region is supported by the rapid scale-up of EV cell and pack manufacturing, growing stationary energy storage deployments, and increasing demand for higher-performance anode formulations that support fast charging and improved cycle stability. Supply-chain localization efforts and long-term procurement strategies are also encouraging investment in regional anode processing and qualification with Tier-1 cell makers.

U.S. Lithium Ion Battery Anode Market

The U.S. lithium-ion battery anode market was USD 0.98 billion in 2025 and is estimated to reach USD 1.11 billion in 2026, driven by the ramp-up of domestic battery manufacturing capacity, EV penetration, and increasing deployment of utility-scale and commercial storage. The growing focus on higher-energy chemistries and fast-charging platforms is also supporting demand for engineered graphite and blended graphite–silicon anodes.

Europe

Europe accounted for USD 1.30 billion in 2025, representing approximately 13.43% of global revenues. The region’s growth is driven by the proliferation of EV platforms, tightening performance expectations for battery packs, and ongoing investments in regional cell manufacturing. Europe also displays rising adoption of higher-spec anode materials (high-purity graphite and silicon-enhanced blends), supported by OEM-driven qualification requirements and localization momentum.

Germany Lithium Ion Battery Anode Market

Germany was estimated at USD 0.37 billion in 2025 and will reach USD 0.42 billion in 2026, supported by its strong automotive base, battery ecosystem investments, and demand for EV-grade anode materials with consistent quality and performance.

U.K. Lithium Ion Battery Anode Market

The U.K. market was valued at USD 0.22 billion in 2025 and is estimated to hit USD 0.25 billion in 2026, driven by EV adoption, the development of the battery supply chain, and rising deployments of stationary energy storage aimed at improving grid flexibility.

Asia Pacific

Asia Pacific was the largest region in 2025, valued at USD 6.92 billion, accounting for approximately 71.67% of global revenues. The region benefits from the world’s largest concentration of battery cell manufacturing, continued capacity additions for EV and ESS, and faster commercialization cycles for advanced anode formulations (including blended graphite–silicon approaches). APAC also leads in manufacturing scale and upstream integration, supporting both volume growth and technology upgrades.

China Lithium Ion Battery Anode Market

China remains the dominant contributor in APAC, hitting USD 4.25 billion in 2025 and is estimated to reach USD 4.88 billion in 2026, supported by massive cell output, EV scale, and continuous process improvements that increase adoption of high-performance, silicon-enhanced anodes.

India Lithium Ion Battery Anode Market

India’s market size reached USD 0.64 billion in 2025 and is expected to reach USD 0.75 billion in 2026, reflecting accelerating EV adoption, the buildout of local cell manufacturing, and increasing demand for anode materials across mobility and stationary storage.

Japan Lithium Ion Battery Anode Market

Japan’s market size was valued at USD 0.62 billion in 2025 and USD 0.70 billion in 2026, supported by a high-quality battery manufacturing base and a stronger preference for premium anode material specifications.

Latin America

Latin America accounted for USD 0.21 billion in 2025, approximating 2.21% of global revenues. The region’s growth is supported by gradual EV adoption, increasing solar-plus-storage deployments, and steady demand from industrial and backup power applications. The market remains largely graphite-led, with silicon-enhanced adoption progressing more selectively as qualification and cost considerations evolve.

Brazil Lithium Ion Battery Anode Market

The Brazilian market was valued at USD 0.084 billion in 2025 and will reach USD 0.091 billion in 2026, driven by growing electrification momentum and early-stage storage deployments.

Middle East & Africa

The Middle East & Africa were valued at USD 0.11 billion in 2025. Grid modernization initiatives, early-stage ESS investments, and expanding demand for lithium-ion batteries across telecom backup, industrial applications, and emerging mobility electrification support growth. The region remains graphite-heavy, while advanced anode adoption grows steadily in premium and higher-reliability systems.

GCC Lithium Ion Battery Anode Market

The GCC market size achieved USD 0.051 billion in 2025 and will reach USD 0.055 billion in 2026, supported by grid modernization, renewable integration, and increasing interest in energy storage projects.

Competitive Landscape

KEY INDUSTRY PLAYERS

Capacity Expansion & Regional Supply Chain Localization are Becoming the Default strategy

The global lithium-ion battery anode market is moderately fragmented, with a mix of large diversified chemical/materials companies and specialized anode producers competing on graphite purification and consistency, particle engineering (PSD control, surface treatment), first-cycle efficiency, and defect/yield control—alongside qualification depth with Tier-1 cell manufacturers. Competitive intensity is increasing as customers push for fast-charging-capable, higher-energy cells, accelerating the shift from “commodity graphite” toward high-spec graphite and silicon-enhanced/blended anodes, where process know-how and repeatability become differentiators.

List of Top Lithium-Ion Battery Anode Companies

- BTR New Material Group (China)

- Shanshan Technology (China)

- POSCO Future M (South Korea)

- Resonac (Japan)

- Mitsubishi Chemical Group (Japan)

- Tokai Carbon (Japan)

- SGL Carbon (Germany)

- Novonix (U.S.)

- Group14 Technologies (U.S.)

- Sila Nanotechnologies (U.S.)

KEY INDUSTRY DEVELOPMENTS

- October 2025: POSCO Future M signs a large natural graphite anode supply contract. This supports the broader trend of long-term supply agreements and the strategic importance of securing qualified anode supply.

- August 2025: Group14 reported closing USD 463 million to expand manufacturing footprint and also moved to full ownership/control of its Korean silicon battery material facility—reinforcing the “scale + localization” strategy for next-gen anodes.

- July 2025: U.S. Commerce announces preliminary affirmative antidumping determination on active anode material from China. This development underscores how policy and trade measures are becoming a factor in anode sourcing strategies and localization planning.

- May 2025: BASF and Group14 introduce a “drop-in” silicon anode solution. The collaboration combines BASF’s binder (Licity) with Group14’s silicon-carbon material (SCC55) and is positioned for faster charging, higher energy density, and durability, supporting the market trend toward engineered, qualification-ready silicon-enhanced anodes.

- April 2025: Sila announced commissioning for its first auto-scale manufacturing plant, Moses Lake plant (U.S.), highlighting ongoing investment to scale silicon anode material production and strengthen localized supply in North America.

REPORT COVERAGE

The report provides a comprehensive analysis of the market, focusing on key aspects such as leading companies, product processes, and Porter’s Five Forces. Additionally, the report provides valuable insights into market trends and highlights key industry developments. In addition to the factors mentioned above, the report also encompasses several factors that contributed to the market's growth in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 13.87% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Anode Material · Graphite-Based Anode o Natural graphite o Synthetic graphite · Silicon-Based Anodes o Silicon oxide (SiOx) o Silicon–carbon composites o Blended graphite–silicon anodes · Lithium Titanate (LTO) · Others |

|

By Battery Chemistry · Lithium-Ion Batteries · Lithium-Ion Polymer Batteries |

|

|

By Application · Electric Vehicles o Passenger EVs o Commercial EVs o Others · Consumer Electronics o Smartphones o Laptops & Tablets o Wearables & Portable Electronics · Energy Storage Systems (ESS) o Grid-Scale ESS o Residential ESS o Commercial & Industrial ESS · Others |

|

|

By Region

|

Frequently Asked Questions

According to a Fortune Business Insights study, the market size was USD 9.65 billion in 2025.

The market is likely to grow at a CAGR of 13.87% over the forecast period.

By battery chemistry, the lithium-ion batteries segment is expected to lead the market.

Asia Pacifics market size stood at USD 6.92 billion in 2025.

The adoption of fast charging and the scale-up of EV/ESS are accelerating demand for advanced anode materials.

Some of the leading players in the market include BTR New Materials Group, POSCO Future M, Resonac, and Tokai Carbon, among others.

The global market size is expected to reach USD 31.16 billion by 2034.

- 2021-2034

- 2025

- 2021-2024

- 187

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us