Military Connectors Market Size, Share & Industry Analysis, By Product Type (Circular connectors, Rectangular connectors, RF/coax connectors, Fiber-optic connectors, and Others), By Platform (Airborne (Manned & Unmanned Systems), Land, Naval, C4ISR infrastructure, and Space & strategic), By Application (C4ISR & tactical communications, Radar & electronic warfare, Avionics & mission computers, Weapon systems, Vehicle vetronics, and Others), By Connectivity Function (Power, Low-speed signal/control, High-speed data, RF, Optical (fiber), and Others), and Regional Forecast, 2026-2034

Military Connectors Market Size and Future Outlook

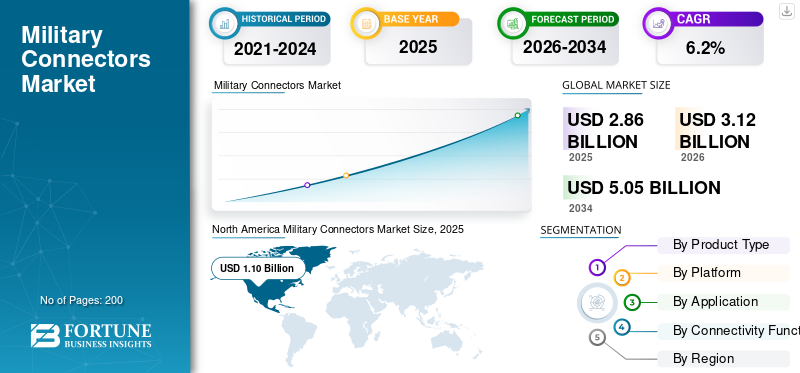

The global military connectors market size was valued at USD 2.86 billion in 2025. The market is projected to grow from USD 3.12 billion in 2026 to USD 5.05 billion by 2034, exhibiting a CAGR of 6.2%. during the forecast period. North America dominated the global military connectors market with a market share of 38.46% in 2025.

Military connectors are tough parts that transmit power and data between defense electronics. These include avionics boxes, vetronics, radars, electronic warfare suites, tactical radios, missiles, and communications and surveillance systems. They are built to be reliable in extreme conditions such as shock, vibration, salt fog, dust, moisture, temperature changes, and heavy electromagnetic interference or electromagnetic pulses. The market is growing due to a clear trend: modern forces are buying more sensors, networking gear, electronic warfare tools, and edge computing devices, creating more connection points. This change is pushing a shift toward high speed data, fiber optics, and hybrid interfaces that reduce wiring while boosting bandwidth and reliability.

Key players present in the market are Amphenol, TE Connectivity, ITT Cannon, Eaton/Souriau, Radiall, Glenair, Fischer Connectors, LEMO, HUBER+SUHNER, Rosenberger, and Smiths Interconnect.

Download Free sample to learn more about this report.

Military Connectors Market Key Takeaways

- 2025 Market Size: USD 2.86 billion

- 2026 Market Size: USD 3.12 billion

- 2034 Forecast Market Size: USD 5.05 billion

- CAGR: 6.2% from 2026–2034

- North America dominated the military connectors market with a 38.46% share in 2025.

- The fiber-optic connectors segment is projected to grow at a CAGR of 10.7% during the forecast period.

- The space & strategic segment is expected to expand at a CAGR of 8.2% during the forecast period.

North America

North America led the market in 2025, supported by strong U.S. defense spending and military modernization programs.

Europe

Europe was valued at approximately USD 0.78 billion in 2025 and is projected to grow at a CAGR of 8.1%.

Asia Pacific

Asia Pacific is anticipated to be the second-fastest-growing regional market, registering a CAGR of 7.0%.

U.S.

The market was valued at approximately USD 1.02 billion in 2025 and is projected to grow at a CAGR of 4.7%.

Japan

Increasing investments in defense modernization and advanced military communication systems are supporting market growth.

Read More

MILITARY CONNECTORS MARKET TRENDS

Open-architecture Plug-and-play Modernization is Increasing Demand for High-speed, Rugged Connectors

Armies and major contractors are shifting away from custom, hardwired integrations and moving toward modular, open standards. This change allows them to swap out sensors, radios, communications and surveillance systems, navigation tools, and computing hardware such as capability cards. This trend quietly increases demand for connectors in two ways. First, platforms need more standardized high-density power and data connections to support quick upgrades.

- In April 2025, the U.S. Army established the CMOSS Mounted Form Factor (CMFF) as a step toward quick plug-and-play capabilities. This approach uses a common chassis already designed for power and networking.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Global Defense Spending is Driving Steady Demand for Rugged Military Connectors

Military connectors sell when platforms and electronics programs sell, plain and simple. As defense budgets grow, more funding goes into radars, electronic warfare systems, tactical communications, avionics updates, air defense systems, missiles, and vehicle or ship upgrades. These areas rely heavily on connectors as they need more boxes, sensors, networking, and power distribution. Even if new platform purchases slow down, upgrade cycles remain strong. This includes replacing old wiring, increasing bandwidth, improving electromagnetic interference resilience, and supporting quicker maintenance through modular line-replaceable units.

- In April 2025, SIPRI reported that global military spending reached USD 2,718 billion in 2024, a 9.4% increase year-over-year in real terms. Spending rose in over 100 countries, creating widespread financial support for modernization and procurement focused on electronics.

MARKET RESTRAINTS

Tighter Chemical Regulations Related to PFAS are Creating Challenges in Redesigning and Qualifying Rugged Connectors

Much of the performance of rugged military interconnects comes from materials that allow connectors to seal, tolerate heat, resist fuels and fluids, and maintain stable insulation. PFAS-linked chemicals appear in many industrial applications. As regulators implement broader PFAS restrictions, connector and cable-assembly suppliers may need to change materials. This creates a difficult situation such as re-testing, re-qualification, documentation, and sometimes redesign to meet the same environmental and reliability standards. This doesn’t reduce demand, but it slows down projects, raises costs, and could limit supply for certain niche parts until alternatives are found.

- In February 2023, the European Chemicals Agency (ECHA) published a proposal for extensive PFAS restrictions. This proposal, submitted in January 2023 by five national authorities, is currently being reviewed by ECHA’s scientific committees. It illustrates how regulatory pressure can drive changes in materials and qualification efforts across aerospace and defense components.

MARKET OPPORTUNITIES

Proliferating Military Satellite Constellations are Creating Valuable Opportunities for Space-Grade and High-Speed Connectors

Space and strategic programs are moving from just a few high-end satellites to larger constellations. This shift quietly increased demand for space-qualified connectors, harnessing, and high-speed optical interconnects. Every satellite bus, payload, and ground segment needs reliable power and data interfaces that can handle vacuum, thermal cycling, vibration during launch, and long-life reliability requirements. As constellations grow, suppliers that provide miniaturized, high-density, and highly reliable interconnects often with optical links and strict size, weight, and power limits witness clear growth opportunities that are less affected by the cycles of traditional platform updates.

- In December 2024, the European Commission signed the concession contract for IRIS with the SpaceRISE consortium. They will develop, deploy, and operate a multi-orbital secure connectivity system consisting of around 290 satellites. This project highlights large-scale sovereign satellite communication programs that increase the demand for space-grade interconnect hardware across satellites and their supporting ground vehicles and infrastructure.

MARKET CHALLENGES

Counterfeit Risk and Traceability Compliance are Major Challenges for Connector Supply Chains

Military connectors are small parts, but they are essential in important electronics for safety and mission success. As a result, the standards for authenticity, traceability, and controlled sourcing are strict. Defense programs increasingly demand detailed documentation of a product's history. Any weak link, such as brokers, gray-market sourcing, or poor chain of custody, increases the risk of suspicious or counterfeit parts. This can lead to the need for re-testing and rework. For suppliers and integrators, these problems lead to higher quality assurance costs, longer procurement cycles, and delays in supplier qualification. This is especially troubling when demand rises and lead times shorten.

- In February 2024, the U.S. Department of Defense issued DoDI 4140.67, titled DoD Counterfeit Prevention Policy. This policy details the responsibilities for preventing counterfeit material in the DoD supply chain, emphasizing special requirements for electronic parts.

Impact of Russia Ukraine War

Russia-Ukraine war Accelerating Military Connectors Industry through Increased Defense Funding and Faster Modernization

As governments buy more radars, air defense systems, tactical radios, electronic warfare suites, drones, vehicles, and spare parts, the demand for connectors grows. Each upgrade requires more boxes, cables, and interfaces. The situation on the ground pushes buyers toward sealed, shielded, and vibration-tolerant connectors that can handle mud, cold, salt fog, and electromagnetic interference. Europe shows the strongest demand shock.

SIPRI points to the invasion as a reason for the spending spike in 2022. European military spending jumped 13% in 2022, and global spending is expected to reach USD 2,718 billion in 2024, reflecting a 9.4% year-over-year increase, the largest rise since at least 1988. On the supply side, the war has also changed market dynamics. Sanctions and export controls have made it harder to access certain electronics and dual-use items. This situation places more focus on traceability, approved sourcing, and local or allied supply chains.

The European Defense Agency reports record EU defense spending, such as €343 billion in 2024, which is significantly higher than in 2023. This trend shows a continued need for modernization that ensures connectors are consistently required across programs and retrofits.

Segmentation Analysis

By Product Type

Due to Standardization and Need for Reliability in Harsh Environments, Circular Connectors Segment leads Market

In terms of product type, the market is categorized into circular connectors, rectangular connectors, RF/coax connectors, fiber-optic connectors, and others.

Circular connectors dominate the market in 2025, and this segment is the preferred choice in military electronics as they can handle real operational challenges. These challenges include vibration, shock, sealing needs, extreme temperatures, and frequent connections and disconnections during maintenance. They are favored as programs prefer predictable, qualified building blocks. Circular families, especially high-density, quick-disconnect designs, are commonly specified for air, land, and naval platforms. This makes them easier to source, qualify, and support over long service lives. In short, when a system needs to maintain power and signals in tough conditions, circular connectors are the reliable option. That is why they hold the largest market share.

- In January 2026, the U.S. Defense Logistics Agency (DLA) Land and Maritime maintained and published the MIL-DTL-38999 general specification for electrical, circular, miniature, high-density, quick-disconnect connectors. This includes environment-resistant and hermetically sealed versions. This highlights why this family of circular connectors remains a key, standardized backbone across DoD systems.

Fiber-optic connectors segment in the market is expected to show fastest grow at a CAGR of 10.7% over the forecast period.

By Platform

Land Platform Segment leads Market as of Large Vehicle Fleets and Ongoing Vetronics Upgrades

On the basis of platform, the market is classified into airborne (manned & unmanned systems), land, naval, C4ISR infrastructure, and space & strategic.

Land segments hold the largest share of the market in 2025, as land forces depend on volume. Armored vehicles, tactical trucks, air-defense launchers, artillery systems, and mobile command posts create a vast installed base that frequently updates communications, navigation, electronic warfare protection, sensors, and power distribution. Each upgrade adds or renews harnessing and interfaces. Connectors are installed widely, not only for new builds but also for retrofits and depot maintenance.

Space & strategic is expected to show fastest military connectors market growth at a CAGR of 8.2% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Application

Due to Network-centric Warfare and Need for Constant Connectivity, C4ISR and Tactical Communications lead Market

Based on application, the market is segmented into C4ISR & tactical communications, radar & electronic warfare, avionics & mission computers, weapon systems, vehicle vetronics, propulsion & powertrain, and others.

C4ISR & tactical communications segment holds the largest military connectors market share. Modern operations rely on the network. Quickly delivering voice, data, video, targeting, blue-force tracking, and sensor feeds to the right location is essential, even in jamming and difficult environments. This reality makes C4ISR and tactical communications the largest user of connectors. It leads to more radios, gateways, SATCOM terminals, datalinks, and edge computing nodes on every platform. There are ongoing updates as waveforms, encryption, and bandwidth needs change. More network nodes mean more rugged interfaces for power, data, and RF/optical.

- In September 2024, the NATO Support and Procurement Agency (NSPA) awarded SES a multi-year contract to provide secure, high-performance, low-latency satellite connectivity for NATO member governments and military users. This contract strengthens the ongoing development of tactical and operational communications infrastructure.

Loitering munitions is the fastest growing segment in the market at a CAGR of 17.1% across the forecast period.

By Connectivity Function

Due to Old Platform Structures and Specific Control Needs Low-speed Signal and Control Segment leads Market

Based on connectivity function, the market is segmented into power, low-speed signal/control, high-speed data, RF, optical (fiber), and mixed/hybrid (power & data & RF).

Low-speed signal/control segments dominate the market. In defense platforms, much of the mission-critical control setup still relies on low-speed signals, discrete I/O, control lines, and established low-speed buses. These options are dependable, easy to validate, and trusted for long service lives. Even when new systems include high-speed links, they often keep low-speed control paths for safety-critical functions, actuator control, subsystem status monitoring, and predictable command and response behavior. The large installed base across aircraft, vehicles, ships, and ground vehicles C4ISR shelters maintains low-speed signal and control as the main volume leader for connectors.

The optical (fiber) segment consists of hydrogen and solar based fuel type is expected to show fastest market growth at a CAGR of 11.5% across the forecast period.

Military Connectors Market Regional Outlook

Due to U.S.'s Large Spending on Defense Electronics and its Extensive Installed Base, North America leads Market

By region, the market is categorized into North America, Europe, Asia Pacific, and Rest of the World.

North America

North America Military Connectors Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America is at the forefront as the region’s demand is driven by the U.S., which is by far the world’s biggest military spender. That funding consistently supports programs that focus on electronics, such as C4ISR networks, electronic warfare, radar upgrades, missiles, avionics updates, and vehicle and ship restorations. This mix creates a steady need for rugged connectors in new projects and maintenance, including repairs, spare parts, and retrofits. Canada contributes a smaller but consistent demand through NATO-related modernization, but the primary force is the scale and speed of military grade communications equipment in the U.S.

- In April 2025, SIPRI reported that U.S. military spending reached about USD 997 billion in 2024, making it the largest in the world. The global military spending totaled USD 2,718 billion. This shows the scale advantage that keeps North America as the main hub for defense electronics and related hardware.

U.S. Military Connectors Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market value can be analytically approximated at around USD 1.02 billion in 2025, increasing at a CAGR of 4.7%.

Europe

During the forecast period, the Europe region is projected to have a CAGR of 8.1%. The market in Europe was valued at around USD 0.78 billion in 2025. Europe is undergoing a major rearmament and modernization cycle. This situation is increasing the demand for connectors due to vehicle upgrades, air-defense systems, electronic warfare and radar updates, and the quick deployment of communication kits. The focus is slowly changing from basic rugged power and signal connections to shielded, sealed, higher-density, and higher-speed interconnects. The region wants to make platforms more resilient in tough electronic warfare environments and better able to adapt over time. Russia is part of the European scene, which drives the area toward improved sustainability and repair or retrofit efforts, not just new purchases.

U.K. Military Connectors Market

The U.K. market value reached approximately USD 0.11 billion in 2025, equivalent to around 7.2% of Europe’s military connectors revenues.

Germany Military Connectors Market

The Germany market value in 2025 was around USD 0.15 billion, representing roughly 9.3% of Europe military connectors revenues.

Asia Pacific

Asia Pacific is anticipated to be the second fastest growing segment in the global market growing at a CAGR of 7.0%. Asia Pacific is working to modernize its naval and air forces significantly. There is also a strong push for network-based C4ISR systems, missiles, and space connectivity. This change is contributing to a faster trend toward high speed data, RF, and fiber connections. This is particularly important for radar, electronic warfare, datalinks, and ship combat systems, where bandwidth and resistance to electromagnetic interference are vital. Another regional factor is local production, especially from China, India, Korea, Japan, and Australia. This raises the demand for qualified local and allied interconnect solutions and accelerates standardization in domestic programs.

China Military Connectors Market

China’s market for military connectors is projected to be one of the largest in Asia Pacific, with 2025 revenues at around USD 0.26 billion, representing roughly 40.18% of Asia Pacific military connectors sales.

India Military Connectors Market

The Indian market in 2025 was valued at around USD 0.11 million, accounting for roughly 17.44% of Asia Pacific military connectors revenues.

Rest of the World

Rest of World (Middle East & Africa and Latin America), has comparatively smaller in share but is growing at a CAGR of 6.3%. Rest of World demand is more driven by specific programs. This includes air-defense and radar purchases, upgrades to tactical communications, and selected improvements to aircraft, armored vehicles, and border or coastal surveillance. The region often prefers durable circular and low-speed/control connectivity as many platforms rely on maintenance or are imported. However, you can find areas with higher demand for RF and fiber wherever ISR, air-defense, and electronic warfare are growing. The main factor influencing this is procurement cycles and readiness needs. As a result, volumes can vary greatly from year to year, even if the long-term trend is upward.

Latin America Military Connectors Market

The Latin America market value in 2025 was around USD 0.09 million, accounting for roughly 26.44% of rest of the world military connectors revenues.

Middle East & Africa Military Connectors Market

Middle East & Africa is projected to be one of the largest region in the rest of the world, with 2025 revenues at around USD 0.25 billion, and the Middle East & Africa market value is expected to reach USD 0.39 billion in 2034, representing roughly 73.56% of rest of the world military connectors sales.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Concentration remains High, while Specialist Gain Share in High-Speed, RF/fiber, and Hybrid Interconnects

The market consists mainly of large general interconnect suppliers and specialized high-spec firms. Defense customers prioritize qualification, reliability, and long-lasting support over just the lowest price. Major companies thrive by offering a wide range of durable circular and rectangular connector families. They maintain consistent quality and support long-term programs and spare parts. This group includes names such as Amphenol, TE Connectivity (DEUTSCH), ITT Cannon, Eaton/Souriau, and Smiths Interconnect, along with other well-known aerospace and defense connector brands. Their strength comes from their size, allowing them to support prime contractors across different platforms, regions, and qualification standards without risking supply.

High competition is at the edges, particularly in high speed data, RF, fiber, miniaturization, hybrid power and data, and harsh-environment sealing and EMI performance. Amphenol, TE Connectivity, ITT Cannon, Eaton (Souriau), and Smiths Interconnect lead the market for high performance connectors. These connectors are used in command centers, electronic warfare, and communication equipment, including rugged rectangular and circular types. Other top companies include specialists such as Glenair, Radiall, HUBER+SUHNER, Rosenberger, and Fischer Connectors. They focus on various data transmission needs, such as high-speed, RF/coax, fiber, and hybrid interconnects.

LIST OF KEY MILITARY CONNECTORS COMPANIES PROFILED

- Amphenol Corporation (U.S.)

- TE Connectivity Ltd. (Switzerland)

- ITT Inc. (U.S.) (Cannon)

- Eaton Corporation plc (Ireland) (Souriau)

- Radiall (France)

- Glenair, Inc. (U.S.)

- Smiths Group plc (U.K.) (Smiths Interconnect)

- HUBER+SUHNER AG (Switzerland)

- Rosenberger Group (Germany)

- LEMO S.A. (Switzerland)

- Fischer Connectors SA (Switzerland)

- Carlisle Interconnect Technologies (U.S.)

- Bel Fuse Inc. (U.S.)

- Cinch Connectivity Solutions (U.S.) (Bel)

- Molex, LLC (U.S.)

- Samtec, Inc. (U.S.)

- Harwin plc (U.K.)

- Japan Aviation Electronics Industry, Ltd. (JAE) (Japan)

- Hirose Electric Co., Ltd. (Japan)

- Sumitomo Electric Industries, Ltd. (Japan)

KEY INDUSTRY DEVELOPMENTS

- October 2025: Smiths Group announced the sale of Smiths Interconnect to Molex, a Koch company, for an enterprise value of GBP 1.30 billion. This sale reflects a multiple of 15.1 times the expected FY2025 EBITDA of GBP 86.10 million and is expected to close in the second half of FY2026.

- August 2025: Amphenol announced plans to acquire Trexon for about USD 1.00 billion in cash. Amphenol stated that Trexon specializes in high-reliability interconnects and cable assemblies mainly for the defense market, with facilities in the U.S. and U.K. Trexon expects around USD 290.00 million in sales for 2025 and a 26% EBITDA margin. The acquisition is targeted for completion in Q4 2025 and will be reported under Harsh Environment Solutions.

- March 2025: Cinch Connectivity Solutions launched Trompeter Space Grade TRB/TRT (miniature) and TTM/TRS (subminiature) connectors designed for military and commercial space missions. The announcement noted compliance with NASA outgassing requirements and compliance with MIL-STD-1553B data bus standards.

- October 2024: USAspending listed PIID SPE7M025P0600 awarded to Winchester Interconnect RF Corporation for ADAPTER, CONNECTOR under PSC 5935 (Electrical Connectors), with USD 10,836.00 obligated. The contract began on 21 Oct 2024 and will end on 21 Apr 2025.

- September 2024: A U.S. DoD contract action on USAspending showed Cinch Connectivity Solutions Inc. with a transaction date of 20 Sep 2024 and a total obligation of USD 14,436.00. This is common for replenishment and sustainment purchases, where small connector lots help maintain and repair operations smoothly.

- February 2024: The U.S. DoD issued DoDI 4140.67, titled DoD Counterfeit Prevention Policy and dated 1 Feb 2024. This policy outlines responsibilities and expectations for preventing, detecting, resolving, and seeking restitution for counterfeit materials across the defense supply chain. This is crucial for connectors, where traceability, quality assurance, and approved sourcing are vital.

- September 2023: DLA Land & Maritime published MIL-DTL-38999 Revision N, along with Amendment 1. This specification covers high-density, quick-disconnect circular connectors, including environment-resistant models with removable crimp contacts and hermetic versions with fixed solder contacts. This update requires OEMs and suppliers to review their compliance, test plans, and qualification status for programs using 38999-class connectors.

- August 2023: The U.S. Department of Justice announced that Amphenol would pay USD 18.00 million to settle allegations under the False Claims Act. The claims involved the sale of military connectors that allegedly did not fully meet testing standards and other program or manufacturing requirements.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.2% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product Type · Circular connectors · Rectangular connectors · RF/coax connectors · Fiber-optic connectors · Others |

|

By Platform · Airborne (Manned & Unmanned Systems) · Land · Naval · C4ISR infrastructure · Space & strategic |

|

|

By Application · C4ISR & tactical communications · Radar & electronic warfare · Avionics & mission computers · Weapon systems · Vehicle vetronics · Propulsion & powertrain · Others |

|

|

By Connectivity Function · Power · Low-speed signal / control · High-speed data · RF · Optical (fiber) · Mixed / hybrid (power & data & RF) |

|

|

By Region

o China (By Product Type) o India (By Product Type) o Japan (By Product Type) o South Korea (By Product Type) o Australia (By Product Type)

o Latin America (By Product Type) · Middle East & Africa (By Product Type) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 3.12 billion in 2026 and is projected to reach USD 5.05 billion by 2034.

In 2025, the market value stood at USD 1.10 billion.

The market is expected to exhibit a CAGR of 6.2% during the forecast period.

The circular connectors led the market by product type.

The rising global defense spending is driving steady demand for rugged military connectors.

Amphenol, TE Connectivity, ITT Cannon, Eaton (Souriau), and Smiths Interconnect for broad rugged interconnect portfolios, alongside specialists such as Glenair, Radiall, HUBER+SUHNER, Rosenberger, and Fischer Connectors, among others are the top companies in the market.

North America dominated the market in 2024.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us