Pea Processed Ingredients Market Size, Share & Industry Analysis, By Product Type (Pea Flour, Pea Starch, Pea Fiber, and Pea Protein{Isolates, Concentrates, and Textured}), By Nature (Organic and Conventional), By Application (Food & Beverages {Meat Substitutes, Functional Foods, Snacks, Bakery & Confectionery, Beverages, and Others}, Dietary Supplements & Nutraceuticals, Personal Care & Cosmetics, and Others), By Source (Yellow Pea, Green Pea, Chickpeas, and Others), By Distribution Channel (Offline and Online), and Regional Forecast, 2026-2034

(Offer valid till 31st Jul 2026)

KEY MARKET INSIGHTS

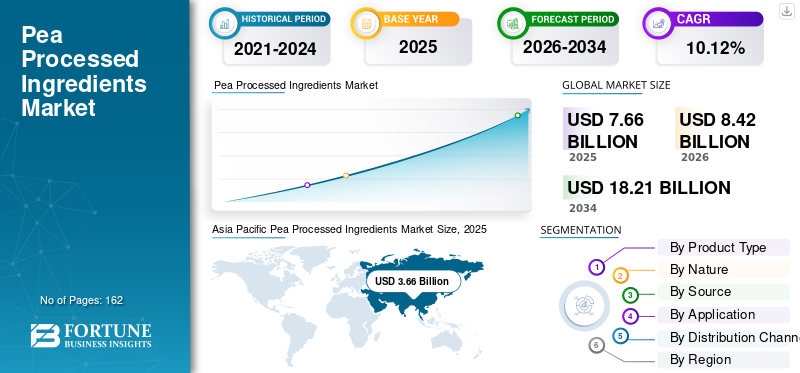

The global pea processed ingredients market size was valued at USD 7.66 billion in 2025. The market is projected to grow from USD 8.42 billion in 2026 to USD 18.21 billion by 2034, exhibiting a CAGR of 10.12% during the forecast period. Asia Pacific dominated the global pea processed ingredients market with a market share of 47.78% in 2025.

Pea processed ingredients are functional ingredients extracted from raw peas, including flour, starch, fiber, and protein, through dry milling, air classification, and wet processing methods. The growing adoption of plant-based diets is a primary driver of demand for these products. Additionally, the increasing demand for allergen-free, high-protein, non-GMO, and rich-nutrient foods among millennials and Gen-Z consumers is expected to drive product demand in the global market. Furthermore, increasing use of pea-based ingredients in cosmetics, personal care, pet food, and other industrial applications is positively influencing market growth.

Emsland Group, Kerry Group, DuPont, Roquette Frères, and Ingredion Inc. are key market players in the market, shaping the industry through diversified strategies such as product launches, base expansions, mergers and acquisitions, and marketing activities.

Download Free sample to learn more about this report.

PEA PROCESSED INGREDIENTS MARKET TRENDS

Allergen-Free Protein Consumption to Change Industry Outlook

Consumers are increasingly conscious of health and wellness, leading them to seek protein sources such as pea protein, which is perceived as healthier or necessary due to dietary restrictions. Furthermore, the rising number of individuals with food allergies and intolerances to whey and soy is increasing the traction for pea-based protein products in the market. To capitalize on the upcoming trend, manufacturers are continually improving taste, texture, and functionality, especially in areas such as sports nutrition and ready-to-drink beverages, to make allergen-free options more appealing. Thus, the emerging allergen-free market trend is anticipated to change the global pea processed ingredients market landscape in the near future.

- According to the FARE (Food Allergy Research & Education), an organization dedicated to improving the quality of life and health, nearly 1.9 million adults are allergic to soy, while 6.2 million adults are allergic to milk and peanuts.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Plan-Based Food Demand to Drive Global Market Growth

One of the key drivers in the current food and beverages industry is the rising demand for plant-based and clean-label products. Plant-based food popularity is drastically shifting with several factors, including rising health consciousness, environmental concerns, and ethical & animal welfare concerns, coupled with significant innovation making products taste better, increased availability, and cultural shifts. Pea processed ingredients are one of the key elements widely used in vegan foods since they have high protein content and excellent functional properties such as texturizing, emulsifying, and stabilizing capacity, thereby driving the global pea processed ingredients market growth.

- According to the CBI.EU., the plant-based foods and beverages sales in key European countries, including Germany, Spain, Italy, France, the U.K., and the Netherlands, accounted for USD 5.84 billion in 2023, an increase of nearly 5.5% from 2022.

MARKET RESTRAINTS

Functional Limitations to Hamper Market Growth

The pea processed ingredients market faces several functional and economic challenges. Compared to conventional ingredients such as soy protein, wheat flour, or corn starch, pea-based ingredients often present functional constraints, including lower solubility, taste differences, and textural limitations, particularly in bakery, dairy-alternative, and beverage formulations. Additionally, raw materials are expensive compared to whey and soy. High raw material cost directly affects the final price of the product. Furthermore, the processing technologies are expensive, which increases the final product price. It will hamper the small-scale industry players such as food & beverage manufacturers, cosmetics producers, and others.

MARKET OPPORTUNITIES

Adoption of Plant-Sourced Ingredients in Cosmetics & Personal Care Industry to Drive Market Growth

The cosmetics industry is increasingly adopting pea-based products due to rising consumer demand for natural, sustainable, and plant-derived ingredients, coupled with the beneficial functional and cosmetic properties of pea extracts and proteins. Additionally, pea-based ingredients align well with the growing emphasis on clean-label, vegan, and allergen-free cosmetics, as they provide an effective alternative to animal-derived or synthetic components. Thus, key players are introducing new products to strengthen their presence in this category. This trend will change the industry landscape over the upcoming years.

- For instance, in April 2024, Roquette Beauté, a cosmetics ingredients manufacturing wing of Roquette Frères, launched a ned plant-based cosmetics ingredient - Roquette® ST 730 INCI Hydroxypropyl Starch made from pea starch for skincare and makeup products.

Segmentation Analysis

By Product Type

Wider Applications Boosted the Pea Starch Segment Growth

By product type, the market is segmented into pea flour, pea starch, pea fiber, pea protein. Pea protein is further segmented into isolates, concentrates, and textured.

Pea starch dominated the market, accounting for a 32.88% share in 2025. The product is extensively used as a clean-label thickener, binder, and texturizer in soups, sauces, ready meals, bakery, snacks, and in non-food industrial applications such as cosmetics, paper, adhesives, and textiles. These applications are volume-intensive, driving higher overall consumption compared to other pea fractions.

The pea protein segment is anticipated to rise with a CAGR of 11.36% over the forecast period.

By Nature

Low Price and High Availability Encouraged the Conventional Segment Growth

Based on nature, the market is segmented into organic and conventional.

The conventional segment held the largest market share, with a value of 76.54% in 2025. The dominance is driven by cost-effectiveness, large-scale availability, and established supply chains. Most commercial pea protein, starch, flour, and fiber used in food processing are sourced from conventionally grown peas, as they allow manufacturers to achieve consistent quality, higher yields, and stable pricing.

The organic segment is projected to grow at a CAGR of 10.82% over the forecast period.

By Application

Wide Acceptability of the Product in the Food & Beverages Application Led to the Dominance of the Segment

Based on application, the market is segmented into food & beverages, dietary supplements & nutraceuticals, personal care & cosmetics, and others. The food & beverages segment is further sub-segmented into meat substitutes, functional foods, snacks, bakery & confectionery, beverages, and others.

The food & beverages segment dominated the global market in 2025, with a share of 77.51%. Pea starch is widely applied as a clean-label thickener and binder in soups, sauces, ready meals, bakery, and snacks, while pea protein is a core ingredient in plant-based meat, dairy alternatives, and protein-fortified foods. Pea flour and fiber further support texture, nutrition, and clean-label positioning. Therefore, the segment is anticipated to dominate the market by the end of 2034 with the highest market share.

The dietary supplements & nutraceuticals are expected to grow at a CAGR of 10.68%, driven by the rising demand for allergen-free protein options and increasing new product launches in the market.

To know how our report can help streamline your business, Speak to Analyst

By Source

High Starch and Protein Content of the Yellow Pea Dominated the Segment

Based on source, the market is segmented into yellow pea, green pea, chickpeas, and others.

The yellow pea segment dominated the global market in 2025, with a share of 57.96%. Yellow pea contains high starch and protein yields, neutral flavor, consistent quality, and excellent suitability for wet fractionation, making it ideal for producing pea protein, starch, and fiber. Additionally, it is predominantly produced in the U.S., Canada, and Asian countries, making it a stable supply, cost-effective, and scalable. Thus, the segment holds the highest market share.

The chickpeas are expected to grow at a CAGR of 9.83% during the forecast period from 2026 to 2034.

By Distribution Channel

High Market Accessibility and Wide Presence to Drive the Offline Channels Growth

Based on the distribution channel, the market is segmented into online and offline.

The offline segment dominated the global market in 2025, with a share of 78.91%. The offline channels are offering more convenience and accessibility to both food service providers, food processors, cosmetics manufacturers, industrial players, and consumers. Furthermore, these channels offer bulk purchase and more options for price negotiation. Thus, the segment is anticipated to grow with a steady CAGR during the forecast period.

The online segment is expected to grow at a CAGR of 10.73% over the forecast period (2026-2034).

Pea Processed Ingredients Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Pea Processed Ingredients Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific market held the dominant share in 2025, valued at USD 3.66 billion, and also maintained its leading share in 2026, at 47.97%. Emerging Western diet practices, growing vegan diets, urbanization, working women’s rate, and the rapid expansion of bakery, snacks, and foodservice industries in China, India, and Japan are likely to drive market growth. Increasing pea production in Asian countries is also contributing to market growth in the near future.

- According to the Government of India’s data, pea production in the Rabi 2025 reached 10 lakh tonnes.

Japan Pea Processed Ingredients Market

In Japan, the market in 2026 is estimated to be around USD 0.31 billion and is anticipated to grow at a CAGR of 9.43% during the forecast period. Growth is supported by increasing adoption of Western-style bakery products, dairy alternatives, and functional foods.

China Pea Processed Ingredients Market

China’s market is projected to reach USD 1.45 billion by the end of 2026. The market popularity is driven by rising consumption of convenience foods, premium bakery products, and plant-based alternatives. Expansion of café culture, international bakery chains, and fusion cuisine has significantly increased demand for pea protein and starch across both foodservice and retail channels.

India Pea Processed Ingredients Market

In India, the market in 2025 is valued at around USD 0.99 billion, accounting for roughly 12.98% of the global market share in 2025.

North America

In North America, the pea processed ingredients market was valued at USD 1.41 billion in 2025 and is expected to grow at a CAGR of 10.15% during the forecast period. Pea processed ingredients are widely used in multiple food & beverage applications, including meat alternatives, dairy alternatives, RTE snacks, and other food products. Increasing vegan diet and allergen-free protein product demand are significantly influencing market growth.

U.S. Pea Processed Ingredients Market

The U.S. pea processed ingredients market in 2025 is estimated at around USD 0.95 billion, representing roughly 12.39% of the global pea processed ingredients market revenues. Increasing on-the-go-snacks, weight management snacks, and healthy dieting, coupled with flourishing vegan food popularity, contribute to the market growth. Key players in the industry are offering new products using pea-based ingredients to meet their consumer demand.

- For instance, in July 2024, Ingredion Incorporated, a global player offering specialty ingredients to the food and beverages industry, launched VITESSENCE® Pea 100 HD, a pea protein optimized for cold-pressed bars. It aimed to meet consumers’ on-the-go breakfast, meal replacement, snack, or pre-and post-workout requirements.

Europe

In Europe, the pea processed ingredients market is valued at USD 1.86 billion in 2025 and secures the position of the second-largest region in the market. Germany, France, and the U.K. hold the highest proportion of the regional market, driven by the friendly regulatory acceptances and guidelines for plant-based food, coupled with growing allergen-free bakery, snacks, and beverage products. Furthermore, increasing new products with allergen-free and label-friendly products in the regional food industry is likely to propel the market in the upcoming years.

- According to the European Court of Auditors (ECA) Special Report on Food Labelling in the EU, published in November 2024, over 12% of new food product launches in Europe include sustainability claims, such as organic, natural, and clean-label, reinforcing the demand for pea-derived ingredients.

Germany Pea Processed Ingredients Market

The Germany pea processed ingredients market in 2026 is estimated to be around USD 0.52 billion and is anticipated to grow at a CAGR of 10.60% during the forecast period. The growing demand for the product is supported by the country’s strong bakery product consumption, emerging popularity for ready meals, and plant-based meat products. The increasing bakery and RTE food product industry in the country is likely to push market growth.

- According to the Central Association of the German Bakery Trade, the German bakery industry is expected to record 2% growth in 2025, reaching approximately USD 19.39 billion, positively influencing demand for functional pea-based ingredients.

South America and the Middle East & Africa

The South America and Middle East & Africa regions are expected to witness moderate growth in the market during the forecast period. The market in South America was valued at USD 0.48 billion in 2025, and it is expected to grow at a CAGR of 9.11% during the forecast period (2026-2034). In the Middle East & Africa, the pea processed ingredients market was valued at USD 0.25 billion in 2025, and it is expected to reach USD 0.46 billion by 2034, registering a CAGR of 7.03% during the forecast period.

UAE Pea Processed Ingredients Market

The pea processed ingredients market in the UAE is projected to reach approximately USD 0.02 billion in 2025, driven by the rapid expansion of the foodservice, bakery, and hospitality sectors. Furthermore, the adoption of Western culture and the emerging popularity of allergen-free products in QSRs and RTE food are further contributing to market growth.

COMPETITIVE LANDSCAPE

Key Industry Players

Major Players Focus on New Product Launches to Secure Strong Market Presence

The global pea processed ingredients market share exhibits a moderately consolidated nature with the presence of a few dominant players. Emsland Group, Kerry Group, DuPont, Roquette Frères, and Ingredion Inc. are key players holding a considerable market share in 2025. The leading companies in the global pea processed ingredients market are focusing on advancements in product development, new product launches, expanding distribution channels, acquisitions, and collaborations to meet the growing clean-label trends in the market.

LIST OF KEY PEA PROCESSED INGREDIENTS COMPANIES PROFILED

- Kerry Group PLC (Ireland)

- Emsland Group (Germany)

- DuPont (U.S.)

- Roquette Frères (France)

- Ingredion Inc. (U.S.)

- Cosucra Groupe Warcoing SA (Belgium)

- AGT Food and Ingredients (Canada)

- Puris Foods (U.S.)

- Cargill Inc (U.S.)

- Meelunie B.V. (Netherlands)

KEY INDUSTRY DEVELOPMENTS

- October 2025: Roquette, a global leader in plant-based ingredients and a pioneer in sustainable food innovation, launched AMYSTA™ L 123 thermally soluble pea starch to meet the growing demand for clean-label ingredients for ready-to-mix beverages, dried soup, sauce, and condiment mixes.

- June 2025: Roquette Freres, a global specialty ingredients manufacturer, launched two textured solutions under its NUTRALYS® plant protein category, NUTRALYS® T WHEAT 600L and NUTRALYS® T PEA 700XC. These two products are made from wheat and pea, desgned for produce chicken-style alternatives.

- December 2024: Burcon NutraScience Corporation, a global technology company in the development of plant-based proteins for foods and beverages, launched high-purity and clean-tasting Peazazz®C pea protein designed for the growing plant-based protein market.

- November 2024: Axiom Foods, a supplier of rice, pea proteins, and other plant-based ingredients, expanded its product portfolio by launching a new pea protein called Pea Protein Vegotein N.

- February 2024: Wednesday, Louis Dreyfus Company, a global merchant and processor of agricultural goods, opened a new pea protein isolate production plant at the site in Yorkton, Canada. The company spent USD 500 million to construct the new plant and completed the operation in 2024.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 10.12% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product Type, Nature, Source, Application, Distribution Channel, and Region |

|

By Product Type |

· Pea Flour · Pea Starch · Pea Fiber · Pea Protein o Isolates o Concentrates o Textured |

|

By Nature |

· Conventional · Organic |

|

By Application |

· Food & Beverages o Meat Substitutes o Functional Foods o Snacks o Bakery & Confectionery o Beverages o Others · Dietary Supplements & Nutraceuticals · Personal Care & Cosmetics · Others |

|

By Source |

· Yellow Pea · Green Pea · Chickpeas · Others |

|

By Distribution Channel |

· Online · Offline |

|

By Region |

· North America (By Product Type, Nature, Source, Application, Distribution Channel, and Country) o U.S. (By Distribution Channel) o Canada (By Distribution Channel) o Mexico (By Distribution Channel) · Europe (By Product Type, Nature, Source, Application, Distribution Channel, and Country/Sub-region) o Germany (By Distribution Channel) o U.K. (By Distribution Channel) o France (By Distribution Channel) o Spain (By Distribution Channel) o Italy (By Distribution Channel) o Rest of Europe (By Distribution Channel) · Asia Pacific (By Product Type, Nature, Source, Application, Distribution Channel, and Country/Sub-region) o China (By Distribution Channel) o Japan (By Distribution Channel) o India (By Distribution Channel) o Australia (By Distribution Channel) o Rest of Asia Pacific (By Distribution Channel) · South America (By Product Type, Nature, Source, Application, Distribution Channel, and Country/Sub-region) o Brazil (By End-Use) o Argentina (By End-Use) o Rest of Latin America (By End-Use) · Middle East & Africa (By Product Type, Nature, Source, Application, Distribution Channel, and Country/Sub-region) o UAE (By Distribution Channel) o South Africa (By Distribution Channel) o Rest of Middle East & Africa (By Distribution Channel) |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 7.66 billion in 2025 and is projected to reach USD 18.21 billion by 2034.

In 2025, the market value stood at USD 3.66 billion.

The market is expected to exhibit a CAGR of 10.12% during the forecast period (2026-2034).

By product type, the pea starch segment is expected to lead the market.

Increasing plan-based food demand is the key factor driving global market growth.

Emsland Group, Kerry Group, DuPont, Roquette Frères, and Ingredion Inc. are the major players in the global market.

Asia Pacific dominated the market in 2025.

Allergen-free protein consumption is the key trend in the industry.

- 2021-2034

- 2025

- 2021-2024

- 162

-

(Offer valid till 31st Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us