PET Preforms Market Size, Share & Industry Analysis, By Type (Virgin PET Preforms, Recycled-content PET Preforms, Multilayer PET Preforms, and Others), By End-use Industry (Beverages, Food, Personal Care & Cosmetics, Pharmaceuticals, and Others), and Regional Forecast, 2026-2034

PET Preforms Market Size and Future Outlook

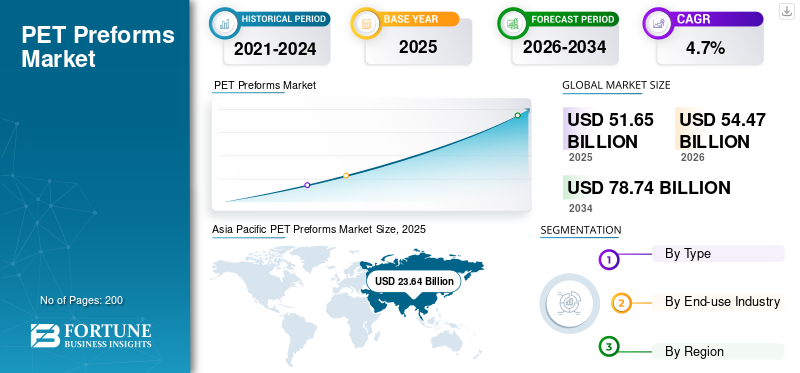

The global PET preforms market size was valued at USD 51.65 billion in 2025. The market is projected to grow from USD 54.47 billion in 2026 to USD 78.74 billion by 2034, exhibiting a CAGR of 4.7% during the forecast period. Asia Pacific dominated the PET preforms market with a market share of 45.76% in 2025

PET preforms are injection-molded intermediate packaging components manufactured from Polyethylene Terephthalate (PET) resin and subsequently transformed into containers via blow molding. These preforms are extensively used in PET packaging and are vital for producing PET bottles and jars in the beverage industry, as well as in food, personal care, household products, and specific pharmaceutical applications. The PET preform industry caters to a diverse array of products including bottled water, carbonated soft drinks, juices, edible oils, sauces, liquid detergents, and selected alcoholic beverages, contingent upon packaging design and regulatory compliance.

The market is primarily sustained by the increasing global consumption of packaged beverages and the ongoing transition toward lightweight, recyclable plastic containers. Demand remains notably robust in the soft drink and water packaging sectors, where PET continues to offer benefits such as transparency, durability, cost-effectiveness during transportation, and recyclability. Given that each PET bottle originates from a preform, the growing use of PET bottles in both mass-market and premium packaging solutions consistently drives up global demand for PET preforms.

Furthermore, the market consists of both large, integrated packaging corporations and specialized regional converters. Principal industry participants include ALPLA, Plastipak, Resilux, Retal Industries, Hon Chuan, and Amcor, among others. Their competitive advantages stem from expertise in lightweighting, custom neck-finish design, compatibility with recycled materials, and robust regional production capabilities. Consequently, the market continues to witness product innovation, geographic expansion, and the development of customer-specific packaging solutions across both beverage and non-beverage sectors.

Download Free sample to learn more about this report.

PET Preforms Market KEY TAKEAWAYS

- 2025 Market Size: USD 51.65 billion

- 2026 Market Size: USD 54.47 billion

- 2034 Forecast Market Size: USD 78.74 billion

- CAGR: 4.7% from 2026–2034

- Asia Pacific dominated the market with a 45.76% share in 2025.

- Recycled-content PET preforms segment is projected to grow at the fastest CAGR of 7.9%.

- Personal care & cosmetics segment is projected to grow at a CAGR of 5.6%.

Asia Pacific

USD 23.64 billion in 2025. High beverage consumption, large-scale PET bottle manufacturing, and expanding packaged consumer goods demand drive regional growth.

Europe

USD 10.85 billion by 2026. Sustainability regulations and growing adoption of recycled PET support market growth.

North America

Strong regional market supported by bottled beverages, branded food packaging, and established PET recycling systems.

U.S.

USD 3.58 billion by 2026. Demand is driven by bottled beverages, consumer packaged goods, and lightweight packaging innovations.

Japan

USD 2.70 billion by 2026. Demand is supported by the beverage industry and advanced PET packaging applications.

Read More

PET PREFORMS MARKET TRENDS

Sustainable PET Packaging and Lightweight Bottle Design are Emerging as Core Market Trends

A major shift in the market is the increasing focus on sustainable PET packaging, especially lightweight bottle formats and preforms that can process higher levels of recycled PET. Brand owners, bottlers, and packaging converters are redesigning containers to reduce resin consumption, improve recyclability, and comply with tightening sustainability regulations. These market trends are reshaping product development priorities across the PET preform industry, particularly in regions with stricter circular packaging frameworks.

At the same time, converters are moving beyond commodity water bottles and developing application-specific solutions for carbonated soft drinks, hot-fill beverages, food containers, and personal care packaging. This trend is improving the industry's value profile, as specialty preforms often require more advanced engineering for weight distribution, neck finish, thermal resistance, and bottle performance during blow molding. As a result, product innovation is becoming an important differentiator in the market.

Another visible trend is regional diversification. While Asia Pacific remains the dominant manufacturing and consumption hub for global PET bottle packaging, demand is also expanding steadily in Latin America and the Middle East, where beverage bottling and consumer goods packaging are becoming increasingly sophisticated. This broadening geographic base is supporting long-term market expansion.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Expanding Beverage Bottling Activity and Growing Demand for PET Bottles are Accelerating Market Growth

The strongest driver of the market is the steady expansion of the global beverage industry, in which PET remains one of the most widely used rigid packaging materials. The continued rise in consumption of bottled water, juices, ready-to-drink teas, energy drinks, and carbonated soft drinks is driving demand for PET preforms. PET preforms are a necessary intermediate component in bottle production, making beverage packaging growth one of the significant drivers of market expansion.

Demand is particularly strong in soft drinks and water applications as PET bottles combine light weight, strength, shelf visibility, and transportation efficiency. In many countries, PET has become the preferred packaging format for mass-consumption beverages as it supports cost-effective large-scale production and fast filling-line operations. This is especially important in high-volume beverage markets where bottlers need consistent, lightweight, and scalable packaging solutions.

In addition, rising urbanization, convenience-led consumption, and changing retail patterns are strengthening the role of packaged liquid products in daily consumption. These trends are increasing the need for high-output preform manufacturing lines and strengthening the market's long-term growth outlook.

MARKET RESTRAINTS

Resin Cost Volatility and Rising Sustainability Compliance Requirements can Restrain Profitability

One of the main restraints in the market is its exposure to fluctuations in PET resin and recycled PET pricing. Since raw materials account for a large share of total preform production cost, swings in virgin resin, energy, and food-grade recycled material costs can significantly affect margins. This is especially challenging in high-volume standard product categories where pricing pressure is strong, and competition is intense.

A second restraint is the growing complexity of sustainability and recycling compliance. Beverage brand owners increasingly demand lighter bottles, higher recycled-content levels, and packaging designs optimized for collection and recycling. While these shifts create long-term opportunity, they also raise short-term production challenges for converters, who must invest in tooling, testing, and process adjustments to maintain quality during molding and bottle conversion.

Moreover, in some applications, such as food, household products, and selected alcoholic beverages, regulatory, performance, or customer-specific packaging requirements may limit standardization. This can increase production complexity and create additional validation work for converters serving multiple end-use markets.

MARKET OPPORTUNITIES

Specialty Packaging, Recycled PET Integration, and Regional Capacity Expansion are Creating New Opportunities

A major opportunity lies in developing higher-value specialty preforms for differentiated applications. While bottled water and standard beverage packaging remain the largest volume segments, there is a growing opportunity in categories such as sauces, edible oils, functional beverages, cosmetics, and personal care products. These segments often require stronger design support, differentiated neck finishes, and more customized bottle formats, allowing suppliers to move beyond standard commodity preforms.

Another important opportunity is the increasing integration of recycled PET in preform production. As brand owners and regulators push for more circular packaging, converters that can reliably process recycled resin while maintaining clarity, food-contact compliance, and mechanical consistency are likely to gain a strategic advantage. This is expected to become one of the most important competitive themes during the forecast period.

Geographically, new opportunities are also emerging in developing regions. While Asia Pacific remains the largest regional market, investment interest is also growing in Latin America, Africa, and the Middle East, where beverage bottling, consumer packaging, and local recycling systems are expanding. This offers room for new production lines, regional partnerships, and export-oriented growth strategies.

MARKET CHALLENGES

Product Standardization Limits and Processing Precision Continue to Challenge Suppliers

The market also faces technical and operational challenges. Although PET bottles appear standardized on the outside, preforms vary significantly in neck finish, weight, application, filling conditions, and end-use performance. This means suppliers must support multiple product configurations across water, food, hot-fill, household, and beverage applications, increasing mold complexity and production planning requirements.

Processing precision is another challenge. Since preforms must perform consistently during blow molding, even minor inconsistencies in resin quality, wall-thickness distribution, or injection parameters can affect the final bottle's performance. This is particularly important in lightweight bottles and pressure-resistant formats used for carbonated soft drinks, where structural integrity is critical.

Lastly, the market remains highly competitive, especially in standard high-volume beverage applications. Suppliers must balance cost efficiency with product quality, recycled-content capability, and customer-specific development needs, all while protecting profitability in a price-sensitive environment.

Segmentation Analysis

By Type

Strong Clarity, Mechanical Strength, and Process Consistency Contributed to Virgin PET Preforms Segmental Dominance

Based on type, the market is segmented into virgin PET preforms, recycled-content PET preforms, multilayer PET preforms, and others.

The virgin PET preforms segment accounted for the largest share of the market in 2025, supported by its strong clarity, mechanical strength, process consistency, and broad suitability across high-volume packaging applications. Virgin resin-based preforms remain widely used across the beverage industry, particularly for soft drinks, water, bottled water, juices, and carbonated soft drinks, where appearance, bottle strength, and reliable processing during blow molding are critical. In the global market, virgin PET remains the preferred material for applications requiring high transparency, stable intrinsic viscosity, and reliable food-contact compliance. Additionally, this segment is projected to grow at a 3.7% compound annual growth rate over the forecast period.

The recycled-content PET preforms segment is expected to grow at the fastest CAGR of 7.9% during the forecast period, driven by sustainability targets, regulatory pressure, and increasing brand-owner focus on circular PET packaging solutions. Demand is rising as beverage companies and packaging converters work to reduce virgin plastic usage and increase the recycled content of bottles. This is creating strong momentum for recycled-content preforms in bottled water, carbonated beverages, food packaging, and selected personal care applications, where environmental positioning is becoming an important purchase and branding factor.

By End-use Industry

To know how our report can help streamline your business, Speak to Analyst

Large Installed Base of Filling Lines and Bottle Conversion Capacity Led to Dominance of Beverages Segment

In terms of end-use industry, the market is categorized into beverages, food, personal care & cosmetics, pharmaceuticals, and others.

The beverages segment accounted for the largest PET preforms market share. The segment includes bottled water, juices, sports drinks, ready-to-drink products, and carbonated soft drinks, all of which rely heavily on PET bottles for convenience, light weight, and cost-effective distribution. The large installed base of filling lines and bottle conversion capacity across the global beverage industry continues to support this segment’s leadership.

The personal care & cosmetics segment is also emerging as an attractive growth area for PET preforms. These include packaging for shampoos, lotions, liquid soaps, and similar consumer products. Compared with standard beverage packaging, this category often involves greater design variation and a stronger emphasis on appearance, helping suppliers add value in the overall market. Furthermore, this segment is projected to grow at a 5.6% CAGR over the projected period.

Food is an important end-use segment for PET preforms, especially in packaging formats for edible oils, sauces, condiments, and other liquid or semi-liquid food products. PET offers transparency, break resistance, and design flexibility, making it attractive for both mainstream and premium retail packaging. This segment is smaller than beverages but continues to expand in line with packaged-food consumption.

PET Preforms Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific PET Preforms Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2024, the Asia Pacific region accounted for the largest share, valued at USD 22.84 billion, and continued to lead in 2025, valued at USD 23.64 billion, and is expected to remain dominant over the forecast period. The region benefits from high beverage consumption, large-scale PET bottle manufacturing, strong export-oriented packaging industries, and rising urban demand for packaged consumer products. China, India, and Southeast Asia remain central to both production and consumption growth in the regional market.

China PET Preforms Market

By 2026, the Chinese market is projected to attain a valuation of USD 76.28 billion. China is the largest market in the Asia Pacific for PET preforms, supported by its massive beverage industry, a large PET bottle production base, and strong demand for bottled water, carbonated soft drinks, edible oils, and personal care packaging. A rising focus on sustainability, adoption of recycled PET, and large-scale blow-molding capacity continue to strengthen China’s role in the global market.

To know how our report can help streamline your business, Speak to Analyst

Japan PET Preforms Market

The Japanese market is estimated to be around USD 2.70 billion in 2026, accounting for roughly 5.0% of the global revenues.

India PET Preforms Market

The Indian market is estimated at around USD 4.08 billion in 2026, accounting for roughly 7.5% of global revenues.

Europe

Europe is expected to experience substantial PET preforms market growth in the coming years. Over the forecast period, the region is projected to grow at an annual rate of 3.2%, reaching a market valuation of USD 10.85 billion by 2026. Europe represents a mature but strategically important market, driven by sustainability regulations, packaging redesign, and greater adoption of recycled PET. The region is seeing growing demand for lightweight and regulation-ready PET bottles, particularly in beverage and food applications. As a result, European suppliers are focusing more on circular packaging compatibility than purely volume-led growth.

U.K. PET Preforms Market

The U.K. market is estimated at around USD 1.62 billion in 2026, accounting for roughly 3.0% of global revenues.

Germany PET Preforms Market

Germany’s market is estimated at around USD 2.42 billion in 2026, accounting for roughly 4.4% of global revenues.

North America

North America remains a strong market supported by bottled beverages, branded food packaging, and established PET recycling systems. Demand continues to be supported by large consumer packaged goods companies and by ongoing innovation in lightweight packaging design. The region also remains important for premium and specialty bottle formats.

U.S. PET Preforms Market

Given the U.S. dominance in the region, the U.S. market is estimated at around USD 3.58 billion in 2026, accounting for roughly 6.6% of global sales.

Latin America and Middle East & Africa

Latin America is expected to witness steady growth in the market due to expansion in packaged beverages, cost-efficient PET bottle usage, and improving manufacturing infrastructure. The region has strong potential in water, juices, and soft drink packaging, particularly where PET remains a preferred packaging material due to affordability and distribution efficiency. The Latin America market is projected to reach USD 5.31 billion by 2026. The Middle East & Africa region is comparatively smaller but offers meaningful long-term growth potential. Rising demand for bottled water, improving consumer goods packaging capacity, and increasing investment in local packaging conversion are supporting market expansion. Over time, both domestic beverage production and recycling investments are expected to improve regional demand fundamentals.

GCC PET Preforms Market

The GCC market is estimated at USD 2.85 billion in 2026, accounting for approximately 5.2% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Product Customization, Sustainable PET Packaging, and Regional Reach are Defining Competition

The global market is moderately fragmented, with competition shaped by scale, product flexibility, recycled-content capability, and customer-specific design support. Companies are increasingly differentiated by their ability to deliver high-output production, lightweight bottle solutions, and sustainable PET packaging formats across multiple end uses. The ability to supply customized products, including water preforms, CSD preforms, food-grade formats, and non-beverage packaging, has become increasingly important.

Key players in the market include Retal Industries, ALPLA, Plastipak, Resilux, Hon Chuan, and Amcor, among others. These companies compete through broad production footprints, technical support in blow molding compatibility, customer relationships in the beverage industry, and innovation in recyclable packaging design. As sustainability becomes more central to buying decisions, competitive advantage is increasingly shifting toward circularity, lightweighting, and application-specific product development.

LIST OF KEY PET PREFORMS COMPANIES PROFILED IN REPORT

- ALPLA Group (Austria)

- RETAL Industries Ltd. (Cyprus)

- Resilux NV (Belgium)

- Plastipak Packaging, Inc. (U.S.)

- Hon Chuan Group (Taiwan)

- SGT (France)

- Esterform Packaging Ltd. (U.K.)

- Petainer (U.K.)

- Amcor plc (Switzerland)

- Logoplaste (Portugal)

KEY INDUSTRY DEVELOPMENTS

- January 2025: ALPLA acquired all shares from its joint venture partner Taba in Egypt, fully integrating the site into its group operations. The facility manufactures plastic bottles, preforms, and closures for North Africa and the Middle East, making the transaction a notable regional consolidation move in the PET packaging value chain.

- October 2024: Plastipak introduced EcoPreform, a new preform and bottle concept made with 75% recycled PET and 25% bio-based PET. The launch underscores growing industry focus on low-impact PET packaging formats and demonstrates continued innovation in sustainable preform development.

REPORT COVERAGE

The global PET preforms market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market during the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The market research report also encompasses detailed competitive landscape with information on the market shares and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.7% from 2026-2034 |

| Unit | Value (USD Billion), Volume (Kiloton) |

| Segmentation | By Type, End-use Industry, and Region |

| By Type |

|

| By End-use Industry |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 51.65 billion in 2025 and is projected to reach USD 78.74 billion by 2034.

Recording a CAGR of 4.7%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

The beverages end-use industry segment is leading in the market.

Asia Pacific held the highest market share in 2025.

Expanding beverage bottling activity and growing demand for PET bottles are accelerating the adoption of PET Preforms.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us