Polymer Nanomembrane Market Size, Share & Industry Analysis, By Material Type (Polyamide, Polysulfone (PSU), Polyethersulfone (PES), PVDF and Others), By Application (Water & Wastewater Treatment, Gas Separation, Bio-medical & Healthcare, Energy & Power and Others), By End-Use Industry (Municipal, Industrial, Healthcare and Others) and Regional Forecast, 2026-2034

Polymer Nanomembrane Market Size and Future Outlook

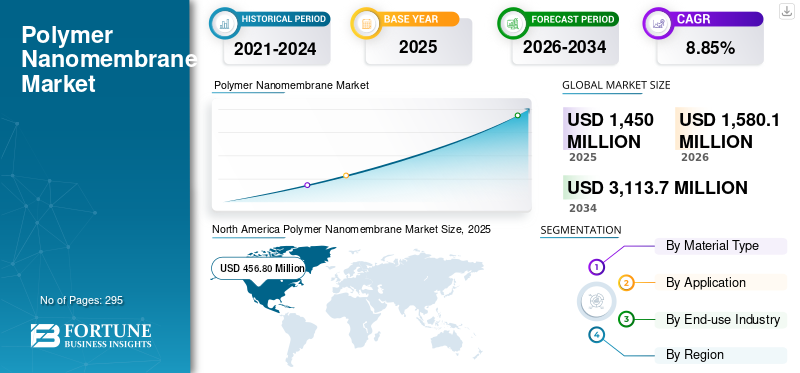

The polymer nanomembrane market size was valued at USD 1,450.0 million in 2025. The market is projected to grow from USD 1,580.1 million in 2026 to USD 3,113.7 million by 2034, exhibiting a CAGR of 8.85% during the forecast period. North America dominated the polymer nanomembrane market with a market share of 31.50% in 2025.

A polymer nanomembrane is an ultra-thin, selectively permeable membrane fabricated from polymeric materials (such as polyamide, polysulfone, polyethersulfone, or PVDF) with structural features engineered at the nanometer scale. The market is fundamentally driven with energy transition and healthcare compliance acting as strong secondary accelerators.

Furthermore, many key industry players, including Toray Industries, Inc., Asahi Kasei Corporation, SUEZ Water Technologies & Solutions, DuPont de Nemours, Inc., and LG Chem operating in the market, are focusing on developing innovative products to meet the rising demand.

Download Free sample to learn more about this report.

Polymer Nanomembrane Market KEY TAKEAWAYS

- 2025 Market Size: USD 1,450.0 million

- 2026 Market Size: USD 1,580.1 million

- 2034 Forecast Market Size: USD 3,113.7 million

- CAGR: 8.85% from 2026–2034

- North America dominated the market with a 31.50% share in 2025.

- Gas separation segment is projected to grow at a CAGR of 8.1%.

- Industrial segment is projected to grow at a CAGR of 9.1%.

North America

Valued at USD 456.8 million in 2025, supported by advanced water infrastructure, industrial filtration demand, and strong R&D capabilities.

Europe

Projected to reach USD 361.3 million by 2026, driven by stringent environmental regulations and growing adoption of advanced membrane technologies.

Asia Pacific

Valued at USD 417.6 million in 2025, driven by rapid industrialization, water treatment investments, and expanding membrane manufacturing.

U.S.

Projected to reach USD 436.3 million by 2026, supported by advanced water treatment infrastructure and increasing energy transition investments.

Japan

Projected to reach USD 68.4 million by 2026, driven by innovation in high-performance membranes and semiconductor filtration applications.

Read More

POLYMER NANOMEMBRANE MARKET TRENDS

Shift Toward High-Performance, Thin-Film Composite (TFC) Membranes is Latest Market Trend

One of the most significant trends in the market is the shift toward high-performance thin-film composite (TFC) membranes, particularly in water treatment and desalination applications. Traditional polymer membranes were often limited by a trade-off between permeability and selectivity, improving one typically reduced the other. Thin-film composite membranes address this limitation by combining multiple functional layers into a single structure. Typically, a TFC membrane consists of very thin polyamide selective layer (often less than 200 nanometers thick) formed on top of a porous support layer made from materials such as polysulfone or polyethersulfone. This layered design allows the ultra-thin active layer to provide high salt rejection and molecular selectivity, while the support layer ensures mechanical strength and structural stability under high pressure. As a result, TFC membranes deliver higher water flux at lower operating pressures, reducing energy consumption and improving overall system efficiency.

- For example, in large-scale seawater desalination plants in Saudi Arabia or the UAE, operators increasingly prefer advanced polyamide TFC reverse osmosis membranes. This helps achieve higher permeate output per unit area while lowering energy costs where energy is one of the largest operational expenditures in desalination.

- A newer generation of TFC membranes may reduce required operating pressure by several bars compared to earlier models, translating into significant electricity savings over the life of the plant.

- Similarly, in Healthcare wastewater treatment facilities across China & India, TFC nanofiltration membranes enable selective removal of multivalent ions and organic contaminants while allowing higher throughput, supporting zero-liquid-discharge (ZLD) compliance. Beyond water treatment, TFC designs are also influencing gas separation applications, where ultra-thin selective layers enhance CO₂ removal efficiency in hydrogen purification systems.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rapid Expansion of Global Water And Wastewater Treatment to Boost Market Growth

A primary market driver for the market is the rapid expansion of global water and wastewater treatment driven by rising water scarcity and stricter environmental regulations. Many regions across the world including the Middle East, India, parts of China, and even water-stressed areas in the U.S. are facing increasing pressure on freshwater resources due to population growth, urbanization, healthcare expansion, and climate change. As a result, governments and municipalities are investing heavily in desalination plants, wastewater recycling facilities and Healthcare effluent treatment systems. Polymer nanomembranes, particularly polyamide-based Reverse Osmosis (RO) and nanofiltration membranes, are essential components in these systems as they provide high selectivity, strong contaminant rejection, and energy-efficient separation performance.

In developed markets including Europe and North America, aging municipal water Others is being upgraded with advanced membrane technologies to meet tighter discharge standards and sustainability targets.

The significance of polymer nanomembranes lies in their ability to deliver high separation efficiency at relatively lower operating energy compared to traditional thermal separation methods. As energy efficiency and environmental compliance become central to planning, demand for high-performance membrane systems continues to rise. Therefore, expanding water treatment and desalination capacity globally remains the most significant structural driver supporting long-term polymer nanomembrane market growth.

MARKET RESTRAINTS

Membrane Fouling and Performance Degradation Over Time To Hamper Market Growth

A key market restraint is membrane fouling and performance degradation over time, which directly affects operational efficiency and lifecycle costs. Fouling occurs when suspended solids, organic matter, microorganisms or scaling salts accumulate on the membrane surface or within its pores, reducing permeability and increasing pressure requirements. This leads to higher energy consumption, frequent cleaning cycles, chemical usage and eventually membrane replacement. In large-scale desalination or healthcare wastewater plants, even a small decline in membrane efficiency can significantly increase Operating Expenditure (OPEX), making buyers highly cautious in procurement decisions.

- For example, in seawater desalination plants in the Middle East, membranes are continuously exposed to high salinity, biofouling agents, and scaling minerals. Over time, biofilm formation on polymer nanomembranes reduces water flux, forcing operators to use aggressive chemical cleaning protocols. These cleaning processes not only increase costs but may also shorten membrane lifespan.

- Similarly, in sectors such as textiles or mining in countries such as India or Chile, wastewater streams often contain complex organic and inorganic contaminants that accelerate fouling. As a result, system downtime and maintenance frequency rise, reducing overall system reliability.

MARKET OPPORTUNITIES

Rapid Expansion of Hydrogen Economy and Carbon Capture Applications May Create Lucrative Growth Opportunities

A major market opportunity in the market lies in the rapid expansion of the hydrogen economy and carbon capture applications, where advanced gas separation membranes are emerging as energy-efficient alternatives to traditional separation technologies. As governments worldwide commit to decarbonization targets and net-zero emissions, investments in green hydrogen production, blue hydrogen with carbon capture, and Healthcare Carbon Capture and Storage (CCUS) projects are accelerating. Polymer nanomembranes, particularly those engineered with ultra-thin selective layers, offer high selectivity for hydrogen and carbon dioxide separation while consuming significantly less energy compared to conventional cryogenic or pressure swing adsorption systems.

For example, in hydrogen production facilities using steam methane reforming or electrolysis, polymer nanomembranes can selectively separate hydrogen from mixed gas streams with lower energy requirements and smaller system footprints. This is particularly valuable in regions such as Europe and North America, where hydrogen development is supported by policy incentives and funding programs. Similarly, in carbon capture projects at power plants or healthcare facilities, membrane-based CO₂ separation systems provide modular and scalable solutions, making them attractive for retrofitting existing plants.

MARKET CHALLENGES

Technical Durability Under Harsh Operating Conditions Pose Critical Challenge To Market Growth

One of the most critical technical challenges in the market is ensuring long-term mechanical, chemical, and biological stability under harsh operating conditions, without sacrificing permeability or selectivity. In real-world applications, membranes rarely operate under ideal laboratory conditions. Instead, they are continuously exposed to high pressures, chemically aggressive cleaning agents, dissolved salts, organic foulants, microorganisms and in some industries, solvents and heavy metals. These stressors collectively accelerate membrane degradation.

In desalination plants, particularly Seawater Reverse Osmosis (SWRO) systems in regions including the Middle East, membranes operate under pressures that can exceed 60–80 bar. Over time, sustained hydraulic pressure can cause compaction of the polymer structure. Compaction reduces pore size and water flux, lowering productivity and increasing energy consumption. Simultaneously, membranes are frequently cleaned using strong oxidizing agents or acidic and alkaline solutions to remove scaling and biofouling. Polyamide-based nanomembranes, while highly selective, are particularly sensitive to chlorine and oxidants. Repeated exposure can break down the polymer chains, leading to reduced salt rejection and structural weakening.

Segmentation Analysis

By Material Type

Polyamide Segment To Lead Due to Its Significant Role in Reverse Osmosis

Based on material type, the market is segmented into polyamide, polysulfone (PSU), polyethersulfone (PES), PVDF and others.

The polyamide accounted for the largest polymer nanomembrane market share in 2025 due to its dominant role in RO and nanofiltration systems used in desalination and wastewater treatment. For example, seawater desalination plants extensively use polyamide-based RO membranes to convert seawater into potable water. As global desalination capacity expands and Zero-Liquid-Discharge (ZLD) policies tighten in Asia, demand for polyamide nanomembranes continues to rise. The balance between performance and scalability reinforces their leading position.

Polysulfone segment is the second largest segment. It is widely used as a support layer material in composite membranes and in ultrafiltration applications. PSU membranes are common in industrial wastewater treatment and as structural backbones in TFC membranes.

By Application

Water & Wastewater Treatment to Lead Market Due To Expansion of Desalination

Based on the application, the market is segmented into water & wastewater treatment, gas separation, bio-medical & healthcare, energy & power and others.

Amongst these, the water & wastewater treatment segment accounted for the dominant market share in 2025 driven by global desalination expansion, rising wastewater recycling needs, and stricter environmental discharge regulations.

Gas separation is the second-largest segment, supported by growth in hydrogen purification, natural gas processing, and carbon capture applications. Polymer nanomembranes selectively separate gases such as hydrogen, nitrogen, and carbon dioxide with lower energy consumption compared to cryogenic methods. The segment is expected to grow with a CAGR of 8.1%.

By End-use Industry

To know how our report can help streamline your business, Speak to Analyst

Municipal Segment To Lead Market Due To High Need for Safe Drinking Water

Based on the end use industry, the market is segmented into municipal, industrial, healthcare, and others.

Municipal segment accounted for the dominant market share in 2025 driven by increasing global demand for safe drinking water, wastewater recycling, and desalination. Rapid urbanization, population growth, and climate change have intensified pressure on freshwater resources, compelling governments to expand and modernize water treatment infrastructure. Polymer nanomembranes—particularly polyamide-based RO and nanofiltration membranes—are extensively used in municipal desalination plants, wastewater reuse facilities, and drinking water purification systems.

The industrial segment represents a significant share of the market, driven by wastewater treatment and process water purification across industries such as chemicals, petrochemicals, mining, textiles, food & beverage, and power generation. Increasingly stringent discharge norms and ZLD regulations are compelling industries to adopt advanced membrane systems. The segment is expected to grow with a CAGR of 9.1%.

Polymer Nanomembrane Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Polymer Nanomembrane Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America held largest share in 2025, valued at around USD 456.8 million. North America market is supported by strong technological capabilities and a mature water treatment infrastructure base. The U.S. dominates regional demand due to extensive municipal wastewater recycling, industrial effluent compliance, and growing hydrogen purification projects. The presence of major membrane manufacturers and strong R&D ecosystems further supports innovation and product adoption. Growth in this region is largely replacement-driven, with increasing demand for energy-efficient and durable membranes in industrial and biomedical applications.

U.S. Polymer Nanomembrane Market

The U.S. market can be analytically approximated at around USD 436.3 million in 2026. The U.S. represents the largest market for polymer nanomembranes in North America, supported by advanced water infrastructure, strong industrial filtration demand, and growing energy transition investments.

To know how our report can help streamline your business, Speak to Analyst

Asia Pacific

Asia Pacific reached at USD 417.6 million in 2025 and secure its position as the fastest growing region in the global market. Rapid urbanization, industrial expansion and increasing water scarcity are accelerating investments in desalination and wastewater treatment. China and India are major growth engines, driven by large-scale municipal infrastructure development and ZLD regulations. Japan and South Korea contribute through advanced material innovation and semiconductor-related filtration demand. The region also benefits from expanding domestic membrane manufacturing capacity, intensifying competition and driving cost optimization.

Japan Polymer Nanomembrane Market

The Japan market in 2026 is estimated at around USD 68.4 million, accounting for roughly 5.1% of global revenues. Japan represents a technologically advanced and innovation-driven market within the Asia Pacific region. Although smaller in volume, Japan plays a crucial role in high-performance membrane development and specialty applications.

China Polymer Nanomembrane Market

China’s market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 292.0 million, representing roughly 13.8% of global sales. China is the largest market in Asia Pacific and one of the fastest-growing countries in the global market. Growth is primarily driven by large-scale water infrastructure expansion, industrial wastewater regulation, and rapid manufacturing.

India Polymer Nanomembrane Market

The India market in 2026 is estimated at around USD 164.2 million, accounting for roughly 4.7% of global revenues. India is one of the fastest-growing markets in Asia Pacific for polymer nanomembranes, driven by rising water scarcity, expanding industrialization, and tightening environmental compliance norms. India shows strong long-term growth potential due to infrastructure expansion and regulatory reforms.

Europe

Europe is projected to grow at 7.8% over the coming years and reach a valuation of USD 361.3 million by 2026. Europe holds a significant share of the market, driven by stringent environmental regulations and sustainability targets. EU directives on wastewater discharge and water reuse encourage the adoption of advanced membrane technologies. Countries such as Germany, France, and the U.K. lead in industrial filtration and municipal water treatment modernization. Additionally, Europe’s focus on hydrogen economy development and carbon capture projects supports demand for gas separation membranes. While the market is relatively mature, steady growth continues through regulatory compliance and infrastructure upgrades.

U.K. Polymer Nanomembrane Market

The U.K. market in 2026 is estimated at around USD 55.2 million, representing roughly 3.5% of global revenues.

Germany Polymer Nanomembrane Market

Germany’s market is projected to reach approximately USD 107.4 million in 2026, equivalent to around 6.8% of global sales.

Latin America and Middle East & Africa

Latin America shows moderate growth, led by Brazil and Mexico. Municipal water treatment expansion and industrial wastewater management particularly in mining-heavy economies such as Chile and Peru support demand. The market remains relatively import-dependent, with global suppliers playing a dominant role. The Latin America market is set to reach a valuation of USD 118.7 million in 2026.

The Middle East & Africa region is driven primarily by desalination demand. Water scarcity and limited freshwater resources in GCC countries such as Saudi Arabia and the UAE result in large-scale investments in seawater desalination plants. Polymer nanomembranes are critical components in these systems. While Africa outside the GCC has smaller market size, mining and municipal water challenges support steady growth. Overall, Middle East & Africa shows strong expansion potential due to infrastructure-driven demand. The Middle East & Africa is set to reach USD 142.4 million in 2025.

GCC Polymer Nanomembrane Market

The GCC market is projected to reach around USD 94.2 million in 2026, representing roughly 5.96% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive Pressure & Technological Differentiation to Propel Market Progress

The global market is moderately consolidated, with a mix of large multinational corporations and specialized membrane technology providers. Competition is primarily driven by technological innovation, product performance, durability, and long-term supply agreements, rather than purely price in developed markets. Competition—particularly from emerging Asian manufacturers is pushing global leaders to differentiate through nanocomposite membrane integration, anti-fouling coatings, extended membrane lifespan, and energy-saving designs. Toray Industries, Inc., Asahi Kasei Corporation, SUEZ Water Technologies & Solutions, DuPont de Nemours, Inc., and LG Chem are the few key players in the market.

Other notable players in the global market include Hydronautics, Pentair, Synder Filtration, Alfa Laval, Pall Corporation, and KOCH Separation Solutions.

LIST OF KEY POLYMER NANOMEMBRANE COMPANIES PROFILED

- Toray Industries, Inc. (Japan)

- Asahi Kasei Corporation (Japan)

- SUEZ Water Technologies & Solutions (France)

- DuPont de Nemours, Inc. (U.S.)

- LG Chem (South Korea)

- Hydranautics (U.S.)

- Pentair (U.S.)

- Synder Filtration, Inc. (U.S.)

- Sumitomo Electric Fine Polymer, Inc. (Japan)

- ALFA LAVAL (Sweden)

- Koch Separation Solutions (U.S.)

- Pall Corporation (U.S.)

KEY INDUSTRY DEVELOPMENTS

- December 2025: Toray Industries, Inc. announced the development of a scalable technology for a new high-durability, high-selectivity nanofiltration membrane element capable of efficiently recovering high yields of high-purity lithium from recycled automotive lithium-ion batteries. This innovation is expected to significantly improve lithium recovery rates compared to conventional recycling methods, which often result in substantial lithium losses. As the adoption of electric vehicles accelerates and global decarbonization efforts intensify, establishing a closed-loop lithium recycling system has become an increasingly important technological priority.

- July 2023: DuPont announced the commercial launch of its new DuPont FilmTec LiNE-XD nanofiltration membrane elements, specifically designed for lithium brine purification. The FilmTec LiNE-XD and LiNE-XD HP are the company’s first membrane products dedicated to this application. These advanced membranes enable high lithium recovery from chloride-rich brine streams while delivering strong selectivity against divalent metals such as magnesium, enhancing purification efficiency.

- August 2022: Toray Industries, Inc. announced the development of an advanced nanofiltration membrane designed to recover lithium from used automotive lithium-ion batteries. With the expected surge in end-of-life electric vehicle batteries many of which are currently discarded, the company aims to address the growing need for efficient lithium recovery solutions. Toray has begun testing the technology using actual spent lithium-ion batteries and plans to further advance research and technical development efforts to move toward commercial deployment of the solution.

- March 2021: The SUEZ Group announced the signing of two new international contracts in Brazil and Russia. Through these agreements, SUEZ will deliver its advanced water technology expertise and tailored solutions to industrial clients operating in key sectors, including energy. The state-of-the-art technologies deployed by SUEZ are designed to support industrial operators in achieving operational efficiency, enhancing environmental performance, and meeting increasingly stringent regulatory requirements.

REPORT COVERAGE

The global market analysis includes a comprehensive study of the market size & forecast across all market segments covered in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including technological advancements, pipeline candidates, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, and key industry developments, as well as their prevalence by key regions. The global market research report also provides a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 8.85% from 2026 to 2034 |

| Unit | Value (USD Million) |

| Segmentation | By Material Type, Application, End-Use Industry, and Region |

| By Material Type |

|

| By Application |

|

| By End-use Industry |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 1,450.0 million in 2025 and is projected to reach USD 3,113.7 million by 2034.

In 2025, the market value in the North America stood at USD 456.80 million.

The market is expected to grow at a CAGR of 8.85% over the forecast period of 2026-2034.

By material type, the polyamide segment is expected to lead the market.

Rapid expansion of global water and wastewater treatment is expected to be the key driver of the market.

Asahi Kasei Corporation, SUEZ Water Technologies & Solutions, DuPont de Nemours, Inc., and LG Chem are the largest players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 295

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us