Target Drone Market Size, Share, and Industry Analysis by Type (Fixed Wing, Rotary Wing, and Hybrid), By Application (Military (Army, Naval (Anti-Ship Target Practice, Surface & Subsurface Threat Training)) and Commercial), By Range (Short Range (Up to 100 km), Medium Range (101km – 400 km), and Long Range (Above 400 km)), By Payload Capacity (Low <25kg), Medium (25kg to 50Kg), and Heavy (>50kg)), By Autonomous Level (Remotely Piloted, Autonomous, and Semi-Autonomous), By Use (Conventional and Advanced Dual-Purpose Use), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

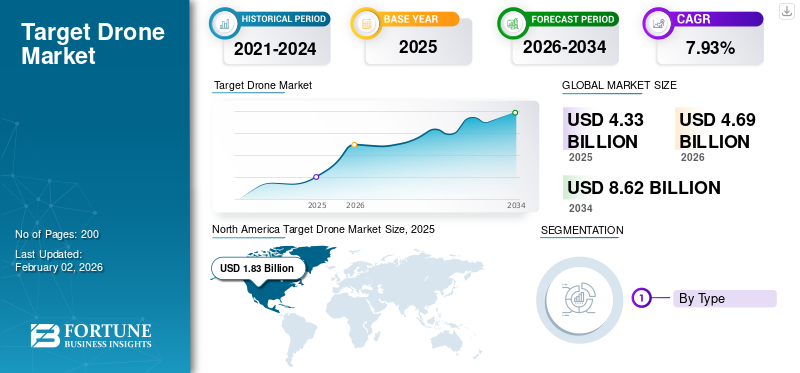

The global target drone market size was valued at USD 4.33 billion in 2025 and is projected to grow from USD 4.69 billion in 2026 to USD 8.62 billion by 2034, exhibiting a CAGR of 7.93% during the forecast period. North America dominated the target drone market with a market share of 42.19% in 2025.

Target drones are unmanned aerial vehicle (UAVs), which are remotely controlled or pre-programmed to simulate as enemy aircraft or missiles for advanced training applications of military personnel and weapons testing such as anti-aircraft systems and combat systems. These drones can also mimic the radar and infrared signatures of aerial threats and some can even be equipped with explosive payloads to function as suicide attack drones. Increased defense sector’s spending and military modernization are driving the demand for realistic and cost-effective training solutions (target drone systems) for air defense systems and personnel training.

Key players in the target drone market, such as Kratos Defense Security Solutions, Northrop Grumman, QinetiQ, Boeing, Lockheed Martin, and Airbus, drive market expansion through their focus on developing advanced, high-fidelity, and cost-effective training solutions that simulate various threats for military and defense sectors. These companies are investing in innovation, securing strategic contracts, forming partnerships, and creating more durable and realistic target drones to meet the escalating demand for realistic combat solution.

Download Free sample to learn more about this report.

Target Drone Market KEY TAKEAWAYS

- 2025 Market Size: USD 4.33 billion

- 2026 Market Size: USD 4.69 billion

- 2034 Forecast Market Size: USD 8.62 billion

- CAGR: 7.93% from 2026–2034

- North America dominated the target drone market with a 42.19% share in 2025.

- The fixed-wing drones segment is expected to hold the largest market share of 82.46% in 2026.

- The military segment is projected to dominate the market with a 93.31% share in 2026.

North America

North America generated USD 1.83 billion in 2025, accounting for 42.19% of the global market, and is projected to reach USD 1.98 billion in 2026.

Asia Pacific

Asia Pacific accounted for USD 1.20 billion in 2025 and is expected to grow to USD 1.31 billion in 2026, supported by increasing defense modernization programs.

Europe

Europe recorded USD 0.98 billion in 2025 and is projected to reach USD 1.06 billion in 2026, driven by rising investments in military training technologies.

U.S.

U.S. The target drone market is projected to reach USD 1.80 billion by 2026, supported by strong defense spending and advanced military training requirements.

Japan

Japan The market is projected to reach USD 0.29 billion by 2026, driven by growing investments in defense preparedness and simulation technologies.

Read More

Market Dynamics

Market Drivers

Increasing Global Defense Budget to Boost Need for Realistic, Cost-Effective Training and Simulation

Target drones offer advanced training environments that closely mimic actual combat situations at a fraction of the cost of manned aircraft, which is driving increased adoption by militaries across the globe. The drones can be used for repeated live-fire training and missile defense exercises as they are much less expensive and safer to deploy than piloted fighter jets, which can cost millions of dollars to operate and maintain.

- In March 2022, the Japan Ground Self-Defense Force (JGSDF), the service responsible for land warfare in Japan, awarded QinetiQ a contract to use Uncrewed aerial targets for anti-aircraft firing training by delivering the Banshee Jet 80, logistics support, spare parts, and other related components for the Banshee target.

Market Restraints

High Procurement Costs and Operational Limitations May Hinder the Market Growth

Target drones are cheaper than manned aircraft. However, advanced variants, such as supersonic or stealth-capable drones, still have high procurement and maintenance costs. This can strain the budgets of smaller defense forces. Additionally, its reusability is limited as many target drones are designed to be used only once. This makes large-scale advanced training exercises expensive over time. Furthermore, export restrictions and strict defense regulations slow down cross-border sales and collaboration.

- For instance, the U.S. places tight export controls on systems such as Kratos’s BQM-177A, limiting their availability to allied nations.

Market Opportunities

Market Presents Significant Opportunities as Armed Forces Modernize their Training Infrastructure to Deal with Evolving Aerial Threats

The global market offers vital opportunities as armed forces upgrade their training setups to address changing aerial threats. These threats include cruise missiles, loitering munitions, and fifth-generation fighter aircraft. One key opportunity is the creation of supersonic and stealth-capable target drones. These drones can more accurately mimic real-world threats for air defense systems.

- In April 2024, the U.S. Navy awarded Northrop Grumman a contract worth USD 52.1 million to manufacture 16 new GQM-163A “Coyote” supersonic sea-skimming target drones. These high-speed drones are designed to simulate advanced supersonic and hypersonic anti-ship cruise missiles offering warship crews more realistic and cost-effective training in detecting and countering such threats.

Target Drone Market Trends

Increasing Demand for Reusable and Modular Platforms

The target drone demand is rising for reusable and modular platforms. Traditionally, most of these drones were disposable; they were destroyed after just one mission. However, increasing procurement costs and the need for more frequent training exercises have driven militaries to seek drones that can be recovered, refurbished, and used again.

Moreover, modern target drones have advanced beyond simple flying targets. They now come with AI-powered flight control, radar cross-section modification, infrared signatures, and electronic jamming systems. These features allow them to closely imitate advanced threats, including stealth aircraft and incoming missiles.

- For instance, in June 2024, the Defence Research and Development Organisation (DRDO) successfully completed six consecutive development trials of High Speed Expendable Aerial Target (HEAT) 'ABHYAS' with enhanced booster configuration from the Integrated Test Range (ITR) based in Chandipur, Odisha.

Download Free sample to learn more about this report.

Impact of Russia-Ukraine Conflict

Surge in Demand for Realistic Training Systems Bolsters Market Expansion

The strong use of drones in the Russia–Ukraine war has changed how militaries around the world see aerial threats. Ukraine is set to produce over 2 million drones in 2024, using them for swarming, kamikaze, and reconnaissance missions. As a result, defense forces in NATO, Asia-Pacific, and elsewhere are quickly looking for training platforms that can mimic these varied, low-cost, yet highly effective aerial threats. This has led to more investment in the target drone market, focusing on flexible, AI-driven, and disposable systems that simulate real combat situations, such as FPV drones that can carry out precise strikes. This demand is forcing traditional drone manufacturers to go beyond supersonic missile simulators. They need to develop training drones that can replicate the swarming and electronic warfare tactics seen in Ukraine.

Acceleration of Technological Innovation in Target Drones Favors Industry Expansion

The conflict has sped up the integration of AI, autonomy, and electronic countermeasure resilience into target drones. Both Russia and Ukraine have used drones that can operate under heavy GPS jamming and electronic warfare. This situation has forced militaries around the world to change their training programs to address these new challenges. There is strong demand for target drones with modular payloads, radar cross-section shaping, and autonomous maneuvering. These features can help train forces face AI-enabled and electronic warfare-resilient threats. For instance, Russia’s creation of a dedicated Unmanned Systems Forces branch and Ukraine’s development of AI-powered kamikaze drones are serving as models for future aerial warfare. This is pushing drone developers to adopt similar advancements in their platforms.

SEGMENTATION ANALYSIS

By Type

Fixed-Wing Drones Dominates the Market due to Suitability for Simulating Modern Fighter Jets, Cruise Missiles, and other FAT

The market is segmented by type into fixed wing, rotary wing, and hybrid.

- For instance, in January 2025, QinetiQ won a contract worth USD 14 million from the U.S. Department of Defense to supply its Vindicator drones to the Naval Air Warfare Center Weapons Division (NAWCWD). The UAV will help the USN to test its air defense systems. The five-year contract came into effect in December 2024 and will run until late 2029.

To know how our report can help streamline your business, Speak to Analyst

By Application

Military Segment Dominates as Armed Forces are the Main Users of these Systems

The market is segmented by application into military and commercial.

The military segment is expected to dominate the market with a share of 93.31% in 2026, as armed forces will continue to be the primary users of these systems. They use target drones for combat training, weapons testing, and simulating threats. Today’s militaries deal with more complicated aerial threats, including cruise missiles, UAV swarms, and stealth aircraft. These challenges need realistic training environments to prepare air defense crews and fighter pilots. Target drones offer a safe and affordable way to simulate these threats without endangering manned aircraft.

- For instance, in June 2025, the U.S. Department of Defense awarded Boeing a USD 10.25 million contract to convert additional retired F-16 Fighting Falcons into QF-16 full-scale aerial target drones. This builds on an extensive program where Boeing has already delivered 75 QF-16s to the U.S. Air Force.

By Range

Medium Range (101km to 400 km) Leads the Market Due to its Operational Flexibility and Mission Realism

The market is segmented by range into short range (up to 100 km), medium range (101km – 400 km), and long range (above 400 km).

The medium-range (101 km to 400 km) segment is expected to hold the largest share of the global target drone market at 44.78% in 2026 and is anticipated to be the fastest-growing segment during the forecast period. These drones offer operational flexibility and mission realism, driving segment growth. Short-range drones have limits in endurance and training uses. In contrast, medium-range drones can handle extended air defense drills, beyond-visual-line-of-sight operations, and realistic missile threat simulations without the high costs associated with long-range systems. Militaries favor this segment for regular live-fire training, radar calibration, and electronic warfare exercises. It enables forces to replicate various aerial threats while keeping operational costs under control.

- For instance, in July 2023, the U.S. Army awarded Kratos Defense & Security Solutions a contract worth USD 95 million to supply drones for its aerial target activity under a firm-fixed-price contract over five years.

By Payload Capacity

Low (<25kg) Segment Dominates the Market Due to Cost-Effective Nature and Ease of Deployment

The market is segmented by payload capacity into low (<25kg), medium (25kg to 50Kg), and heavy (>50kg).

The low (<25kg) segment is expected to dominate the market with a share of 46.45% in 2026. As they are cost-effective, easy to deploy, and widely applicable in basic training missions, these drones are heavily used for gunnery training, short-range surface-to-air missile drills, and radar tracking exercises. They do not require high-endurance or heavy-payload systems. Additionally, their lightweight design lowers manufacturing costs, speeds up deployment, and makes recovery easier. This allows armed forces to conduct high-volume training exercises at lower operational costs.

- For instance, in September 2020, the U.S. Army awarded Griffon Aerospace a contract worth USD 49 million for the supply of MQM-170 “Outlaw” aerial target drone systems. The MQM-170 has a maximum payload capacity of about 18 kg, making it suitable for gunnery and air-defense training missions.

By Autonomous Level

Semi-Autonomous Segment Dominates the Market as the Level Provides Balance between Cost, Operational Flexibility, and Safety

By autonomous level, the market is divided into remotely piloted, autonomous, and semi-autonomous.

The semi-autonomous segment dominates the market as this autonomy level provides a balance between cost, operational flexibility, and safety. Semi-autonomous drones can be remotely controlled with pre-programmed flight paths. This allows them to mimic realistic enemy aircraft or missile maneuvers while still letting operators step in if necessary. This mixed approach makes them perfect for air defense training, missile tracking, and radar calibration. They offer a high level of threat simulation without the risks and costs associated with fully autonomous systems.

By Use

Conventional Segment Dominates the Market Due to Extensive Use in Armed Forces

By use, the market is divided into conventional use and advanced dual-purpose use.

The conventional use segment currently leads the target drone market. Most armed forces depend on drones for basic training, target practice, radar calibration, and missile tracking exercises. These missions need high-volume, cost-effective drones that can be used repeatedly without needing complex multi-role features.

- For instance, the U.S. Navy’s BQM-177A Subsonic Aerial Target and India’s Lakshya PTA are common in conventional training situations. They simulate incoming threats for air defense and missile crews.

The dual-purpose use segment is expected to grow at the fastest rate. This growth is driven by the increasing demand for drones that can perform both training and tactical roles, such as electronic warfare (EW), surveillance, and loitering strike missions. Militaries are investing more in these type of multipurpose platforms to improve cost-efficiency and operational use.

Target Drone Market Regional Outlook

The market has been studied across North America, Europe, Asia Pacific, and Rest of the World (Middle East & Africa and Latin America).

North America

North America Target Drone Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

North America Dominates the Market with Strong Defense Budgets and Presence of Established Players

North America dominates the global target drone market due to strong defense budgets and ongoing investment in training systems to increase defense capabilities. North America maintained a strong presence in the global market, reaching USD 1.83 billion in 2025, accounting for 42.19% share, and is expected to reach USD 1.98 billion in 2026. The U.S. dominates North America, due to its large naval and air force training programs. For instance, the U.S. Navy has significantly increased the use of the BQM-177A target drone. In Europe, NATO members are quickly expanding training programs due to increased tensions after the Russia-Ukraine conflict. For instance, in 2022, the U.K. Ministry of Defence signed a contract to grow QinetiQ’s Banshee Jet 80+ target drone fleet. This aims to improve air defense training. The U.S. market is projected to reach USD 1.8 billion by 2026.

Asia Pacific

The Asia Pacific market accounted for USD 1.2 billion in 2025, representing 27.72% of the global industry, and is expected to reach USD 1.31 billion in 2026. Asia Pacific is becoming the fastest-growing region. India’s DRDO programs, such as Abhyas and Lakshya, and China’s extensive UAV testing lead the way. South Korea recently revealed the Foosung lightweight loitering drone in 2024. This supports the regional target drone market growth in both training and tactical roles. In the Middle East, rising missile defense drills have increased demand. Saudi Arabia and the UAE are investing in new UAV training systems. In Latin America, Brazil has tested low-cost aerial targets to support its Air Force modernization efforts. The Japan market is projected to reach USD 0.29 billion by 2026. The China market is projected to reach USD 0.47 billion by 2026. The India market is projected to reach USD 0.26 billion by 2026.

- For instance, in July 2025, Turkish Aerospace Industries (TAI) introduced a new VTOL tactical UAV at IDEF 2025. This hybrid platform, 3.1 m long with a 5 m wingspan, supports up to 2.5 kg payload, boasts 10 h endurance, a 1300 km range, and modular wing design for rapid assembly bridging gap between rotary and fixed-wing tactical systems.

Europe & Rest of the World

In 2025, Europe generated USD 0.98 billion, contributing 22.61% to global market revenue, and is projected to grow to USD 1.06 billion in 2026. Rest of the World accounted for USD 0.32 billion in 2025, representing 7.48% of the global market share, and is projected to reach USD 0.34 billion in 2026.

Competitive Landscape

Key Industry Players

Market Landscape Dominated by Established Companies Focused on Developing High-Value Systems

Established companies such as Kratos Defense Security Solutions, Northrop Grumman, QinetiQ, Boeing, and AeroVironment lead the global market. Each company specializes in different areas. Kratos is at the forefront with its expendable BQM-177. Northrop Grumman’s GQM-163A supersonic target is vital for U.S. Navy training. QinetiQ has a strong presence in Europe with its Banshee series. Boeing’s QF-16 serves as a full-scale aerial target for advanced air combat training. At the same time, AeroVironment and General Atomics are growing in the field of tactical and loitering drone systems. Innovators such as Shield AI are creating AI-enabled autonomous solutions.

The competition depends on performance range, cost, and autonomy. Governments are awarding contracts, such as Kratos’ USD 95 million deal with the U.S. Army and AeroVironment’s USD 990 million contract for loitering munitions. This indicates a preference for scalable and proven platforms. While major companies focus on complex and high-value systems, newer companies are finding their place in low-cost, attritable, and AI-driven drones. This creates a market with both established leaders and disruptive newcomers.

LIST OF KEY TARGET DRONE COMPANIES PROFILED

- Boeing (U.S.)

- Lockheed Martin Corporation (U.S.)

- Kratos Defense & Security Solutions (U.S.)

- QinetiQ (U.K.)

- Leonardo S.p.A (Italy)

- Griffon Corporation (U.S.)

- DRDO - Defence Research and Development Organization (India)

- Airbus Defence and Space (Netherlands)

- Turkish Aerospace Industry (Turkey)

- AeroTargets International (U.S.)

- Northrop Grumman (U.S.)

- Israel Aerospace Industry (Israel)

KEY INDUSTRY DEVELOPMENTS

- In August 2025, Kratos confirmed collaboration with Taiwan’s National Chung-Shan Institute of Science and Technology (NCSIST) on a version of its jet-powered MQM-178 Firejet target drone, known as the Chien Feng IV.

- In April 2025, at FEINDEF 2025 in Madrid, Spanish company AERTEC introduced the TARSIS-W tactical UAV. This is an armed version of its UAV line. It comes with FOX-F02 laser-guided micro-missiles, combining reconnaissance and precision strike into one agile platform.

- In April 2023, the U.S. Department of Defense awarded Rapid Expeditionary Concepts, in partnership with Alpha Unmanned Systems, a contract (value not publicly disclosed) to deliver Alpha A900 unmanned helicopters, including the A900T target-drone variant. The A900T has a maximum take-off weight of 25 kg and a payload capacity of up to 4 kg, designed specifically for training and radar tracking roles.

- In August 2022, Kratos Defense & Security Solutions, Inc., a major National Security Solutions provider, announced that it received a contract worth about USD 20 million for high-performance, jet-powered, unmanned aerial target drone systems.

- In January 2022, the Indian Army signed a contract worth USD 12.88 million with Anadrone Systems for MEAT (maneuverable expendable aerial target). This contract to buy the aerial target systems is the first one the army has signed under the Make-II category.

REPORT COVERAGE

The research report delivers a detailed global market analysis and emphasizes key aspects such as key players, offerings, objects, and end-users of target drones. Moreover, the report deals with insights into market trends, competitive landscape, market competition, product pricing, regional analysis, market players, and market status, and highlights key industry growth drivers. In addition to the factors stated above, the report encompasses several direct and indirect influences that have influenced the market size in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.93% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Type

|

By Application

|

|

By Range

|

|

By Payload Capacity

|

|

By Autonomous Level

|

|

By Use

|

|

By Region

|

Frequently Asked Questions

According to a study by Fortune Business Insights, the global market was valued at USD 4.33 billion in 2025 and is anticipated to reach USD 8.62 billion by 2034.

The market is likely to grow at a CAGR of 7.93% over the forecast period (2026-2034).

The top twelve players in the industry are Boeing, Lockheed Martin Corporation, Kratos Defense & Security Solutions, QinetiQ, Leonardo S.p.A, Griffon Corporation, DRDO (India), Airbus Defence and Space, Turkish Aerospace Industry, AeroTargets International, Northrop Grumman, and Israel Aerospace Industry based on parameters such as service portfolio, regional presence, and industry experience.

North America dominated the global market in 2025 with a value of USD 1.83 billion.

With increasing global defense budget, the growing need for realistic, cost-effective training and simulation is a key factor fueling the growth of the market.

The modernization of training infrastructure by armed forces to deal with evolving aerial threats presents significant opportunities for market players.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us