Veterinary Oncology Market Size, Share & Industry Analysis, By Offering (Diagnostics {By Product [Instruments and Reagents & Consumables], By Technique [Cytology, Hematology, Clinical Biochemistry, and Others]} and Therapeutics {By Drug Class [Cytotoxic Chemotherapy Drugs, Targeted Anticancer Drugs, and Others], By Therapy Type [Targeted Therapy, Chemotherapy, Immunotherapy, and Others]}), By Cancer Type (Lymphoma, Mast Cell Tumor, Melanoma, Osteosarcoma, Mammary Tumors, and Others), By Animal Type (Canine, Feline, Equine, and Others), and Regional Forecast, 2026-2034

Veterinary Oncology Market Size and Future Outlook

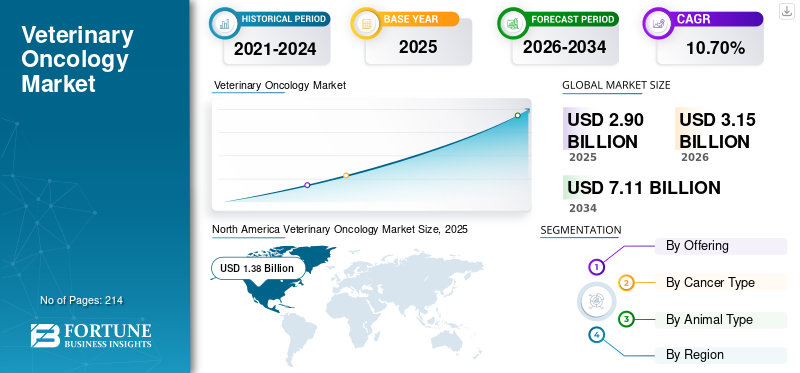

The global veterinary oncology market size was valued at USD 2.90 billion in 2025. The market is projected to grow from USD 3.15 billion in 2026 to USD 7.11 billion by 2034, exhibiting a CAGR of 10.70% during the forecast period. North America dominated the veterinary oncology market with a market share of 47.58% in 2025.

The global market includes diagnostic tools, diagnostic services, and therapeutic medications used for identifying, verifying, staging, treating, and supervising cancer in animals, primarily companion animals such as dogs and cats. The market is driven by the increasing rates of cancer diagnoses in older pets, a rise in pet ownership and spending on pet healthcare, broader acceptance of cytology, histopathology, imaging, molecular diagnostics, and cancer screening tests. Additional factors supporting industry expansion comprise the heightened use of chemotherapy, targeted anticancer medications, cancer vaccines, corticosteroids, and supportive oncology therapies in veterinary cancer treatment.

Key players in the global market include IDEXX Laboratories, Inc., Zoetis Services LLC., Elanco, Dechra Limited, and Boehringer Ingelheim International GmbH, among others. Strong reference laboratory networks, veterinary oncology drug portfolios, cancer screening and liquid biopsy offerings, AI-based imaging platforms, treatment-selection technologies, and continued focus on companion animal oncology diagnostics and therapeutics are some of the factors supporting the dominance of these companies in the global market.

Download Free sample to learn more about this report.

Veterinary Oncology Market Key Takeaways

- 2025 Market Size: USD 2.90 billion

- 2026 Market Size: USD 3.15 billion

- 2034 Forecast Market Size: USD 7.11 billion

- CAGR: 10.70% from 2026–2034

- North America dominated the market with a 47.58% share in 2025.

- Lymphoma segment is projected to hold a 23.8% share in 2026.

- Canine segment is projected to hold a 72.2% share in 2026.

North America

The market reached USD 1.38 billion in 2025 and is projected to reach USD 1.32 billion by 2026.

Asia Pacific

The market is projected to reach USD 0.60 billion by 2026, driven by rising pet healthcare spending.

Europe

The market is expected to grow at a 9.71% CAGR during the forecast period.

U.S.

The market is projected to reach USD 1.32 billion by 2026.

Japan

The market is projected to reach USD 0.13 billion by 2026.

Read More

VETERINARY ONCOLOGY MARKET TRENDS

Advancements in Veterinary Cancer Diagnostics and Treatments is a Remarkable Market Trend

Advancements in veterinary cancer diagnostics and therapies are becoming a significant trend as the sector shifts from simple tumor confirmation to earlier detection, tumor-specific categorization, and more individualized treatment strategies. The increased application of cytology, histopathology, immunophenotyping, molecular diagnostics, liquid biopsy, AI-assisted imaging, and drug-response prediction enhances veterinarians' capacity to identify cancer sooner and choose more appropriate treatments. Simultaneously, targeted anticancer medications, therapies specific to lymphoma, cancer vaccines, and supportive oncology drugs are expanding treatment choices for companion animals. This trend is enhancing market growth as an increasing number of diagnosed cases are transitioning into organized treatment and monitoring processes. It is also raising average revenue per case, since advanced diagnostics frequently result in further staging, monitoring, and therapy choices. Eventually, these advancements are anticipated to transition the market from reactive cancer treatment to preventative screenings, tailored oncology, and prolonged disease management. These factors are supporting the global veterinary oncology market growth during the forecast period.

- For instance, in 2025, IDEXX Laboratories highlighted its Cancer Dx testing as a canine cancer diagnostic available to detect lymphoma earlier, with mast cell tumor detection planned next. The company states that the test can detect canine lymphoma up to 6–8 months before clinical signs and provides clear cancer-type-specific results, supporting earlier diagnosis and treatment decision-making in veterinary cancer care.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Increasing Awareness of Animal Health to Propel Market Growth

The growing awareness of animal health is a crucial factor driving the market, as pet owners are increasingly taking proactive steps toward preventive care, early detection, and ongoing disease management. With pets being more frequently regarded as family, owners are more inclined to look into symptoms such as lumps, weight loss, appetite changes, swelling, or unusual behavior instead of postponing trips to the veterinarian. This directly bolsters the need for oncology diagnostics such as cytology, biopsy, histopathology, imaging, blood tests, and cancer screening examinations. Increased awareness enhances treatment acceptance, as more pet owners are receptive to chemotherapy, targeted therapy, cancer vaccines, corticosteroids, and palliative oncology care upon cancer diagnosis. This trend is particularly significant in companion animals as the growing elderly pet populations and deeper human-animal connections are raising the demand for cancer care. Owing to these factors, operating players are focusing on new product launches, thereby driving the market growth.

- For instance, in January 2026, Dechra Pharmaceuticals received full approval of the U.S. FDA for LAVERDIA-CA1/verdinexor tablets for the treatment of lymphoma in dogs. This makes these tablets the first fully approved oral treatment option for canine lymphoma.

MARKET RESTRAINTS

Limited Accessibility and Affordability of Advanced Therapies to Hamper Market Growth

The limited accessibility and high cost of advanced therapies significantly hinder the market since numerous cancer treatments necessitate expert consultations, ongoing diagnostics, chemotherapy appointments, targeted medications, radiation treatments, and prolonged monitoring. Pet owners typically cover these expenses themselves, particularly in countries with low pet insurance coverage or restricted reimbursement options. Consequently, numerous owners might opt for just basic diagnostics, corticosteroids, palliative medications, or no treatment rather than advanced oncology options. The limitation is more pronounced in emerging markets, where veterinary oncology experts, advanced imaging technologies, cancer vaccines, and targeted therapies are primarily found in major urban areas. In developed markets, substantial treatment costs can postpone diagnosis or decrease the transition to treatment following cancer confirmation. This restricts the utilization of advanced treatments and diminishes the overall market potential, even as the awareness of cancer grows among pet owners.

- For example, according to a Bank of America analysis, the U.S. veterinary visits fell by 2–3% in 2025, while veterinary industry revenue growth was supported by 5–6% year-over-year price increases. This indicates that rising care costs are already reducing visit volumes, which can directly affect uptake of expensive veterinary cancer diagnostics and advanced treatments.

MARKET OPPORTUNITIES

Improvements in Veterinary Diagnostic Tools to Offer Market Growth Opportunities

Improvements in veterinary diagnostic tools are creating a strong market opportunity for market players as they help veterinarians detect cancer earlier and with better accuracy. Traditional cancer diagnosis often depended on visible symptoms, cytology, biopsy, and imaging, but newer tools such as blood-based cancer screening, liquid biopsy, digital cytology, AI-supported imaging, immunophenotyping, and molecular diagnostics are making cancer workups faster and more accessible. These tools can increase the number of pets entering the oncology care pathway, especially older dogs and high-risk breeds. Earlier diagnosis also supports better staging, treatment planning, and monitoring, which can increase the use of chemotherapy, targeted therapy, immunotherapy, and supportive care. For clinics, advanced diagnostic platforms create recurring revenue from tests, reagents, consumables, and reference-lab services. All these factors would drive the market growth in the coming years.

- For instance, in February 2025, IDEXX announced the upcoming U.S. and Canada availability of its Cancer Dx screening test for canine lymphoma, highlighting it as part of a new wave of companion animal diagnostic innovation.

MARKET CHALLENGES

Limited Insurance Coverage for Pet Treatments to Emerge as a Prominent Challenge to Market Growth

The limited insurance coverage for pet medical treatments presents a significant challenge for market expansion. Cancer care frequently requires ongoing diagnostics, biopsies, imaging, chemotherapy, targeted therapies, immunotherapy, and extended monitoring. In several countries, pet insurance uptake is still minimal and even those with coverage might encounter exclusions, yearly limits, deductibles, waiting periods, or restricted options for advanced cancer therapies. Since pet owners typically cover most veterinary oncology costs, significant out-of-pocket expenses may lower treatment uptake following a diagnosis. This issue is particularly crucial for advanced treatments such as targeted cancer medications, cancer vaccines, radiation-assisted therapy, and specialized oncology procedures. It also restricts market expansion in developing areas where insurance coverage remains minimal and specialized care is focused in major urban centers. Consequently, numerous owners might opt for merely basic diagnostics, corticosteroids, supportive medications, or palliative care rather than full oncology treatment. All these factors cumulatively affect the market growth.

- For instance, according to the Association of British Insurers data published in December 2025, despite a record 4.6 million pet owners in the U.K. having pet insurance in 2024, this number accounted for only approximately 17% of all pet owners. This indicates that the majority still did not have protection against unforeseen veterinary expenses.

Segmentation Analysis

By Offering

Diagnostics Segment Dominated the Market Due to the Growing Need for Early Cancer Confirmation and Treatment Planning

In terms of offering, the market is divided into diagnostics and therapeutics.

The diagnostics segment captured the largest global veterinary oncology market share in 2025. The segment’s dominance is due to the growing need for cancer detection, confirmation, staging, and monitoring before any drug therapy is selected. The segment also benefits from higher test frequency, as one cancer case may require multiple diagnostic steps such as biopsy, bloodwork, imaging, tumor grading, and follow-up monitoring. Therefore, recurring diagnostic test volumes, reference laboratory use, and the adoption of advanced cancer screening tools support the diagnostics segment’s dominance.

- For instance, in January 2026, the American Animal Hospital Association (AAHA) released its Oncology Guidelines for Dogs and Cats, emphasizing that cytology or histopathology is needed to define tumor diagnosis, and that staging may include CBC, chemistry, urinalysis, and other diagnostic tests. This supports the central role of diagnostics in veterinary cancer care.

The therapeutics segment is anticipated to rise at a CAGR of 12.67% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Cancer Type

High Diagnosis Frequency and Strong Treatment Pathway Pushed the Dominance of the Lymphoma Segment

On the basis of cancer type, the market is divided into lymphoma, mast cell tumor, melanoma, osteosarcoma, mammary tumors, soft tissue sarcoma, hemangiosarcoma, squamous cell carcinoma, and others.

The lymphoma segment accounted for the largest market share in 2025. It is one of the most frequently diagnosed cancers in companion animals, especially dogs, thereby leading the global market. Moreover, factors such as relatively higher treatment conversion, high case volume, repeat diagnostics, recurring monitoring, and availability of lymphoma-specific drugs further support the dominance of the segment throughout the forecast period. Furthermore, the segment is set to hold a share of 23.8% in 2026.

- For instance, ImpriMed reported that its AI-driven Drug Response Predictions service had been ordered by 300+ veterinary oncologists, supported by 250+ collaborating hospitals, and had delivered 15,000+ canine lymphoma tests. The service is designed for canine lymphoma and leukemia and uses live cancer cells, flow cytometry, PARR, and AI-based response prediction to guide anticancer drug selection, supporting lymphoma’s strong diagnostic and treatment value within veterinary oncology.

The mast cell tumor segment is poised to grow at a CAGR of 12.35% over the forecast period.

By Animal Type

Higher Cancer Diagnosis Rates and Stronger Product Availability Supported the Canine Segment’s Growth

In terms of animal type, the market is segmented into canine, feline, equine, and others.

The canine segment dominated the market in 2025. The segmental dominance is supported by the availability of dog-specific oncology products and tests, including lymphoma diagnostics, mast cell tumor therapies, melanoma vaccines, and canine cancer screening tools. Additionally, higher clinical need, stronger owner willingness to treat, and broader commercial product availability kept the canine segment in leading position in the global market. Furthermore, the segment is set to hold a share of 72.2% in 2026.

- For instance, in August 2025, Yale University reported that a Yale-developed canine cancer vaccine was being tested in clinical trials across 11 U.S. sites for dogs with cancers such as osteosarcoma.

The feline segment is anticipated to rise at a CAGR of 12.14% over the forecast period.

Veterinary Oncology Market Regional Outlook

By geography, the market is separated into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Veterinary Oncology Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market reached USD 1.27 billion in 2024 and led the global market. In 2025, the region continued to hold its leading position with a value of USD 1.38 billion. The North America market growth is supported by high pet ownership, strong pet humanization, and higher willingness to spend on advanced veterinary care. Moreover, the region also has a well-developed network of specialty veterinary hospitals, veterinary oncologists, reference laboratories, diagnostic imaging centers, and oncology-focused service providers, which further support the market growth.

U.S. Veterinary Oncology Market

The U.S. dominated the North America market and can be analytically approximated at around USD 1.32 billion in 2026, accounting for roughly 42.0% of the global market.

Europe

The Europe market size is anticipated to grow at a CAGR of 9.71% during the forecast period. The regional market growth is supported by strong companion animal ownership, mature veterinary infrastructure, and growing access to specialty veterinary cancer care services and advanced diagnostic laboratories.

U.K. Veterinary Oncology Market

The U.K. market is estimated to touch around USD 0.12 billion in 2026, representing roughly 3.9% of global revenues.

Germany Veterinary Oncology Market

The Germany market size is projected to reach approximately USD 0.13 billion in 2026, equivalent to around 4.2% of global sales.

Asia Pacific

The Asia Pacific market is expected to reach a valuation of USD 0.60 billion by 2026. Asia Pacific is expected to be the fastest-growing region due to rising pet ownership, rapid urbanization, increasing disposable income, and growing pet healthcare spending in countries such as China, India, Japan, South Korea, and Australia.

Japan Veterinary Oncology Market

The Japan market is estimated to touch a value of around USD 0.13 billion in 2026, accounting for roughly 4.3% of global revenues.

China Veterinary Oncology Market

The China market is projected to reach revenues of around USD 0.16 billion in 2026, representing roughly 4.9% of global sales.

India Veterinary Oncology Market

The India market is estimated to reach around USD 0.06 billion in 2026, accounting for roughly 1.8% of global revenues.

Latin America and Middle East & Africa

The Middle East & Africa and Latin America regions are likely to witness slower growth over the forecast period. Prominent factors such as expanding companion animal care, rising pet ownership, increasing demand for private veterinary services, and development of premium veterinary clinics in selected urban markets are boosting the market growth in these regions. The market in Latin America is projected to hit a valuation of USD 0.17 billion by 2026.

In the Middle East and Africa region, the GCC market is projected to reach approximately USD 0.06 billion by 2026, representing about 2.0% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Strong Diagnostics and Oncology Drug Portfolios to Support Key Players’ Market Position

The global veterinary oncology market features a moderately fragmented structure with the presence of both diagnostic companies as well as animal health pharmaceutical players. Major companies such as IDEXX Laboratories, Inc., Zoetis Services LLC., Elanco, Dechra Limited, and Boehringer Ingelheim International GmbH hold considerable market presence. This can be attributed to their wide portfolio of cancer screening tests, reference laboratory networks, and strong drug product offerings. Additionally, broad companion animal diagnostic reach and established veterinary distribution channels also support the leading position of these companies.

- For instance, in July 2021, the U.S. FDA granted full approval to Tanovea for the treatment of lymphoma in dogs. This makes it the first conditionally approved new animal drug for dogs to achieve full FDA approval and strengthening Elanco’s position in veterinary cancer therapeutics.

Additional key contributors include Oncotect, Virbac, Novavive Inc., and others. These companies are also emphasizing advanced cancer screening, molecular diagnostics, reference-lab services, targeted anticancer drugs, and precision treatment tools to expand their role across the market.

LIST OF KEY VETERINARY ONCOLOGY COMPANIES PROFILED

- IDEXX Laboratories, Inc. (U.S.)

- Zoetis Services LLC (U.S.)

- Antech Diagnostics, Inc. (U.S.)

- Volition (U.S.)

- Elanco (U.S.)

- Dechra Limited (U.K.)

- Boehringer Ingelheim International GmbH (Germany)

- Oncotect (U.S.)

- Virbac (France)

- Novavive Inc. (Canada)

KEY INDUSTRY DEVELOPMENTS

- February 2026:S.-based pharmaceutical company Avammune advanced its Enzistat cancer drug through a University of Queensland veterinary clinical trial for dogs with terminal, inoperable tumors. The study tested whether the drug can shrink tumors or improve comfort in palliative cases.

- August 2025: TheraJan, the company linked to Yale’s canine cancer vaccine program, continued clinical trials across 11 U.S. sites for dogs with cancers such as osteosarcoma, with early results showing improved 12-month survival when used alongside standard care.

- March 2025: A team of researchers from Cornell University evaluated quantitative ultrasound and immune cytokine profiling for tumor monitoring and lymph node metastasis detection in dogs undergoing radiation therapy, supporting non-invasive monitoring advancements in veterinary oncology.

- January 2024: A deep learning model was developed by a team of researchers from Cornell University to predict c-Kit exon 11 mutation status in canine cutaneous mast cell tumors using H&E-stained histology slides, supporting AI-assisted pathology and treatment-selection tools.

- April 2023: Oncotect, a Raleigh-based animal health startup, developed a urine-based cancer screening test for dogs and planned expansion through at-home test kits, supporting non-invasive canine cancer screening.

REPORT COVERAGE

The global veterinary oncology market analysis encompasses an extensive examination of the market size and projections for all market segments featured in the report. It provides information on the market dynamics and trends that are anticipated to propel the market during the forecast period. It offers insights into crucial elements, such as innovations in products, the regulatory landscape, pipeline analysis, and the introduction of new products. Furthermore, it outlines collaborations, mergers & acquisitions, along with significant advancements in the industry within the market. The global market forecast report additionally offers a comprehensive competitive landscape with details on market share and profiles of major active participants.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 10.70% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Offering, Cancer Type, Animal Type, and Region |

| By Offering |

|

| By Cancer Type |

|

| By Animal Type |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 2.90 billion in 2025 and is projected to reach USD 7.11 billion by 2034.

In 2025, the North America market value stood at USD 1.38 billion.

The market is expected to exhibit a CAGR of 10.70% during the forecast period of 2026-2034.

By offering, the diagnostics segment led the market in 2025.

The rising prevalence of cancer in animals coupled with increasing awareness regarding animal health are primarily driving market expansion.

IDEXX Laboratories, Inc., Zoetis Services LLC., Antech Diagnostics, Inc., and Elanco are some of the prominent players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 214

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us