Military Cables Market Size, Share & Industry Analysis, By Cable Type (Power cables, Data cables (copper), RF/Coax, Fiber optic and Hybrid cable assemblies/harnesses), By Platform (Airborne, Land systems, Naval and C4ISR & Defense Infrastructure), By Procurement (Line-fit (OEM/prime), Tier subsystem integrators, MRO / upgrade programs and Defense logistics), By Application (Power distribution, Mission systems & sensors, EW / SIGINT, Weapon systems and Comms networks), By End User (Army Forces, Navy Forces, Air & Space Forces and Others), and Regional Forecast, 2026-2034

(Offer valid till 15th Jul 2026)

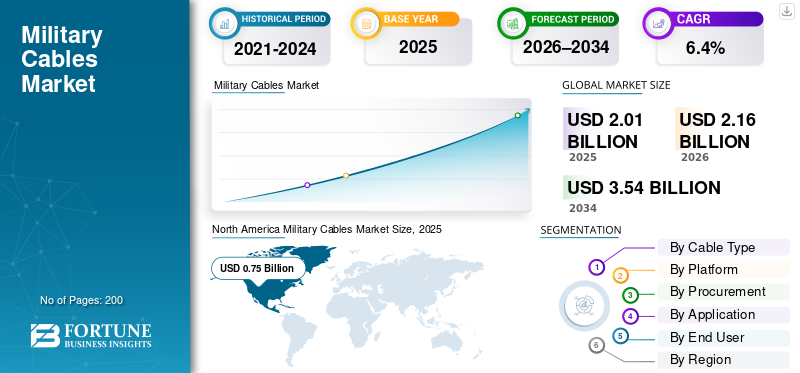

Military Cables Market Size and Future Outlook

The military cables market size was valued at USD 2.01 billion in 2025. The market is projected to grow from USD 2.16 billion in 2026 to USD 3.54 billion by 2034, exhibiting a CAGR of 6.4% during the forecast period. North America dominated the military cables market with a market share of 37.31 in 2025

The market includes ruggedized power, data (copper), RF/coax, fiber-optic, and hybrid harnesses used in defense platforms and networks such as aircraft, land vehicles, ships, radars, electronic warfare suites, and command infrastructure. The product demand is increasing mainly due to modern forces that are fitting more electronics onto each platform, which includes sensors, electronic warfare systems, computing and secure communications. They are also upgrading C4ISR and base networks, which require higher bandwidth, better shielding, and stronger survivability. Reports from SIPRI show that defense spending is rising in several regions, which supports the overall trend in procurement and upgrades that boosts cable demand.

Key players in the market include TE Connectivity Ltd., Amphenol Corporation, Carlisle Interconnect Technologies, Collins Aerospace (RTX Corporation), Nexans S.A., Prysmian Group, HUBER & SUHNER AG, Radiall S.A., Rosenberger Hochfrequenztechnik GmbH & Co. KG and LAPP Group among others. They are advancing the market by promoting lighter and more compact harnesses, improved EMI/EMC protection and faster copper and fiber solutions that simplify integration for prime contractors and speed up retrofit and maintenance work.

Download Free sample to learn more about this report.

MILITARY CABLES MARKET TRENDS

Fiber-First, High-Bandwidth Digital Backbone Upgrades are Emerging Market Trends

In defense systems, forces are sending more sensor data, electronic warfare feeds, and mission computing across platforms and networks. As a result, the cable mix is shifting toward high bandwidth architectures. This highlights more fiber optic runs for backbone links, rugged cable assembly with pre-engineered harnessing to speed up integration. This also depicts smarter combinations of coaxial cables for radio frequency, twisted pair for data and hybrid builds to meet size, weight, and power requirements as well as electromagnetic interference and compatibility constraints. This trend is particularly strong in the U.S. and is growing in Asia Pacific and the Middle East.

In June 2025, the U.S. Defense Logistics Agency (DLA) Land & Maritime issued MIL-STD-1678-4C with Change 4. This reinforces standardized requirements and measurements for fiber-optic cabling test sample configuration and fabrication. It illustrates how the Department of Defense is formalizing fiber-centric cabling practices for military use.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Increased Defense Budgets are Driving Procurement and Upgrade Cycles Leading to Market Growth

As defense budgets increase, defense forces and nations buy new platforms and also upgrades fund to defense systems. This includes refreshing C4ISR, adding electronic warfare capabilities, integrating air defense and modernizing ships or aircraft, fueling demand for military cables. The need for more durable cable assemblies, higher bandwidth links for sensors and communications, and military wiring across various platforms and infrastructure is growing. This eventually drives the military cables market growth.

In April 2025, SIPRI reported that world military spending reached USD 2,718 billion in 2024. This marked a 9.4% increase from the previous year, the largest rise since at least the end of the Cold War. Spending has risen in all regions, indicating a budget trend that usually boosts the demand for high performance cables.

MARKET RESTRAINTS

Sensitive Defense-Grade Supply Chains Limit Delivery of High-Performance Military Cable Assemblies

Even while programs get funding, the supply chains for certified cable assemblies can become a bottleneck. Specialty materials, screened components and qualified manufacturing steps do not scale quickly. This leads to longer lead times for rugged coaxial cables, twisted pair data runs and high-bandwidth fiber builds used in frontline defense systems. As a result, prime contractors and maintenance, repair, and overhaul (MRO) shops may have to wait for specific parts or processing capacity, delaying upgrades and new equipment integration.

In July 2024, NATO published its Defence-Critical Supply Chain Security Roadmap fact sheet, which NATO Defence Ministers endorsed in June 2024. The fact sheet highlighted that recent disruptions and growing complexity have exposed the fragile and vulnerable nature of critical defense supply chains. It also laid out a plan to reduce vulnerabilities and dependencies.

MARKET OPPORTUNITIES

JADC2 and Battle-Network Buildouts Creates Long Runway for High-Bandwidth Cable Solutions and Rugged Cable Assembly

As militaries connect sensors, shooters and command nodes in nearly real time, they must modernize their systems. This involves secure transport, sturdy infrastructure and dependable connectivity from base to tactical edge. This offers a clear opportunity for suppliers of high-bandwidth cable solutions, including fiber backbones, RF runs and rugged data links. Suppliers can also provide faster-to-install cable assembly and harnessing that cuts down integration time on platforms and in C4ISR sites.

In October 2024, the U.S. Air Force provided Leidos a USD 303 million contract to lead planning and analysis for the Advanced Battle Management System (ABMS) digital infrastructure network. This network plays a crucial role in the Pentagon's initiative to connect everything. It exemplifies the kind of network growth that drives the demand for high performance cables.

MARKET CHALLENGES

Cybersecurity Compliance is Becoming a Major Market Challenge

Cybersecurity compliance raises costs and creates friction in defense supply chains. Even in basic areas including cable assembly, prime contractors and tier suppliers must show their cyber hygiene. This is necessary as design files, test data, configuration baselines, and supplier records move digitally through the supply chains that support modern defense systems. Unfortunately, stricter cyber requirements tend to impact smaller cable and interconnect vendors. They face more audits, documentation, and process overhead. This situation slows down onboarding and extends lead times for high-performance cables, including coaxial cables and twisted pair data lines, especially when programs need quick fielding and upgrades.

In November 2025, the U.S. DoD’s CMMC rollout began Phase 1, starting on Nov 10, 2025. The DoD announced that the new DFARS 252.204-7021 clause will add CMMC requirements directly to contracts. Contracting officers will include CMMC Level 1 and 2 requirements in new awards. This decision officially makes cybersecurity compliance a requirement for the defense industrial base.

Impact of Russia Ukraine War

Russia Ukraine War Have Sped Up European Rearmament and Modernization Of C4ISR and EW Systems

The Russia-Ukraine war has created a demand shock for military cabling. It has accelerated two main factors for cable use including rapid upgrades of platforms and faster growth of C4ISR, air defense and electronic warfare networks. Europe’s shift in security has led to a notable increase in spending and a push for modernization. SIPRI highlighted the sharp rise in global spending for 2024, with a particular emphasis on Europe’s increase. This depicts more funded integration work needs power, data, RF/coax, and fiber cabling. The war has also changed the types of cables required. The battlefield has demonstrated the need for electromagnetic contestation and resilience. There is a higher demand for electronic warfare, more distributed nodes and strong communications. This trend drives militaries to adopt systems that offer higher bandwidth and better resistance to jamming.

On the supply side, the war has exposed limitations that impact cable programs directly. Factors such as defense-critical supply chains, materials availability, qualification capacity and delivery lead times are now vital. NATO's Defence-Critical Supply Chain Security Roadmap, approved in June 2024, recognizes that supply chain resilience has become a deterrence issue instead of just a procurement problem. EU efforts to increase production, such as ASAP for ammunition capacity and EDIRPA for joint procurement, also suggest a longer period of rearmament and maintenance activities.

Segmentation Analysis

By Cable Type

Power Cables Dominate Market Due to Growing Need for Onboard Electrification and Power-Hungry Defense Systems

In terms of cable type, the market is categorized into power cables, data cables (copper), RF/coax, fiber optic, and hybrid cable assemblies / harnesses.

Power cables held the largest military cables market share in 2025. For airborne, land, naval, and fixed C4ISR sites, the main focus is providing stable electrical power to all equipment. This includes radars, electronic warfare systems, mission computers, communications racks, actuators and power conversion units. As platforms add more electronics and peak loads rise, the wiring that works best is power distribution cabling. This is important as every new box, sensor, or subsystem needs reliable power feeds, protection and solid routing. Moreover, power cables connect to almost every system on every platform consistently.

In September 2022, the U.S. Defense Logistics Agency (DLA) Land & Maritime issued and maintained MIL-DTL-3432 Revision J with Amendment 2. This specification covers electrical power and special purpose cables for 300V and 600V applications. It emphasizes the importance of standardized, defense-qualified power cabling in military procurement.

Hybrid cable assemblies / harnesses segment in market expected to show fastest grow at a CAGR of 10.4% over the forecast period.

By Platform

Land Systems lead Due to Large Vehicle Fleets and Quick Upgrades in Digital Technology

On the basis of platform, the market is classified into airborne, land systems, naval, and C4ISR & defense infrastructure.

Land systems dominated the market in 2025, and anticipated to be dominating throughout the forecast period. This dominance is attributed to land forces using most platforms in militaries. This includes tanks, IFVs, artillery, air-defense vehicles, command trucks and support fleets. Even minor changes in wiring can create a big demand. Furthermore, land platforms now include more electronics such as radios, BMS, sensors, EW add-ons, and power management. This increase the need for strong power and data cabling, along with more cable assembly and harnessing during upgrades and retrofits.

C4ISR & defense infrastructure is expected to show fastest market growth at a CAGR of 7.7% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Procurement

Large Number of Existing Units and Ongoing Digitization Updates Leads to MRO/ upgrade Programs Segment Dominance

Based on procurement, the market is segmented into, line-fit (OEM/prime), tier subsystem integrators, MRO / upgrade programs, and defense logistics.

MRO / upgrade programs segments held the largest market share in 2025. Most militaries gain combat power per dollar by updating their current equipment. They install new radios, battle management systems, sensors, electronic warfare kits and subsystems for vehicles, ships and aircraft. This emphasis on upgrades creates a steady need for replacing cables, rerouting, new harnessing and integration work during depot visits and mid-life refresh cycles. MRO and upgrade spending keeps cables moving even when deliveries of new platforms are inconsistent.

Tier subsystem integrators is predicted to be the fastest growing segment in market at a CAGR of 7.4% during the forecast period.

By Application

Power Distribution Dominates Market Due To Nonstop Electrification Across Defense Systems

Based on application, the market is segmented into, power distribution, mission systems & sensors, EW/SIGINT, weapon systems, and comms networks.

Power distribution segment dominated the market in 2025. Military cables operation begins with clean, reliable power, regardless of the platform. Radars, EW suites, communications, mission computers, sensors, actuators, and vehicle or ship subsystems rely on power distribution. As militaries add more electronics and higher-load equipment, power distribution becomes the constant requirement that grows with every upgrade and new capability.

In October 2020, the U.S. Department of Defense issued MIL-STD-2003B. This active standard outlines shipboard installation requirements for electrical cabling and related electric-plant elements. It emphasizes how essential and mission-critical power distribution and cabling are in military environments.

Comms networks is fastest growing segment in market at a CAGR of 7.9% across the forecast period.

By End User

Army Forces Dominates Due to Size Of Land Force Fleets and Ongoing Modernization

Based on end user, the market is segmented into army forces, navy forces, air & space forces and others.

Army forces segment held the largest share of the market in 2025. Army fleets are typically the biggest driver for military cables. Tanks, infantry fighting vehicles, air-defense vehicles, artillery systems, and command/support trucks build a large installed base that regularly sees upgrades. Each update, such as new radios, battle-management systems, sensors, power management, active protection, and electronic warfare kits, quietly increases the demand for wiring and replacements. Consequently, army forces often have the highest ongoing spending on retrofits, depot maintenance and platform modernization.

In April 2025, the U.S. Congressional Research Service (CRS) updated its report on the M-1E3 Abrams modernization program. It pointed out that in 2020, General Dynamics Land Systems received a USD 4.6 billion contract for M-1A2 SEPv3 upgrades, which are expected to wrap up by June 2028.

Air & space forces segment is expected to show fastest market growth at a CAGR of 7.0% across the forecast period.

Military Cables Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Middle East, and Rest of the World (Africa, and Latin America).

North America

North America Military Cables Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America leads as the U.S. has largest and most capable military structure. It boasts more aircraft, ships, and land fleets, along with ongoing upgrades to its C4ISR systems. This drives a steady need for durable power and data cables, higher bandwidth connections and regular cable assembly and harness work during upgrades and maintenance. This pace of modernization strengthens the region’s market position in the military cabling and harnessing. While Canada contributes to this demand, the scale of the U.S. distinguishes the region.

In April 2025, SIPRI reported that U.S. military spending reached about USD 997 billion in 2024, marking a 5.7% increase from the previous year. The U.S. accounted for roughly 37% of global military spending.

U.S. Military Cables Market

Based on North America market size, the U.S. market had reached at USD 0.71 billion in 2025, increasing at a CAGR of 5.7%.

Europe

Europe market size was second largest in 2025, during the forecast period, the Europe region is projected to have a CAGR of 6.5%. The market in Europe was at USD 0.53 billion in 2025. Europe’s need for cables comes from urgent updates in air defense, electronic warfare, secure communications, and improvements for vehicles, aircraft and ships. As fleets are refreshed quickly, power distribution, RF/coax, data, and fiber systems are replaced or expanded during the integration process.

In April 2025, SIPRI reported that Europe’s military spending increased 17% in 2024 to USD 693 billion, mainly due to Russia-Ukraine war and a greater need for readiness.

U.K. Military Cables Market

U.K. market reached USD 0.06 billion in 2025, equivalent to around 10.55% of market revenues.

Germany Military Cables Market

The Germany market was at USD 0.07 billion in 2025, representing roughly 13.28% of market sales.

Asia Pacific

Asia Pacific market is third largest and is anticipated to be the second fastest growing segment during the forecast period, growing at a CAGR of 6.8%. The region shows steady growth. There are more sensors, increased networking, electronic warfare, and greater platform complexity, especially as air and maritime capabilities are modernized. This leads to higher demand for high-bandwidth connectivity and more durable cabling and harnessing during upgrades and new production. Moreover, ongoing updates to military capabilities are boosting Asia Pacific’s market position globally.

In April 2025, SIPRI reported that military spending in Asia and Oceania reached USD 629 billion in 2024, a rise of 6.3% from the previous year and an increase of 46% since 2015.

China Military Cables Market

China’s market is projected to be one of the largest Asia Pacific, with 2025 revenues at USD 0.25 billion, representing roughly 43.29% of market sales.

India Military Cables Market

The India market in 2025 was at USD 0.07 billion, accounting for roughly 14.97% of market revenues.

Middle East

Middle East market anticipated to be the fastest growing segment during the forecast period, growing at a CAGR of 7.3%. The region’s demand is shaped by the rapid growth of capabilities such as air defense networks, electronic warfare, hardened communications, and base infrastructure. There is always a need for cables and its assemblies for integration.

In April 2025, SIPRI stated that military spending in the Middle East hit around USD 243 billion in 2024, marking a 15% increase from the year before. The Gaza war and wider regional conflicts were major factors fueling this increase.

Saudi Arabia Military Cables Market

Saudi Arabia market is projected to be the largest in Middle East, with 2025 revenues was at USD 0.08 billion, representing roughly 41.59% of market sales.

Türkiye Military Cables Market

Türkiye market in 2025 is was at USD 0.03 Billion, accounting for roughly 19.10% of Asia Pacific Military Cables revenues.

Rest of the World

Rest of World (Africa and Latin America), has comparatively smaller share but is growing at a CAGR of 5.8%. Latin America and Africa focus more on upgrading. Modernization occurs in specific areas, and the demand is for maintaining existing platforms and infrastructure. This often leads to a greater emphasis on replacement, repair and practical improvements instead of new designs.

In April 2025, SIPRI reported that Africa spent USD 52.1 billion in 2024, which is a 3.0% increase from the previous year. South America, on the other hand, was nearly unchanged at USD 53.6 billion, showing a slight decrease of 0.1% from the previous year.

Latin America Military Cables Market

The Latin America market was at USD 0.04 million, accounting for roughly 45.29% of market revenues.

Africa Military Cables Market

Africa market is reached USD 0.05 billion in 2025, and is expected to reach USD 0.09 billion in 2034, representing roughly 54.71% of market sales.

COMPETITIVE LANDSCAPE

Key Industry Players

Company’s Scale, Qualification, and Integration Speed Drives Market Competition

The global military cables market is competitive and fragmented. It has two main groups, large interconnect companies that provide extensive catalogs and global manufacturing, and specialist firms that excel in program-specific ruggedization and complex harness builds. Buyers, including primes, tier integrators, and MRO depots, usually focus on a company's qualification history, EMI/EMC performance, reliability in tough environments, and delivery assurance. A cable failure can lead to mission failure, and a late harness can disrupt an entire production line. Demand is increasingly linked to applications including C4ISR backbones, EW suites, radar chains, secure communication nodes, and vehicle, ship, and aircraft modernization. These are vital military applications where uptime and signal integrity are essential.

Companies such as TE Connectivity Ltd., Amphenol Corporation, Carlisle Interconnect Technologies, Collins Aerospace (RTX Corporation), Nexans S.A., Prysmian Group, HUBER & SUHNER AG, Radiall S.A., Rosenberger Hochfrequenztechnik GmbH & Co. KG and LAPP Group compete by providing lighter, denser, and higher-bandwidth solutions with more fiber and better data links. They also focus on maintaining supply continuity, which helps primes integrate more quickly and allows MRO shops to retrofit.

LIST OF KEY MILITARY CABLES COMPANIES PROFILED

- TE Connectivity Ltd. (Switzerland)

- Amphenol Corporation (U.S.)

- Carlisle Interconnect Technologies (U.S.)

- Collins Aerospace (RTX Corporation) (U.S.)

- Nexans S.A. (France)

- Prysmian Group (Italy)

- HUBER & SUHNER AG (Switzerland)

- Radiall S.A. (France)

- Rosenberger Hochfrequenztechnik GmbH & Co. KG (Germany)

- LAPP Group (Germany)

- Corning Incorporated (U.S.)

- Belden Inc. (U.S.)

- Leoni AG (Germany)

- Samtec, Inc. (U.S.)

- Molex, LLC (U.S.)

- Glenair, Inc. (U.S.)

- TT Electronics plc. (U.K.)

- Eaton Corporation plc. (Ireland)

- General Cable (Prysmian Group) (U.S.)

- Northern Technologies / NTE (U.S.)

KEY INDUSTRY DEVELOPMENTS

- September 2025: The DoD moved forward with CMMC implementation, launching Phase 1 in November 2025. They published the final DFARS rule that incorporates CMMC requirements into contracts, raising compliance expectations for defense suppliers, including those providing cable and harnesses that handle controlled data.

- February 2025: Rheinmetall introduced the TaWAN LBO framework, set for 10 years, starting with a first call-off of around USD 1.94 billion. This program focuses on a deployable, interference-resistant communications network, which will directly boost the demand for high-performance cabling in land C4ISR systems.

- December 2024: Germany announced the D-LBO vehicle integration award, worth USD 2.06 billion. This effort aims to digitize around 10,000 vehicles, which will require significant retrofit wiring and harness work.

- October 2024: Leidos received a USD 303.00 million contract from the U.S. Air Force. This contract supports the ABMS Digital Infrastructure network, which is part of a major effort to connect various systems through a robust network infrastructure, including the cabling and harnessing needed for it.

- July 2024: NATO published the Defence-Critical Supply Chain Security Roadmap. This was endorsed by Defence Ministers in June 2024 to lower disruption risk and dependencies in defense-critical industrial supply chains.

- January 2024: Amphenol announced it would acquire Carlisle Interconnect Technologies (CIT) for USD 2.03 Billion in cash. This marks a significant consolidation in the market for interconnects and cable assemblies used in defense platforms that operate in harsh environments.

- January 2022: the U.S. DoD/DLA kept MIL-STD-1678 (Part 6) as an active standard for Fiber Optic Cabling Systems Requirements and Measurements. This reinforced the need for standardized parts and common requirements for platform fiber harnessing.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.4% from 2026 to 2034 |

| Unit | Value (USD Billion) |

|

Segmentation |

By Cable Type

|

|

By Platform

|

|

|

By Procurement

|

|

|

By Application

|

|

|

By End User

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 2.16 billion in 2026 and is projected to reach USD 3.54 billion by 2034.

In 2025, the market value stood at USD 0.75 billion.

The market is expected to exhibit a CAGR of 6.4% during the forecast period of 2026-2034.

The power cables led the market by cable type.

Increased defense budgets are driving procurement and upgrade cycles, raising the demand for high-performance military cabling.

TE Connectivity Ltd., Amphenol Corporation, Carlisle Interconnect Technologies, Collins Aerospace (RTX Corporation), Nexans S.A., Prysmian Group, HUBER & SUHNER AG, Radiall S.A., Rosenberger Hochfrequenztechnik GmbH & Co. KG and LAPP Group are few major players.

North America dominated the market by holding the largest share.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us