RF Device and Semiconductor Test Fixture Market Size, Share & Industry Analysis, By Device Type (Power Amplifier, Low-Noise Amplifier, RF Switch, Mixer, Divider/Combiner, Filter, Duplexer/Multiplexer, & Others), By Technology/Material (CMOS RFIC, GaAs MMIC, GaN, SiGe, and InP), By Frequency Band (<1 GHz, 1–6 GHz, 6–24 GHz, and >24 GHz), By Application (Mobile Devices, Telecom Infrastructure, Automotive (Radar, V2X), & Others), By Test Stage (Wafer-Probe Test, Package/Final Test, Module-Level RF Test, & Others), By Fixture Type, By Customer Type, and Regional Forecast, 2026-2034

RF DEVICE AND SEMICONDUCTOR TEST FIXTURE MARKET SIZE AND FUTURE OUTLOOK

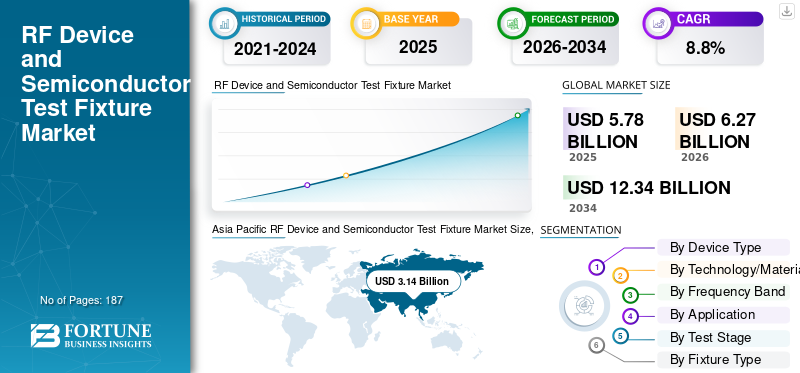

The global RF device and semiconductor test fixture market size was valued at USD 5.78 billion in 2025. The market is projected to grow from USD 6.27 billion in 2026 to USD 12.34 billion by 2034, exhibiting a CAGR of 8.8% during the forecast period. Asia Pacific dominated the RF device and semiconductor test fixture market with a market share of 54.32% in 2025.

The global market refers to the revenue generated from hardware solutions and interfaces designed to enable organizations to test, measure, and validate RF devices, components, and modules used in high-frequency applications across various industries. These fixtures play a critical role in ensuring the accuracy and performance of RF devices by providing electrical connections, mechanical alignment, and signal integrity during testing and validation.

The scope of the global RF test equipment industry encompasses a wide range of test fixtures, including probe cards, test sockets, RF module test fixtures, OTA/chamber fixtures, burn-in boards, and RF inspection probes. It serves a wide range of applications, including mobile devices, telecom infrastructure, automotive (Radar, V2X), aerospace and defense, industrial and test equipment, and IoT & consumer electronics.

The market is driven by growing demand for advanced testing solutions, driven by the rise of RF devices across sectors, miniaturization, increased R&D investment, and regulatory compliance.

Key players in the market include Keysight Technologies, Form Factor, Rohde & Schwarz GmbH & Co. KG, Advantest Corporation, Teradyne Inc., Technoprobe S.p.A., MICRONICS JAPAN CO., LTD., MPI Corporation, GGB Industries, and Fairview Microwave.

Download Free sample to learn more about this report.

RF Device and Semiconductor Test Fixture Market KEY TAKEAWAYS

- 2025 Market Size: USD 5.78 billion

- 2026 Market Size: USD 6.27 billion

- 2034 Forecast Market Size: USD 12.34 billion

- CAGR: 8.8% from 2026–2034

- Asia Pacific dominated the RF device and semiconductor test fixture market with a 54.32% share in 2025.

- The RF Front-End Modules (FEMs) segment held the largest market share of 26.9%.

- The CMOS RFIC segment held the largest market share of 35.2%.

Asia Pacific

The market is estimated at USD 3.14 billion in 2025, maintaining the leading market position with a 54.32% share.

North America

The region held the second-largest market share of 23.2%, driven by the rapid growth of 5G networks, IoT devices.

Europe

The region held a 14.3% market share, supported by its strong presence in wireless communication technologies.

U.S.

The market was valued at around USD 1.13 billion in 2025.

Japan

The market was valued at around USD 0.46 billion in 2025.

Read More

RF DEVICE AND SEMICONDUCTOR TEST FIXTURE MARKET TRENDS

Shift toward System‑Level and Over-The-Air Testing is a Prominent Market Trend

The shift toward system-level and over-the-air (OTA) testing is being driven by the increasing complexity of RF devices, particularly with the rise of 5G technology. Traditional testing methods, such as wafer-probe and package-level tests, cannot effectively validate the full functionality of next-gen devices. Features such as multi-antenna arrays and beamforming require performance validation in real-world conditions, which OTA testing can provide. As the demand for more integrated devices grows, OTA testing has become a critical part of the validation process, ensuring optimal performance across diverse operating environments. Therefore, OTA testing is essential for ensuring the reliable performance of advanced RF device and semiconductor test fixtures in the evolving 5G and IoT landscape.

- According to Rohde & Schwarz, OTA testing for mobile devices is projected to grow at a 14% CAGR from 2023 to 2028, reflecting the growing demand for real-world performance validation in the RF industry.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Increasing RF Content and Complexity in End‑User Devices Drive Market Growth

The increasing RF content in end-user devices is primarily driven by the growing demand for advanced wireless technologies, such as 5G, Wi-Fi and IoT. These technologies require devices to integrate more RF components, such as multi-band support and higher data throughput, which, in turn, drives the need for sophisticated testing. As devices incorporate more RF functionality, manufacturers face increasing challenges in ensuring consistent performance across a broader range of frequencies. Consequently, manufacturers must invest in advanced RF test fixture solutions to meet the evolving demands of RF performance in next-generation wireless devices, further boosting RF device and semiconductor test fixture market growth.

- According to Ericsson, the number of 5G-enabled devices is expected to surpass 2.7 billion globally by 2025, accelerating the need for RF test solutions across various device types.

MARKET RESTRAINTS

High Complexity and Cost of Advanced RF Test Fixture Design Limits Market Growth

Designing advanced RF test fixtures is complex, especially as the demand for mmWave testing (above 24 GHz) increases. These devices require specialized test solutions to replicate real-world conditions, such as multi-antenna systems and beamforming. The need for precision components and advanced materials increases both complexity and cost. Moreover, test fixtures must support various testing stages, including wafer-probe, module-level, and OTA/system-level testing, adding further challenges to the design process. As a result, developing RF devices and semiconductor test fixtures for high-frequency devices requires significant investment in both technology and time.

MARKET OPPORTUNITIES

Emerging High‑Frequency Applications and mmWave Rollouts Create Market Opportunities

The continuous advancement of wireless technologies has pushed RF device and semiconductor test fixture performance into higher frequency bands, especially in the mmWave spectrum (>24 GHz). This shift presents unique challenges for testing and validation, as signals at these frequencies face greater propagation losses, higher susceptibility to interference, and stricter tolerances. Traditional testing fixtures, designed for sub-6 GHz frequencies, are insufficient for ensuring impedance control, low loss, and repeatability at mmWave frequencies. To overcome these challenges, RF test fixture manufacturers are developing advanced mechanical and interconnect solutions to meet the performance requirements for wafer-probe, module, and OTA/system-level testing. As a result, the ongoing innovation in such RF test fixtures is essential to support the growing demands of mmWave technology and ensure reliable performance in next-generation wireless systems.

- According to Qualcomm, mmWave spectrum is expected to account for up to 20% of global 5G deployments by the mid-2020s, highlighting the need for specialized testing infrastructure.

SEGMENTATION ANALYSIS

By Device Type

RF Front-End Modules Dominate due to their Role in Wireless Communication Systems

Based on the device type, the market is divided into Power Amplifier (PA), Low-Noise Amplifier (LNA), RF switch, mixer, divider/combiner, filter (SAW/BAW/LC), duplexer/multiplexer, RF MEMS, and RF Front-End Modules (FEMs).

RF Front-End Modules (FEMs) hold the largest share of 26.9% in the global market due to their crucial role in wireless communication systems, which involve power amplification, filtering, and signal conversion.

Filters (SAW/BAW/LC) hold the second-largest share due to their importance in filtering signals and minimizing interference in RF device and semiconductor test fixtures.

By Technology/Material

CMOS RFIC Leads due to Low Power Consumption and Cost-effectiveness

Based on the technology/material, the market is divided into CMOS RFIC, GaAs MMIC, GaN (GaN-on-Si/GaN-on-SiC), SiGe, and InP.

CMOS RFIC holds the largest share of 35.2% in the global market due to its low power consumption, cost-effectiveness, and wide range of applications such as signal generators in consumer electronics, particularly in mobile devices.

GaN (GaN-on-Si/GaN-on-SiC) is expected to grow at the highest CAGR due to its high efficiency, superior performance at elevated frequencies, and ability to handle high-power applications.

By Frequency Band

1–6 GHz Band Dominates due to its Use in Communications Systems

Based on the frequency band, the market is divided into <1 GHz, 1–6 GHz, 6–24 GHz, and >24 GHz (mmWave).

The 1–6 GHz frequency range holds the largest share of 53.4% in the global market due to its widespread use in communication systems, including 4G LTE, 5G, and Wi-Fi.

The >24 GHz (mmWave) band is expected to experience the highest CAGR during the forecast period due to its pivotal role in 5G and future 6G networks, providing ultra-high-speed data transmission and low latency.

By Application

Mobile Devices Lead due to Smartphone and Wearable Adoption

Based on the application, the market is divided into mobile devices, telecom infrastructure, automotive (radar, V2X), aerospace & defense, industrial & test equipment, and IoT & consumer electronics.

Mobile devices lead the global market with 39.5% of share, driven by the widespread adoption of smartphones, wearables, and other connected devices that rely on RF technologies.

Telecom infrastructure is expected to grow at the highest CAGR, driven by the rapid deployment of 5G networks and the increasing need for testing solutions across base stations, antennas, and cell towers.

To know how our report can help streamline your business, Speak to Analyst

By Test Stage

Wafer-Probe Test Leads are Used for Semiconductor Testing

By test stage, the market is segmented into wafer-probe test, package/final test, module-level RF test, OTA/system-level test, and burn-in & reliability test.

The wafer-probe test (including RF wafer inspection) holds the largest share of 32.5%. It is expected to grow at the highest CAGR due to its vital role in testing the electrical performance of semiconductor wafers during the production process.

The package/final test holds the second largest share as it ensures that fully integrated RF devices meet performance standards before deployment.

By Fixture Type

Probe Cards are Required for Wafer-Level Testing

By fixture type, the market is segmented into probe cards, test sockets, RF module test fixtures, OTA/chamber fixtures, burn-in boards, and RF inspection probes.

Probe cards hold the largest share of 34.3% and are expected to grow at the highest CAGR, driven by their essential role in wafer-level testing for semiconductor manufacturers.

Test sockets hold the second-largest share due to their role in package-level testing for RF components in mobile devices and other electronics.

By Customer Type

Foundries Dominate due to Large-scale Production and Testing

By customer type, the market is segmented into IDMs, fabless companies, foundries, OSATs, module integrators, and test & certification labs.

Foundries hold the maximum share of 22.8% in the global market due to their large-scale semiconductor production, which requires extensive testing of RF components at various stages.

Test & certification labs are projected to record the highest CAGR as the complexity of RF device and semiconductor test fixtures and the regulatory demand for certification testing increase.

RF Device and Semiconductor Test Fixture Market Regional Outlook

By region, the market is categorized into North America, South America, Europe, the Middle East & Africa, and the Asia Pacific.

Asia Pacific

Asia Pacific RF Device and Semiconductor Test Fixture Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific market holds the largest RF device and semiconductor test fixture market share, at 54.3%, due to the region’s dominance in semiconductor manufacturing, particularly in countries such as China, South Korea, and Japan. With a strong foothold in the global semiconductor supply chain, demand for RF testing solutions is driven by the growing production of RF front-end modules, 5G devices, and advanced electronic components.

- According to the China Semiconductor Industry Association (CSIA), China's semiconductor market is expected to reach USD 200 billion by 2025, further driving demand for RF test fixtures in manufacturing.

Japan RF Device and Semiconductor Test Fixture Market

The Japan market in 2025 was valued at around USD 0.46 billion, accounting for roughly 7.9% of global revenues.

China RF Device and Semiconductor Test Fixture Market

China’s market is projected to be one of the largest worldwide, with 2025 revenues recorded at around USD 0.92 billion, representing roughly 16.0% of global sales.

India RF Device and Semiconductor Test Fixture Market

The Indian market value in 2025 was recorded at around USD 0.43 billion, accounting for roughly 7.5% of global revenues.

North America

North America holds the second-largest share of 23.2% in the global market, primarily driven by the rapid growth of wireless communication technologies, which have increased the complexity and volume of RF testing requirements across various industries. The widespread adoption of 5G networks, IoT devices, and connected systems has increased demand for advanced test fixtures to ensure reliable performance and compliance across higher-frequency bands during testing.

- According to a report by I‑Connect007, the North American RF components market is projected to grow from USD 42.8 billion in 2024 to USD 122.99 billion by 2033, underscoring the increasing demand for robust testing infrastructure as RF technologies evolve.

U.S. RF Device and Semiconductor Test Fixture Market

The U.S. market size was analytically valued at around USD 1.13 billion in 2025, accounting for roughly 19.5% of sales.

Europe

The European market holds a significant 14.3% share, driven by the region’s leadership in wireless communication technologies and semiconductor manufacturing capabilities. With a strong presence of major telecommunications companies, device manufacturers, and leading RF front-end module suppliers, Europe is at the forefront of 5G and IoT technology adoption, driving robust demand for test fixtures.

- According to a European Commission report, the European Union's telecommunications market is projected to exceed €200 billion by 2026, further accelerating the need for advanced RF testing solutions.

U.K. RF Device and Semiconductor Test Fixture Market

The U.K. market in 2025 was valued at around USD 0.12 billion, representing roughly 2.1% of global revenues.

Germany RF Device and Semiconductor Test Fixture Market

Germany’s market reached approximately USD 0.14 million in 2025, equivalent to around 2.5% of global sales.

Middle East & Africa

The Middle East & Africa market is projected to grow at the highest CAGR of 11.8%, driven by the region's rapid adoption of 5G networks and increasing investment in telecommunications and electronics infrastructure. The expansion of 5G networks in key markets such as the UAE, Saudi Arabia, and South Africa is driving demand for high-performance RF testing solutions to ensure reliability and compliance with evolving industry standards.

- According to the UAE Telecommunications Regulatory Authority (TRA), the country’s 5G network is expected to cover 80% of the population by 2025, accelerating the need for advanced RF test fixtures in mobile and wireless communication technologies.

GCC RF Device and Semiconductor Test Fixture Market

The GCC market reached around USD 0.09 billion in 2025, representing roughly 1.6% of global revenues.

South America

The South America market is projected to grow at the second-highest CAGR of 10.7%, driven by the rapid expansion of the telecommunications and consumer electronics industries in the region. With increasing demand for wireless communication technologies and IoT devices, manufacturers are investing more in test fixtures to ensure performance validation and regulatory compliance.

- According to a report by the International Telecommunication Union (ITU), South America’s mobile broadband penetration has grown by over 30% in the last five years, further driving the need for RF validation in wireless devices.

Brazil RF Device and Semiconductor Test Fixture Market

The Brazil market size in 2025 was valued at around USD 0.12 billion, accounting for roughly 2.1% of global revenues.

COMPETITIVE LANDSCAPE

Key Test Stage Players

Key Players Launch New Solutions to Strengthen Market Positioning

Players launch new solutions to enhance their market positioning by leveraging technological advancements, addressing diverse consumer needs, and staying ahead of competitors. They prioritize portfolio enhancement, strategic collaborations, and acquisitions and partnerships to strengthen their offerings. Such strategic decisions enable the companies to maintain and expand their market share in a rapidly evolving landscape.

LIST OF KEY RF DEVICE AND SEMICONDUCTOR TEST FIXTURE COMPANIES PROFILED

- Keysight Technologies (U.S.)

- FormFactor (U.S.)

- Rohde Schwarz GmbH & Co. KG (Germany)

- Advantest Corporation (Japan)

- Teradyne Inc (U.S.)

- Technoprobe S.p.A (Italy)

- MICRONICS JAPAN CO., LTD. (Japan)

- MPI Corporation (Taiwan)

- GGB Industries (U.S.)

- Fairview Microwave (U.S.)

- Murata Manufacturing Co., Ltd. (Japan)

- Broadcom Inc. (U.S.)

- Qualcomm Inc. (U.S.)

- Skyworks Solutions, Inc. (U.S.)

- B&K Precision Corporation (U.S.)

KEY INDUSTRY DEVELOPMENTS

- December 2025: Advantest announced it would showcase its latest semiconductor test solutions at SEMICON Japan 2025 in Tokyo, highlighting advanced test platforms for applications such as high-performance computing (HPC), AI, 6G, and automotive semiconductor testing.

- November 2025: Advantest confirmed it will feature its latest semiconductor test solutions at SEMICON Europa 2025 in Munich, Germany, including a scalable MTe platform for advanced power and IC testing for next-gen wide-bandgap devices.

- October 2025: Advantest announced it would showcase its latest semiconductor test solutions at SEMICON West 2025 in Phoenix, Arizona, emphasizing its AI/HPC, RF, and high-speed memory test solutions, including the V93000 EXA Scale SoC tester and support for advanced memory technologies.

- September 2025: Advantest announced it would highlight its leading IC test solutions at the 2025 International Test Conference in San Diego, featuring advanced silicon validation and system-level test platforms that address the complexity of SoC and RF device testing.

- August 2025: FormFactor, in collaboration with Keysight Technologies, introduced the InfinityXF Probe, a coaxial wafer probe offering broadband performance from DC to 250 GHz in a single sweep. Designed for high-frequency, high-speed, and next-generation semiconductor testing, it features a compact design, precise tip visibility, durable rhodium contacts, a wide temperature range, and support for automation.

- May 2025: Rohde & Schwarz hosted its RF Testing Innovations Forum 2025, a virtual event focused on recent advancements in RF testing methodologies and technologies for designers and test engineers, including high-frequency calibration and vector network analysis improvements.

- January 2025: Advantest formed strategic partnerships and took minority equity stakes in both FormFactor and Technoprobe to boost collaboration on technology development and printed circuit board (PCB) manufacturing for advanced test fixture and probe technology.

REPORT COVERAGE

The global market analysis provides an in-depth study of the size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also includes a detailed competitive landscape, providing market share and profiles of key players.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 8.8% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Device Type, Technology/Material, Frequency Band, Application, Test Stage, Fixture Type, Customer Type, and Region |

| By Device Type |

|

| By Technology/Material |

|

| By Frequency Band |

|

| By Application |

|

| By Test Stage |

|

| By Fixture Type |

|

| By Customer Type |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 5.78 billion in 2025 and is projected to reach USD 12.34 billion by 2034.

In 2025, the market value stood at USD 3.14 billion.

The market is expected to grow at a CAGR of 8.8% over the forecast period.

By application, the mobile devices sector led the market in 2025.

The market is driven by growing demand for advanced testing solutions, driven by the rise of RF devices across sectors, miniaturization, increased R&D investment, and regulatory compliance.

Keysight Technologies, FormFactor, Rohde & Schwarz GmbH & Co. KG, and Advantest Corporation are some of the prominent players in the market.

Asia Pacific dominated the market in 2025.

The defense market is driven by advancements in AI, growing security needs, autonomous systems, and increasing defense spending, aiming to optimize real-time decision-making, cybersecurity, and operational efficiency.

- 2021-2034

- 2025

- 2021-2024

- 187

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us