Tactical UAV Market Size, Share & Russia Ukraine War Analysis, By Size (MTOW) (Light Tactical UAVs (9 kg to 25 kg), Medium Tactical UAVs (25 kg to 150 kg), and Heavy Tactical UAVs (150 kg to 600 kg)), By Type (Fixed-wing, Rotary-wing, & Hybrid VTOL), By Launch & Recovery Method (Hand Launch, Catapult Launch, & Others), By Component (Airframe, Propulsion, Avionics/Flight Control, Payload, & Others), By Range (Visual Line of Sight, Extended Visual Line of Sight, & Others), By Mission (Intelligence, Surveillance, & Reconnaissance, & Others), By End User, and Regional Forecast, 2026-2034

Tactical UAV Market Size and Future Outlook

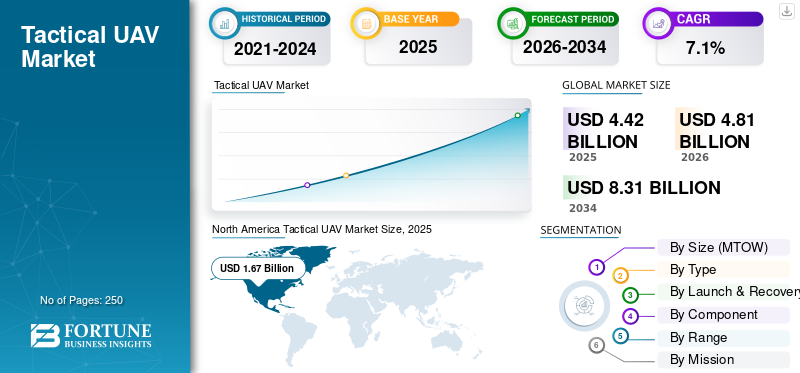

The global tactical UAV market size was valued at USD 4.42 billion in 2025. The market is projected to grow from USD 4.81 billion in 2026 to USD 8.31 billion by 2034, exhibiting a CAGR of 7.1% during the forecast period. North America dominated the tactical UAV market, with a 26.30% share in 2025.

Tactical UAVs are compact, portable unmanned aerial vehicles designed for frontline military use, emphasizing rapid deployment, short- to medium-range operations, and real-time data collection. The global market is experiencing robust growth, fueled by rising demand for affordable, deployable ISR (intelligence, surveillance, and reconnaissance) platforms, advancements in swarm technology, and the push for unmanned systems in asymmetric warfare and national security.

- For instance, in March 2026, the U.S. Army awarded AeroVironment a USD 17.58 million contract for Red Dragon long-range, one-way attack drones optimized for GPS-denied, high-threat environments. The deal includes ground control stations, launchers, spares, training, and support.

Key players such as Lockheed Martin Corporation, Raytheon Technologies Corporation (RTX), Northrop Grumman Corporation, and BAE Systems are prioritizing innovations such as AI-driven autonomous swarming for coordinated strikes, hybrid electric propulsion for extended endurance, and modular payloads for rapid mission reconfiguration.

Download Free sample to learn more about this report.

Tactical UAV Market Key Takeaways

- 2025 Market Size: USD 4.42 billion

- 2026 Market Size: USD 4.81 billion

- 2034 Forecast Market Size: USD 8.31 billion

- CAGR: 7.1% from 2026–2034

- North America dominated the tactical UAV market with a 26.30% share in 2025.

- The Medium Tactical UAVs (25 kg–150 kg) segment leads the global market.

- The Hybrid VTOL segment is projected to grow at the highest CAGR of 8.4% during the forecast period.

Asia Pacific

Asia Pacific reached USD 0.88 billion in 2025.

North America

North America reached USD 1.67 billion in 2025 and is projected to reach USD 1.81 billion in 2026.

Europe

Europe expected to grow at a CAGR of 8.3% during 2026–2034.

U.S.

Large defense budgets and agile procurement continue to strengthen tactical UAV deployment.

Japan

Japan's market reached approximately USD 0.11 billion in 2025, accounting for 2.4% of global revenue.

Read More

Impact of the Russia-Ukraine War on the Market

The Russia-Ukraine war has reshaped the market by underscoring their strategic value in contemporary conflicts. Tactical UAVs have become essential for intelligence gathering, surveillance, and precision targeting, prompting accelerated adoption across military operations.

This conflict has increased global demand for such systems, driving investments in production capabilities and technological advancements. Nations are prioritizing scalable manufacturing to meet operational needs in dynamic battle environments. The war has also driven focus on countermeasures, including electronic warfare integration, to address vulnerabilities exposed in real-world scenarios. Defense industries worldwide are adapting procurement processes for faster deployment cycles.

- For instance, in February 2026, Kratos Defense & Security Solutions aimed to increase XQ-58 Valkyrie collaborative combat aircraft production from 8 to 40 units annually by 2028, targeting current customers such as the U.S. Marine Corps and a potential sole-source deal.

Impact of the Middle East War on the Market

The Middle East conflicts have significantly influenced the market by increasing their operational centrality in regional security dynamics. Tactical UAVs have emerged as indispensable assets for persistent surveillance, border monitoring, and targeted engagements across diverse terrains, accelerating their integration into multi-domain operations. This has promoted regional procurement activities, with defense establishments prioritizing platforms that offer extended endurance and multi-payload adaptability. The emphasis on fixed-wing and rotary configurations reflects strategic needs for comprehensive domain awareness in expansive and contested areas.

- For instance, in March 2026, the U.S. military deployed the Low-Cost Uncrewed Combat Attack System (LUCAS) suicide drone in combat against Iran after its Pentagon unveiling by SpektreWorks. LUCAS drones showcase rapid U.S. adaptation of low-cost, expendable tech for high-threat operations.

TACTICAL UAV MARKET TRENDS

Proliferation of Low-Cost Attributable Designs Emerges as a Key Market Trend

The market exhibits a pronounced trend toward low-cost, attritable platforms optimized for high-volume deployment in contested environments. This evolution reflects operational imperatives for sustained presence amid elevated attrition rates, favoring modular architectures that leverage commercial-off-the-shelf components. Manufacturers are streamlining production processes to enable rapid iteration, aligning with doctrinal shifts emphasizing swarm tactics over singular high-value assets. In addition, there is a rise in the development and deployment of low-cost attritable UAVs to enhance tactical flexibility by integrating seamlessly with manned-unmanned teaming constructs.

- For instance, in March 2026, the U.S. military deployed the Low-Cost Uncrewed Combat Attack System (LUCAS) suicide drone in combat against Iran.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Investment in Sensor Fusion Technologies to Drive Market Growth

A primary driver propelling the industry is the surge in requirement for real-time intelligence, surveillance, and reconnaissance paired with precision strike functionalities. Contemporary operations necessitate persistent domain awareness, which tactical UAVs deliver through extended loiter times and multi-payload versatility. This demand pushes investments in autonomous navigation and sensor fusion technologies, enabling operators to maintain decision superiority in denied-access arenas. Defense procurers across regions are integrating these systems to augment legacy platforms, thereby optimizing resource allocation. Defense procurers across regions are integrating these systems to augment legacy platforms, thereby optimizing resource allocation.

For instance, in March 2026, the U.S. Army awarded AeroVironment a USD 17 million contract for its new Red Dragon long-range, one-way attack drones, featuring a 400+ km range, nearly four times that of the Switchblade 600.

MARKET RESTRAINTS

Supply Chain Vulnerabilities to Limit Market Expansion

Supply chain vulnerabilities represent a significant restraint on market expansion, particularly for critical dual-use electronics and propulsion systems. Geopolitical tensions exacerbate dependencies on concentrated sourcing hubs, leading to production bottlenecks and cost escalations. This constraint compels industry stakeholders to pursue localization strategies, which introduce qualification delays and elevated upfront capital outlays. Mitigation efforts, such as diversified vendor bases, remain challenged by intellectual property protections and regulatory hurdles, which hamper the tactical UAV market growth during the forecast period.

MARKET OPPORTUNITIES

Integration with Electronic Warfare and Counter-UAV Countermeasures Presents Growth Opportunities for the Market

The tactical UAV market presents substantial opportunities through integration with electronic warfare suites and counter-UAV countermeasures. Evolving threats demand layered defense architectures where offensive UAVs synergize with jamming, spoofing, and kinetic interceptors. This interoperability unlocks networked operations, amplifying force multiplication effects in multi-domain scenarios. In addition, the need for reducing reliance on slower, expensive ground‑based EW systems and integration of EW systems in UAVs for different missions and platforms is presenting lucrative opportunities for market growth.

- For instance, in March 2026, TEKEVER and Quadsat successfully completed flight tests integrating the SpectraLoc Electronic Warfare payload on the AR3 EVO tactical UAS, enhancing airborne electromagnetic intelligence collection. When integrated on the AR3 EVO UAS, it turns the drone into an airborne electromagnetic‑intelligence collection node, supporting EW and signals‑intelligence missions.

MARKET CHALLENGES

Regulatory and Ethical Frameworks for Autonomous Operations Act as a Key Market Challenge

A core market challenge lies in navigating evolving regulatory and ethical frameworks governing autonomous tactical UAV employment. Disparate international standards complicate export compliance and interoperability, while domestic policies scrutinize human-in-the-loop requirements for lethal engagements. This regulatory challenge impedes technology maturation, as the validation of sense-and-avoid capabilities frequently encounters certification bottlenecks.

Segmentation Analysis

By Size (MTOW)

High Payload Endurance Supports Medium Tactical UAVs (25 kg to 150 kg) Segment Growth

Based on size (MTOW), the market is divided into light tactical UAVs (9 kg to 25 kg), medium tactical UAVs (25 kg to 150 kg), and heavy tactical UAVs (150 kg to 600 kg).

The medium tactical UAVs (25 kg to 150 kg) segment leads the market, as it occupies the most commercially attractive operating space between small man-portable systems and larger, infrastructure-heavy unmanned platforms. This class offers a more favorable balance of payload capacity, endurance, mobility, and deployment flexibility, making it highly relevant for brigade-level and expeditionary missions. The U.S. Army’s Future Tactical Uncrewed Aircraft System (FTUAS) requirement clearly reflects this demand pattern by prioritizing organic reconnaissance, surveillance, runway independence, and field-level maintainability for Brigade Combat Teams.

The light tactical UAVs (9 kg to 25 kg) segment is anticipated to witness a steady long-term growth, registering a CAGR of 6.9% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Type

Rise in Demand for Fixed Wing UAVs for Overwatch Missions Supported the Segment’s Dominance

By type, the market is segmented into fixed-wing, rotary-wing, and hybrid VTOL.

The fixed-wing segment held the largest market share in 2025 due to superior endurance, broader area coverage, and more efficient persistent surveillance compared to alternative configurations. Fixed-wing configurations are valued for high endurance, payload capacity, and low auditory and visual signatures. Moreover, the rise in demand for fixed-wing UAVs for border monitoring, deep-area reconnaissance, coastal surveillance, and overwatch missions is driving the segment’s growth.

- For instance, in March 2026, the U.S. Army plans to operationally field AV’s P550 vertical take‑off and landing (VTOL) uncrewed aerial system to infantry battalions under the Long Range Reconnaissance (LRR) program. Covered by a USD 117 million production contract, the P550 would provide frontline units with long‑range reconnaissance, surveillance, and target acquisition (RSTA) capability, enabling troops to stay beyond the range of immediate threats.

The hybrid VTOL segment is projected to be the fastest-growing segment, registering a CAGR of 8.4% over the forecast period.

By Launch & Recovery Method

Rapid Deployment and Runway‑Independent Operations Propelled VTOL /No-runway Launch-Recovery Segment Growth

By launch & recovery method, the market is segmented into hand launch, catapult launch, runway/conventional takeoff and landing, and VTOL /no-runway launch-recovery.

The VTOL /No-runway launch-recovery segment led the market in 2025. VTOL and no-runway launch-recovery systems are expanding rapidly, as they solve one of the most critical operational constraints in tactical unmanned operations: dependence on prepared runways or specialized support equipment. Product positioning by leading OEMs such as Schiebel, Textron, and Elbit similarly highlights the ability to operate without prepared surfaces, enabling rapid deployment across land, sea, and urban environments. In addition, advancements in drone design to integrate into expeditionary, naval, and distributed operations are further propelling segment growth.

The hard launch segment is projected to grow at a steady rate of 7.2% over the forecast period.

By Component

Durability in Harsh Operating Conditions Supported Airframe Segment Growth

Based on component, the market is segmented into airframe, propulsion, avionics/flight control, payload, ground control station, and others.

The airframe segment dominated the market in 2025, as platform growth increasingly depends on structural efficiency, modularity, payload adaptability, and durability in harsh operating conditions. Moreover, key players in the industry are improving carbon fiber and titanium fuselage construction to support wider payload and endurance combinations, directly linking airframe design to mission versatility. In addition, research and development in airframe design support lower weight, improved transportability, and enhanced field maintainability.

- For instance, in March 2026, the U.S. Army Research Laboratory and combat Soldiers have jointly developed SPARTA, a 3D‑printed small UAS designed to enhance squad‑level intelligence, surveillance, and reconnaissance through low‑cost, field‑repairable platforms. The airframe is being developed as a fully 3D‑printable, modular structure that can be produced overnight and assembled without specialized tools, with a design that intentionally absorbs crash damage so the relatively inexpensive plastic frame can be replaced while reusing the same electronics.

The payload segment is expected to grow at a CAGR of 15.5% over the forecast period.

By Range

High Operational Reach Boosted Beyond Visual Line of Sight (BVLOS) Segment Growth

Based on range, the market is segmented into Visual Line of Sight (VLOS), Extended Visual Line of Sight (EVLOS), and Beyond Visual Line of Sight (BVLOS).

The Beyond Visual Line of Sight (BVLOS) segment held the largest share of the market in 2025 owing to high operational reach, mission relevance, and economic value of tactical UAV platforms. There is a surge in need for the product with BVLOS capability to enable longer-range reconnaissance, wider-area border surveillance, communications relay, and fewer operational interruptions.

The Extended Visual Line of Sight (EVLOS) segment is projected to grow at a CAGR of 6.7% over the forecast period.

By Mission

Increase in Demand for Swift Decision Making in Defense Forces Supported Intelligence, Surveillance, & Reconnaissance Segment Growth

Based on mission, the market is segmented into intelligence, surveillance, & reconnaissance, communications/relay networking, target acquisition/fire correction, EW/SIGINT/ELINT support, maritime domain awareness, and border security/homeland surveillance.

The intelligence, surveillance, & reconnaissance segment held the largest tactical UAV market share in 2025, owing to an increase in demand for swift decision-making in defense forces with improved situational awareness across land, air, sea, space, and cyber domains. This has propelled procurement demand for unmanned platforms that can collect, process, and transmit actionable intelligence with speed and precision. Manufacturers are also positioning tactical UAVs as multi-mission ISR nodes capable of combining electro-optical, infrared, radar, electronic support, and relay functions.

- For instance, in November 2025, Indian forces awarded home‑grown defence startup ideaForge a roughly USD 11.3 million emergency procurement order for its next‑generation Zolt tactical drone and SWITCH 2 vertical‑takeoff UAV. The deal, driven by successful trials in high‑altitude and jammed electronic‑warfare environments, underscores India’s push to strengthen border‑area precision‑strike and ISR capabilities.

The EW/SIGINT/ELINT support segment is projected to grow at a CAGR of 10.3% over the forecast period.

By End User

Organic, Expeditionary Reconnaissance Integrated With Long‑Endurance UAV Modernization to Propel Segment Growth

On the basis of end user, the market is segmented into army/land forces, navy, air force, special operations forces, border security, and coast guard/maritime law enforcement.

The army/land forces segment is expected to acquire a major share of the market during the study period due to growing demand for organic, responsive reconnaissance without relying entirely on higher-echelon aviation or joint assets. Moreover, army forces are aiming to conduct rapid deployment and integration of long‑endurance drones with alternative propulsion/fuel technologies to modernize and expand their unmanned‑aircraft capabilities. Recent Army procurement activity for long-range reconnaissance systems, along with institutional emphasis on integrating unmanned systems into future combat operations, drives segment growth.

- For instance, in March 2026, the U.S. Army awarded Heven AeroTech a Basic Ordering Agreement (BOA) to simplify procurement of its Z1 hydrogen‑powered unmanned aerial system and supporting hydrogen‑generation equipment.

The navy segment is projected to grow at a CAGR of 10.1% over the forecast period.

Tactical UAV Market Regional Outlook

By geography, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Tactical UAV Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America dominated the market in 2025, with a valuation of USD 1.67 billion and is projected to grow to USD 1.81 billion by 2026. This growth is driven by high defense expenditure, formal military modernization pathways, and a mature operating ecosystem for unmanned systems. The market is growing significantly due to institutional acceptance of tactical UAVs as organic ISR and force-enabling assets. In addition, the region experiences a rise in procurement activity supported by active U.S. Army acquisition reform and ongoing remotely piloted aircraft investment and airspace-integration efforts in Canada.

- For instance, in March 2026, Canadian aerospace firm Volatus Aerospace signed a Memorandum of Understanding with Sentinel R&D to co‑develop a Canadian‑sovereign interceptor UAV, combining Sentinel’s composite airframe engineering with Volatus’ systems integration, autonomy software, and operational expertise. The partnership aims to deliver a domestically developed interceptor platform aligned with Canada’s Defence Industrial Strategy and priority capabilities in defence‑critical UAV technologies.

U.S. Tactical UAV Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market stood at around USD 1.49 billion in 2025. The market is expected to grow significantly due to large defense budgets and increasingly agile acquisition mechanisms. Tactical unmanned systems are being positioned as core enablers of brigade-level reconnaissance, surveillance, targeting support, and broader multi-domain operations. The country also offers a robust procurement environment, which is anticipated to accelerate market growth during the forecast period.

- For instance, in February 2026, the U.S. Army announced plans to acquire at least one million drones over the next two to three years, marking a historic twenty‑fold increase from its current annual purchase of about 50,000 systems. The initiative reflects a strategic shift toward treating drones less as scalable, cost-effective operational assets, influenced by lessons from recent conflicts where large volumes of low‑cost unmanned systems proved battlefield effectiveness.

Europe

Europe is projected to record a growth rate of 8.3% from 2026 to 2034. The region is expected to witness the fastest growth owing to surging demand for tactical ISR, border awareness, resilience, and collaborative defense innovation. European defense funding has increased significantly, and the European Defence Fund is channeling additional resources into collaborative research and development and programs, including technologies relevant to tactical situational awareness and unmanned systems.

- For instance, in March 2026, the European Defence Agency selected Airbus Helicopters, via its subsidiary Survey Copter, to develop a multi‑mission variant of its Capa‑X tactical drone under a USD 1.28 million (€1.1 million), 48‑month M2UAS programme. Using the existing Capa‑X as a baseline, the project will study and evolve a hybrid uncrewed aircraft capable of performing a range of defence missions such as surveillance, reconnaissance, and electronic warfare.

U.K. Tactical UAV Market

The U.K. market in 2025 stood at around USD 0.22 billion, representing roughly 5.0% of global revenues.

Germany Tactical UAV Market

Germany’s market reached approximately USD 0.23 billion in 2025, equivalent to around 5.3%of global sales.

Asia Pacific

The Asia Pacific market reached USD 0.88 billion in 2025. The region is emerging as one of the most attractive growth regions for tactical UAVs as sustained military modernization is being driven by persistent security competition, wide-area surveillance requirements, and expanding national industrial ambitions. The market growth is supported by a broad convergence of ISR prioritization, unmanned capability development, and defense-industrial strengthening. Military expenditure across Asia and Oceania is rising, with major regional defense establishments explicitly reinforcing unmanned, stand-off, and intelligence-related capabilities.

- For instance, in September 2025, India approved a defence‑procurement package worth approximately USD 25 billion aimed at modernising the Army, Air Force, and Coast Guard. The package includes additional Russian‑made S‑400 long‑range air‑defence systems, medium‑range transport aircraft, strike drones, artillery, surveillance systems, and coastal‑security assets.

Japan Tactical UAV Market

The Japanese market in 2025 stood at around USD 0.11 billion, accounting for roughly 2.4% of global revenues.

China Tactical UAV Market

China’s market is projected to be one of the largest worldwide, with 2025 revenues standing at around USD 0.36 billion, representing roughly 8.2% of global sales.

India Tactical UAV Market

The Indian market in 2025 stood at around USD 0.15 billion, accounting for roughly 3.4% of global revenues.

Latin America and the Middle East & Africa

Latin America presents a more selective but still credible growth opportunity in the market, with demand shaped primarily by surveillance-led security missions rather than large-scale warfighting programs. The strongest market opportunity lies in border monitoring, anti-trafficking operations, and maritime and coastal surveillance. The Middle East & Africa will remain strategically important for the product demand owing to high procurement of military UAVs in this region, driven by immediate operational need as much as by modernization planning. In the Middle East, rising military expenditure and a persistently high-threat security environment continue to support investment in unmanned systems for ISR, border monitoring, infrastructure protection.

- For instance, in November 2025, Israeli startup XTEND received a multi‑million‑dollar U.S. Department of Defense contract to develop and deliver AI‑enabled, modular one‑way attack drones for close‑quarter combat. The drones, under the ACQME‑DK program, are small, lethal unmanned aerial systems tailored for irregular warfare in dense urban and confined rural environments.

Saudi Arabia Tactical UAV Market

The Saudi Arabia market in 2025 stood at around USD 0.11 billion, accounting for roughly 2.4% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus on Autonomy Innovation to Gain Competitive Edge

The global tactical UAV market is defined by strong competition among defense contractors and specialized small‑UAV firms delivering short‑to medium‑range reconnaissance, loitering munition, and multi‑role platforms for land, naval, and special‑operations forces. Leading players such as AeroVironment, Elbit Systems, Israel Aerospace Industries, General Atomics, and Textron are prioritizing compact, affordable systems featuring AI‑assisted autonomy, modular payloads, and multi‑domain launch compatibility across infantry, vehicle‑mounted, and shipboard deployments.

Advancements in swarming algorithms, secure data link technologies, and hybrid VTOL‑fixed‑wing designs, together with innovations such as 3D‑printed airframes and rapid‑fielding programs, are accelerating the transition from prototype squad‑level drones to mass‑deployed ISR‑and‑effects layers across modern battlefield architectures.

LIST OF KEY TACTICAL UAV COMPANIES PROFILED

- AeroVironment (U.S.)

- Elbit Systems (Israel)

- Israel Aerospace Industries (Israel)

- Textron Systems (U.S.)

- Thales (France)

- Schiebel (Austria)

- Leonardo (Italy)

- Airbus (France)

- Quantum Systems (Germany)

- Aeronautics (Israel))

KEY INDUSTRY DEVELOPMENTS

- March 2026: The Pentagon awarded San Antonio‑based drone and software firm Darkhive a nearly USD 50 million contract to scale its small‑UAS and counter‑drone technologies for military use. The deal reflects the U.S. military’s push to accelerate procurement of systems that can detect, track, and neutralize hostile drones in contested environments.

- March 2026: The U.S. Army placed an order worth over USD 52 million for more than 2,500 Skydio X10D small unmanned aircraft systems (sUAS). The X10D is designed for tactical intelligence, surveillance, and reconnaissance (ISR), providing soldiers with real‑time situational awareness and target‑acquisition support in complex operational environments.

- February 2026: Teledyne FLIR Defense won a USD 17.5 million contract from Switzerland’s defence procurement agency, armasuisse, to supply multiple Black Hornet 4 Personal Reconnaissance Systems to the Swiss Armed Forces. The nano‑drones will be integrated with the Piranha 8×8 armored engineering vehicle’s digital infrastructure, enabling live video, target coordinates, and situational‑awareness data.

- January 2026: Elbit Systems completed the full acquisition of British drone maker UAV Tactical Systems (UTACS), bringing the Leicester‑based joint venture fully under Elbit ownership while retaining its existing workforce and facilities.

- January 2026: Textron Systems was awarded a contract to supply three Aerosonde Mk 4.7 vertical takeoff and landing (VTOL) unmanned aircraft systems to Tantita Security Services for protecting Nigeria’s critical oil and gas

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.1% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Size (MTOW), By Type, By Launch & Recovery Method, By Component, By Range, By Mission, By End User, and Region |

| By Size (MTOW) |

|

| By Type |

|

| By Launch & Recovery Method |

|

| By Component |

|

| By Range |

|

| By Mission |

|

| By End User |

|

| By Geography |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 4.42 billion in 2025 and is projected to reach USD 8.31 billion by 2034.

In 2025, the market value stood at USD 1.67 billion.

The market is expected to exhibit a CAGR of 7.1% during the forecast period.

By mission, the intelligence, surveillance, & reconnaissance segment led the market in 2025.

Rising investment in sensor fusion technologies is a key factor driving the market.

AeroVironment (U.S.), Elbit Systems (Israel), and Israel Aerospace Industries (Israel) are some of the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 250

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us