Truck Megawatt Charging Market Size, Share & Industry Analysis, By Component (Hardware and Software), By Charging Type (Depot Charging, Public Charging and Semi-Public Charging), By Power Output (1 MW – 2 MW, 2 MW – 3 MW and Above 3 MW), By Application (Long-Haul Transportation, Regional Distribution, Logistics & Warehousing, Industrial Applications and Ports & Intermodal Transport), By End Use (Fleet operators, Charging Infrastructure Providers, Vehicle OEM and Energy Utilities & Grid Operators), and Regional Forecast, 2026-2034.

Truck Megawatt Charging Market Size and Future Outlook

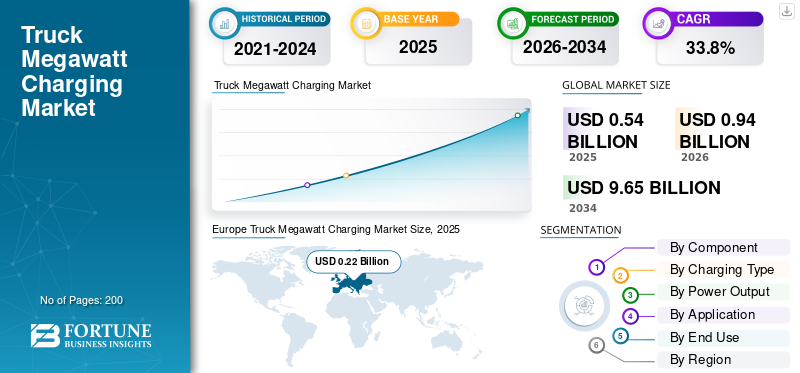

The truck megawatt charging market size was valued at USD 0.54 billion in 2025. The market is projected to grow from USD 0.94 billion in 2026 to USD 9.65 billion by 2034, exhibiting a CAGR of 33.8% during the forecast period.

The market depicts the ecosystem of ultra-high-power charging solutions (typically 1 MW and above) designed for heavy duty electric vehicle (trucks). It includes charging infrastructure, hardware, software, and grid integration systems enabling rapid energy replenishment for long-haul and commercial fleet operations. The market supports electrification of freight transport by reducing charging time, improving operational efficiency, and facilitating adoption of battery electric and fuel cell trucks globally.

Key drivers include rising electrification of heavy-duty transport, stringent emission regulations, and government incentives for zero-emission vehicles. Increasing demand for fast-charging infrastructure to minimize downtime, advancements in battery technology, and expansion of logistics and e-commerce sectors further accelerate adoption of megawatt charging solutions for efficient long-haul operations.

Major players in the market include ABB E-mobility, Siemens, Tesla, ChargePoint, Kempower, Alpitronic, and Shell Recharge, competing through high-power charging technology, grid integration capabilities, and scalable infrastructure solutions. These companies focus on ultra-fast charging systems, smart energy management, partnerships with fleet operators, and expanding charging networks to support long-haul electric truck adoption.

Download Free sample to learn more about this report.

TRUCK MEGAWATT CHARGING MARKET TRENDS

Integration of Smart Energy Management and Digital Charging Ecosystems is a Key Market Trend

A key trend in the market is the growing emphasis on lightweight materials and electronic integration. Manufacturers are increasingly using carbon fiber, advanced alloys, and composite materials to reduce weight while maintaining strength and durability. Simultaneously, electronic shifting systems and wireless technologies are gaining traction among professional and enthusiast cyclists for improved precision and performance. These innovations are enhancing overall riding efficiency and user experience. The trend is also supported by rising participation in competitive cycling and demand for premium bicycles. As technology continues to evolve, component manufacturers are focusing on delivering high-performance, customizable, and aesthetically appealing products to stay competitive.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Stringent Emission Regulations and Decarbonization Targets to Accelerate Market Growth

Governments across North America, Europe, and Asia Pacific are implementing stringent emission norms and net-zero targets, compelling fleet operators to transition toward zero-emission heavy-duty vehicles. Regulations such as CO₂ reduction mandates, diesel bans in urban areas, and green freight initiatives are pushing OEMs and logistics providers to adopt electric trucks. This shift necessitates the development of megawatt charging infrastructure capable of supporting high-capacity large batteries and long-haul operations. Public funding programs and policy frameworks further support infrastructure deployment, reducing the financial burden on stakeholders. As regulatory pressure intensifies, demand for reliable, ultra-fast charging networks is expected to grow significantly, positioning megawatt charging as a critical enabler of sustainable freight transportation, thus driving truck megawatt charging market growth.

MARKET RESTRAINTS

High Capital Investment and Grid Infrastructure Limitations to Restrain Market Expansion

The deployment of megawatt charging systems requires substantial upfront investment in charging hardware, site development, and grid upgrades. These systems demand robust electrical infrastructure, including high-capacity transformers and substations, which may not be readily available in all regions. Additionally, installation costs can be prohibitive for smaller fleet operators and independent charging providers. Grid congestion, permitting delays, and the need for coordination with utilities further complicate project timelines. The lack of standardized pricing models and uncertain return on investment also deter stakeholders from large-scale deployment. These financial and infrastructural barriers collectively slow the pace of adoption, particularly in emerging markets where grid readiness and capital availability remain limited.

MARKET OPPORTUNITIES

Expansion of Long-Haul Electric Trucking to Create Infrastructure Opportunities for Market

The growing adoption of electric trucks for long-haul and regional freight is creating significant opportunities for megawatt charging infrastructure. As battery capacities increase to support extended ranges, the need for ultra-fast charging along highways and logistics corridors becomes critical. This opens avenues for public-private partnerships, corridor-based charging networks, and integration with renewable energy sources. Fleet operators are increasingly seeking dedicated charging hubs to optimize turnaround charging times and improve asset utilization. Additionally, the emergence of truck-as-a-service and electrified logistics ecosystems is driving demand for scalable and interoperable charging solutions. These developments present strong growth potential for infrastructure providers, technology developers, and energy companies entering the market.

MARKET CHALLENGES

Lack of Standardization Across Charging Technologies to Pose Operational Challenges

The absence of globally harmonized standards for megawatt charging systems presents a significant challenge to market growth. Variations in connector types, communication protocols, and charging specifications create compatibility issues between vehicles and infrastructure. This fragmentation can lead to inefficiencies, increased costs, and limited interoperability across regions and manufacturers. Fleet operators may face difficulties in scaling operations due to inconsistent charging experiences. Additionally, evolving standards such as the Megawatt Charging System (MCS) are still in early stages of adoption, leading to uncertainty among stakeholders. Addressing standardization gaps requires collaboration among OEMs, technology providers, and regulatory bodies to ensure seamless integration and widespread deployment of megawatt charging solutions.

Segmentation Analysis

By Component

High Infrastructure Investment and Critical Role in Charging Deployment to Drive Hardware Segment Dominance

Based on component, the market is categorized into hardware and software.

The hardware segment dominates the market due to its essential role in deploying megawatt charging infrastructure, including chargers, power electronics, and grid connection equipment. High capital intensity and the need for robust, high-capacity systems for heavy-duty trucks drive significant investments. Continuous expansion of charging corridors and fleet hubs further sustains demand, as hardware forms the backbone of reliable, ultra-fast charging networks.

The software segment is projected to grow at a CAGR of 35.4% over the forecast period. Increasing adoption of smart charging, energy management systems, and digital platforms for monitoring, billing, and optimization is accelerating demand for advanced software solutions across charging networks.

By Charging Type

Fleet-Centric Charging Needs and Operational Efficiency to Drive Depot Charging Dominance

Based on charging type, the market is categorized into depot charging, public charging, and semi-public charging.

Depot charging dominates the market as fleet operators prefer centralized charging infrastructure at depots to ensure operational control, cost efficiency, and predictable charging schedules. It enables overnight charging, reduces dependency on public infrastructure, and supports high fleet utilization. Large logistics and freight companies are investing heavily in depot-based megawatt charging systems to streamline operations and minimize downtime, reinforcing segment dominance.

Public charging is projected to grow at a CAGR of 35.0% over the forecast period. Expansion of highway charging corridors, government investments, and increasing long-haul electric truck adoption are driving demand for accessible, high-power public charging infrastructure.

To know how our report can help streamline your business, Speak to Analyst

By Power Output

Optimal Balance Between Charging Speed and Infrastructure Feasibility to Drive 1 MW-2 MW Segment Dominance

Based on power output, the market is categorized into 1 MW-2 MW, 2 MW-3 MW, and above 3 MW.

The 1 MW-2 MW segment dominates the market as it offers an optimal balance between high charging speed and manageable infrastructure requirements. This range is widely adopted for current heavy-duty electric trucks, enabling efficient turnaround times without excessive grid strain. It aligns well with existing grid capabilities and is cost-effective for depot and corridor deployments, making it the preferred choice for early-stage megawatt charging rollouts.

The 2 MW-3 MW segment is projected to grow at a CAGR of 37.1% over the forecast period. Increasing battery capacities and demand for ultra-fast charging in long-haul applications are driving adoption of higher power outputs to further reduce charging time.

By Application

Rising Electrification of Freight Corridors to Drive Long-Haul Transportation Segment Dominance

Based on application, the market is categorized into long-haul transportation, regional distribution, logistics & warehousing, industrial applications, and ports & intermodal transport.

The long-haul transportation segment dominates the market due to the growing electrification of freight corridors and increasing demand for zero-emission trucking over extended distances. Megawatt charging is critical for minimizing downtime and enabling high-capacity battery trucks to operate efficiently across highways. Investments in corridor-based infrastructure and partnerships between OEMs, utilities, and logistics providers further reinforce segment leadership.

The industrial applications segment is projected to grow at a CAGR of 33.6% over the forecast period. Increasing electrification of heavy-duty operations in mining, construction, and manufacturing facilities is driving demand for high-power charging solutions to support continuous, energy-intensive vehicle usage.

By End Use

Growing Fleet Electrification and Need for Operational Control to Drive Fleet Operators Segment Dominance

Based on end use, the market is categorized into fleet operators, charging infrastructure providers, vehicle OEMs, and energy utilities & grid operators.

The fleet operators segment dominates the market as logistics companies increasingly electrify their fleets to reduce emissions and operating costs. These operators invest directly in megawatt charging infrastructure to ensure reliability, optimize charging schedules, and maintain high vehicle utilization. Dedicated depot and corridor charging setups enable better control over energy consumption and minimize downtime, reinforcing their leading position.

Charging infrastructure providers are projected to grow at a CAGR of 35.3% over the forecast period. Rising investments in public and corridor-based charging networks, along with partnerships with fleets and utilities, are accelerating the deployment of scalable, high-power charging solutions.

Truck Megawatt Charging Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Middle East & Africa and Latin America.

Europe

Europe Truck Megawatt Charging Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Europe dominates the market due to stringent emission regulations, aggressive decarburization targets, and strong policy backing for zero-emission freight transport. The region benefits from early adoption of electric trucks and significant investments in cross-border charging corridors under initiatives such as AFIR. Collaboration between governments, OEMs, and energy providers accelerates infrastructure deployment. Well-established grid networks and funding programs further support large-scale rollout of megawatt charging systems, reinforcing Europe’s leadership position.

U.K. Truck Megawatt Charging Market

The U.K. market, in 2026 is estimated at around USD 0.05 billion, accounting for a modest share of global revenues. Strong government incentives, net-zero targets, and expanding electric freight corridors are accelerating infrastructure deployment and fleet electrification.

Germany Truck Megawatt Charging Market

The Germany market in 2026 is estimated at around USD 0.10 billion, accounting for a notable share of global revenues. Robust industrial base, early adoption of electric trucks, and heavy investments in highway charging corridors are driving steady market expansion.

Asia Pacific

Asia Pacific holds the second-largest truck megawatt charging market share and is projected to grow at a CAGR of 35.2% over the forecast period. Rapid industrialization, expanding e-commerce, and strong government support for electric mobility drive demand for heavy-duty electric trucks. Countries such as China, Japan, and South Korea are investing heavily in charging infrastructure and battery technologies. Increasing domestic manufacturing capabilities and large-scale fleet electrification initiatives further accelerate adoption across the region.

China Truck Megawatt Charging Market

The China market in 2026 is estimated at around USD 0.21 billion, accounting for a leading share of global revenues. Strong government backing, large commercial vehicle base, and rapid EV infrastructure expansion are accelerating megawatt charging adoption.

North America

North America represents the third-largest market, driven by rising investments in zero-emission freight transportation and supportive regulatory frameworks. Federal and state-level incentives, particularly in the U.S., encourage adoption of electric trucks and charging infrastructure. Expansion of logistics networks and pilot megawatt charging corridor projects are boosting regional market growth. Strategic partnerships between OEMs, utilities, and charging providers are also facilitating infrastructure deployment across key freight routes.

U.S. Truck Megawatt Charging Market

The U.S. market in 2026 is estimated at around USD 0.16 billion, accounting for a significant share of global revenues. Federal funding programs, rising logistics electrification, and pilot megawatt charging corridors are supporting large-scale infrastructure development.

Middle East & Africa

The Middle East & Africa market is in a developing phase, with gradual adoption of electric trucks and charging infrastructure. Government initiatives focused on sustainability, particularly in the UAE and Saudi Arabia, are supporting early-stage deployment. Investments in smart cities and logistics hubs are creating opportunities for megawatt charging solutions. However, limited grid readiness and high infrastructure costs may slow large-scale adoption in the future.

Latin America

Latin America is witnessing steady growth driven by increasing logistics activities and rising focus on sustainable transportation. Countries such as Brazil and Mexico are exploring electric mobility solutions to reduce emissions and fuel dependency. Pilot projects and public-private partnerships are supporting initial deployment of charging infrastructure. While adoption remains at an early stage, improving regulatory support and urban freight electrification trends are expected to drive future demand.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Advancements and Strategic Partnerships to Intensify Market Competition

The truck megawatt charging market is characterized by the presence of established electrical equipment manufacturers, charging solution providers, and emerging technology firms competing to build high-power charging ecosystems. Key players such as ABB, Siemens, Tesla, Kempower, and Alpitronic focus on developing ultra-fast charging systems with enhanced efficiency and scalability. Companies are investing heavily in R&D to improve power output capabilities, reduce charging time, and ensure compatibility with next-generation heavy-duty electric trucks, strengthening their technological positioning.

Market participants are increasingly engaging in strategic collaborations with fleet operators, OEMs, and energy providers to accelerate infrastructure deployment and expand geographic reach. Partnerships, joint ventures, and pilot corridor projects are common strategies to establish early market presence. Additionally, firms are emphasizing software integration, smart energy management, and grid optimization to differentiate their offerings. Competitive intensity is expected to rise as new entrants and regional players focus on innovation, cost optimization, and expanding charging networks globally.

LIST OF KEY TRUCK MEGAWATT CHARGING COMPANIES PROFILED

- ABB E-mobility (Switzerland)

- Siemens (Germany)

- Tesla (U.S.)

- Heliox (Netherlands)

- Kempower (Finland)

- Alpitronic (Italy)

- Delta Electronics (Taiwan)

- Milence (Netherlands)

- Shell Recharge (U.K.)

- bp pulse (U.K.)

- ON (Germany)

- Enel X Way (Italy)

- Daimler Truck (Germany)

- Volvo Group (Sweden)

- Traton Group (Germany)

KEY INDUSTRY DEVELOPMENTS

- March 2026: ABB announced the deployment of its next-generation megawatt charging systems across key European freight corridors, aiming to support long-haul electric trucks with ultra-fast charging and advanced grid integration capabilities.

- March 2026: Tesla has inaugurated the first Megacharger charging station for customers of its electric truck, the Semi, in the US. Tesla plans to open truck chargers at 37 locations by 2026. The first publicly accessible charger has now reportedly gone live in California. The company announced this development on social media.

- December 2025: Kempower secured a major contract to supply megawatt charging solutions for a Nordic logistics fleet, enhancing charging efficiency and supporting regional electrification goals.

- November 2025: Siemens AG Austria and OMV AG have signed a cooperation agreement to reduce CO2 emissions generated by heavy duty vehicle traffic and logistics operations companies. This is what the memorandum of understanding between Siemens AG and OMV AG aims to achieve. The two companies intend to provide innovative and safe charging solutions for the future so-called eDepots to meet sustainable mobility requirements. These offer numerous advantages to fleet operators, especially in the transportation and logistics sector.

- November 2025: Alpitronic launched a high-power charging platform capable of supporting megawatt charging standards, targeting heavy-duty commercial vehicles across Europe.

- October 2025: ChargePoint announced the development of megawatt charging architecture tailored for electric trucks, focusing on scalable infrastructure and smart energy management solutions.

- September 2025: Shell Recharge partnered with fleet operators to deploy high-capacity charging hubs along key logistics corridors in Europe, accelerating adoption of electric freight transport.

REPORT COVERAGE

The truck megawatt charging market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 33.8% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Component, By Charging Type, By Power Output, By Application, By End Use and By Region |

| By Component |

|

| By Charging Type |

|

| By Power Output |

|

| By Application |

|

| By End Use |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 0.54 billion in 2025 and is projected to reach USD 9.65 billion by 2034.

In 2025, the Europe market value stood at USD 0.22 billion.

The market is expected to exhibit a CAGR of 33.8% during the forecast period of 2026-2034

The depot charging segment led the market by power output.

Stringent emission regulations and decarburization targets drive market growth.

Europe held largest share in the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us