Aviation Lubricants Market Size, Share & Industry Analysis, By Chemistry (Mineral (Group I/II/III), Synthetic Esters, Alkylated Naphthalenes, Silicone Fluids, PFPE (Perfluoropolyether), Bio-based Esters, and Water-Glycol), By Technology (Antioxidant Systems, Anti-Wear Systems, EP (Extreme Pressure) Systems, Ashless Dispersant Systems, Corrosion/Sust Inhibition Systems, Metal Deactivators, and Others), By Application (Propulsion System, APU Lubrication, Propulsion-Driven Gearboxes, Airframe Lubrication Points, & Others), By Platform, By End User, and Regional Forecast, 2026-2034

Aviation Lubricants Market Size and Regional Outlook

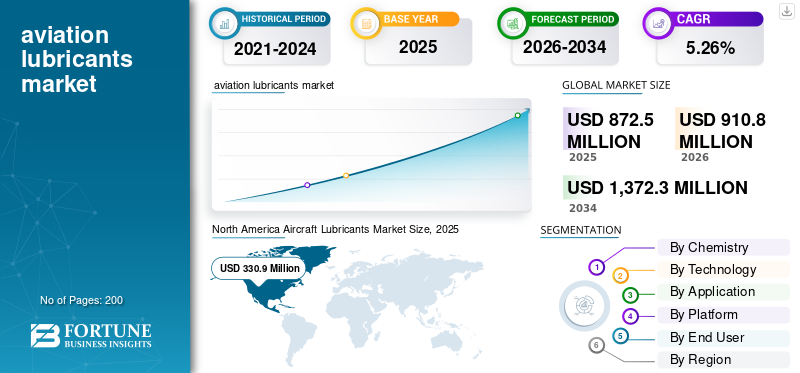

The global aviation lubricants market size was valued at USD 872.5 million in 2025 and is projected to grow from USD 910.8 million in 2026 to USD 1,372.3 million by 2034, exhibiting a CAGR of 5.26% during the forecast period. North America dominated the global market with a market share of 37.92% in 2025.

Aviation lubricants include specialized fluids, oils, greases, or additives intended to reduce friction, cool, or protect components of an aircraft from wear, corrosion, or rust. These lubricants are required in all types of aviation, including commercial aviation segment, military, or general aviation aircraft. They are mostly used in engines, hydraulic systems, landing gears, or airframes, as well as other moving components such as bearings, gears, or piston rings.

The market is expected to grow, driven by the rising air transport movement of more than 5 million per year, as per IATA (International Air Transport Association), and an ever-growing air transport fleet. The factors that enhance growth include rising global air passenger traffic movements, surging disposable incomes, developments and constructions of airports, especially in the Asia Pacific, Latin America, and the Middle East & Africa regions, and government expenditure on military air transport developments.

Market players such as ExxonMobil, Shell, Chevron, TotalEnergies, and BP lead with significant market shares in terms of extensive research & development, distribution networks, and their offerings that include engine oils, hydraulic fluids, and greases.

Download Free sample to learn more about this report.

Aviation Lubricants Market Key Takeaways

- 2025 Market Size: USD 872.5 million

- 2026 Market Size: USD 910.8 million

- 2034 Forecast Market Size: USD 1,372.3 million

- CAGR: 5.26% from 2026–2034

- North America dominated the aviation lubricants market with a 37.92% share in 2025.

- The synthetic esters segment accounted for the largest market share of 58.34% in 2025.

- The commercial fixed wing segment held 54.58% market share in 2025.

North America

North America held 37.92% share in 2025, valued at USD 330.9 million.

Asia Pacific

Asia Pacific market valued at USD 177.2 million in 2025.

Europe

Europe market valued at USD 224.0 million in 2025.

U.S.

The market in the U.S. was valued at USD 305.9 million in 2025.

Japan

The market in Japan was valued at USD 21.6 million in 2025.

Read More

Aviation Lubricants Market Trends

Evolution of Synthetics and Additives in Oils Delivering Better Performance

Synthetic polyalphaolefins provide outstanding oxidative stability for longer life. Ester-based fluids have better low-temperature fluidity for polar applications. Nano-additives improve wear resistance in boundary lubrication. Smart sensors integrate for continuous monitoring. AI-based formulation offers precise failure prediction.

Phased array testing speeds up the qualification process. Bio-synthetics combine performance and renewability. Low volatility bases prevent vapor lock problems. These technologies raise the bar on reliability, driving the demand for high-quality aviation lubricants.

Download Free sample to learn more about this report.

Market Dynamics

Market Drivers

Growing Demand for Modernization and Fleet Expansion to Push Market Growth

The increasing air transport volume across the globe along with modernization programs for aircraft act as major drivers for aviation lubricants market growth. Surging air transport requirements in the aviation industry, driven by economic recovery, lead to demands for superior lubrication capabilities for engine and system high performance. Defense purchases across the globe also drive this industry as advanced fighter aircraft, along with transport aircraft, require superior lubricants for endurance in rugged operating conditions.

- In March 2025, the FAA introduced new specifications for synthetic engine oil used by wide-body aircraft.

Market Restraints

Supply Volatility and Cost Pressures May Hamper the Market Growth

Supply volatility directly affects the cost of production of petroleum-based lubricants. Geopolitical issues cause shortages in feedstock supplies. OEM certification is strict, causing delays in launches. The environmental regulations on additive chemistry increase the cost of compliance for manufacturers. Another challenge comes from new emerging competition. There is complexity in inventory management due to maintenance standards in a mixed fleet.

Market Opportunity

Advanced Applications in Next-Gen Aircraft to Offer New Market Opportunities

Renewable resource bio-based special lubricants show increased acceptance with net-zero commitments. Vegetable oil-based derivatives provide eco-compatibility without affecting their efficacy. Joint ventures by car manufacturers aim for direct substitutes for mineral oil-based products. Carbon offset initiatives encourage the adoption of ecolubes within fleet use. Emerging countries within Asia Pacific represent uncharted market shares for green products. Research tax incentives catalyze innovation pipelines. These advanced applications are likely to create new opportunities over the coming years.

Market Challenges

Contamination and Performance Risks May Hinder the Market Growth

Aerosol contamination by fuels reduces lubricate effectiveness. Particulate intrusion during MRO degrades it. While bacterial activity in storage tanks is risky, severe environment conditions stress formulation boundaries. Spec integration among different carmakers is a challenge for suppliers.

The need for quality assurance grows with the volume. Public trust is undermined by the counterfeit goods. Such challenges require close attention.

Segmentation Analysis

By Chemistry

Unmatched Chemical Inertness to Fuel the PFPE (Perfluoropolyether) Segmental Growth

Based on chemistry, the market is divided into Mineral (Group I/II/III), synthetic esters, alkylated naphthalenes, silicone fluids, PFPE (Perfluoropolyether), bio-based esters, and water-glycol.

The PFPE (Perfluoropolyether) is estimated to be the fastest growing segment with the highest CAGR of 8.87% during the forecast period. The growth is propelled by unmatched chemical inertness in hypersonic and space vehicle access due to oxidative instability in conventional fluids. Radiation resistance is effectively utilized in actuators in satellites and re-entry systems, securing lucrative defense department orders.

The synthetic esters segment accounts for the largest market share of 58.34% and is set to grow at a CAGR of 4.77% over the analysis period.

By Technology

Harsh Environment Imperatives to Protect the Components to Fuel the Corrosion/Sust Inhibition Systems Segmental Growth

The market, by technology, is divided into antioxidant systems, anti-wear systems, EP (Extreme Pressure) systems, ashless dispersant systems, corrosion/sust inhibition systems, metal deactivators, and others.

The corrosion/sust inhibition systems segment is projected to be the fastest growing with a highest CAGR of 6.94% during the forecast period of 2026-2034. Volatile corrosion inhibitors (VCIs) and contact inhibitors acting as vapor phase inhibitors protect airframes in storage and humid transportation, of prime importance in Asia Pacific monsoon seasons. Nano-encapsulated azoles ensure constant release, penetrating micro-cracks in aluminum alloys with protection cycles of 6 months. There are peak demands with microbial corrosion introduced into BLENdSAF.

The anti-wear systems segment dominated the global market in 2025 with the highest share of 23.05%.

To know how our report can help streamline your business, Speak to Analyst

By Application

Surging Need for Electro-Hydrostatic Actuators to Drive Hydraulic System Segment Growth

The market, by application, is divided into propulsion system, APU Lubrication, propulsion-driven gearboxes, airframe lubrication points, landing gear, hydraulic system, and others.

The hydraulic system segment is estimated to be the fastest growing segment with the highest CAGR of 6.40% during the forecast period. The growth is propelled by the proliferation of Fly-By-Wire in next-generation aircraft that demands less compressible hydraulic fluids with high actuation accuracy in primary flight controls. Electro-hydrostatic actuators decrease plumbing weight by 30%, which exacerbates hydraulic fluid magnitudes in branched networks. Urban air mobility aircraft, such as eVTOLs, utilize redundant hydraulics that open up market opportunities. The higher pricing is due to testing difficulty for zero-leakage performance.

The propulsion system segment dominates the market with a 38.80% share.

By Platform

Mounting Economic Volume Anchor and Fleet Scale Imperative to Cater the Market Growth

Based on platform, the market is subdivided into commercial fixed-wing, business aviation, general aviation, rotorcraft, military fixed-wing, UAV/UAS, and Advanced Air Mobility (AAM).

The UAV/UAS segment is anticipated to be the fastest growing segment with the highest CAGR of 7.58% during the forecast period. The growth is driven by the use of military drone swarms with a strength of over 15,000 and the need for low volatility greases. Logistics webs such as Amazon Prime Air require hydraulic systems that can withstand contaminants to enable autonomous continuous operation and achieve projections of a million hours of flight time.

The commercial fixed wing segment leads the global market with a 54.58% share and is estimated to surge at a CAGR of 5.50% during 2026-2034.

By End User

Operational Scale Leadership and Aftermarket Volume Anchor to Drive the Segmental Growth

Based on end user, the market is subdivided into airlines, military users, MRO providers, and OEMs.

The airlines segment held the largest aviation lubricants market share of 68.42% in 2025. In addition, the segment is projected to emerge as the fastest growing segment with a CAGR of 7.83% during the forecast period of 2026-2034. The growth is fueled by the extensive global air fleet. As per the Emirates Group Annual Report, 90% of worldwide passenger and cargo flights create a constant replenishment cycle for 30,000+ active air travel. Frequent schedules that have averages of 10 cycles/day for a short-haul aircraft create a high demand for fluids for its hydraulics and propulsion systems that have embedded airline-specific fluids through supply contracts.

The MRO providers segment is estimated to be the second fastest growing segment with a CAGR of 6.31% over the forecast period and a market share of 11.26% in 2025.

Aircraft Lubricants Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America.

North America

North America Aircraft Lubricants Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2025, valuing at USD 330.9 million, and is also estimated to maintain the leading share in 2026, with a value of USD 343.7 million. The dominance is due to the presence of major OEM production facilities for aircraft such as Boeing and Pratt & Whitney, where its own fluid requirements are incorporated in 40% of the global market.

U.S. Aviation Lubricants Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 305.9 million in 2025. It is estimated to expand at a CAGR of 4.85% during the forecast period.

Europe

The Europe market is projected to grow at the highest CAGR of 6.43% during the forecast period of 2026-2034. In 2025, the Europe market value stood at USD 224.0 million. European militaries face urgent requirements to upgrade aging Cold War-era fleets amid heightened Russian border threats, driving the rapid adoption of hybrid-electric systems for enhanced stealth and reduced fuel convoys across all regional platform.

U.K. Aviation Lubricants Market

The U.K. market touched a value of around USD 36.4 million in 2025 and is estimated to depict a growth rate of 4.66% during the forecast period of 2026-2034.

Germany Aviation Lubricants Market

The Germany market reached a valuation of around USD 34.0 million in 2025 and is estimated to depict a growth rate of 6.21% during the forecast period of 2026-2034.

Rest of Europe Aviation Lubricants Market

In 2025, the rest of Europe market reached around USD 41.1 million and is estimated to show a growth rate of 3.70% during the forecast period of 2026-2034.

Asia Pacific

Asia Pacific reached a value of USD 177.2 million in 2025 and secured the position of the third-largest region in the market. Indo-Pacific pivot and archipelago logistics ignite multi-domain electrification. Regional doctrines emphasize swarm tactics, with electric UGVs comprising procurements for distributed lethality.

China Aviation Lubricants Market

In 2025, the China market reached around USD 50.8 million and is estimated to depict a growth rate of 6.33% during the forecast period of 2026-2034.

India Aviation Lubricants Market

The India market touched a value of around USD 32.3 million in 2025 and is estimated to show a growth rate of 8.13% during the forecast period of 2026-2034.

Japan Aviation Lubricants Market

The Japan market reached USD 21.6 million in 2025 and is estimated to depict a growth rate of 4.28% during the forecast period of 2026-2034.

Middle East & Africa and Latin America

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market during the forecast period. The Latin America market reached a valuation of USD 18.85 million in 2025. The Middle East & Africa market touched a valuation of USD 121.6 million in 2025.

Brazil Aviation Lubricants Market

The Brazil market reached a value of around USD 8.72 million in 2025 and is estimated to show a growth rate of 1.85% during the forecast period of 2026-2034.

Israel Aviation Lubricants Market

The Israel market reached a value of around USD 15.2 million in 2025 and is estimated to depict a growth rate of 3.22% during the forecast period of 2026-2034.

COMPETITIVE LANDSCAPE

Key Industry Players

OEM-Driven Innovation Surge and Growth Catalysts in Propulsion Shifts to Drive the Market Growth

The global aviation lubricants market has an extremely concentrated competitive environment, wherein differentiation on quality comes solely via rigorous approvals and certifications for future-generation aircraft platforms. Market leaders compete based on parameters of high stability, long oil-change intervals, and low volatility, which are critical for high-bypass turbofan engines and composite aircraft structures, respectively.

Advances by OEMs emphasize the growth opportunities within the market such as fast-track engine development, requiring tailored fluid solutions. Partnerships mainly focus on the bio-synthetic ester candidate for use in geared turbofan engines for unlocking growth opportunities.

List of Key Aircraft Lubricants Companies Profiled

- Shell plc (U.K.)

- Exxon Mobil Corporation (U.S.)

- BP p.l.c. (U.K.)

- TotalEnergies SE (France)

- NYCO S.A. (France)

- Eastman Chemical Company (U.S.)

- LANXESS Corporation (Germany)

- Radco Industries, Inc. (U.S.)

- The Chemours Company FC, LLC (U.S.)

- DuPont de Nemours, Inc. (U.S.)

- Aerospace Lubricants, Inc. (U.S.)

- Eni S.p.A. (Italy)

- China Petroleum & Chemical Corporation (China)

- AVI-OIL India [P] Ltd (India)

- Henkel AG & Co. KGaA (Germany)

KEY INDUSTRY DEVELOPMENTS

- October 2025: ExxonMobil Marine received USD 954 million IDIQ Navy deal to provide global lubricants program supplies, diesel oils, turbine oils, hydraulic fluids, and greases, along with engineering services.

- October 2025: Shell Aviation enhanced partnerships with OEMs for fuel and lubricant blends. These include collaborations with GE, KLM, and Airbus for thermo stable additives and with Boeing for greases.

- September 2025: Avioparts inked multi-year global supply agreement with Avia Solutions Group for ExxonMobil aviation lubricants in Europe, Middle East, Asia, and the Americas.

- September 2025: The U.S. Department of War awarded a contract worth USD 9,863,657 million to Thomas Instrument Inc. This contract involves aviation-related support under the Defense Logistics Agency Aviation at Oklahoma-based Tinker Air Force Base.

- August 2025: 2Excel won 20-year OSRL contract for worldwide oil spill dispersing using their Boeing 737 planes equipped with the TERSUS II system, starting in 2028.

REPORT COVERAGE

The global aircraft lubricants market analysis includes a comprehensive study of the market size and forecast by all the market segments included in the report. It includes details on the market dynamics and global trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, pipeline candidates, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, as well as key industry developments and prevalence by key regions. The global market research report also provides an in-depth competitive landscape with information on the market share and profiles of key players operating in the industry.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2024 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.26% from 2026-2034 |

|

Unit |

USD Million |

|

Segmentation |

By Chemistry · Mineral (Group I/II/III) · Synthetic Esters · Alkylated Naphthalenes · Silicone Fluids · PFPE (Perfluoropolyether) · Bio-based Esters · Water-Glycol By Technology · Antioxidant Systems · Anti-Wear Systems · EP (Extreme Pressure) Systems · Ashless Dispersant Systems · Corrosion/Sust Inhibition Systems · Metal Deactivators · Others By Application · Propulsion System · APU Lubrication · Propulsion-Driven Gearboxes · Airframe Lubrication Points · Landing Gear · Hydraulic System · Others By Platform · Commercial Fixed-Wing · Business Aviation · General Aviation · Rotorcraft · Military Fixed-wing · UAV/UAS · Advanced Air Mobility (AAM) By End User · Airlines · Military Users · MRO Providers · OEMs By Region North America (By Chemistry, By Technology, By Application, By Platform, By End User, By Country) · U.S. (By End User) · Canada (By End User) Europe (By Chemistry, By Technology, By Application, By Platform, By End User, By Country) · U.K. (By End User) · Germany (By End User) · France (By End User) · Nordic Countries (By End User) · Eastern Europe (By End User) · Rest of Europe (By End User) Asia Pacific (By Chemistry, By Technology, By Application, By Platform, By End User, By Country) · China (By End User) · India (By End User) · Japan (By End User) · South Korea (By End User) · Southeast Asia (By End User) · Rest of Asia Pacific (By End User) Middle East & Africa (By Chemistry, By Technology, By Application, By Platform, By End User, By Country) · Gulf Countries (By End User) · Israel (By End User) · Turkey (By End User) · North Africa (By End User) · South Africa (By End User) · Rest of the Middle East & Africa (By End User) Latin America (By Chemistry, By Technology, By Application, By Platform, By End User, By Country) · Brazil (By End User) · Mexico (By End User) · Argentina (By End User) · Rest of Latin America (By End User) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 872.5 million in 2025 and is projected to reach USD 1,372.3 million by 2034.

In 2025, the Europe market value stood at USD 224.0 million.

The market is expected to exhibit a CAGR of 5.26% during the forecast period of 2026-2034.

Based on chemistry, the PFPE (Perfluoropolyether) segment is poised to depict the highest CAGR over the forecast period.

The growing demand for modernization and fleet expansion is a key factor propelling market expansion.

ExxonMobil, Shell, Chevron, TotalEnergies, and BP are the top players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us