Poultry Health & Performance Market Size, Share & Industry Analysis, By Product (Drugs & Vaccines and Performance Additives {Phytogenics, Prebiotics & Probiotics, and Others}), By Animal Type (Broilers, Layers, and Breeders), By Distribution Channel (Animal Farms, Veterinary Clinics & Hospitals, Retail Channels, Online Channels, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

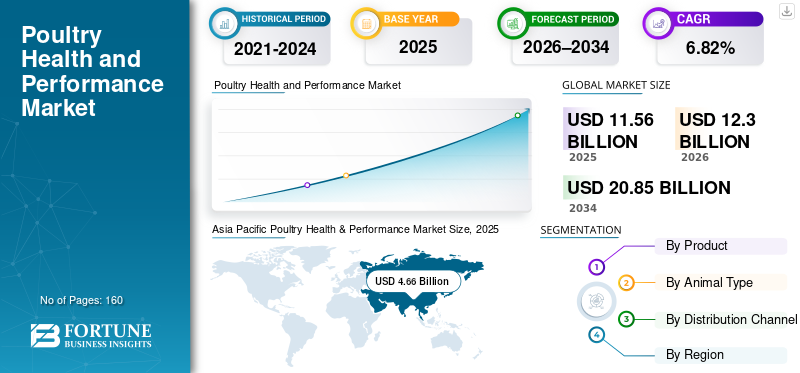

The global poultry health & performance market size was valued at USD 11.56 billion in 2025. The market is projected to grow from USD 12.30 billion in 2026 to USD 20.85 billion by 2034, exhibiting a CAGR of 6.82% during the forecast period. Asia Pacific dominated the poultry health & performance market with a market share of 40.31% in 2025.

The global poultry health & performance market includes products used to control and manage disease and improve the productivity of poultry animals. The global market is projected to grow at a steady rate due to increasing trade prospects owing to rising demand, which is further prone to disease outbreak risks, such as the highly pathogenic avian influenza (HPAI). Moreover, in the recent scenario, there has been an increasing awareness regarding various poultry-centric diseases and the need to prevent them, such as infectious bursal disease (IBD), Marek's disease, coccidiosis, Newcastle disease, and avian influenza. Furthermore, several market players have been engaged in innovative vaccine development, which is further supported by government-led initiatives to improve poultry health.

- For instance, in February 2025, the USDA announced an investment of up to USD 1 billion for the development of a detailed strategy to eliminate occurrences of the highly pathogenic avian influenza (HPAI), lowering of the egg prices in the U.S. The heightened protection of the poultry business in the U.S. Such initiatives are to support the market growth through the increased adoption of offerings such as drugs, vaccines and performance additives.

Also, numerous animal health companies such as Boehringer Ingelheim International GmbH, Merck & Co., Inc., Ceva, and others comprise the key players of the market. These companies are engaged in innovative product launches, coupled with strategic initiatives such as expansion of their manufacturing capacities to bolster their global market shares.

Download Free sample to learn more about this report.

Poultry Health & Performance Market Key Takeaways

- 2025 Market Size: USD 11.56 Billion

- 2026 Market Size: USD 12.30 Billion

- 2034 Forecast Market Size: USD 20.85 Billion

- CAGR: 6.82% from 2026–2034

- Asia Pacific dominated the poultry health & performance market with a 40.31% share in 2025.

- The performance additives segment is anticipated to grow at a CAGR of 7.29% during the forecast period.

- The layers segment is projected to grow at a CAGR of 6.42% during the forecast period.

Asia Pacific

Asia Pacific was the largest regional market, reaching a valuation of USD 4.66 billion in 2025.

North America

North America maintained a strong market position with a value of USD 2.01 billion in 2025.

Europe

Europe is projected to reach USD 2.61 billion by 2026, growing at a CAGR of 5.49%.

U.S.

The market is analytically approximated to reach around USD 1.78 billion in 2026.

Japan

The poultry health & performance market was estimated at around USD 0.24 billion in 2025.

Read More

POULTRY HEALTH & PERFORMANCE MARKET TRENDS

Increasing Emphasis on Hatchery Delivered Vaccination is a Key Market Trend

Some of the emerging essential trends witnessed in the global market are the increasing trend of vaccination of poultry birds in settings such as hatcheries. Some of the types of vaccines that are administered in these settings include vector vaccines and combination products. This is a positive emerging trend as it reduces field labor, improves protection, and delivers critical protection at an earlier stage for the birds. This practice of providing expeditious vaccination is particularly valuable in broilers, which typically have short cycles. Furthermore, administration of combination vaccines is helpful as it allows for protection against multiple diseases and also involves lower handling stress.

- For instance, in February 2025, Boehringer Ingelheim announced the launch of its new trivalent vaccine called the VAXXITEK HVT+IBD+H5, which offers vaccination against multiple diseases such as Infectious Bursal Disease, Marek’s disease, and H5 avian influenza. This vaccine is developed to be administered at the hatcheries.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Strong Product Adoption Due to Risk of Disease Outbreaks to Drive Market Growth

Some of the driving factors that will contribute to the considerable market growth across the forecast period are the risk that HPAI will become endemic across the region. If the cases of HPAI outbreaks increase across the globe, poultry suppliers potentially face the dangers of pricing volatilities, egg/meat supply shocks, and increases in export restrictions. Hence, such risks lead to the considerable allocation of funding towards vaccines, surveillance, and biosecurity. Also, many poultry manufacturers are exploring other means of improving their productivity, such as gut-health/performance programs to eliminate stress susceptibility and secondary losses. Such factors together drive the poultry health & performance market growth across the forecast period.

- For instance, in April 2025, Evonik showcased and debuted its poultry probiotic product, Ecobiol, at the China Feed Industry Expo 2025. This is the first ever registered feed-grade probiotic in China and considerably improves the feed conversion, reduces mortality in birds, and improves animal performance.

MARKET RESTRAINTS

Regulatory Complexities and Cost Sensitivities to Hinder Market Growth

The regulatory restraints associated with key product categories, such as vaccines, hinder the market growth rate. For example, in terms of animal vaccines, the regulations differ across several countries, leading to an uneven launch scenario, resulting in lower market adoption of key products. Another critical limiting parameter in this market includes the lack of ability to pay for the products with technological advancements which often carry premium costs attached to them. The large integrators may be able to afford them, but the smaller, fragmented farms usually are not. They prioritize immediate cash cost over longer-term performance return on investment ROI. This further restrains the greater market growth prospects for these offerings.

- For instance, in February 2025, during the launch of Boehringer Ingelheim’s vaccine of VAXXITEK HVT+IBD+H5, the company explicitly noted that there are country-to-country differences in vaccine regulations, highlighting the regulatory fragmentation.

MARKET OPPORTUNITIES

Development of Next Generation Vaccines Platforms to Provide Opportunities for the Market

As an efficient process of poultry manufacturing becomes critical for the global supply chain driven by consumer demand, and also the number of disease outbreaks increases, many vaccine manufacturers are focusing on the development of advanced vaccine platforms. Hence, there is a growing opportunity for manufacturers to scale new vaccine platforms such as vector animal vaccines, genetic vaccines, etc. This also allows various government and industry bodies to align on vaccination guidelines and surveillance frameworks, significantly increasing trade confidence. This substantially increases the addressable demand for vaccinations, programs, and monitoring services.

- For instance, in January 2025, Ceva Animal Health and Touchlight signed an agreement, with Ceva being granted rights to develop and manufacture innovative animal health products, including vaccines, using Touchlight’s dbDNA technology.

MARKET CHALLENGES

Outbreaks of Diseases and Biological Complexities in Poultry Animals to Disrupt Growth Prospects

Some of the significant challenges associated with the poultry health & performance market are the outbreaks of poultry diseases such as HPAI, leading to the disruption of production planning and causing trade bans. Such outbreaks divert the funds towards the mitigation of the financial impact of outbreaks, reducing the working capital of manufacturers to procure advanced vaccines and therapeutics. Also, the poultry birds are subject to biological complexities; hence, the results of performance additives are not similar across all birds or farms. Performance outcomes are often factor-based on parameters such as feed quality, mycotoxins, litter, genetics, and pathogen load. Hence, this makes the return on investment (ROI) variable across all farms and seasons, and companies often have to prove their products’ efficacy to gain suitable adoption for their products as they compete against cheaper alternatives.

- For instance, in May 2025, Brazil declared an outbreak of avian flu, which impacted a considerable number of birds. In response, the country’s several major trading partners, such as the European Union, China, and Canada, suspended imports of poultry from the region.

Segmentation Analysis

By Product

Robust Adoption of Drugs & Vaccines for Management of Various Outbreaks to Boost Segmental Dominance

On the basis of the product, the market is segmented into drugs & vaccines, and performance additives. The performance additives segment is further sub-segmented into phytogenics, prebiotics & probiotics, and others.

As of product, the drugs & vaccines segment is projected to account for the dominant poultry health & performance market share. The segment’s dominating market share is owing to the fact that drugs and vaccines are considerably used, and are often not an optional expenditure for the animal farms. The process of vaccination is usually standardized and regulated at the level of hatcheries, and drugs remain critical when approved for coccidiosis/enteric control.

- For instance, in July 2025, the U.S. FDA approved Exzolt (fluralaner), the first oral product for the treatment and control of northern fowl mites in laying hens and replacement chickens.

The performance additives segment is anticipated to rise with a CAGR of 7.29% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Animal Type

Owing to Largest Production of Broilers Leads to Segmental Dominance

On the basis of animal type, the market is segmented into broilers, layers, and breeders.

In 2025, the broilers segment accounted for the largest revenue share of the global market. This segment’s dominance is primarily due to the reason that the broilers have the largest production throughput, and even a small impact on their productivity impacts massive volumes of birds. Hence, that alone drives the large scale of poultry vaccination and the high inclusion of performance additives.

- For instance, in November 2024, Ceva Animal Health, a leader in broiler vaccination, announced an investment in a new 7,000 m2 plant in Monor, Hungary.

The layers segment is projected to grow at a CAGR of 6.42% over the forecast period.

By Distribution Channel

Integrators and Large Farms Control the Process and Protocols Leads to Animal Farms Segmental Growth

In terms of distribution channel, the market is segmented into animal farms, veterinary clinics & hospitals, retail channels, online channels, and others.

The segment of animal farms accounted for the largest global poultry health & performance market share. The animal farms held a significant proportion of the market value as integrators, and large farms control the procurement process and protocols. They also negotiate the direct contracts for vaccines and set standards for the performance additives. Moreover, the segment is set to hold a 36.03% share in 2026.

- For instance, in a February 2026 note published by the USDA, it was noted that the agency conducts a substantial proportion of the biosecurity assessments in commercial facilities in the highest egg-producing states across the U.S. This reflects where the value and volume scales are concentrated.

Moreover, the online channels segment is projected to grow at a CAGR of 12.50% across the forecast period.

Poultry Health & Performance Market Regional Outlook

In terms of region, the market is categorized into North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

North America

Asia Pacific Poultry Health & Performance Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held a significant value in 2024, valued at USD 1.91 billion, and also maintained a considerable value in 2025, with USD 2.01 billion. The market in North America is projected to grow significantly across the forecast period, owing to North America being one of the largest consumers of poultry health & performance products across the globe. The recurrence of HPAI outbreaks, the need for control on egg pricing, and the demand for products that improve gut integrity and reduce pathogen load are expected to drive the region’s growth.

U.S. Poultry Health & Performance Market

Based on North America’s regional dominance and the U.S.’ largest share within the region, the U.S. market can be analytically approximated at around USD 1.78 billion in 2026, accounting for roughly 14.4% of global sales.

Europe

Europe is on track to record a growth rate of 5.49% in the coming years and reach a valuation of USD 2.61 billion by 2026. Some of the parameters to the region’s strong market share include the firm adherence to regulatory norms, which classifies this region as a high-regulation, high-standard poultry market with strong retailer-driven requirements. Furthermore, the production in the region has been on an increasing trajectory in recent years.

U.K. Poultry Health & Performance Market

The U.K. market in 2025 is estimated at around USD 0.21 billion, representing roughly 1.8% of global poultry health & performance revenues.

Germany Poultry Health & Performance Market

Germany’s market is projected to reach approximately USD 0.28 billion in 2025, equivalent to around 2.5% of global poultry health & performance sales.

Asia Pacific

The Asia Pacific is estimated to reach USD 4.66 billion in 2025 and secure the position of the largest region in the market. In the region, India and China are both estimated to reach USD 0.65 billion and USD 1.37 billion, respectively, in 2025.

Japan Poultry Health & Performance Market

The Japanese market in 2025 is estimated at around USD 0.24 billion, accounting for roughly 2.0% of the global revenues. Japan has a steady share in the global market owing to the repeated incidences of disease outbreaks, tight biosecurity, and strong official veterinary oversight.

China Poultry Health & Performance Market

China’s market is projected to be one of the largest worldwide, with 2025 revenues estimated at around USD 1.37 billion, representing roughly 11.9% of global poultry health & performance sales.

India Poultry Health & Performance Market

The Indian market in 2025 is estimated at around USD 0.65 billion, accounting for roughly 5.6% of global poultry health & performance revenues.

South America, and the Middle East & Africa

The South America, Middle East, and Africa regions are expected to witness considerable growth rates in this market space during the forecast period. The South America market is set to reach a valuation of USD 1.20 billion in 2025. Brazil is heavily influenced by export competitiveness, and disease events and trade import restrictions create strong incentives for vaccination, biosecurity, and performance consistency. In the Middle East, Saudi Arabia is set to reach USD 0.19 billion in 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

Diverse Product Portfolio Breadth Coupled with Wide Geographical Reach to Enable Dominance of Major Companies

The global poultry health & performance market comprises of a semi-fragmented competitive landscape, including key companies such as Boehringer Ingelheim International GmbH, Merck & Co., Inc., Ceva and others. The significant company revenue share possessed by these companies is attributable to their strong product portfolio, robust regulatory approvals, and focus on increasing market presence through capacity expansions. Furthermore, these players are also engaged in several research initiatives for the development of innovative products, including vaccines.

- For instance, in February 2025, Boehringer Ingelheim announced the launch of its new trivalent poultry vaccine called the VAXXITEK HVT+IBD+H5 in the Egyptian market.

Other major companies present in the global market include Zoetis Services LLC, Elanco, Phibro Animal Health Corporation, Novozymes A/S, and others. These companies have several offerings in their product portfolio, including performance additives and a wide geographical presence, which support their strong market share across the forecast period.

LIST OF KEY POULTRY HEALTH & PERFORMANCE COMPANIES PROFILED

- Boehringer Ingelheim International GmbH (Germany)

- Merck & Co., Inc. (U.S.)

- Ceva (France)

- Zoetis Services LLC (U.S.)

- Elanco (U.S.)

- Phibro Animal Health Corporation (U.S.)

- Novozymes A/S (Denmark)

- dsm-firmenich (Switzerland)

- Cargill, Incorporated (U.S.)

- Danisco Animal Health & Nutrition (IFF) (Denmark)

KEY INDUSTRY DEVELOPMENTS

- August 2025: DSM-Firmenich Animal Nutrition and Health received the Canadian Food Inspection Agency (CFIA) approval of a novel enzyme, fumonisin esterase, to help swine and poultry producers manage mycotoxins in feed.

- July 2025: Proteon Pharmaceuticals announced the European approval for BAFASAL, a pioneering bacteriophage-based feed additive for use in poultry.

- March 2025: MSD Animal Health announced the European approval of NOBILIS MULTRIVA REOm for use in chickens.

- October 2024: Ceva Animal Health announced the opening of its new European distribution logistics platform in France.

- April 2024: Zoetis Inc. and Phibro Animal Health Corporation announced an agreement where Phibro Animal Health acquired Zoetis’ medicated feed additive (MFA) product portfolio, certain water-soluble products, and related assets for USD 350.0 million

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 6.82% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product, Animal Type, Distribution Channel, and Region |

| By Product |

· Drugs & Vaccines · Performance Additives o Phytogenics o Prebiotics & Probiotics o Others |

| By Animal Type |

· Broilers · Layers · Breeders |

| By Distribution Channel |

· Animal Farms · Veterinary Clinics & Hospitals · Retail Channels · Online Channels · Others |

| By Region |

· North America (By Product, Animal Type, Distribution Channel, and Country) o U.S. o Canada o Mexico · Europe (By Product, Animal Type, Distribution Channel, and Country/Sub-Region) o U.K. o Germany o France o Italy o Spain o Poland o The Netherlands o Russia o Rest of Europe · Asia Pacific (By Product, Animal Type, Distribution Channel, and Country/Sub-Region) o China o India o Japan o Australia o Indonesia o Vietnam o Bangladesh o South Korea o Rest of Asia Pacific · South America (By Product, Animal Type, Distribution Channel, and Country/Sub-Region) o Brazil o Argentina o Chile o Peru o Rest of South America · Middle East (By Product, Animal Type, Distribution Channel, and Country/Sub-Region) o Saudi Arabia o UAE o Israel o Turkey o Egypt o Qatar o Kuwait o Rest of the Middle East

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 11.56 billion in 2025 and is projected to reach USD 20.85 billion by 2034.

In 2025, Asia Pacifics market value stood at USD 4.66 billion.

The market is expected to exhibit a CAGR of 6.82% during the forecast period of 2026-2034.

By product, the drugs & vaccines segment is expected to lead the market.

Risks of disease outbreaks, prompting product adoption, a strong poultry population, and innovative product launches are driving the market expansion.

Boehringer Ingelheim International GmbH, Merck & Co., Inc., and Ceva are the major players in the global market.

Asia Pacific dominated the market in 2025 by holding the largest share.

- 2021-2034

- 2025

- 2021-2024

- 160

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us